Taxation Law Assignment: Exploring Taxation Law in Australia

VerifiedAdded on 2019/11/26

|12

|2206

|218

Homework Assignment

AI Summary

This taxation law assignment delves into several key aspects of Australian taxation. It begins by examining capital gains and losses derived from asset sales, referencing ITAA 1997 sections. The assignment then explores Fringe Benefit Tax (FBT) calculations, referencing Taxation Ruling TR 93/6. The third section focuses on the allocation of losses from rental properties under joint ownership, referencing ITAA 1997 section 51 and TR 93/32. The assignment also analyzes tax avoidance principles, citing IRC v Duke of Westminster [1936] AC 1. Finally, it assesses income from the sale of felled timber, referencing the Income Tax Assessment Act 1936, subsection 6(1) and the case of McCauley v. The Federal Commissioner of Taxation. Each section includes the relevant laws, applications, and conclusions to provide a comprehensive understanding of the tax issues.

Running head: TAXATION LAW

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................4

Application.................................................................................................................................4

Application:................................................................................................................................5

Conclusion:................................................................................................................................5

Answer to question 3..................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

Laws:..........................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................4

Application.................................................................................................................................4

Application:................................................................................................................................5

Conclusion:................................................................................................................................5

Answer to question 3..................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

Laws:..........................................................................................................................................8

2TAXATION LAW

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference List:.........................................................................................................................11

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference List:.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

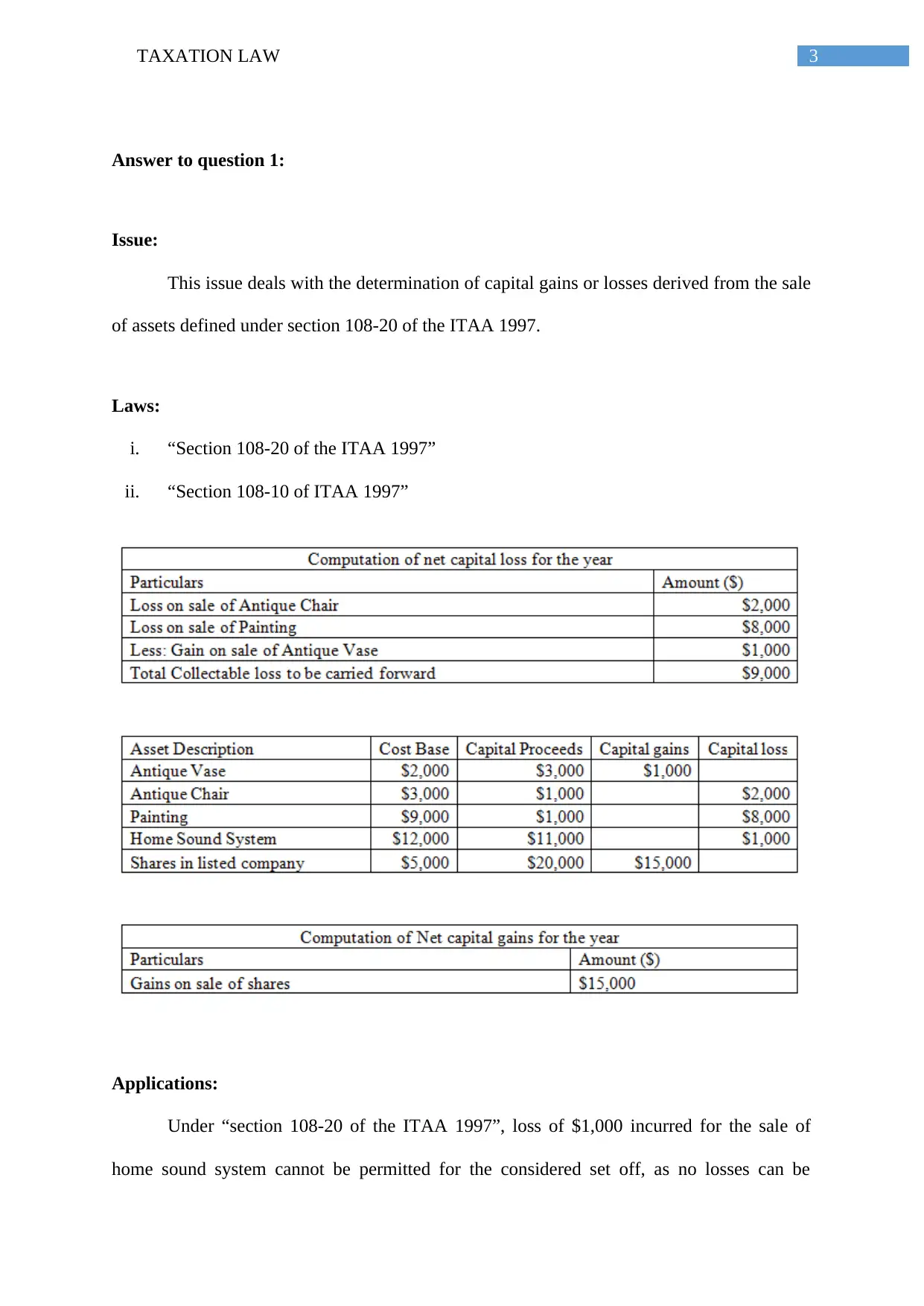

Answer to question 1:

Issue:

This issue deals with the determination of capital gains or losses derived from the sale

of assets defined under section 108-20 of the ITAA 1997.

Laws:

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Applications:

Under “section 108-20 of the ITAA 1997”, loss of $1,000 incurred for the sale of

home sound system cannot be permitted for the considered set off, as no losses can be

Answer to question 1:

Issue:

This issue deals with the determination of capital gains or losses derived from the sale

of assets defined under section 108-20 of the ITAA 1997.

Laws:

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Applications:

Under “section 108-20 of the ITAA 1997”, loss of $1,000 incurred for the sale of

home sound system cannot be permitted for the considered set off, as no losses can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

considered based on the disposal of personal use assets. In accordance with the section 108-

10 of the ITAA 1997, the collectable losses cannot be set off against the common gains in the

form of sales of shares (Kenny 2013). Additionally, the offset can also be considered

according to Section 108-10 of ITAA 1997. As Eric has gained profit on the disposal of

ordinary assets and there are no current year ordinary capital or other kind of applicable

reductions. Additionally, the capital gain for Eric has current stands as $15,000.

Conclusion:

It can be concluded that Eric cannot offset the loss from collectibles since he has only

gained profit from the disposal of ordinary assets.

Answer to question 2:

Issue:

The below stated issue is concerned with the ascertainment of FBT in accordance

with the “Taxation Ruling of TR 93/6”.

Laws:

i. Taxation rulings of TR 93/6

Application

Computation of Fringe Benefit Tax

considered based on the disposal of personal use assets. In accordance with the section 108-

10 of the ITAA 1997, the collectable losses cannot be set off against the common gains in the

form of sales of shares (Kenny 2013). Additionally, the offset can also be considered

according to Section 108-10 of ITAA 1997. As Eric has gained profit on the disposal of

ordinary assets and there are no current year ordinary capital or other kind of applicable

reductions. Additionally, the capital gain for Eric has current stands as $15,000.

Conclusion:

It can be concluded that Eric cannot offset the loss from collectibles since he has only

gained profit from the disposal of ordinary assets.

Answer to question 2:

Issue:

The below stated issue is concerned with the ascertainment of FBT in accordance

with the “Taxation Ruling of TR 93/6”.

Laws:

i. Taxation rulings of TR 93/6

Application

Computation of Fringe Benefit Tax

5TAXATION LAW

Application:

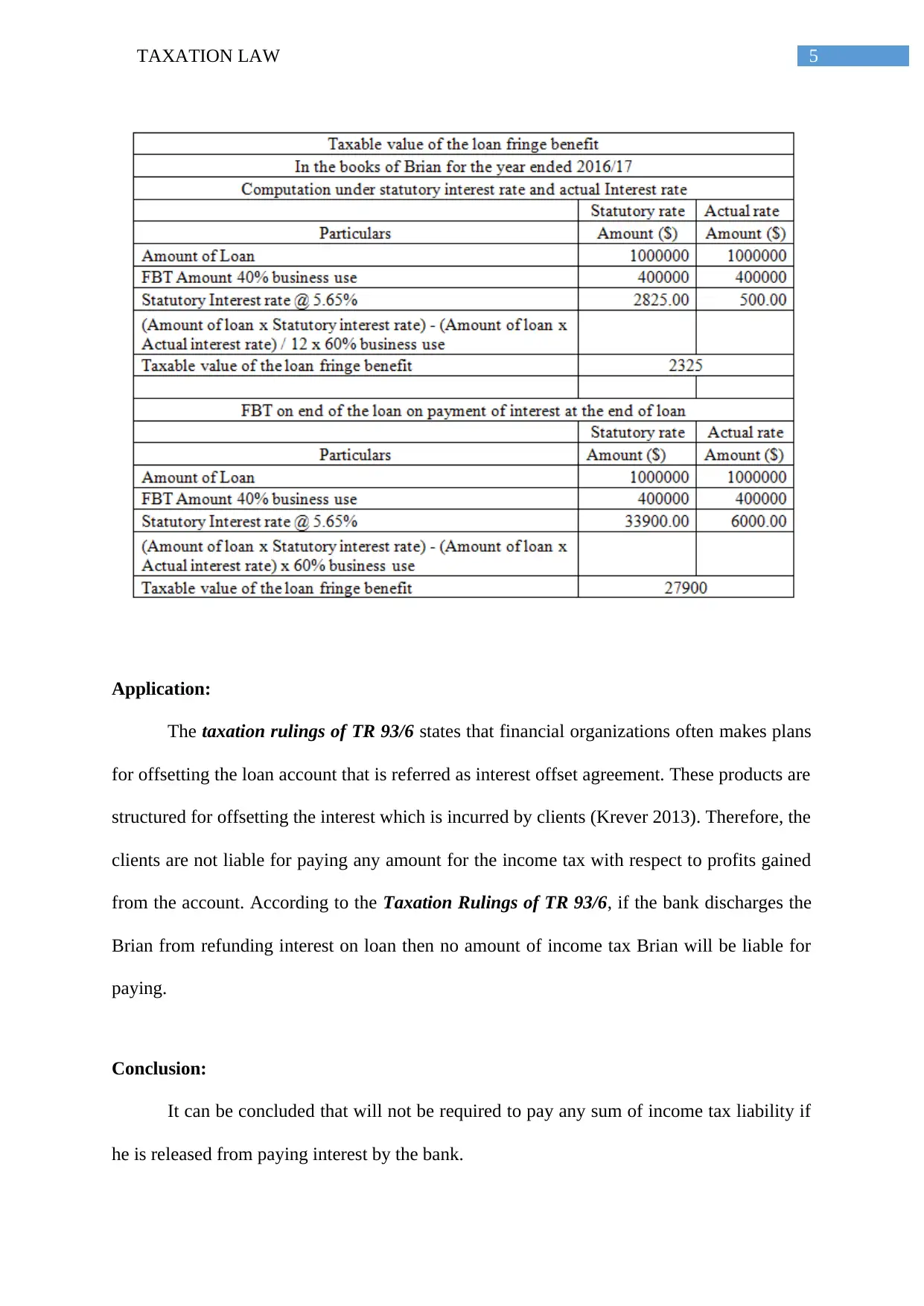

The taxation rulings of TR 93/6 states that financial organizations often makes plans

for offsetting the loan account that is referred as interest offset agreement. These products are

structured for offsetting the interest which is incurred by clients (Krever 2013). Therefore, the

clients are not liable for paying any amount for the income tax with respect to profits gained

from the account. According to the Taxation Rulings of TR 93/6, if the bank discharges the

Brian from refunding interest on loan then no amount of income tax Brian will be liable for

paying.

Conclusion:

It can be concluded that will not be required to pay any sum of income tax liability if

he is released from paying interest by the bank.

Application:

The taxation rulings of TR 93/6 states that financial organizations often makes plans

for offsetting the loan account that is referred as interest offset agreement. These products are

structured for offsetting the interest which is incurred by clients (Krever 2013). Therefore, the

clients are not liable for paying any amount for the income tax with respect to profits gained

from the account. According to the Taxation Rulings of TR 93/6, if the bank discharges the

Brian from refunding interest on loan then no amount of income tax Brian will be liable for

paying.

Conclusion:

It can be concluded that will not be required to pay any sum of income tax liability if

he is released from paying interest by the bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 3

Issue:

This question brings forward the issue that is connected with the allocation of loss

derived from the rental property as the joint ownership by Jack and Jill.

Laws:

i. Section 51 of the ITAA 1997

ii. Taxation rulings of TR 93/32

iii. F.C. of T. v McDonald (1987)

Application:

According to the taxation rulings of TR 93/32, it is consists of the explanation of the

divisionary net proceeds or generated loss from the property that is rented among the co-

owners of the considered property (Barton 2013). Additionally, the ruling is mainly

considered with the evaluation of taxable position of Co-owners those are not responsible for

carrying their values within actions. The current scenario in Jack and Jill considers the

evaluation of taxable position of the rental property. Jack is entitled for 10% of the property

and Jill is entitled for 90% from the property.

In accordance with the Taxation rulings, TR 92/32 Co-ownership of the property that

is rented which is known as one partnership relating to the income tax purpose but this is not

considered as one partnership at the general law except the co-ownership accounts for

carrying value for any business practice, where the Co-ownership is considered as the

partnership for satisfying the purpose of income tax only. The loss of income gained from the

rental property is managed through the Co-ownership of the property that is rented out as

Answer to question 3

Issue:

This question brings forward the issue that is connected with the allocation of loss

derived from the rental property as the joint ownership by Jack and Jill.

Laws:

i. Section 51 of the ITAA 1997

ii. Taxation rulings of TR 93/32

iii. F.C. of T. v McDonald (1987)

Application:

According to the taxation rulings of TR 93/32, it is consists of the explanation of the

divisionary net proceeds or generated loss from the property that is rented among the co-

owners of the considered property (Barton 2013). Additionally, the ruling is mainly

considered with the evaluation of taxable position of Co-owners those are not responsible for

carrying their values within actions. The current scenario in Jack and Jill considers the

evaluation of taxable position of the rental property. Jack is entitled for 10% of the property

and Jill is entitled for 90% from the property.

In accordance with the Taxation rulings, TR 92/32 Co-ownership of the property that

is rented which is known as one partnership relating to the income tax purpose but this is not

considered as one partnership at the general law except the co-ownership accounts for

carrying value for any business practice, where the Co-ownership is considered as the

partnership for satisfying the purpose of income tax only. The loss of income gained from the

rental property is managed through the Co-ownership of the property that is rented out as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

well as from the allocation of joint venture proceeds and losses (Morgan, Mortimer and Pinto

2013). The current condition of Jack and Jill shows the co-ownership for the rental property

between them which is based on the income tax purpose and cannot be regarded as the

partnership in consideration with the general law.

The taxation rulings of TR 92/32 states that co-owners of the property that is rented

out are usually not considered partners in association with the “General Law” (Milton 2013).

In this case the partnership agreement is either in the form of writing or oral that doesn’t have

consequence on the shared value of proceeds or loss from the considered rented property.

Therefore, Co-owners of the rental property Jack and Jill will hold the property as the joint

renters as one common factor.

As held in the case of “F.C. of T. v McDonald (1987)”, the taxpayer’s wife and he

legally owned two strata title units as the joint renters (Woellner 2013). The agreement

confirmed between them states that the net earnings gained from the property that is rented

out will be distributed as 25% to McDonald and 75% to Mrs McDonald. Now the total loss

amount will be borne by Mr McDonald.

Conclusion:

It can be concluded from the above discussion that both Jack and Jill are required to

distribute the loss equally and joint ownership does not accounts as partnership business.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1 was regularly quoted as the occurrence of

tax avoidance. This case established one principle that states each man is allowed to order his

affairs for allowing the taxation assigning which is made in fitting Act. This taxation

assigning is less than it (Barkoczy 2016). Though it cannot be considered that this ruling was

well as from the allocation of joint venture proceeds and losses (Morgan, Mortimer and Pinto

2013). The current condition of Jack and Jill shows the co-ownership for the rental property

between them which is based on the income tax purpose and cannot be regarded as the

partnership in consideration with the general law.

The taxation rulings of TR 92/32 states that co-owners of the property that is rented

out are usually not considered partners in association with the “General Law” (Milton 2013).

In this case the partnership agreement is either in the form of writing or oral that doesn’t have

consequence on the shared value of proceeds or loss from the considered rented property.

Therefore, Co-owners of the rental property Jack and Jill will hold the property as the joint

renters as one common factor.

As held in the case of “F.C. of T. v McDonald (1987)”, the taxpayer’s wife and he

legally owned two strata title units as the joint renters (Woellner 2013). The agreement

confirmed between them states that the net earnings gained from the property that is rented

out will be distributed as 25% to McDonald and 75% to Mrs McDonald. Now the total loss

amount will be borne by Mr McDonald.

Conclusion:

It can be concluded from the above discussion that both Jack and Jill are required to

distribute the loss equally and joint ownership does not accounts as partnership business.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1 was regularly quoted as the occurrence of

tax avoidance. This case established one principle that states each man is allowed to order his

affairs for allowing the taxation assigning which is made in fitting Act. This taxation

assigning is less than it (Barkoczy 2016). Though it cannot be considered that this ruling was

8TAXATION LAW

very attractive for others for seeking the avoidance of tax with respect to law’s complex

structures and these are weakened by the subsequent cases where the courts have looked on

the overall impact. Citing an example of the court in the upcoming stages are more restrictive

and were adopted under the WT Ramsay v. IRC principle. In this case the transaction has pre-

arranged artificially and this is served not in the form of commercial purpose (Braithwaite

2017). The perfect rule was to impose tax for extending the transaction as a total fact.

In the contemporary situation, this principle within Australia depicts that if an

individual achieves success for making this result secured, then the Inland Revenue might be

of their initiative and they cannot be forced to pay any increased amount of tax (Saad 2014).

Additionally, it is understood that this aspect allows individuals and corporations for

structuring the financial agreements with respect to their fixed objectives of decreasing the

tax liabilities based on their structures within the structure of laws.

Answer to question 5:

Issue:

In the contemporary scenario assessment of income from the sale of felled timber is

analysed under “subsection 6 (1) of the Income Tax Assessment Act 1936”.

Laws:

i. “Subsection 6 (1) of the Income Tax Assessment Act 1936”

ii. “McCauley v. The Federal Commissioner of Taxation”

Application:

In the contemporary scenario, this is found that Bill owns a large piece of land on

which there are several pine trees. Bill primarily aimed to use the land for grazing sheep and

very attractive for others for seeking the avoidance of tax with respect to law’s complex

structures and these are weakened by the subsequent cases where the courts have looked on

the overall impact. Citing an example of the court in the upcoming stages are more restrictive

and were adopted under the WT Ramsay v. IRC principle. In this case the transaction has pre-

arranged artificially and this is served not in the form of commercial purpose (Braithwaite

2017). The perfect rule was to impose tax for extending the transaction as a total fact.

In the contemporary situation, this principle within Australia depicts that if an

individual achieves success for making this result secured, then the Inland Revenue might be

of their initiative and they cannot be forced to pay any increased amount of tax (Saad 2014).

Additionally, it is understood that this aspect allows individuals and corporations for

structuring the financial agreements with respect to their fixed objectives of decreasing the

tax liabilities based on their structures within the structure of laws.

Answer to question 5:

Issue:

In the contemporary scenario assessment of income from the sale of felled timber is

analysed under “subsection 6 (1) of the Income Tax Assessment Act 1936”.

Laws:

i. “Subsection 6 (1) of the Income Tax Assessment Act 1936”

ii. “McCauley v. The Federal Commissioner of Taxation”

Application:

In the contemporary scenario, this is found that Bill owns a large piece of land on

which there are several pine trees. Bill primarily aimed to use the land for grazing sheep and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

wanted to have it cleared. Bill discovers a logging company that prepared to pay him $1000

for every 100 meters of timber. The logging companies can grab from his piece of land. The

taxation ruling related to 95/6, set down the income tax consequences generating from the

activities of primary production and forestry (Woellner et al. 2016). The ruling offers the

limit to which the receipts that is derived from the sale of timber. This aspect constitutes

assessable income whether the tax payers are indulged into the activities of forestry industry.

According to subsection 6 (1) of the Income Tax Assessment Act 1936 the tax payer is

indulged into the activities of forest operations is known as the primary creator.

In accordance with the “subsection 6 (1), the Income Tax Assessment Act 1936”,

primary production is commonly defined as the planting of trees within plantation which is

required for felling forest (Robin 2017). As an evidence from the case study, the Bill is

regarded as the basic producer since he has indulged into the processes of primary production

“subsection 6 (1) of the Income Tax Assessment Act 1936”. The forest operations include

felling of trees in a forest or plantation though the tax payers are not concerned about the

planted trees.

Being the possessor of large piece of land, bill did not planted the trees but the whole

amount of receipts that was derived by Bill from the sale of felled timber constitutes

assessable earning of the considered tax payers disposes about the trees that have not

necessarily planted by the tax payer and rendered for the goal of sale forms the part of

assessable income. In spite of these facts, the considered sales combines either completely or

partial assets of a business, the considered trees are taken as assessable income of the tax

payers under “subsection 6 (1) of the Income Tax Assessment Act 1936”.

Conversely, if the tax payer was simply paid a lump sum of $50,000 by surrendering

the right to the logging organization for removing the necessary amount of timber, then that

wanted to have it cleared. Bill discovers a logging company that prepared to pay him $1000

for every 100 meters of timber. The logging companies can grab from his piece of land. The

taxation ruling related to 95/6, set down the income tax consequences generating from the

activities of primary production and forestry (Woellner et al. 2016). The ruling offers the

limit to which the receipts that is derived from the sale of timber. This aspect constitutes

assessable income whether the tax payers are indulged into the activities of forestry industry.

According to subsection 6 (1) of the Income Tax Assessment Act 1936 the tax payer is

indulged into the activities of forest operations is known as the primary creator.

In accordance with the “subsection 6 (1), the Income Tax Assessment Act 1936”,

primary production is commonly defined as the planting of trees within plantation which is

required for felling forest (Robin 2017). As an evidence from the case study, the Bill is

regarded as the basic producer since he has indulged into the processes of primary production

“subsection 6 (1) of the Income Tax Assessment Act 1936”. The forest operations include

felling of trees in a forest or plantation though the tax payers are not concerned about the

planted trees.

Being the possessor of large piece of land, bill did not planted the trees but the whole

amount of receipts that was derived by Bill from the sale of felled timber constitutes

assessable earning of the considered tax payers disposes about the trees that have not

necessarily planted by the tax payer and rendered for the goal of sale forms the part of

assessable income. In spite of these facts, the considered sales combines either completely or

partial assets of a business, the considered trees are taken as assessable income of the tax

payers under “subsection 6 (1) of the Income Tax Assessment Act 1936”.

Conversely, if the tax payer was simply paid a lump sum of $50,000 by surrendering

the right to the logging organization for removing the necessary amount of timber, then that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

receipt of sum will be considered as “Royalties”. In agreement with the section 26 (f) receipt

of “royalties” from the tax payer on granting the right to fell the timber on land obtained by

the tax payer (Barkoczy et al. 2016). Under this kind of situations, Bill will not be considered

as carrying on the trade of forest operations. Here it is considered that the tax payers did not

planted the trees for sake of gaining profit from that. As held in McCauley v. The Federal

Commissioner of Taxation payments obtained by the grantor is under the right of doing so.

The amounts those are receipted by Bill as royalty combines assessable income under section

26 (f).

Conclusion:

It can be concluded that receiving income from cutting the timber will be considered

as taxable proceeds under subsection 6 (1) of the ITAA 1997.

receipt of sum will be considered as “Royalties”. In agreement with the section 26 (f) receipt

of “royalties” from the tax payer on granting the right to fell the timber on land obtained by

the tax payer (Barkoczy et al. 2016). Under this kind of situations, Bill will not be considered

as carrying on the trade of forest operations. Here it is considered that the tax payers did not

planted the trees for sake of gaining profit from that. As held in McCauley v. The Federal

Commissioner of Taxation payments obtained by the grantor is under the right of doing so.

The amounts those are receipted by Bill as royalty combines assessable income under section

26 (f).

Conclusion:

It can be concluded that receiving income from cutting the timber will be considered

as taxable proceeds under subsection 6 (1) of the ITAA 1997.

11TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G., 2016. Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Barton, 2013. Management of the Australian Taxation Office's property portfolio. ACT:

Australian National Audit Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Milton, 2013. The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G., 2016. Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Barton, 2013. Management of the Australian Taxation Office's property portfolio. ACT:

Australian National Audit Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Milton, 2013. The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.