Taxation Law Assignment: Analysis of Fringe Benefits and Income

VerifiedAdded on 2020/05/28

|12

|2450

|268

Homework Assignment

AI Summary

This assignment solution addresses taxation law, focusing on fringe benefits tax (FBT) and income tax. The first part analyzes the FBT implications for an employee provided with a company car, calculating the taxable value using both the statutory and operating cost methods. It considers various scenarios, including private use, car hire for personal events, and accommodation. The second part examines income tax, addressing the tax liabilities of individuals with diverse income sources including part-time work, locum services, and a barter system. It discusses the distinction between business and hobby activities, as well as the tax treatment of income derived from a barter system. The solution references relevant legislation, case laws, and taxation rulings to support its analysis and calculations.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Case Facts:.................................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to part (A):....................................................................................................................6

Answer to part (B)......................................................................................................................6

Answer to part (c ):....................................................................................................................7

Answer to Part (D):....................................................................................................................7

Reference List:...........................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Case Facts:.................................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to part (A):....................................................................................................................6

Answer to part (B)......................................................................................................................6

Answer to part (c ):....................................................................................................................7

Answer to Part (D):....................................................................................................................7

Reference List:...........................................................................................................................9

2TAXATION LAW

Answer to question 1:

According to the “Fringe Benefit Tax Assessment Act 1986” any form of benefit that

is paid to the employees apart from the salaries and wages is regarded as the fringe benefit

(Legislation.gov.au, 2018). however, the act lay down that there should be an association

among the employer and the employee along with the provider of the fringe benefit tax

legislation. This would help in keeping an account of the tax liabilities originating from such

benefits provided for both the employer and the employee.

As laid down under “Section 6 of the FBTAA 1986” car provided to employee by the

employer and the same is used for the private purpose altogether then it would attract car

fringe benefit tax (Ato.gov.au, 2018). The car fringe benefit tax is applicable at any time of

the day in regard to the occupation of the employee for the car held by the person or it is

taken to be available for the personal usage of the employee or the associate.

As defined under the “sub-section 136 (1) of the taxation ruling MT 2027” usage of

car by the employee which is not directly related to the course of generating the taxable

salary of the associate would be regarded as the personal use. In order to arrive at the

assessable amount of the fringe benefit of the car, the statutory method or the operating cost

formula is employed. Additionally, “section 10A and Section 10 B of the FBTAA 1986”

transacts with the determination of the taxable value of the car based on the operating cost

method (Ato.gov.au, 2018). Under “sub-section 136 (1)”, the method of operating cost

considers the cost that is sustained on the operations of the car and the details of the business

journeys is required to incorporated in the log book if they are used for ascertaining the

proportion of the private use of the car for implementing the operating cost method.

Answer to question 1:

According to the “Fringe Benefit Tax Assessment Act 1986” any form of benefit that

is paid to the employees apart from the salaries and wages is regarded as the fringe benefit

(Legislation.gov.au, 2018). however, the act lay down that there should be an association

among the employer and the employee along with the provider of the fringe benefit tax

legislation. This would help in keeping an account of the tax liabilities originating from such

benefits provided for both the employer and the employee.

As laid down under “Section 6 of the FBTAA 1986” car provided to employee by the

employer and the same is used for the private purpose altogether then it would attract car

fringe benefit tax (Ato.gov.au, 2018). The car fringe benefit tax is applicable at any time of

the day in regard to the occupation of the employee for the car held by the person or it is

taken to be available for the personal usage of the employee or the associate.

As defined under the “sub-section 136 (1) of the taxation ruling MT 2027” usage of

car by the employee which is not directly related to the course of generating the taxable

salary of the associate would be regarded as the personal use. In order to arrive at the

assessable amount of the fringe benefit of the car, the statutory method or the operating cost

formula is employed. Additionally, “section 10A and Section 10 B of the FBTAA 1986”

transacts with the determination of the taxable value of the car based on the operating cost

method (Ato.gov.au, 2018). Under “sub-section 136 (1)”, the method of operating cost

considers the cost that is sustained on the operations of the car and the details of the business

journeys is required to incorporated in the log book if they are used for ascertaining the

proportion of the private use of the car for implementing the operating cost method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Case Facts:

In the present case study, Charlie is the employee of Shiny Homes Pty Ltd and has

been provided with the car and the same would be liable for fringe benefit tax under the

legislation. As evident Charlie used the car for both private and business purpose and under

“Sub-section 136 (1)” it would attract fringe benefit tax.

The decision laid down in the case of “Lunney and Hayley v FCT (1958)” stated that

the travel from the employee home to the place of work is regarded as the ordinary private

travel (Ato.gov.au, 2018). Additionally, the travel to the place of work is considered as the

necessary “pre-requisite”. Charlie in this circumstance has travelled kilometres from his

home to the place of work and the same cannot be regarded for fringe benefit since they were

not in the course of generating taxable income. The private kilometres travelled by Charlie

would not change the outcome since the place of work is regarded as itinerant in nature.

There are two methods involved in computing the assessable amount of the fringe

benefit tax namely the “statutory method and the operating cost method” (Deutsch, 2014).

The statutory rate for computing the chargeable worth of the fringe benefit of the car is 20%.

The statutory percent is multiplied with the base amount of the car in order ascertain the

assessable value of the fringe benefits. The degree of private use of the car offered to the

employer is not pertinent in the ascertainment of the assessable amount of the fringe benefit

in statutory formula. Whereas under the operating costing method both the work and private

purpose of the car is separated in determining the assessable amount of the car fringe benefit.

The below stated statutory method is employed in determining the value of fringe benefit;

Computation of Fringe Benefit Tax under Statutory Method

Statutory method

Taxable value of fringe benefits

Particular Amount ($) Amount ($)

Case Facts:

In the present case study, Charlie is the employee of Shiny Homes Pty Ltd and has

been provided with the car and the same would be liable for fringe benefit tax under the

legislation. As evident Charlie used the car for both private and business purpose and under

“Sub-section 136 (1)” it would attract fringe benefit tax.

The decision laid down in the case of “Lunney and Hayley v FCT (1958)” stated that

the travel from the employee home to the place of work is regarded as the ordinary private

travel (Ato.gov.au, 2018). Additionally, the travel to the place of work is considered as the

necessary “pre-requisite”. Charlie in this circumstance has travelled kilometres from his

home to the place of work and the same cannot be regarded for fringe benefit since they were

not in the course of generating taxable income. The private kilometres travelled by Charlie

would not change the outcome since the place of work is regarded as itinerant in nature.

There are two methods involved in computing the assessable amount of the fringe

benefit tax namely the “statutory method and the operating cost method” (Deutsch, 2014).

The statutory rate for computing the chargeable worth of the fringe benefit of the car is 20%.

The statutory percent is multiplied with the base amount of the car in order ascertain the

assessable value of the fringe benefits. The degree of private use of the car offered to the

employer is not pertinent in the ascertainment of the assessable amount of the fringe benefit

in statutory formula. Whereas under the operating costing method both the work and private

purpose of the car is separated in determining the assessable amount of the car fringe benefit.

The below stated statutory method is employed in determining the value of fringe benefit;

Computation of Fringe Benefit Tax under Statutory Method

Statutory method

Taxable value of fringe benefits

Particular Amount ($) Amount ($)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

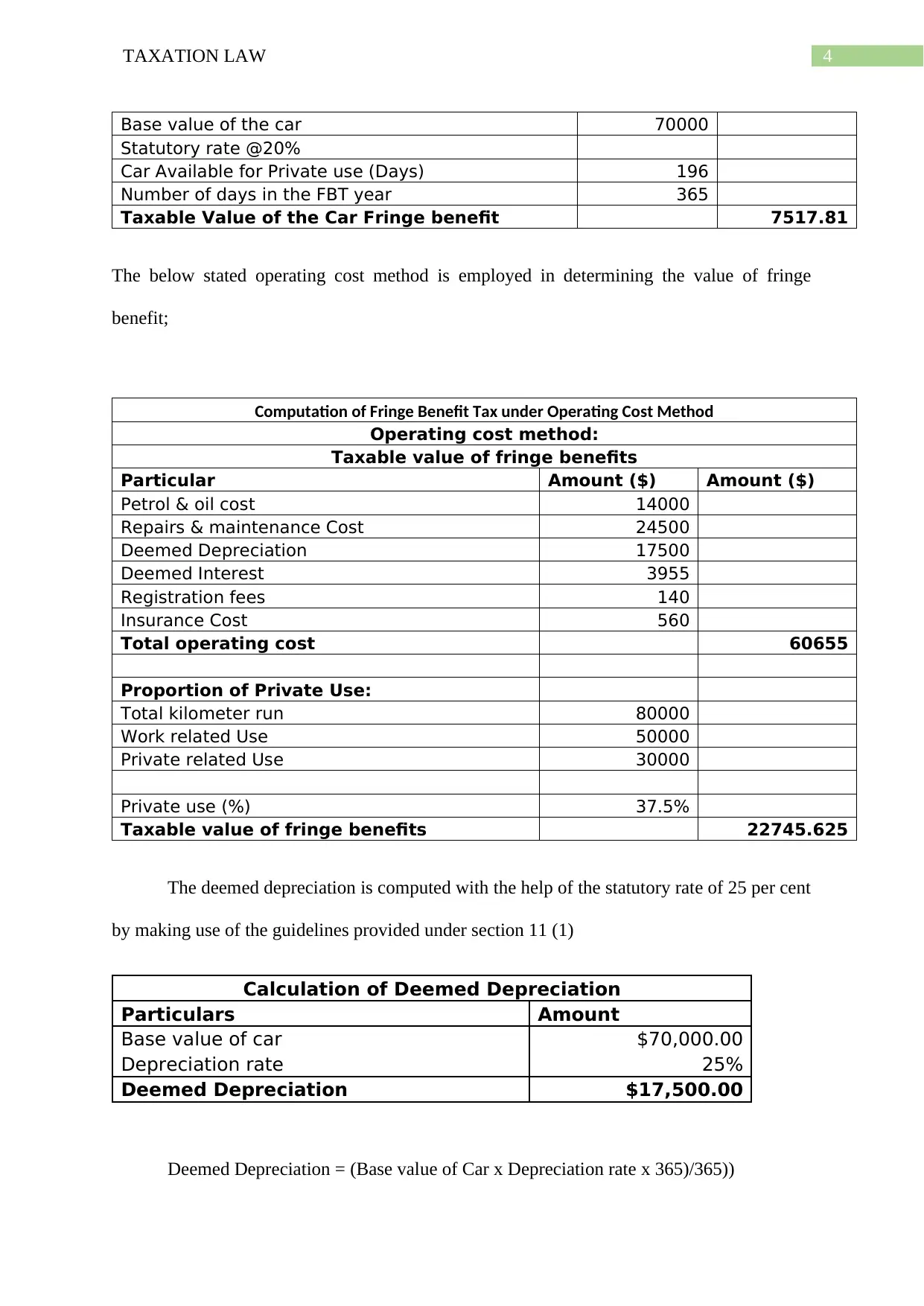

Base value of the car 70000

Statutory rate @20%

Car Available for Private use (Days) 196

Number of days in the FBT year 365

Taxable Value of the Car Fringe benefit 7517.81

The below stated operating cost method is employed in determining the value of fringe

benefit;

Computation of Fringe Benefit Tax under Operating Cost Method

Operating cost method:

Taxable value of fringe benefits

Particular Amount ($) Amount ($)

Petrol & oil cost 14000

Repairs & maintenance Cost 24500

Deemed Depreciation 17500

Deemed Interest 3955

Registration fees 140

Insurance Cost 560

Total operating cost 60655

Proportion of Private Use:

Total kilometer run 80000

Work related Use 50000

Private related Use 30000

Private use (%) 37.5%

Taxable value of fringe benefits 22745.625

The deemed depreciation is computed with the help of the statutory rate of 25 per cent

by making use of the guidelines provided under section 11 (1)

Calculation of Deemed Depreciation

Particulars Amount

Base value of car $70,000.00

Depreciation rate 25%

Deemed Depreciation $17,500.00

Deemed Depreciation = (Base value of Car x Depreciation rate x 365)/365))

Base value of the car 70000

Statutory rate @20%

Car Available for Private use (Days) 196

Number of days in the FBT year 365

Taxable Value of the Car Fringe benefit 7517.81

The below stated operating cost method is employed in determining the value of fringe

benefit;

Computation of Fringe Benefit Tax under Operating Cost Method

Operating cost method:

Taxable value of fringe benefits

Particular Amount ($) Amount ($)

Petrol & oil cost 14000

Repairs & maintenance Cost 24500

Deemed Depreciation 17500

Deemed Interest 3955

Registration fees 140

Insurance Cost 560

Total operating cost 60655

Proportion of Private Use:

Total kilometer run 80000

Work related Use 50000

Private related Use 30000

Private use (%) 37.5%

Taxable value of fringe benefits 22745.625

The deemed depreciation is computed with the help of the statutory rate of 25 per cent

by making use of the guidelines provided under section 11 (1)

Calculation of Deemed Depreciation

Particulars Amount

Base value of car $70,000.00

Depreciation rate 25%

Deemed Depreciation $17,500.00

Deemed Depreciation = (Base value of Car x Depreciation rate x 365)/365))

5TAXATION LAW

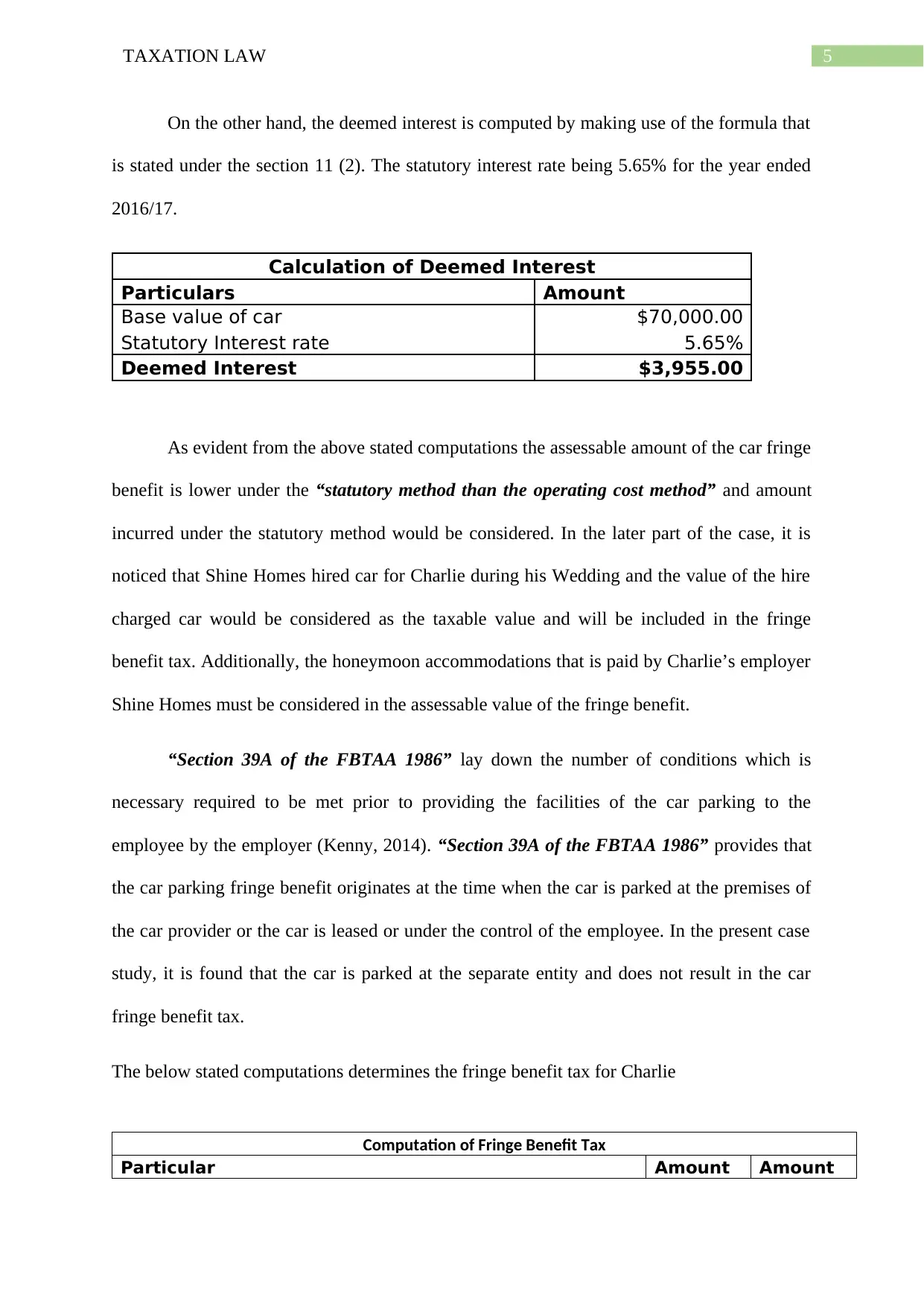

On the other hand, the deemed interest is computed by making use of the formula that

is stated under the section 11 (2). The statutory interest rate being 5.65% for the year ended

2016/17.

Calculation of Deemed Interest

Particulars Amount

Base value of car $70,000.00

Statutory Interest rate 5.65%

Deemed Interest $3,955.00

As evident from the above stated computations the assessable amount of the car fringe

benefit is lower under the “statutory method than the operating cost method” and amount

incurred under the statutory method would be considered. In the later part of the case, it is

noticed that Shine Homes hired car for Charlie during his Wedding and the value of the hire

charged car would be considered as the taxable value and will be included in the fringe

benefit tax. Additionally, the honeymoon accommodations that is paid by Charlie’s employer

Shine Homes must be considered in the assessable value of the fringe benefit.

“Section 39A of the FBTAA 1986” lay down the number of conditions which is

necessary required to be met prior to providing the facilities of the car parking to the

employee by the employer (Kenny, 2014). “Section 39A of the FBTAA 1986” provides that

the car parking fringe benefit originates at the time when the car is parked at the premises of

the car provider or the car is leased or under the control of the employee. In the present case

study, it is found that the car is parked at the separate entity and does not result in the car

fringe benefit tax.

The below stated computations determines the fringe benefit tax for Charlie

Computation of Fringe Benefit Tax

Particular Amount Amount

On the other hand, the deemed interest is computed by making use of the formula that

is stated under the section 11 (2). The statutory interest rate being 5.65% for the year ended

2016/17.

Calculation of Deemed Interest

Particulars Amount

Base value of car $70,000.00

Statutory Interest rate 5.65%

Deemed Interest $3,955.00

As evident from the above stated computations the assessable amount of the car fringe

benefit is lower under the “statutory method than the operating cost method” and amount

incurred under the statutory method would be considered. In the later part of the case, it is

noticed that Shine Homes hired car for Charlie during his Wedding and the value of the hire

charged car would be considered as the taxable value and will be included in the fringe

benefit tax. Additionally, the honeymoon accommodations that is paid by Charlie’s employer

Shine Homes must be considered in the assessable value of the fringe benefit.

“Section 39A of the FBTAA 1986” lay down the number of conditions which is

necessary required to be met prior to providing the facilities of the car parking to the

employee by the employer (Kenny, 2014). “Section 39A of the FBTAA 1986” provides that

the car parking fringe benefit originates at the time when the car is parked at the premises of

the car provider or the car is leased or under the control of the employee. In the present case

study, it is found that the car is parked at the separate entity and does not result in the car

fringe benefit tax.

The below stated computations determines the fringe benefit tax for Charlie

Computation of Fringe Benefit Tax

Particular Amount Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

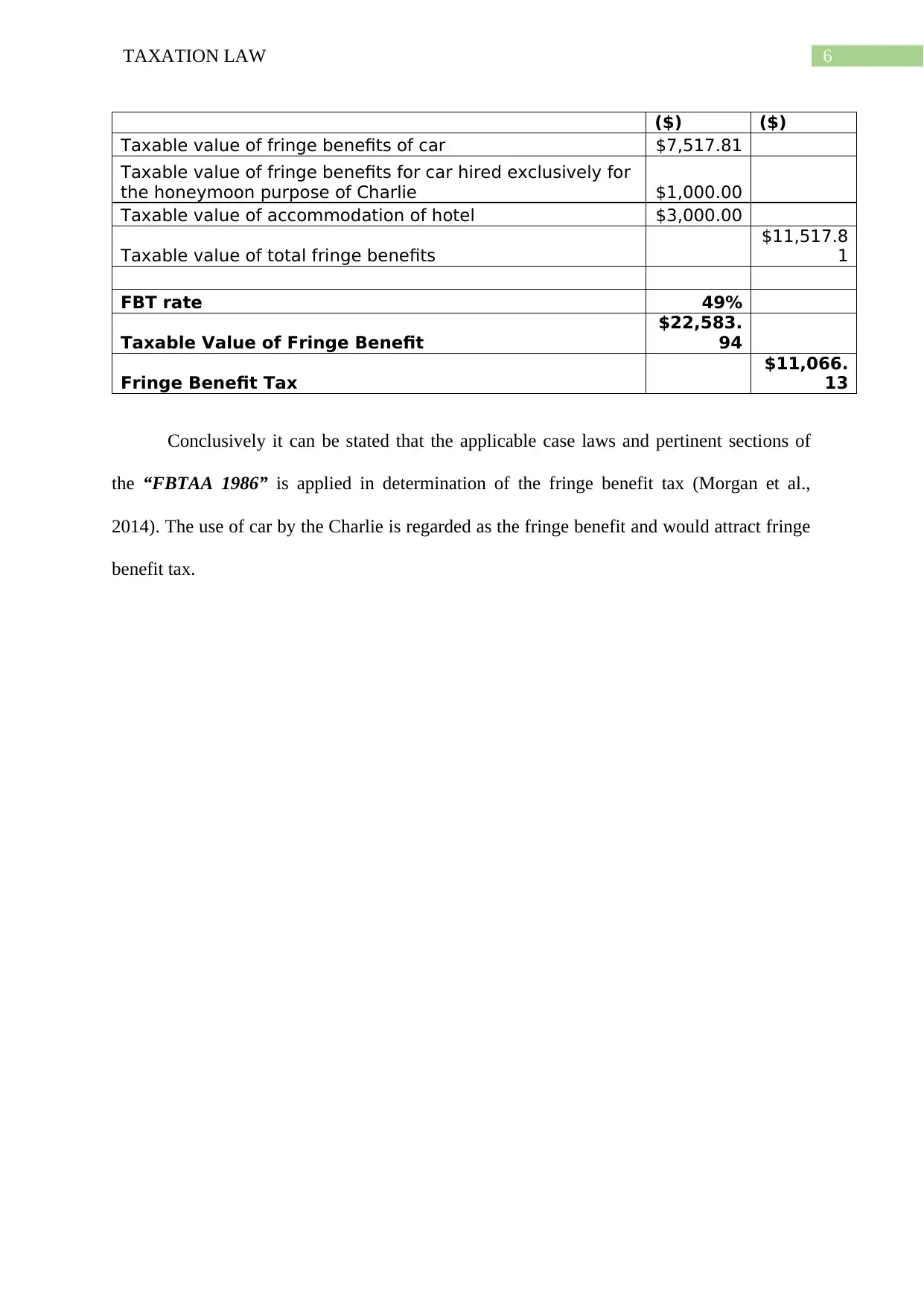

6TAXATION LAW

($) ($)

Taxable value of fringe benefits of car $7,517.81

Taxable value of fringe benefits for car hired exclusively for

the honeymoon purpose of Charlie $1,000.00

Taxable value of accommodation of hotel $3,000.00

Taxable value of total fringe benefits

$11,517.8

1

FBT rate 49%

Taxable Value of Fringe Benefit

$22,583.

94

Fringe Benefit Tax

$11,066.

13

Conclusively it can be stated that the applicable case laws and pertinent sections of

the “FBTAA 1986” is applied in determination of the fringe benefit tax (Morgan et al.,

2014). The use of car by the Charlie is regarded as the fringe benefit and would attract fringe

benefit tax.

($) ($)

Taxable value of fringe benefits of car $7,517.81

Taxable value of fringe benefits for car hired exclusively for

the honeymoon purpose of Charlie $1,000.00

Taxable value of accommodation of hotel $3,000.00

Taxable value of total fringe benefits

$11,517.8

1

FBT rate 49%

Taxable Value of Fringe Benefit

$22,583.

94

Fringe Benefit Tax

$11,066.

13

Conclusively it can be stated that the applicable case laws and pertinent sections of

the “FBTAA 1986” is applied in determination of the fringe benefit tax (Morgan et al.,

2014). The use of car by the Charlie is regarded as the fringe benefit and would attract fringe

benefit tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Answer to part (A):

As evident from the current case study of Allan and Betty they undertook the decision

of tree change. Additionally, they decided to sell their house located in Melbourne in order to

acquire the country home located in the Central Victoria and the same will be liable for any

tax liability. However, according to the “section 6-5 of the ITAA 1997” income derived

directly from the business or profession will be considered for taxation (Sadiq et al., 2014).

Similarly, the income derived by Allan and Betty as the part time accountant and the Locum

doctor will attract tax liability under the “section 6-5 of the ITAA 1997”.

The case study evidently puts forward that Allan was wide known among his elderly

clients as the locum doctor and charged fees from the patients that visited him. He received a

large number of homemade cakes and food from his patients in the form of token for

appreciation. It is worth mentioning that cakes and food does not attracts tax liability since

they did not possess the nature of commercial goods nor having any commercial value

(Woellner et al., 2014). Apart from this Allan did received wine from one of his customer

that contained commercial value of $36. Therefore, the value of wine that is received by

Allan will attract tax liability and will be included in the taxable revenue in respect of the

ITAA 1997.

Answer to part (B)

The “taxation ruling of TR 97/11” is concerned with the determination of the individuals

indulged in business activities (Woellner et al., 2014). The “taxation ruling of TR 97/11”

helps in distinguishing the differences associated with business and hobbies which is listed

below;

Answer to question 2:

Answer to part (A):

As evident from the current case study of Allan and Betty they undertook the decision

of tree change. Additionally, they decided to sell their house located in Melbourne in order to

acquire the country home located in the Central Victoria and the same will be liable for any

tax liability. However, according to the “section 6-5 of the ITAA 1997” income derived

directly from the business or profession will be considered for taxation (Sadiq et al., 2014).

Similarly, the income derived by Allan and Betty as the part time accountant and the Locum

doctor will attract tax liability under the “section 6-5 of the ITAA 1997”.

The case study evidently puts forward that Allan was wide known among his elderly

clients as the locum doctor and charged fees from the patients that visited him. He received a

large number of homemade cakes and food from his patients in the form of token for

appreciation. It is worth mentioning that cakes and food does not attracts tax liability since

they did not possess the nature of commercial goods nor having any commercial value

(Woellner et al., 2014). Apart from this Allan did received wine from one of his customer

that contained commercial value of $36. Therefore, the value of wine that is received by

Allan will attract tax liability and will be included in the taxable revenue in respect of the

ITAA 1997.

Answer to part (B)

The “taxation ruling of TR 97/11” is concerned with the determination of the individuals

indulged in business activities (Woellner et al., 2014). The “taxation ruling of TR 97/11”

helps in distinguishing the differences associated with business and hobbies which is listed

below;

8TAXATION LAW

a. The objective of the activity forms vital element in ascertaining whether the activity

constituted business or hobby. On finding that the activity holds business objective

then the same will be considered as the business activity.

b. The purpose of the business is to derive profit while the hobby does not holds such

purpose.

c. Business activities generally attracts large number of capital investment whereas

hobby does not contain any capital investment.

d. The business activities contain of the employer and employee relationships however

under hobby there is no such relationships exists.

e. To conduct business there is a need for premises, however no such premises is

required in performing the hobby.

As held in the case of “Cooper Books Pty Ltd vs. Commissioner of Taxation of

Commonwealth of Australia” the court in its decision has stated the necessary criteria to

distinguish between the business activities and the hobby.

Answer to part (c ):

On finding that the hobby of the tax payer transforms into the business activities and

derives profits from the same then it will attract tax liability for any amount of income

derived from the business (Frecknall et al., 2014). As evident in the present case of Allan and

Betty the hobby of gardening has transformed into the business activities and derived the

revenue of approximately $500 to $600 from the sale of Marmalade will be liable for

taxation. Similarly, the barter system of Allan and Betty will additionally attract tax liability

in respect of the ITAA 1997.

a. The objective of the activity forms vital element in ascertaining whether the activity

constituted business or hobby. On finding that the activity holds business objective

then the same will be considered as the business activity.

b. The purpose of the business is to derive profit while the hobby does not holds such

purpose.

c. Business activities generally attracts large number of capital investment whereas

hobby does not contain any capital investment.

d. The business activities contain of the employer and employee relationships however

under hobby there is no such relationships exists.

e. To conduct business there is a need for premises, however no such premises is

required in performing the hobby.

As held in the case of “Cooper Books Pty Ltd vs. Commissioner of Taxation of

Commonwealth of Australia” the court in its decision has stated the necessary criteria to

distinguish between the business activities and the hobby.

Answer to part (c ):

On finding that the hobby of the tax payer transforms into the business activities and

derives profits from the same then it will attract tax liability for any amount of income

derived from the business (Frecknall et al., 2014). As evident in the present case of Allan and

Betty the hobby of gardening has transformed into the business activities and derived the

revenue of approximately $500 to $600 from the sale of Marmalade will be liable for

taxation. Similarly, the barter system of Allan and Betty will additionally attract tax liability

in respect of the ITAA 1997.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to Part (D):

The transactions of the barter system are subjected to the provision of the taxation

under the ITAA 1997 and GSTR1999 given that the transactions holds the nature of the

business transactions (Miller & Oats, 2016). The commercial transaction under the barter

system would be considered at with the transactions conducted under the cash and credit.

Income derived from such transaction would attract tax liability under the ITAA 1997 and

GSTR 1999. The barter system set up Allan and Betty will be considered in respect of the

cash and credit transaction and would be liable for income tax and GST.

Answer to Part (D):

The transactions of the barter system are subjected to the provision of the taxation

under the ITAA 1997 and GSTR1999 given that the transactions holds the nature of the

business transactions (Miller & Oats, 2016). The commercial transaction under the barter

system would be considered at with the transactions conducted under the cash and credit.

Income derived from such transaction would attract tax liability under the ITAA 1997 and

GSTR 1999. The barter system set up Allan and Betty will be considered in respect of the

cash and credit transaction and would be liable for income tax and GST.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Deutsch, R. (2014). Australian tax handbook 2014. Pyrmont, NSW: Thomson Reuters.

Frecknall-Hughes, J. (2014). The Theory, Principles and Management of Taxation: An

Introduction. Routledge.

Fringe Benefits Tax Assessment Act 1986. (2018). Legislation.gov.au. Retrieved 6 January

2018, from https://www.legislation.gov.au/Details/C2016C00276

Kenny, P. Australian tax 2014.

Legal Database. (2018). Ato.gov.au. Retrieved 6 January 2018, from

https://www.ato.gov.au/law/view/document?docid=PAC/19860039/7

Legal Database. (2018). Ato.gov.au. Retrieved 6 January 2018, from

https://www.ato.gov.au/law/view/document?docid=MTR/MT2027/NAT/ATO/00001

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. A practical introduction to Australian taxation law.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting,

A. Principles of taxation law 2014.

TD 2016/7 - Fringe benefits tax: for the purposes of section 39A of the Fringe Benefits Tax

Assessment Act 1986 what is the car parking threshold for the fringe benefits tax year

commencing on 1 April 2016 (As at 18 May 2016). (2018). Law.ato.gov.au. Retrieved

6 January 2018, from http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD

%2FTD20167%2FNAT%2FATO%2F00001%22

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. Australian taxation law select

2014.

Reference List:

Deutsch, R. (2014). Australian tax handbook 2014. Pyrmont, NSW: Thomson Reuters.

Frecknall-Hughes, J. (2014). The Theory, Principles and Management of Taxation: An

Introduction. Routledge.

Fringe Benefits Tax Assessment Act 1986. (2018). Legislation.gov.au. Retrieved 6 January

2018, from https://www.legislation.gov.au/Details/C2016C00276

Kenny, P. Australian tax 2014.

Legal Database. (2018). Ato.gov.au. Retrieved 6 January 2018, from

https://www.ato.gov.au/law/view/document?docid=PAC/19860039/7

Legal Database. (2018). Ato.gov.au. Retrieved 6 January 2018, from

https://www.ato.gov.au/law/view/document?docid=MTR/MT2027/NAT/ATO/00001

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. A practical introduction to Australian taxation law.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting,

A. Principles of taxation law 2014.

TD 2016/7 - Fringe benefits tax: for the purposes of section 39A of the Fringe Benefits Tax

Assessment Act 1986 what is the car parking threshold for the fringe benefits tax year

commencing on 1 April 2016 (As at 18 May 2016). (2018). Law.ato.gov.au. Retrieved

6 January 2018, from http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD

%2FTD20167%2FNAT%2FATO%2F00001%22

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. Australian taxation law select

2014.

11TAXATION LAW

Woellner, R., Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. Australian

Taxation Law 2015.

Woellner, R., Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. Australian

Taxation Law 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.