Comprehensive Analysis of Taxation Theory, Practice, and Law

VerifiedAdded on 2020/09/03

|12

|3699

|34

Report

AI Summary

This report provides a comprehensive analysis of taxation, encompassing capital gains, fringe benefits, and property transactions. The first section examines capital gains, differentiating between short-term and long-term gains, and calculating tax liabilities based on asset sales. The second section focuses on fringe benefits, specifically a loan provided to an employee, calculating taxable benefits and deductions. The third section delves into property taxation, analyzing the tax implications of a rental property purchase, including deductions for expenses and the impact of agreements between owners. The report provides detailed calculations and practical examples, referencing relevant tax laws and provisions, offering a thorough understanding of various taxation aspects.

Taxation theory, practice and

law

law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

Introduction............................................................................................................................1

Critical analysis......................................................................................................................1

Supporting Evidence..............................................................................................................1

Conclusion..............................................................................................................................2

QUESTION 2...................................................................................................................................2

Introduction............................................................................................................................2

Critical analysis......................................................................................................................2

Supportive evidence:..............................................................................................................4

Conclusion..............................................................................................................................4

QUESTION 3...................................................................................................................................4

Introduction............................................................................................................................4

Critical analysis......................................................................................................................5

Supportive evidence...............................................................................................................5

Conclusion..............................................................................................................................5

QUESTION 4...................................................................................................................................6

Introduction............................................................................................................................6

Critical analysis......................................................................................................................6

Supporting evidence...............................................................................................................7

Conclusion..............................................................................................................................7

QUESTION 5...................................................................................................................................7

Introduction............................................................................................................................7

Critical analysis......................................................................................................................7

Supporting evidence...............................................................................................................8

Conclusion..............................................................................................................................8

REFERENCES................................................................................................................................9

QUESTION 1...................................................................................................................................1

Introduction............................................................................................................................1

Critical analysis......................................................................................................................1

Supporting Evidence..............................................................................................................1

Conclusion..............................................................................................................................2

QUESTION 2...................................................................................................................................2

Introduction............................................................................................................................2

Critical analysis......................................................................................................................2

Supportive evidence:..............................................................................................................4

Conclusion..............................................................................................................................4

QUESTION 3...................................................................................................................................4

Introduction............................................................................................................................4

Critical analysis......................................................................................................................5

Supportive evidence...............................................................................................................5

Conclusion..............................................................................................................................5

QUESTION 4...................................................................................................................................6

Introduction............................................................................................................................6

Critical analysis......................................................................................................................6

Supporting evidence...............................................................................................................7

Conclusion..............................................................................................................................7

QUESTION 5...................................................................................................................................7

Introduction............................................................................................................................7

Critical analysis......................................................................................................................7

Supporting evidence...............................................................................................................8

Conclusion..............................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

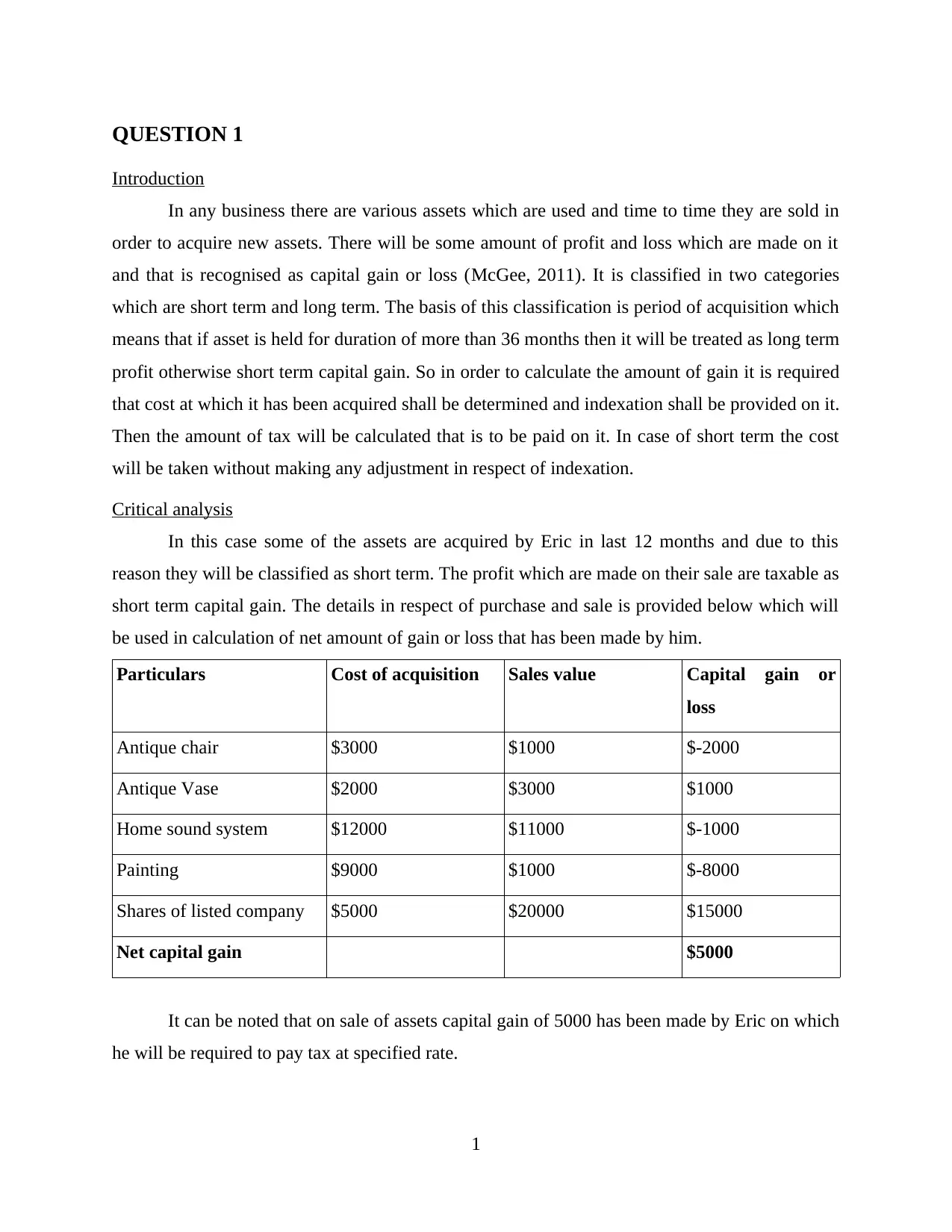

QUESTION 1

Introduction

In any business there are various assets which are used and time to time they are sold in

order to acquire new assets. There will be some amount of profit and loss which are made on it

and that is recognised as capital gain or loss (McGee, 2011). It is classified in two categories

which are short term and long term. The basis of this classification is period of acquisition which

means that if asset is held for duration of more than 36 months then it will be treated as long term

profit otherwise short term capital gain. So in order to calculate the amount of gain it is required

that cost at which it has been acquired shall be determined and indexation shall be provided on it.

Then the amount of tax will be calculated that is to be paid on it. In case of short term the cost

will be taken without making any adjustment in respect of indexation.

Critical analysis

In this case some of the assets are acquired by Eric in last 12 months and due to this

reason they will be classified as short term. The profit which are made on their sale are taxable as

short term capital gain. The details in respect of purchase and sale is provided below which will

be used in calculation of net amount of gain or loss that has been made by him.

Particulars Cost of acquisition Sales value Capital gain or

loss

Antique chair $3000 $1000 $-2000

Antique Vase $2000 $3000 $1000

Home sound system $12000 $11000 $-1000

Painting $9000 $1000 $-8000

Shares of listed company $5000 $20000 $15000

Net capital gain $5000

It can be noted that on sale of assets capital gain of 5000 has been made by Eric on which

he will be required to pay tax at specified rate.

1

Introduction

In any business there are various assets which are used and time to time they are sold in

order to acquire new assets. There will be some amount of profit and loss which are made on it

and that is recognised as capital gain or loss (McGee, 2011). It is classified in two categories

which are short term and long term. The basis of this classification is period of acquisition which

means that if asset is held for duration of more than 36 months then it will be treated as long term

profit otherwise short term capital gain. So in order to calculate the amount of gain it is required

that cost at which it has been acquired shall be determined and indexation shall be provided on it.

Then the amount of tax will be calculated that is to be paid on it. In case of short term the cost

will be taken without making any adjustment in respect of indexation.

Critical analysis

In this case some of the assets are acquired by Eric in last 12 months and due to this

reason they will be classified as short term. The profit which are made on their sale are taxable as

short term capital gain. The details in respect of purchase and sale is provided below which will

be used in calculation of net amount of gain or loss that has been made by him.

Particulars Cost of acquisition Sales value Capital gain or

loss

Antique chair $3000 $1000 $-2000

Antique Vase $2000 $3000 $1000

Home sound system $12000 $11000 $-1000

Painting $9000 $1000 $-8000

Shares of listed company $5000 $20000 $15000

Net capital gain $5000

It can be noted that on sale of assets capital gain of 5000 has been made by Eric on which

he will be required to pay tax at specified rate.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supporting Evidence

The capital gain is made when the assets or shares are sold. For this it shall be determined

that it is capital asset and then on disposition amount earned will be calculated by comparing it

with cost. All the individuals are required to pay tax under the specified Act. For this he will be

needed to make a report that is provided in annual report which is filed. In that all the

information in regards to the net amount of gain and the liability that is to be met will be

mentioned (Brigham and Ehrhardt, 2013). There are various provisions which are made in

relation to set off of losses. According to them all the losses which will be arising on capital

assets shall be set off from income under same head. This means that capital losses will have to

be deducted from capital gains only and by this liability of assessee will be reduced and this is

beneficial for them as less amount of tax will have to be paid now. Out of all the assets, some of

them are such which have been excluded from the provisions of act. In case of those assets which

have been acquired upto 20th September, 1985, there are certain assets which will be avoided

from the tax liability. The main among them are such assets which are used for personal purpose

or those on which depreciation is provided. So on them individual will not be required to pay any

amount of tax as laws will not be applicable on them.

Conclusion

Under the income tax act there are various laws which are prescribed in context of capital

gains and losses. It is required that they shall be complied by all and for that assessment will be

made in which taxable amount is determined so that final liability can be calculated. All of this

has been provided above with the help of practical solution.

QUESTION 2

Introduction

In an organisation there are various benefits which are provided to employees by

employers in addition to regular salary and they are known as fringe benefits (Baldwin, Cave and

Lodge, 2012). For taxation purpose there are some which are exempted and on others tax will

have to be paid. In order to meet this criteria it is needed that taxable amount of benefits shall be

calculated. In given case Brian had been provided with loan at interest of 1% that will be paid on

monthly basis. So the benefits in respect of it are discussed below.

2

The capital gain is made when the assets or shares are sold. For this it shall be determined

that it is capital asset and then on disposition amount earned will be calculated by comparing it

with cost. All the individuals are required to pay tax under the specified Act. For this he will be

needed to make a report that is provided in annual report which is filed. In that all the

information in regards to the net amount of gain and the liability that is to be met will be

mentioned (Brigham and Ehrhardt, 2013). There are various provisions which are made in

relation to set off of losses. According to them all the losses which will be arising on capital

assets shall be set off from income under same head. This means that capital losses will have to

be deducted from capital gains only and by this liability of assessee will be reduced and this is

beneficial for them as less amount of tax will have to be paid now. Out of all the assets, some of

them are such which have been excluded from the provisions of act. In case of those assets which

have been acquired upto 20th September, 1985, there are certain assets which will be avoided

from the tax liability. The main among them are such assets which are used for personal purpose

or those on which depreciation is provided. So on them individual will not be required to pay any

amount of tax as laws will not be applicable on them.

Conclusion

Under the income tax act there are various laws which are prescribed in context of capital

gains and losses. It is required that they shall be complied by all and for that assessment will be

made in which taxable amount is determined so that final liability can be calculated. All of this

has been provided above with the help of practical solution.

QUESTION 2

Introduction

In an organisation there are various benefits which are provided to employees by

employers in addition to regular salary and they are known as fringe benefits (Baldwin, Cave and

Lodge, 2012). For taxation purpose there are some which are exempted and on others tax will

have to be paid. In order to meet this criteria it is needed that taxable amount of benefits shall be

calculated. In given case Brian had been provided with loan at interest of 1% that will be paid on

monthly basis. So the benefits in respect of it are discussed below.

2

Critical analysis

Fringe benefits are those which are provided additionally or can say specifically to some

employees. Same has been done in given case under which a loan is provided by bank to its

employee Brian and that too at a rate of 1% interest. As the rate is less that what is set by

industry so there will be benefits which are included in it. That rate which is specified at which

interest is to be paid is 5.65% for financial year 2016-17. So the amount of taxable benefits will

be calculated by identifying the variation between interest that is to be paid according to

statutory rates and actual rate. The manner in which it will be calculated is provided here under.

Calculation of Taxable fringe benefits:

Step 1: Calculation of gross taxable amount:

Actual Interest = Loan amount * 1/100

= $1000000 * 1/100

=$10000

Statutory interest = $1000000 * 5.65/100

= $56500

Gross taxable Amount of benefit = $56500 - $10000 = $46500

Step 2: Value of benefits if no interest is paid:

= $1000000 * 5.65 /100

= $56500

Step 3: Deduction allowed to Brian in respect of statutory interest:

= $56500 * 40/100

= $22600

Step 4: Deduction allowed to Brian in respect of Actual interest:

= $10000 * 40/100

= $4000

Step 5: Notional Deduction which will be provided to Brian:

= $22600 - $4000

= $18600

Step 6: Calculation of net taxable amount:

= Gross taxable amount – notional deduction

= 46500 – 18600

3

Fringe benefits are those which are provided additionally or can say specifically to some

employees. Same has been done in given case under which a loan is provided by bank to its

employee Brian and that too at a rate of 1% interest. As the rate is less that what is set by

industry so there will be benefits which are included in it. That rate which is specified at which

interest is to be paid is 5.65% for financial year 2016-17. So the amount of taxable benefits will

be calculated by identifying the variation between interest that is to be paid according to

statutory rates and actual rate. The manner in which it will be calculated is provided here under.

Calculation of Taxable fringe benefits:

Step 1: Calculation of gross taxable amount:

Actual Interest = Loan amount * 1/100

= $1000000 * 1/100

=$10000

Statutory interest = $1000000 * 5.65/100

= $56500

Gross taxable Amount of benefit = $56500 - $10000 = $46500

Step 2: Value of benefits if no interest is paid:

= $1000000 * 5.65 /100

= $56500

Step 3: Deduction allowed to Brian in respect of statutory interest:

= $56500 * 40/100

= $22600

Step 4: Deduction allowed to Brian in respect of Actual interest:

= $10000 * 40/100

= $4000

Step 5: Notional Deduction which will be provided to Brian:

= $22600 - $4000

= $18600

Step 6: Calculation of net taxable amount:

= Gross taxable amount – notional deduction

= 46500 – 18600

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= $27900

So the net amount of fringe benefits on which tax will be paid is $ 27900.

In order to make the monthly payments equated instalments will be required to be

determined and for this total liability is to be divided among 12 months period.

According to the next situation which demands that no interest will be paid, then in this case

amount of fringe benefit will be as follows:

= (loan amount * 5.65%) * 60%

= ($1000000 * 5.65%) * 60%

= $56500 * 60%

= $33900

So the taxable fringe benefits are $33900.

Supportive evidence:

Under this provisions which are specified under fringe benefit tax policy will be required

to be followed (Kaplow, 2011). The amount on which tax is to be paid is to be determined and in

this interest that is calculated on notional basis will be higher than that which are paid in actual

manner. In order to identify the total value of fringe benefits all the loans that are received by

employee will be considered differently. So calculation will have to be made separately and then

at last it shall be accumulated to have final value.

Conclusion

From all the discussion and practical problem it has been identified that the amount

which will be provided by employer in form of additional benefit to employee is taxable in hands

of employee. The manner in which amount will be calculated is also determined for which

various measurements are made. There will be deduction that is allowed on taxable value upto

the amount which is utilised for advantage of business. So that will have to be deducted from

total value so that net amount can be attained.

QUESTION 3

Introduction

In process of purchase, there will be requirement of some borrowings so that liabilities

can be met. In given case Jack and Jill are to purchase a rental property and for that they have

borrowed some amount. As they are sharing the property so agreement is made according to

4

So the net amount of fringe benefits on which tax will be paid is $ 27900.

In order to make the monthly payments equated instalments will be required to be

determined and for this total liability is to be divided among 12 months period.

According to the next situation which demands that no interest will be paid, then in this case

amount of fringe benefit will be as follows:

= (loan amount * 5.65%) * 60%

= ($1000000 * 5.65%) * 60%

= $56500 * 60%

= $33900

So the taxable fringe benefits are $33900.

Supportive evidence:

Under this provisions which are specified under fringe benefit tax policy will be required

to be followed (Kaplow, 2011). The amount on which tax is to be paid is to be determined and in

this interest that is calculated on notional basis will be higher than that which are paid in actual

manner. In order to identify the total value of fringe benefits all the loans that are received by

employee will be considered differently. So calculation will have to be made separately and then

at last it shall be accumulated to have final value.

Conclusion

From all the discussion and practical problem it has been identified that the amount

which will be provided by employer in form of additional benefit to employee is taxable in hands

of employee. The manner in which amount will be calculated is also determined for which

various measurements are made. There will be deduction that is allowed on taxable value upto

the amount which is utilised for advantage of business. So that will have to be deducted from

total value so that net amount can be attained.

QUESTION 3

Introduction

In process of purchase, there will be requirement of some borrowings so that liabilities

can be met. In given case Jack and Jill are to purchase a rental property and for that they have

borrowed some amount. As they are sharing the property so agreement is made according to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which 90 percent share of profits will be provided to Jill and remaining 10 percent is received by

Jack (Dhami and Al-Nowaihi, 2010). The losses, if made will be borne wholly by Jack and no

share of it will be met by Jill. They are considering to sell the property because of loss of $10000

which is faced by them in last year. Due to this there will be capital gain or loss which has be

dealt with.

Critical analysis

The deduction can be availed on the amount which is spend on maintenance by Jack. The

benefit of this can be taken by only one person so if it will be claimed by Jill then it will not be

available to his wife. All the deductions which are there can be carried forward by any person for

that period which is specified. Therefore expenditure made on borrowing and depreciation which

is charged on property are to carried in future period. Other then this there are some expenses on

which deduction can be availed in same year and an example of this is interest which is charged

on loan and by this liability to be met will be reduced. All the other expense which are not paid

by them cannot be claimed in order to decrease the amount on which tax will be paid. As the

case is in relation to residential property so the provisions of GST will not be applicable on Jack

and Jill (Choné and Laroque, 2011). In last year there was loss of 10000 and it shall be noted that

this will not be allowed for the purpose of deduction. The profit or loss which will be arising by

selling of property is to be considered as capital gain or loss. So in that situation tax will have to

be paid on the amount of gain that is earned by Jack. They have made an agreement so that tax

saving can be achieved but it is not possible in given situation. All the gain will be used to set off

the loss which is made in past years and if loss will be made then it shall be kept to be utilised in

coming period.

Supportive evidence

The deduction will be allowed to any person in respect of only those expenses which

have been paid by them and this is specified by the Australian tax authorities. Therefore it will

have to be followed by all. The set off will be made under this head only which means that if

there will be any loss then it can be deducted from the capital gains. It is provided under law that

if there is any income which is earned by any dependent then it shall be clubbed in hands of their

guardian (Albertazzi and Gambacorta, 2010). Same will be applying in case of capital gains also

and they will also be accumulated in income of parent.

5

Jack (Dhami and Al-Nowaihi, 2010). The losses, if made will be borne wholly by Jack and no

share of it will be met by Jill. They are considering to sell the property because of loss of $10000

which is faced by them in last year. Due to this there will be capital gain or loss which has be

dealt with.

Critical analysis

The deduction can be availed on the amount which is spend on maintenance by Jack. The

benefit of this can be taken by only one person so if it will be claimed by Jill then it will not be

available to his wife. All the deductions which are there can be carried forward by any person for

that period which is specified. Therefore expenditure made on borrowing and depreciation which

is charged on property are to carried in future period. Other then this there are some expenses on

which deduction can be availed in same year and an example of this is interest which is charged

on loan and by this liability to be met will be reduced. All the other expense which are not paid

by them cannot be claimed in order to decrease the amount on which tax will be paid. As the

case is in relation to residential property so the provisions of GST will not be applicable on Jack

and Jill (Choné and Laroque, 2011). In last year there was loss of 10000 and it shall be noted that

this will not be allowed for the purpose of deduction. The profit or loss which will be arising by

selling of property is to be considered as capital gain or loss. So in that situation tax will have to

be paid on the amount of gain that is earned by Jack. They have made an agreement so that tax

saving can be achieved but it is not possible in given situation. All the gain will be used to set off

the loss which is made in past years and if loss will be made then it shall be kept to be utilised in

coming period.

Supportive evidence

The deduction will be allowed to any person in respect of only those expenses which

have been paid by them and this is specified by the Australian tax authorities. Therefore it will

have to be followed by all. The set off will be made under this head only which means that if

there will be any loss then it can be deducted from the capital gains. It is provided under law that

if there is any income which is earned by any dependent then it shall be clubbed in hands of their

guardian (Albertazzi and Gambacorta, 2010). Same will be applying in case of capital gains also

and they will also be accumulated in income of parent.

5

Conclusion

It has been noted that the agreement is made in which 90 percent share is transferred to

wife so that tax can be saved on that amount. But this has not been possible and they are required

to pay the whole tax as no deduction is made in respect of expenses which are made by others.

So by clubbing also they will not be exempted from liability of tax which is to be met.

QUESTION 4

Introduction

All the persons who will be earning income will try to find out the ways by which they

can save the tax that is to be paid on it (Grochulski and Piskorski, 2010). There are various

complex processes which are involved due to this accountants keeps on finding such ways by

which taxable income can be reduced. In respect of this there are many cases which can be

considered but the one that is most popular is IRC v/s Duke of Westminster which took place in

1936. This was used as reference by many people so that tax can be avoided. But with time new

cases keep coming and that reduced its importance to some extent. In them it was found that

people are using such structures which are complex so that tax saving can be attained and were

proved guilty for this.

Critical analysis

In the case of IRC v/s Duke of Westminster there is an appointment which is made of

gardener with whom it has been settled that all the payments that will be made by Duke to him

will be allowed as tax deductions. By this taxable income will be reduced and they will have to

pay less amount of tax. It can be said that a way was found out of the complex procedure to earn

maximum benefits. A case was filed against him by IRC in which it was stated that liabilty in

respect of tax has been reduced by Duke so that he will have to pay lesser amount. In this

judgement was provided by court in favour of Westminster in which it was decided that Duke

has not committed any offence as all that id being done by him is legally acceptable and it was

stated that if less tax is paid by following all procedures and laws then that person will not be

considered as guilty. There is no power with IRC in such case by which it can force the other

party to make payment of more amount.

As per the contracts which are made for employment it is essential that there shall be

timely payments which are to be made (Rothschild and Scheuer, 2013). In the given case

6

It has been noted that the agreement is made in which 90 percent share is transferred to

wife so that tax can be saved on that amount. But this has not been possible and they are required

to pay the whole tax as no deduction is made in respect of expenses which are made by others.

So by clubbing also they will not be exempted from liability of tax which is to be met.

QUESTION 4

Introduction

All the persons who will be earning income will try to find out the ways by which they

can save the tax that is to be paid on it (Grochulski and Piskorski, 2010). There are various

complex processes which are involved due to this accountants keeps on finding such ways by

which taxable income can be reduced. In respect of this there are many cases which can be

considered but the one that is most popular is IRC v/s Duke of Westminster which took place in

1936. This was used as reference by many people so that tax can be avoided. But with time new

cases keep coming and that reduced its importance to some extent. In them it was found that

people are using such structures which are complex so that tax saving can be attained and were

proved guilty for this.

Critical analysis

In the case of IRC v/s Duke of Westminster there is an appointment which is made of

gardener with whom it has been settled that all the payments that will be made by Duke to him

will be allowed as tax deductions. By this taxable income will be reduced and they will have to

pay less amount of tax. It can be said that a way was found out of the complex procedure to earn

maximum benefits. A case was filed against him by IRC in which it was stated that liabilty in

respect of tax has been reduced by Duke so that he will have to pay lesser amount. In this

judgement was provided by court in favour of Westminster in which it was decided that Duke

has not committed any offence as all that id being done by him is legally acceptable and it was

stated that if less tax is paid by following all procedures and laws then that person will not be

considered as guilty. There is no power with IRC in such case by which it can force the other

party to make payment of more amount.

As per the contracts which are made for employment it is essential that there shall be

timely payments which are to be made (Rothschild and Scheuer, 2013). In the given case

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gardener was hired but he was not paid any monthly or weekly payments by Duke. It was

identified by authorities that people are finding such ways by which they can save tax in legal

manner. Due to this reason such laws were brought by which it has become more difficult to

avoid the tax payment. Various cases were provided on the basis of which decisions are made.

Supporting evidence

In the process of tax avoidance the above mentioned case is most important. It was

believed that if any law is wrong then in that case payment cannot be forced but this was proved

wrong by case of Lord Tomlin (A reconciliation of recent results in optimal taxation theory,

2017). It was provided that if any step is taken in order to save tax and there is no other purpose

of it then it will be required that whole of the amount will have to be taxed.

Conclusion.

From the above discussion it can be said that no one can be forced to pay tax if they are

using legal means for tax saving. It is also provided that with coming of more cases this has

become difficult to avoid the tax payments as now laws are made in all the aspects from which it

could have been saved.

QUESTION 5

Introduction

In this case there is revenue which is generated by providing the land to timber producers

who will be paying money in return to timber (Weinzierl, 2014). For this pine trees will be cut

and this shall be done as Bill wants his land to be cleared. There are options under which he is

offered $1000 for every 100 meters of timer. This case is covered under rules set for production

and forestry and the one for given case is rule 95/6. under this all the revenues whether related to

forestry or not will be included if they are earned by means of timber sale. The treatment which

will be provided in respect of tax under such situation are provided under such rulings and there

shall be some amount which will be allowed as deduction.

Critical analysis

In the present case Mr bill is giving his land foe clearance purpose and for that he will be

paid a fixed amount. Although the situation is not covered under forestry activities but then also

rules will be applied as the final outcome is that disposing of forest item is taking place. Due to

this reason all the incomes which will be earned by him are exempted and no tax will have to be

7

identified by authorities that people are finding such ways by which they can save tax in legal

manner. Due to this reason such laws were brought by which it has become more difficult to

avoid the tax payment. Various cases were provided on the basis of which decisions are made.

Supporting evidence

In the process of tax avoidance the above mentioned case is most important. It was

believed that if any law is wrong then in that case payment cannot be forced but this was proved

wrong by case of Lord Tomlin (A reconciliation of recent results in optimal taxation theory,

2017). It was provided that if any step is taken in order to save tax and there is no other purpose

of it then it will be required that whole of the amount will have to be taxed.

Conclusion.

From the above discussion it can be said that no one can be forced to pay tax if they are

using legal means for tax saving. It is also provided that with coming of more cases this has

become difficult to avoid the tax payments as now laws are made in all the aspects from which it

could have been saved.

QUESTION 5

Introduction

In this case there is revenue which is generated by providing the land to timber producers

who will be paying money in return to timber (Weinzierl, 2014). For this pine trees will be cut

and this shall be done as Bill wants his land to be cleared. There are options under which he is

offered $1000 for every 100 meters of timer. This case is covered under rules set for production

and forestry and the one for given case is rule 95/6. under this all the revenues whether related to

forestry or not will be included if they are earned by means of timber sale. The treatment which

will be provided in respect of tax under such situation are provided under such rulings and there

shall be some amount which will be allowed as deduction.

Critical analysis

In the present case Mr bill is giving his land foe clearance purpose and for that he will be

paid a fixed amount. Although the situation is not covered under forestry activities but then also

rules will be applied as the final outcome is that disposing of forest item is taking place. Due to

this reason all the incomes which will be earned by him are exempted and no tax will have to be

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

paid on it. But if the payment is received in lump sum of $50000 then it will be included in forest

operations and so are covered under the income on which tax is charged. So liability to make the

payment of tax will be borne by Mr. Bill. Therefore both the cases will have to dealt by in

different manner as they are related to separate regulations.

Supporting evidence

The given case will be covered under such condition in which forest operation is not

taking place but selling is being done of timber. Here land is provided in order to remove the

trees and the amount received will be treated as royalty which is not any forest operations as all

the trees are not planted with this intention (Chiorazzo and Milani, 2011). Due to all these

reasons there will be no liability on Mr Bill to pay any tax on such revenue. But it has been

provided that it will be treated as operation of forest of the payment will be made in lump sum

and then the treatment that is to be provided is different. Now tax shall be paid on the amount of

$50000 at such rate which is specified by taxation department.

Conclusion

It can be said that all the operations which are related to trees will not be covered under

forest operation. There are other criteria also which shall be met in order to have the law of

forestry to become applicable. It has been found that tax payment will be made only in respect of

those transactions on which amount will be received once and not in any instalments or on basis

of some other condition. For this purpose assessable amount will have to be calculated so that

amount to be paid can be identified.

8

operations and so are covered under the income on which tax is charged. So liability to make the

payment of tax will be borne by Mr. Bill. Therefore both the cases will have to dealt by in

different manner as they are related to separate regulations.

Supporting evidence

The given case will be covered under such condition in which forest operation is not

taking place but selling is being done of timber. Here land is provided in order to remove the

trees and the amount received will be treated as royalty which is not any forest operations as all

the trees are not planted with this intention (Chiorazzo and Milani, 2011). Due to all these

reasons there will be no liability on Mr Bill to pay any tax on such revenue. But it has been

provided that it will be treated as operation of forest of the payment will be made in lump sum

and then the treatment that is to be provided is different. Now tax shall be paid on the amount of

$50000 at such rate which is specified by taxation department.

Conclusion

It can be said that all the operations which are related to trees will not be covered under

forest operation. There are other criteria also which shall be met in order to have the law of

forestry to become applicable. It has been found that tax payment will be made only in respect of

those transactions on which amount will be received once and not in any instalments or on basis

of some other condition. For this purpose assessable amount will have to be calculated so that

amount to be paid can be identified.

8

REFERENCES

Book and Journals:

Albertazzi, U. and Gambacorta, L., 2010. Bank profitability and taxation. Journal of Banking &

Finance. 34(11). pp.2801-2810.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Chiorazzo, V. and Milani, C., 2011. The impact of taxation on bank profits: Evidence from EU

banks. Journal of Banking & Finance. 35(12). pp.3202-3212.

Choné, P. and Laroque, G., 2011. Optimal taxation in the extensive model. Journal of Economic

Theory. 146(2). pp.425-453.

Dhami, S. and Al-Nowaihi, A., 2010. Optimal taxation in the presence of tax evasion: Expected

utility versus prospect theory. Journal of Economic Behavior & Organization. 75(2).

pp.313-337.

Grochulski, B. and Piskorski, T., 2010. Risky human capital and deferred capital income

taxation. Journal of Economic Theory. 145(3). pp.908-943.

Kaplow, L., 2011. The theory of taxation and public economics. Princeton University Press.

McGee, R.W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Rothschild, C. and Scheuer, F., 2013. Redistributive taxation in the roy model. The Quarterly

Journal of Economics. 128(2). pp.623-668.

Weinzierl, M., 2014. The promise of positive optimal taxation: normative diversity and a role for

equal sacrifice. Journal of Public Economics. 118. pp.128-142.

Online

A reconciliation of recent results in optimal taxation theory. 2017. [Online]. Available through:

<http://www.sciencedirect.com/science/article/pii/0047272779900112>. [Accessed on

18th September 2017].

9

Book and Journals:

Albertazzi, U. and Gambacorta, L., 2010. Bank profitability and taxation. Journal of Banking &

Finance. 34(11). pp.2801-2810.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Chiorazzo, V. and Milani, C., 2011. The impact of taxation on bank profits: Evidence from EU

banks. Journal of Banking & Finance. 35(12). pp.3202-3212.

Choné, P. and Laroque, G., 2011. Optimal taxation in the extensive model. Journal of Economic

Theory. 146(2). pp.425-453.

Dhami, S. and Al-Nowaihi, A., 2010. Optimal taxation in the presence of tax evasion: Expected

utility versus prospect theory. Journal of Economic Behavior & Organization. 75(2).

pp.313-337.

Grochulski, B. and Piskorski, T., 2010. Risky human capital and deferred capital income

taxation. Journal of Economic Theory. 145(3). pp.908-943.

Kaplow, L., 2011. The theory of taxation and public economics. Princeton University Press.

McGee, R.W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Rothschild, C. and Scheuer, F., 2013. Redistributive taxation in the roy model. The Quarterly

Journal of Economics. 128(2). pp.623-668.

Weinzierl, M., 2014. The promise of positive optimal taxation: normative diversity and a role for

equal sacrifice. Journal of Public Economics. 118. pp.128-142.

Online

A reconciliation of recent results in optimal taxation theory. 2017. [Online]. Available through:

<http://www.sciencedirect.com/science/article/pii/0047272779900112>. [Accessed on

18th September 2017].

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.