LAW300 Taxation Law Assignment: Income Tax and Regulatory Measures

VerifiedAdded on 2022/08/21

|12

|2759

|18

Homework Assignment

AI Summary

This assignment solution addresses a taxation law problem, analyzing income tax, deductions, and the Australian Taxation Office (ATO) regulations. Part A examines income from personal exertion and business, determining assessable income and allowable deductions for Zara and the Smartmans' business, including specific deductions for tax return expenses. It applies relevant sections of the ITAA 1936 and 1997, and case law such as McNeil v FCT and Mansfield v FCT. Part B explores the ATO's IT and regulatory measures, including MyTax, end-to-end solutions, and activity-based compliance. It also discusses policy responses to challenges presented by emerging technologies and the need for reliable data to improve automation and reduce taxpayer compliance burden. The solution provides a detailed computation of Zara's tax liability and discusses the importance of technology and regulatory measures in taxation.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to Requirement (i):....................................................................................................2

Answer to requirement (ii):....................................................................................................4

Answer to Part B:.......................................................................................................................5

Answer to requirement (i):.....................................................................................................5

Answer to requirement (ii):....................................................................................................7

References:.................................................................................................................................9

Table of Contents

Answer to Part A:.......................................................................................................................2

Answer to Requirement (i):....................................................................................................2

Answer to requirement (ii):....................................................................................................4

Answer to Part B:.......................................................................................................................5

Answer to requirement (i):.....................................................................................................5

Answer to requirement (ii):....................................................................................................7

References:.................................................................................................................................9

2TAXATION LAW

Answer to Part A:

Answer to Requirement (i):

Income obtained from personal exertion is explained under the “sec 6 (1) ITAA

1936”, and it is not put into use anywhere else in the Act (Woellner et al. 2016). When a

taxpayer earns income from salary, wages, bonus, fees, commissions etc. or any proceeds

from the business falls within the head of “sec 6 (1) ITAA 1936”.. The law court in the

“McNeil v FCT (2007)” explained that whether or not an amount can be classified as income

it is mainly reliant on the quality in the recipients hands and not based on the character of

expenses occurred by other party. Under “sec 6-5 ITAA 1997”, the assessable income

comprises of ordinary earnings under the ordinary concepts.

The case study provides that Zara is employed with American Express in Sydney and

reports the receipt of gross salary that amounted to $225,000. As defined in “sec 6 (1) ITAA

1936”, the gross salary that is received by Sara amounts to income from personal exertion

(Sadiq 2019). Referring to “McNeil v FCT (2007)” the gross salary will be considered

taxable as ordinary income under the “section 6-5 ITAA 1997”.

As explained in “sec 8-1 (1)” a tax payer is permitted to get deduction from their

taxable earnings for any kind of loss or expenses till the extent that it is occurred in earning

taxable earnings or the expenses that are occurred necessarily in conducting the business with

the motive of earning income (Barkoczy 2016). While the negative limb of “sec 8-1 (2)” says

that a person is not permitted to get deduction if the expenses are capital in nature or private

or domestic in type. The taxpayers are required to denote that costs that is occurred in the

ordinary articles of clothing such as suits is not allowed deduction. The decision given in

“Mansfield v FCT (1996)” explained that usually outgoings that is occurred on ordinary

Answer to Part A:

Answer to Requirement (i):

Income obtained from personal exertion is explained under the “sec 6 (1) ITAA

1936”, and it is not put into use anywhere else in the Act (Woellner et al. 2016). When a

taxpayer earns income from salary, wages, bonus, fees, commissions etc. or any proceeds

from the business falls within the head of “sec 6 (1) ITAA 1936”.. The law court in the

“McNeil v FCT (2007)” explained that whether or not an amount can be classified as income

it is mainly reliant on the quality in the recipients hands and not based on the character of

expenses occurred by other party. Under “sec 6-5 ITAA 1997”, the assessable income

comprises of ordinary earnings under the ordinary concepts.

The case study provides that Zara is employed with American Express in Sydney and

reports the receipt of gross salary that amounted to $225,000. As defined in “sec 6 (1) ITAA

1936”, the gross salary that is received by Sara amounts to income from personal exertion

(Sadiq 2019). Referring to “McNeil v FCT (2007)” the gross salary will be considered

taxable as ordinary income under the “section 6-5 ITAA 1997”.

As explained in “sec 8-1 (1)” a tax payer is permitted to get deduction from their

taxable earnings for any kind of loss or expenses till the extent that it is occurred in earning

taxable earnings or the expenses that are occurred necessarily in conducting the business with

the motive of earning income (Barkoczy 2016). While the negative limb of “sec 8-1 (2)” says

that a person is not permitted to get deduction if the expenses are capital in nature or private

or domestic in type. The taxpayers are required to denote that costs that is occurred in the

ordinary articles of clothing such as suits is not allowed deduction. The decision given in

“Mansfield v FCT (1996)” explained that usually outgoings that is occurred on ordinary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

clothing articles would not be allowed for deduction, irrespective that such kind of outgoings

is important to assure that a suitable appearance is maintained in a specific job or profession.

Sara during the year occurred expenses on dresses, jewellery and personal fitness.

Referring to factual decision made in “Mansfield v FCT (1996)” it can be stated that Zara is

not allowed to claim deduction for the expenses on dresses, jewellery and personal fitness

because it is a private expense under “sec 8-1 (2)” and it is not permitted for deduction

(Taylor et al. 2017). The expenses are not related to derivation of assessable income and

hence it is not relevant in the derivation of the taxable income.

As stated by the ATO, an individual is allowed to claim deduction for the cost that is

occurred in attending the seminars, education, conferences and educational workshops which

is related to the taxpayer’s work related activity. There may be circumstances where the

taxpayer may occur for expenses for meals, accommodation, incidentals at the time of

travelling away for overnight work. The examples include the interstate work related

conferences.

As evident in case of Zara she reported expenses on interstate travel that included air

ticket, food and transportation of $20,000. The expenses will be allowed for deduction under

the general provision of “section 8-1 ITAA 1997”, because the expenses are relevant in the

derivation of taxable income (Morgan, Mortimer and Pinto 2018). Furthermore, Zara also

reported attending an international IT conference and occurred expenses on conference fees,

air ticket and food & accommodation. Zara within “sec 8-1 ITAA 1997”, is allowed to obtain

deduction for conference, air tickets and accommodation because it is adequately related to

her work activities. These expense are directly related to her income producing activities.

Gains that amounts to simple prize winnings are not held as income under the

ordinary concept of “sec 6-5 ITAA 1997” (Keyzer, Goff and Fisher 2017). As held in the

clothing articles would not be allowed for deduction, irrespective that such kind of outgoings

is important to assure that a suitable appearance is maintained in a specific job or profession.

Sara during the year occurred expenses on dresses, jewellery and personal fitness.

Referring to factual decision made in “Mansfield v FCT (1996)” it can be stated that Zara is

not allowed to claim deduction for the expenses on dresses, jewellery and personal fitness

because it is a private expense under “sec 8-1 (2)” and it is not permitted for deduction

(Taylor et al. 2017). The expenses are not related to derivation of assessable income and

hence it is not relevant in the derivation of the taxable income.

As stated by the ATO, an individual is allowed to claim deduction for the cost that is

occurred in attending the seminars, education, conferences and educational workshops which

is related to the taxpayer’s work related activity. There may be circumstances where the

taxpayer may occur for expenses for meals, accommodation, incidentals at the time of

travelling away for overnight work. The examples include the interstate work related

conferences.

As evident in case of Zara she reported expenses on interstate travel that included air

ticket, food and transportation of $20,000. The expenses will be allowed for deduction under

the general provision of “section 8-1 ITAA 1997”, because the expenses are relevant in the

derivation of taxable income (Morgan, Mortimer and Pinto 2018). Furthermore, Zara also

reported attending an international IT conference and occurred expenses on conference fees,

air ticket and food & accommodation. Zara within “sec 8-1 ITAA 1997”, is allowed to obtain

deduction for conference, air tickets and accommodation because it is adequately related to

her work activities. These expense are directly related to her income producing activities.

Gains that amounts to simple prize winnings are not held as income under the

ordinary concept of “sec 6-5 ITAA 1997” (Keyzer, Goff and Fisher 2017). As held in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

case of “Moore v Griffiths (1972)” winning any simple prize is not held as income. Zara

during the year won a first prize of Rolex that worth $35,000 in a lucky draw conference. The

amount will not be classified as income because it is a simple prize winnings and does not

relates to any derivation of assessable income.

The definition of business is given in “sec 995-1” comprises of any profession, trade,

employment vocation and calling but do not take into account the employees engaged in

occupation (Robin and Barkoczy 2020). The proceeds that are earned from business are held

as taxable ordinary income under “sec 6-5” and the outgoings occurred for while carrying out

the business are allowed for deduction under “sec 8-1 ITAA 1997”.

In the later part of the case both Mr and Mrs Smartman has opened a home-based

business for developing and marketing a comprehensive computer software. During the year

ended 30th June 2020 the business reported an income of $80,000 while the total expenses

occurred stood $40,000. The proceeds derived from business will be included in her taxable

income as ordinary business gains and will be held assessable under the “sec 6-5 ITAA

1997” (Freudenberg et al. 2017). While the business expenses will be allowed for deduction

within “sec 8-1 ITAA 1997” because the expenses occurred in conducting business activities.

Commonly, a specific deduction happens when the specific provision under the

income tax legislation allows taxpayer with a deduction. As given in the “sec 25-5” taxpayers

are given deduction for specific types of expenses occurred in managing their tax affairs

(Butler 2019). As evident in case of Zara, for the year ended 30th June 2020 reported tax

return expenses for her business and lodgement of personal tax return. Zara will be allowed a

specific deduction under “sec 25-5 ITAA 1997” for the expenses occurred on managing tax

affairs.

case of “Moore v Griffiths (1972)” winning any simple prize is not held as income. Zara

during the year won a first prize of Rolex that worth $35,000 in a lucky draw conference. The

amount will not be classified as income because it is a simple prize winnings and does not

relates to any derivation of assessable income.

The definition of business is given in “sec 995-1” comprises of any profession, trade,

employment vocation and calling but do not take into account the employees engaged in

occupation (Robin and Barkoczy 2020). The proceeds that are earned from business are held

as taxable ordinary income under “sec 6-5” and the outgoings occurred for while carrying out

the business are allowed for deduction under “sec 8-1 ITAA 1997”.

In the later part of the case both Mr and Mrs Smartman has opened a home-based

business for developing and marketing a comprehensive computer software. During the year

ended 30th June 2020 the business reported an income of $80,000 while the total expenses

occurred stood $40,000. The proceeds derived from business will be included in her taxable

income as ordinary business gains and will be held assessable under the “sec 6-5 ITAA

1997” (Freudenberg et al. 2017). While the business expenses will be allowed for deduction

within “sec 8-1 ITAA 1997” because the expenses occurred in conducting business activities.

Commonly, a specific deduction happens when the specific provision under the

income tax legislation allows taxpayer with a deduction. As given in the “sec 25-5” taxpayers

are given deduction for specific types of expenses occurred in managing their tax affairs

(Butler 2019). As evident in case of Zara, for the year ended 30th June 2020 reported tax

return expenses for her business and lodgement of personal tax return. Zara will be allowed a

specific deduction under “sec 25-5 ITAA 1997” for the expenses occurred on managing tax

affairs.

5TAXATION LAW

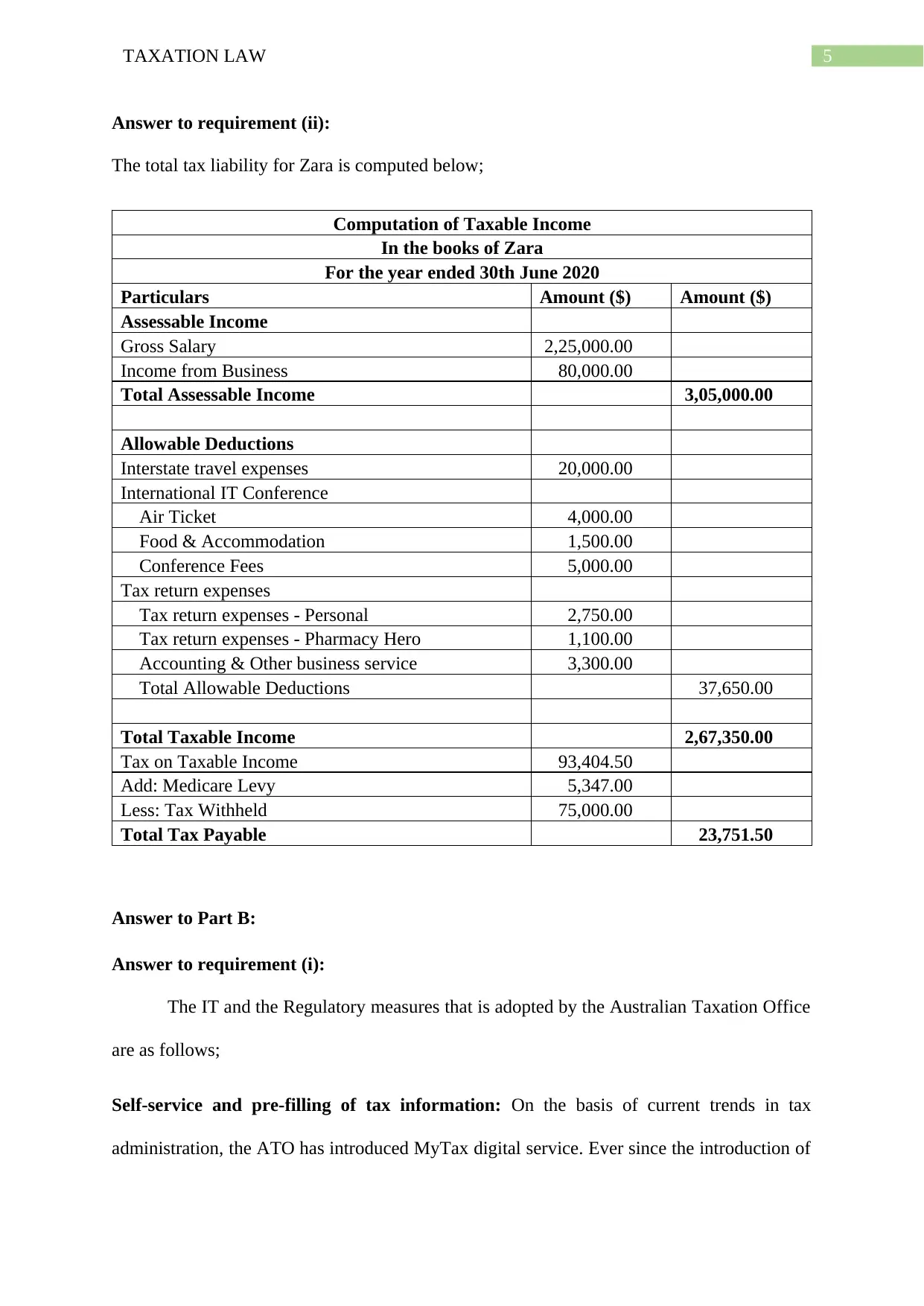

Answer to requirement (ii):

The total tax liability for Zara is computed below;

Computation of Taxable Income

In the books of Zara

For the year ended 30th June 2020

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 2,25,000.00

Income from Business 80,000.00

Total Assessable Income 3,05,000.00

Allowable Deductions

Interstate travel expenses 20,000.00

International IT Conference

Air Ticket 4,000.00

Food & Accommodation 1,500.00

Conference Fees 5,000.00

Tax return expenses

Tax return expenses - Personal 2,750.00

Tax return expenses - Pharmacy Hero 1,100.00

Accounting & Other business service 3,300.00

Total Allowable Deductions 37,650.00

Total Taxable Income 2,67,350.00

Tax on Taxable Income 93,404.50

Add: Medicare Levy 5,347.00

Less: Tax Withheld 75,000.00

Total Tax Payable 23,751.50

Answer to Part B:

Answer to requirement (i):

The IT and the Regulatory measures that is adopted by the Australian Taxation Office

are as follows;

Self-service and pre-filling of tax information: On the basis of current trends in tax

administration, the ATO has introduced MyTax digital service. Ever since the introduction of

Answer to requirement (ii):

The total tax liability for Zara is computed below;

Computation of Taxable Income

In the books of Zara

For the year ended 30th June 2020

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 2,25,000.00

Income from Business 80,000.00

Total Assessable Income 3,05,000.00

Allowable Deductions

Interstate travel expenses 20,000.00

International IT Conference

Air Ticket 4,000.00

Food & Accommodation 1,500.00

Conference Fees 5,000.00

Tax return expenses

Tax return expenses - Personal 2,750.00

Tax return expenses - Pharmacy Hero 1,100.00

Accounting & Other business service 3,300.00

Total Allowable Deductions 37,650.00

Total Taxable Income 2,67,350.00

Tax on Taxable Income 93,404.50

Add: Medicare Levy 5,347.00

Less: Tax Withheld 75,000.00

Total Tax Payable 23,751.50

Answer to Part B:

Answer to requirement (i):

The IT and the Regulatory measures that is adopted by the Australian Taxation Office

are as follows;

Self-service and pre-filling of tax information: On the basis of current trends in tax

administration, the ATO has introduced MyTax digital service. Ever since the introduction of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

the MyTax it is projected that the system has successfully delivered a reduction in the

compliance cost for the individual tax payers of approximately $285 million each year. By

the year April more than $3.2 individual tax returns have been filed by making use of mytax.

It is commonly available in many devices and it is very convenient for the taxpayer. For the

Australian taxation office the return on investment happens based on the fact that the

taxpayers are more likely to be voluntarily adhere with the obligations of tax when doing the

work in quick and easy manner (Main 2019). Taxpayers that are using the my tax also have

the access to the pre-filing services which makes it easy to make sure that they have not

omitted the income such as the salary and wages or dividend and interest.

The study reveals that in spite of the advances the online tax returns for individuals

has been lagging behind. Whereas the electronic lodgement was high for the business but

only two third of the individuals taxpayers that lodge online (Van Brederode 2019). As per

the tax administrators it is estimated that attaining the higher use of electronic lodgement and

payment system will help in reducing the costs and improving the service to the taxpayers.

The most significant innovation in this respect involves the provision of pre-filled tax

information for the individual tax payers.

End to end solutions:

The latest innovation involves the modern tax administration ecosystem which

involves several partners in public and private sector along with the taxpayers themselves.

This has allowed the tax administration at ATO to submit an advice regarding the

effectiveness that the end to end solution is integrated into the natural system that these

products affords both the agency and businesses.

An important significant improvement that has happened for the business that has

employers is the super stream that has streamlined the procedure of paying the

the MyTax it is projected that the system has successfully delivered a reduction in the

compliance cost for the individual tax payers of approximately $285 million each year. By

the year April more than $3.2 individual tax returns have been filed by making use of mytax.

It is commonly available in many devices and it is very convenient for the taxpayer. For the

Australian taxation office the return on investment happens based on the fact that the

taxpayers are more likely to be voluntarily adhere with the obligations of tax when doing the

work in quick and easy manner (Main 2019). Taxpayers that are using the my tax also have

the access to the pre-filing services which makes it easy to make sure that they have not

omitted the income such as the salary and wages or dividend and interest.

The study reveals that in spite of the advances the online tax returns for individuals

has been lagging behind. Whereas the electronic lodgement was high for the business but

only two third of the individuals taxpayers that lodge online (Van Brederode 2019). As per

the tax administrators it is estimated that attaining the higher use of electronic lodgement and

payment system will help in reducing the costs and improving the service to the taxpayers.

The most significant innovation in this respect involves the provision of pre-filled tax

information for the individual tax payers.

End to end solutions:

The latest innovation involves the modern tax administration ecosystem which

involves several partners in public and private sector along with the taxpayers themselves.

This has allowed the tax administration at ATO to submit an advice regarding the

effectiveness that the end to end solution is integrated into the natural system that these

products affords both the agency and businesses.

An important significant improvement that has happened for the business that has

employers is the super stream that has streamlined the procedure of paying the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

superannuation contribution for employees (Hum et al. 2019). This has enabled them to use

the single channel for paying multiple funds. It is anticipated to render savings to the

employers of around $350 million per year. The single touch payroll system would

additionally streamline and automate the obligations for reporting for employers through their

regular payroll events. From the perspective of technology, an ecosystem is built around the

core accounting system. With Xero being an international accounting platform, the

innovation provides effective horizontal accounting regime which is integrated through the

ATO if some is a tax agent. Besides this, it is also thriving the ecosystem of industry through

specific vertical applications.

Regulatory measures taken by ATO:

Activity based evidence and metrics: The ATO has introduced activity based proportionate

approach for compliance obligations, indulgence and regulatory enforcement actions. The

ATO has introduced the risk management policies and process that comprises of qualitative

assessment of the policies and process place and compliance by the ATO staff (Bankman et

al. 2018). The compliance as well as enforcement strategies are consistent with the policies

and procedures of ATO which includes qualitative assessment of communication with the

help of compliance and strategies of enforcement.

Base monitoring and inspection: Base monitoring and inspection approaches on the risk has

been adopted by the ATO wherever possible in order to consider the circumstances and

operational requirements of the taxpayers (Oishi, Kushlev and Schimmack 2018). The

qualitative reporting assessment comprises of the monitoring and enforcement of strategies

that is adopted for drawing the commissioner’s discretion to the application of penalties.

superannuation contribution for employees (Hum et al. 2019). This has enabled them to use

the single channel for paying multiple funds. It is anticipated to render savings to the

employers of around $350 million per year. The single touch payroll system would

additionally streamline and automate the obligations for reporting for employers through their

regular payroll events. From the perspective of technology, an ecosystem is built around the

core accounting system. With Xero being an international accounting platform, the

innovation provides effective horizontal accounting regime which is integrated through the

ATO if some is a tax agent. Besides this, it is also thriving the ecosystem of industry through

specific vertical applications.

Regulatory measures taken by ATO:

Activity based evidence and metrics: The ATO has introduced activity based proportionate

approach for compliance obligations, indulgence and regulatory enforcement actions. The

ATO has introduced the risk management policies and process that comprises of qualitative

assessment of the policies and process place and compliance by the ATO staff (Bankman et

al. 2018). The compliance as well as enforcement strategies are consistent with the policies

and procedures of ATO which includes qualitative assessment of communication with the

help of compliance and strategies of enforcement.

Base monitoring and inspection: Base monitoring and inspection approaches on the risk has

been adopted by the ATO wherever possible in order to consider the circumstances and

operational requirements of the taxpayers (Oishi, Kushlev and Schimmack 2018). The

qualitative reporting assessment comprises of the monitoring and enforcement of strategies

that is adopted for drawing the commissioner’s discretion to the application of penalties.

8TAXATION LAW

Answer to requirement (ii):

To address holistically the certain types of opportunities and challenges that is

presented by emerging technologies and regulatory measures, a policy response along with

the administrative measures may be needed. The stakeholders have acknowledge that the

quick technological advancement and regulatory measures have resulted in several changes

which includes newer working patterns in gig or sharing economy. According to the

stakeholders, it is believed that the ATO and the government must have the systematic

approach in place in order as well as respond to the technological developments and

innovations (Woellner et al. 2016). The stakeholders have also cited their opinion that

making use of emerging technology and new regulatory changes would help in increasing the

automation inside the taxation system, however there is a significant need for more reliable

data.

The data must be obtained by the third parties such banks, whose burden of

compliance would increase correspondingly. The advantage of availability of large amount of

reliable data to government and its agencies, particularly the ATO involves greater

efficiencies and lower costs. The compliance of the taxpayers is also reduced with the help of

such kind of initiatives and brings improvement to pre-filled returns. The stakeholders have

expressed their views that there are restrictions to the degree of automation which can be

attained within the Australian taxation system largely due to the complexity and features such

as the work related expense deductions.

The stakeholders have also observed that the DTA offers wide range of guidance to

those agencies that are seeking to modernize the manner in which the taxpayers interact with

the government with the help of online service which is considered effective and cost

effective. The stakeholders believe that which are adopting the different platforms results in

Answer to requirement (ii):

To address holistically the certain types of opportunities and challenges that is

presented by emerging technologies and regulatory measures, a policy response along with

the administrative measures may be needed. The stakeholders have acknowledge that the

quick technological advancement and regulatory measures have resulted in several changes

which includes newer working patterns in gig or sharing economy. According to the

stakeholders, it is believed that the ATO and the government must have the systematic

approach in place in order as well as respond to the technological developments and

innovations (Woellner et al. 2016). The stakeholders have also cited their opinion that

making use of emerging technology and new regulatory changes would help in increasing the

automation inside the taxation system, however there is a significant need for more reliable

data.

The data must be obtained by the third parties such banks, whose burden of

compliance would increase correspondingly. The advantage of availability of large amount of

reliable data to government and its agencies, particularly the ATO involves greater

efficiencies and lower costs. The compliance of the taxpayers is also reduced with the help of

such kind of initiatives and brings improvement to pre-filled returns. The stakeholders have

expressed their views that there are restrictions to the degree of automation which can be

attained within the Australian taxation system largely due to the complexity and features such

as the work related expense deductions.

The stakeholders have also observed that the DTA offers wide range of guidance to

those agencies that are seeking to modernize the manner in which the taxpayers interact with

the government with the help of online service which is considered effective and cost

effective. The stakeholders believe that which are adopting the different platforms results in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

range of compliance requirements (Feld 2016). The stakeholders believe that to attain optimal

results, there should be more coordination and constant approach should be taken.

range of compliance requirements (Feld 2016). The stakeholders believe that to attain optimal

results, there should be more coordination and constant approach should be taken.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Feld, A., 2016. Federal Taxation of State Tax Credits.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Hum, F., Jackman, B., Quirico, O., Urbas, G. and Werren, K., 2019. Australian Uniform

Evidence Law. Cambridge University Press.

Keyzer, P., Goff, C. and Fisher, A., 2017. Principles of Australian constitutional law.

LexisNexis Butterworths.

Main, J., 2019. Taxation: Buying or selling: beware the sting of GST. LSJ: Law Society of

NSW Journal, (55), p.73.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Oishi, S., Kushlev, K. and Schimmack, U., 2018. Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), p.157.

Robin and Barkoczy woellner (stephen & murphy, shirley et al.), 2020. Australian taxation

law 2020. Oxford university press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Feld, A., 2016. Federal Taxation of State Tax Credits.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Hum, F., Jackman, B., Quirico, O., Urbas, G. and Werren, K., 2019. Australian Uniform

Evidence Law. Cambridge University Press.

Keyzer, P., Goff, C. and Fisher, A., 2017. Principles of Australian constitutional law.

LexisNexis Butterworths.

Main, J., 2019. Taxation: Buying or selling: beware the sting of GST. LSJ: Law Society of

NSW Journal, (55), p.73.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Oishi, S., Kushlev, K. and Schimmack, U., 2018. Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), p.157.

Robin and Barkoczy woellner (stephen & murphy, shirley et al.), 2020. Australian taxation

law 2020. Oxford university press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

11TAXATION LAW

Taylor, J., Walpole, M., Burton, M., Ciro, T. and Murray, I., 2017. Understanding Taxation

Law 2018. LexisNexis Butterworths.

Van Brederode, R.F., 2019. Ethics and Taxation. Springer.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Taylor, J., Walpole, M., Burton, M., Ciro, T. and Murray, I., 2017. Understanding Taxation

Law 2018. LexisNexis Butterworths.

Van Brederode, R.F., 2019. Ethics and Taxation. Springer.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.