BX3112 Taxation Law SP 22: Analysis of Capital Gains and Tax Issues

VerifiedAdded on 2023/06/06

|4

|894

|312

Homework Assignment

AI Summary

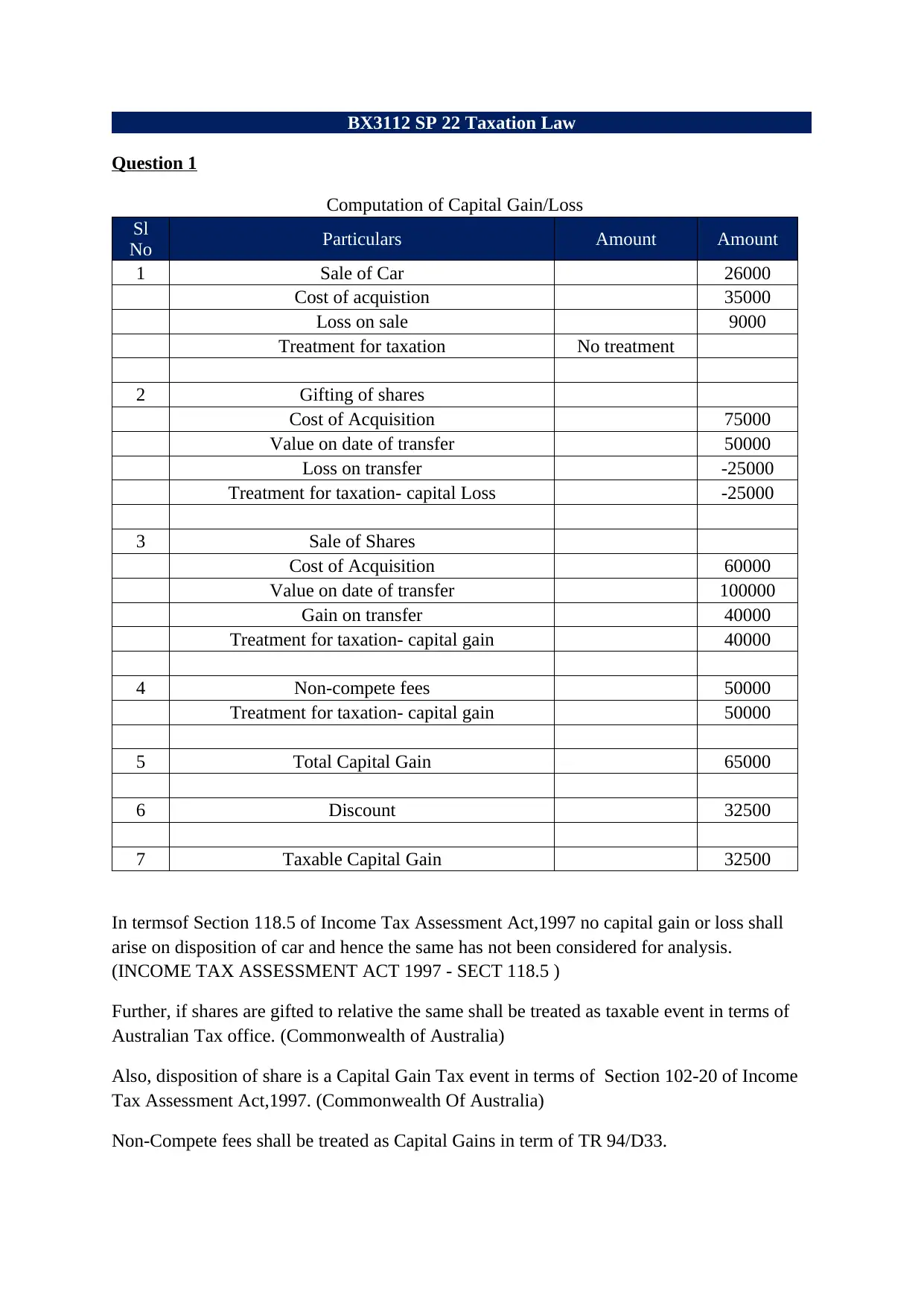

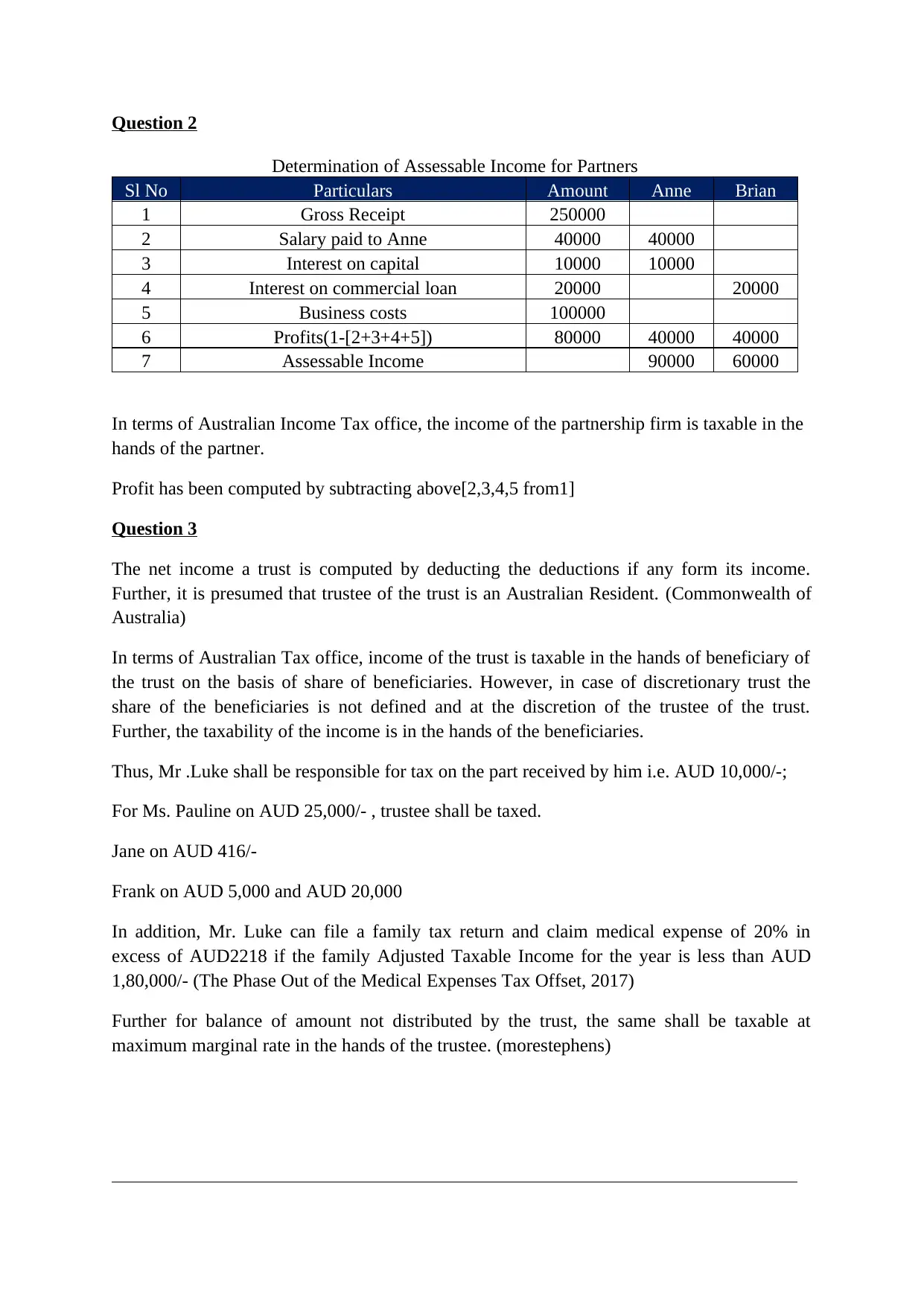

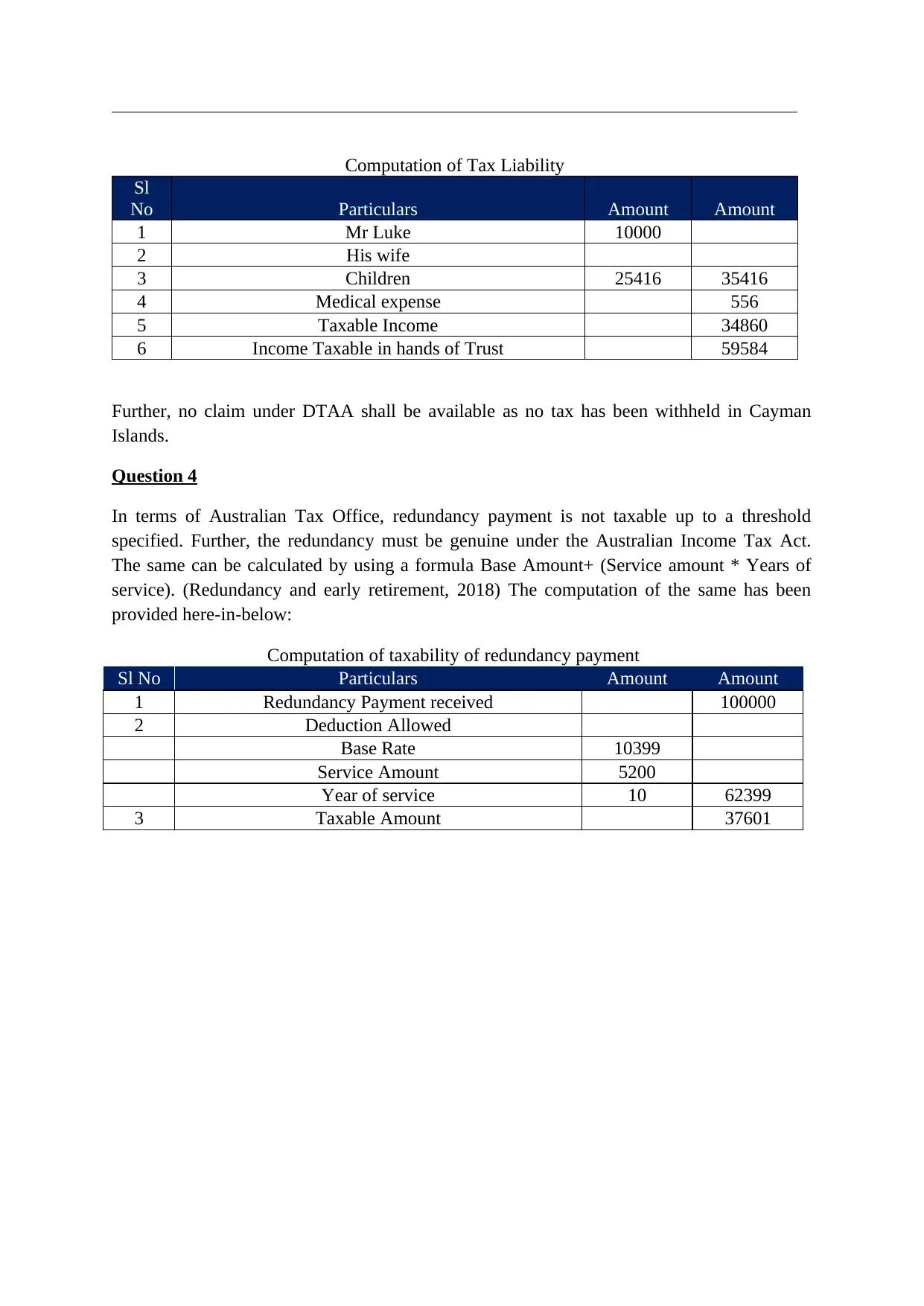

This assignment solution addresses key aspects of taxation law, including the computation of capital gains and losses from various transactions such as the sale of a car and shares, the treatment of non-compete fees, and the implications of gifting shares. It also delves into the determination of assessable income for partners in a firm, considering salary, interest on capital, and business costs. Furthermore, the assignment analyzes the taxability of trust income in the hands of beneficiaries and the trustee, along with the computation of individual tax liabilities, including potential medical expense claims. Finally, it examines the tax treatment of redundancy payments, outlining the calculation of taxable amounts based on base and service amounts, referencing relevant sections of the Australian Income Tax Act and Australian Tax Office guidelines. The document provides detailed calculations and legal justifications for each scenario.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.