Principles of Taxation Law Assignment: CBP and Monica's Taxation

VerifiedAdded on 2023/06/10

|11

|1727

|347

Homework Assignment

AI Summary

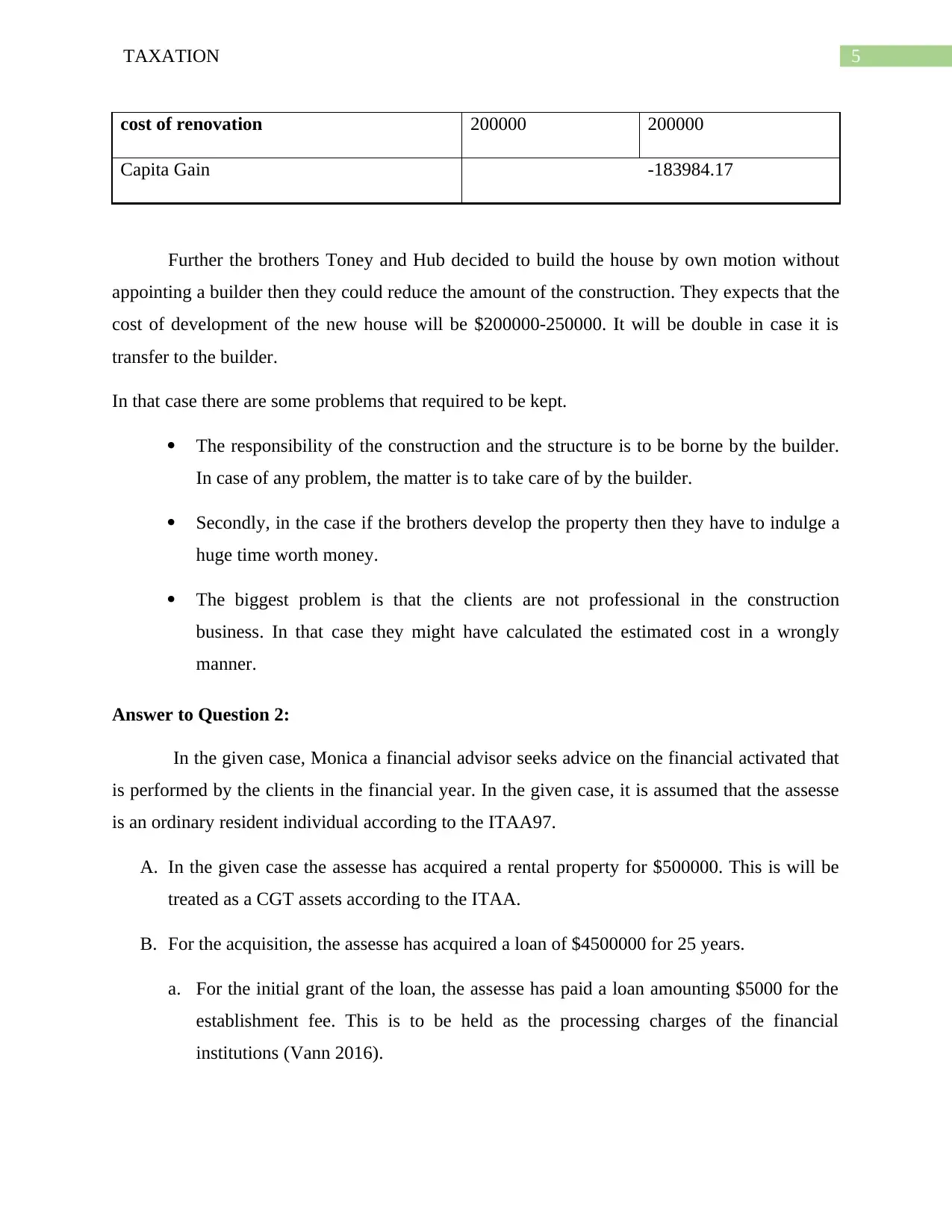

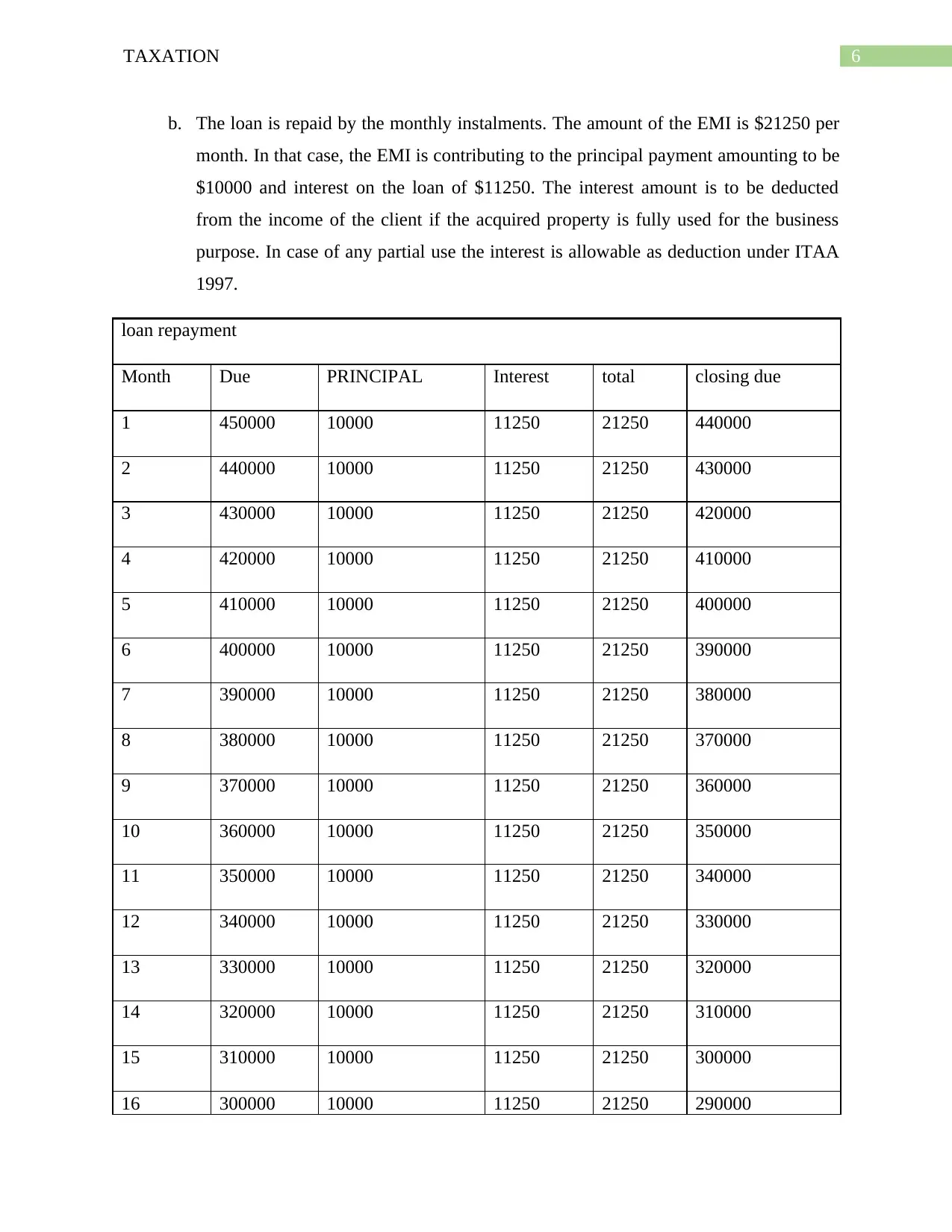

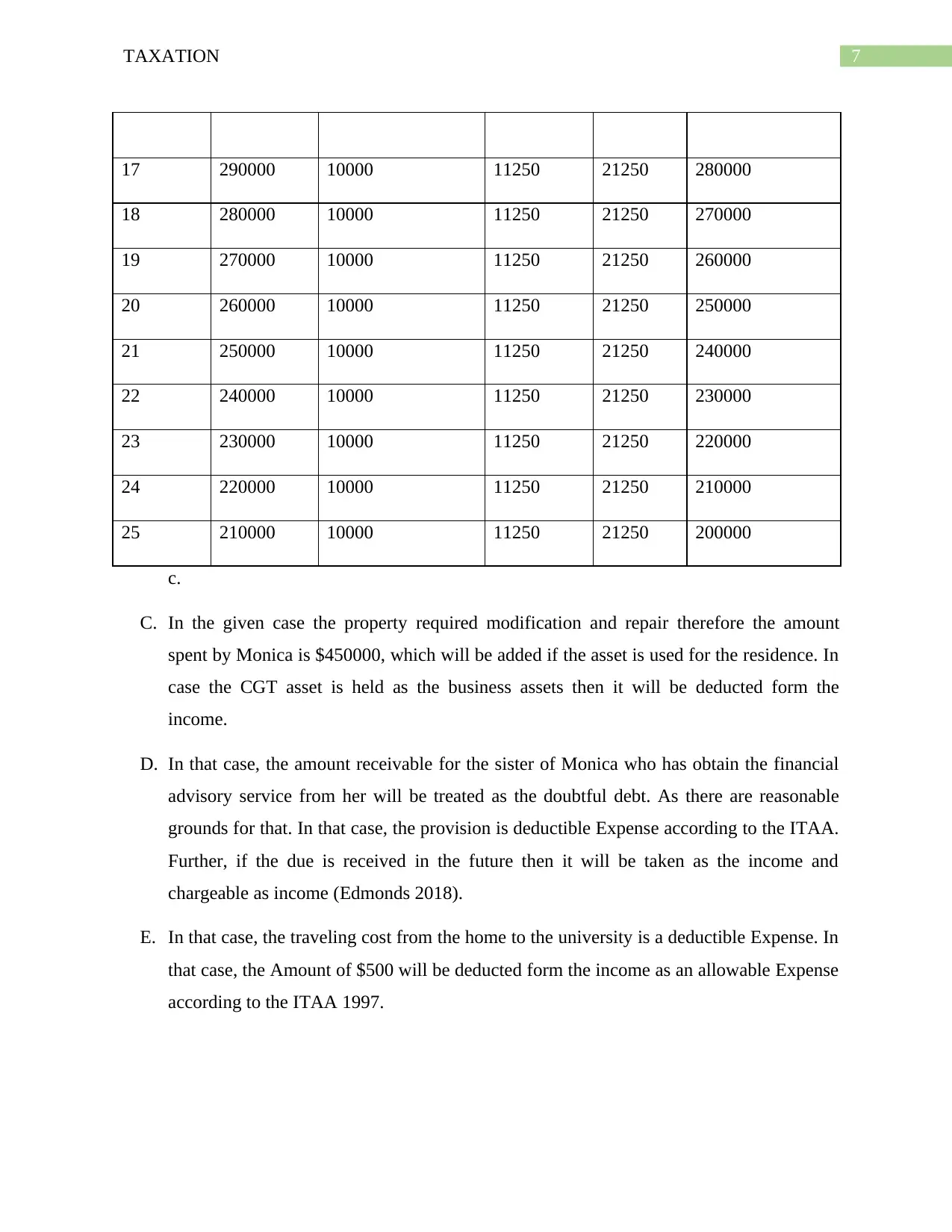

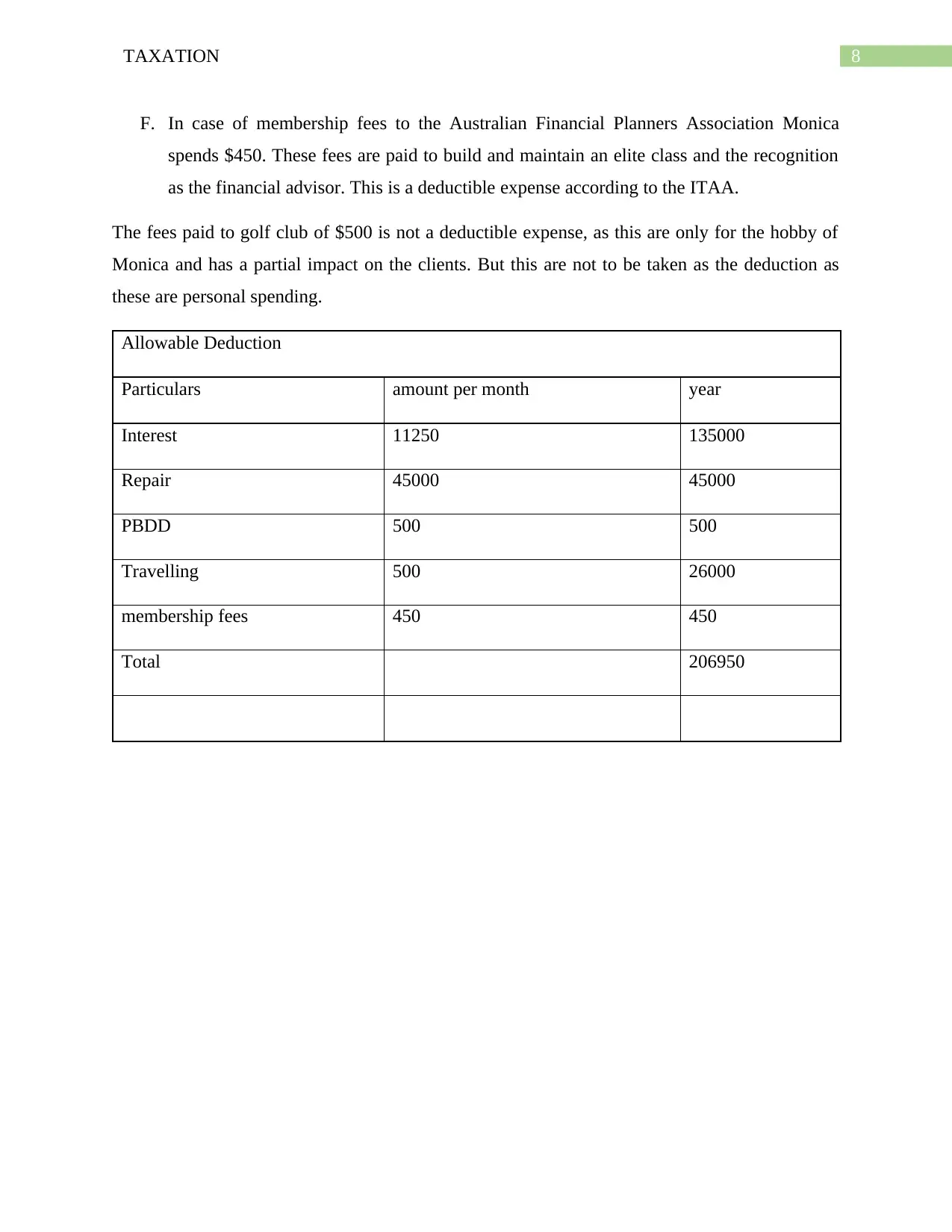

This document presents a comprehensive solution to a Principles of Taxation Law assignment. The assignment addresses two main questions: the first question analyzes the tax implications for a building partnership, Cedars Building Partners (CBP), focusing on property inheritance, rental income, capital gains, and construction costs. It explores various scenarios including property sales, rental income, and the impact of construction methods on tax liabilities. The second question provides financial advice to Monica, evaluating the tax treatment of rental properties, loan repayments, property modifications, doubtful debts, travel expenses, and professional membership fees. The solution provides detailed calculations and explanations based on the ITAA97, covering capital gains tax, allowable deductions, and income tax considerations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.