Holmes Institute HA3042 Taxation Law Assignment: Individual Tax

VerifiedAdded on 2022/10/18

|12

|2932

|264

Homework Assignment

AI Summary

This assignment solution addresses key aspects of Australian taxation law, focusing on individual tax scenarios. The first part of the assignment analyzes Jasmine's tax liabilities, examining capital gains tax (CGT) implications from the sale of her family home (pre-CGT asset), a car (personal use asset), and business assets (small business concessions). It also covers the sale of furniture and paintings (collectables), determining whether CGT is applicable. The second part focuses on depreciating assets, specifically a CNC machine purchased by John, and the allowable deductions for its decline in value. The solution applies relevant sections of the ITA Act 1997, including those related to CGT events, small business concessions, and capital allowances, providing a detailed analysis of each scenario and the applicable tax implications.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Sale of family home:

A gain is generally branded capital since it is not the subject of income inside the

ordinary earnings concepts. The regime of capital gains has begun on 20/9/1985 and it brings

the capital earnings in the tax base (Lam & Whitney, 2016). The income tax liability of the

taxpayer also includes the net capital gains. Any gains that is made before this date is termed

as “pre-CGT” and it does not attracts any capital gains tax.

There are some basic exemption which is available to the taxpayer from the capital

gains or capital loss transpiring from CGT event. Main residence exemption is available only

under “sec 118-110 (1) ITA Act 1997” when the taxpayer is treated as individual and the

house was the main place of dwelling during the ownership period (Phan, 2016).

Jasmine here lived in the dwelling that she has purchased for $40,000. As she is

relocating to UK permanently, the dwelling was eventually sold for $650,000. It must be

noted that dwelling is a pre-CGT asset because Jasmine has purchased it before 20th

September 1985. As a result the capital gains that she has made from the main dwelling will

exempted from CGT.

Sale of car:

“Section 108.5 ITA Act 1997” says that CGT asset usually encompasses any property

or lawful or equitable right (Armstrong, 2016). A CGT event is identified as occurrence for

particular assets that determines the net capital gains or loss from such event. A “CGT event

A1” under “sec 104-10 (1) ITA Act 1997” commonly applies to majority of the assets that

are disposed.

Answer to question 1:

Sale of family home:

A gain is generally branded capital since it is not the subject of income inside the

ordinary earnings concepts. The regime of capital gains has begun on 20/9/1985 and it brings

the capital earnings in the tax base (Lam & Whitney, 2016). The income tax liability of the

taxpayer also includes the net capital gains. Any gains that is made before this date is termed

as “pre-CGT” and it does not attracts any capital gains tax.

There are some basic exemption which is available to the taxpayer from the capital

gains or capital loss transpiring from CGT event. Main residence exemption is available only

under “sec 118-110 (1) ITA Act 1997” when the taxpayer is treated as individual and the

house was the main place of dwelling during the ownership period (Phan, 2016).

Jasmine here lived in the dwelling that she has purchased for $40,000. As she is

relocating to UK permanently, the dwelling was eventually sold for $650,000. It must be

noted that dwelling is a pre-CGT asset because Jasmine has purchased it before 20th

September 1985. As a result the capital gains that she has made from the main dwelling will

exempted from CGT.

Sale of car:

“Section 108.5 ITA Act 1997” says that CGT asset usually encompasses any property

or lawful or equitable right (Armstrong, 2016). A CGT event is identified as occurrence for

particular assets that determines the net capital gains or loss from such event. A “CGT event

A1” under “sec 104-10 (1) ITA Act 1997” commonly applies to majority of the assets that

are disposed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

An important explanation regarding personal use asset given in “sec 108-20 ITA Act

1997” denotes that these assets are mainly kept by taxpayer for their own enjoyment (Mahar,

2016). The examples of this assets namely include the TV, vehicles, yacht, furniture etc. The

capital loss that happens from the sale of the personal use asset is on a frequent basis ignored

under “sec 108.20 (1) ITA Act 1997”.

In the present year Jasmine sold a car and received around $10,000. It must be noted

that Jasmine bought the car for $31,000 in 2011. The car here is a personal use asset within

“sec 108.20 ITA Act 1997”. Additionally, a “CGT Event A1” triggered when the car was

disposed by Jasmine. Eventually, she realised a capital loss when the car was sold.

Henceforth, under “sec 108.20 (1) ITA Act 1997” Jasmine should disregard the capital loss

from her personal use car.

Capital gains for Sale of business:

“Div 152” provides concessions to the small business so that they obtain relief from

capital gains tax (Friend, 2014). However to access the concessions, some basic conditions

needs to be satisfied:

a. The entity must meet the condition of small business entity where its net value of

asset must not go beyond $6 million or its gross turnover must not exceed $2 million

in a relevant year.

b. The small business asset must be an active asset

When the small business satisfies the conditions that is given above, they are provided

with the access of four small business concessions;

a. 15-year exemption: The total sum of capital gains is exempted from CGT when the

asset is owned for 15 years and the age of taxpayer is 55 years or more.

An important explanation regarding personal use asset given in “sec 108-20 ITA Act

1997” denotes that these assets are mainly kept by taxpayer for their own enjoyment (Mahar,

2016). The examples of this assets namely include the TV, vehicles, yacht, furniture etc. The

capital loss that happens from the sale of the personal use asset is on a frequent basis ignored

under “sec 108.20 (1) ITA Act 1997”.

In the present year Jasmine sold a car and received around $10,000. It must be noted

that Jasmine bought the car for $31,000 in 2011. The car here is a personal use asset within

“sec 108.20 ITA Act 1997”. Additionally, a “CGT Event A1” triggered when the car was

disposed by Jasmine. Eventually, she realised a capital loss when the car was sold.

Henceforth, under “sec 108.20 (1) ITA Act 1997” Jasmine should disregard the capital loss

from her personal use car.

Capital gains for Sale of business:

“Div 152” provides concessions to the small business so that they obtain relief from

capital gains tax (Friend, 2014). However to access the concessions, some basic conditions

needs to be satisfied:

a. The entity must meet the condition of small business entity where its net value of

asset must not go beyond $6 million or its gross turnover must not exceed $2 million

in a relevant year.

b. The small business asset must be an active asset

When the small business satisfies the conditions that is given above, they are provided

with the access of four small business concessions;

a. 15-year exemption: The total sum of capital gains is exempted from CGT when the

asset is owned for 15 years and the age of taxpayer is 55 years or more.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

b. 50% CGT Reduction: The taxpayer that are meeting the qualification criteria are

allowed to reduce the capital gain by further 50% following the application of general

50% discount percentage.

c. Retirement concession: Capital gains is disregarded for CGT asset related with small

business given that the amount is used by taxpayer for retirement purpose (Ingram,

2016).

d. Roll-over relief: This is given to taxpayer when the proceeds of capital gain is used

for purchasing another replacement asset.

The case facts that is found advises that Jasmine has retired from her small business

and has sold all her assets for $65,000 while her business goodwill for $65,000 to fetch an

overall amount of $125,000. Jasmine here qualifies for the small business concession because

the value of her asset is not greater than $6 million and all her CGT asset is an active asset.

Jasmine will be permitted to avail a 15-year exemption since the asset was owned by her for

15-year and she also ages more than 55 years.

Capital gain on Sale of furniture:

Most importantly, there are some vital rules that is applicable on disposal of personal

use asset. Accordingly, in “sec 118.10 (3) ITA Act 1997” the taxpayer must ignore the capital

gains when the asset fail to meet the first element cost base of $10,000 (Hay-Bartlem, 2017).

In the present situation, Jasmine sells her furniture for $5,000 which she eventually purchases

for $2,000. As understood the capital gains made here will be ignored by Jasmine because the

first element cost base is not satisfied since the painting was bought for less than $10,000.

Sale of paintings:

“Sec 108.10 ITA Act 1997” defines collectable as asset which is held by taxpayer for

own enjoyment (Mannix, 2017). Examples include antiques, paintings, rare stamps, coins etc.

b. 50% CGT Reduction: The taxpayer that are meeting the qualification criteria are

allowed to reduce the capital gain by further 50% following the application of general

50% discount percentage.

c. Retirement concession: Capital gains is disregarded for CGT asset related with small

business given that the amount is used by taxpayer for retirement purpose (Ingram,

2016).

d. Roll-over relief: This is given to taxpayer when the proceeds of capital gain is used

for purchasing another replacement asset.

The case facts that is found advises that Jasmine has retired from her small business

and has sold all her assets for $65,000 while her business goodwill for $65,000 to fetch an

overall amount of $125,000. Jasmine here qualifies for the small business concession because

the value of her asset is not greater than $6 million and all her CGT asset is an active asset.

Jasmine will be permitted to avail a 15-year exemption since the asset was owned by her for

15-year and she also ages more than 55 years.

Capital gain on Sale of furniture:

Most importantly, there are some vital rules that is applicable on disposal of personal

use asset. Accordingly, in “sec 118.10 (3) ITA Act 1997” the taxpayer must ignore the capital

gains when the asset fail to meet the first element cost base of $10,000 (Hay-Bartlem, 2017).

In the present situation, Jasmine sells her furniture for $5,000 which she eventually purchases

for $2,000. As understood the capital gains made here will be ignored by Jasmine because the

first element cost base is not satisfied since the painting was bought for less than $10,000.

Sale of paintings:

“Sec 108.10 ITA Act 1997” defines collectable as asset which is held by taxpayer for

own enjoyment (Mannix, 2017). Examples include antiques, paintings, rare stamps, coins etc.

5TAXATION LAW

Capital gains are overlooked under “sec 118-10 (1) ITA Act 1997” when collectables are

purchased for less than $500.

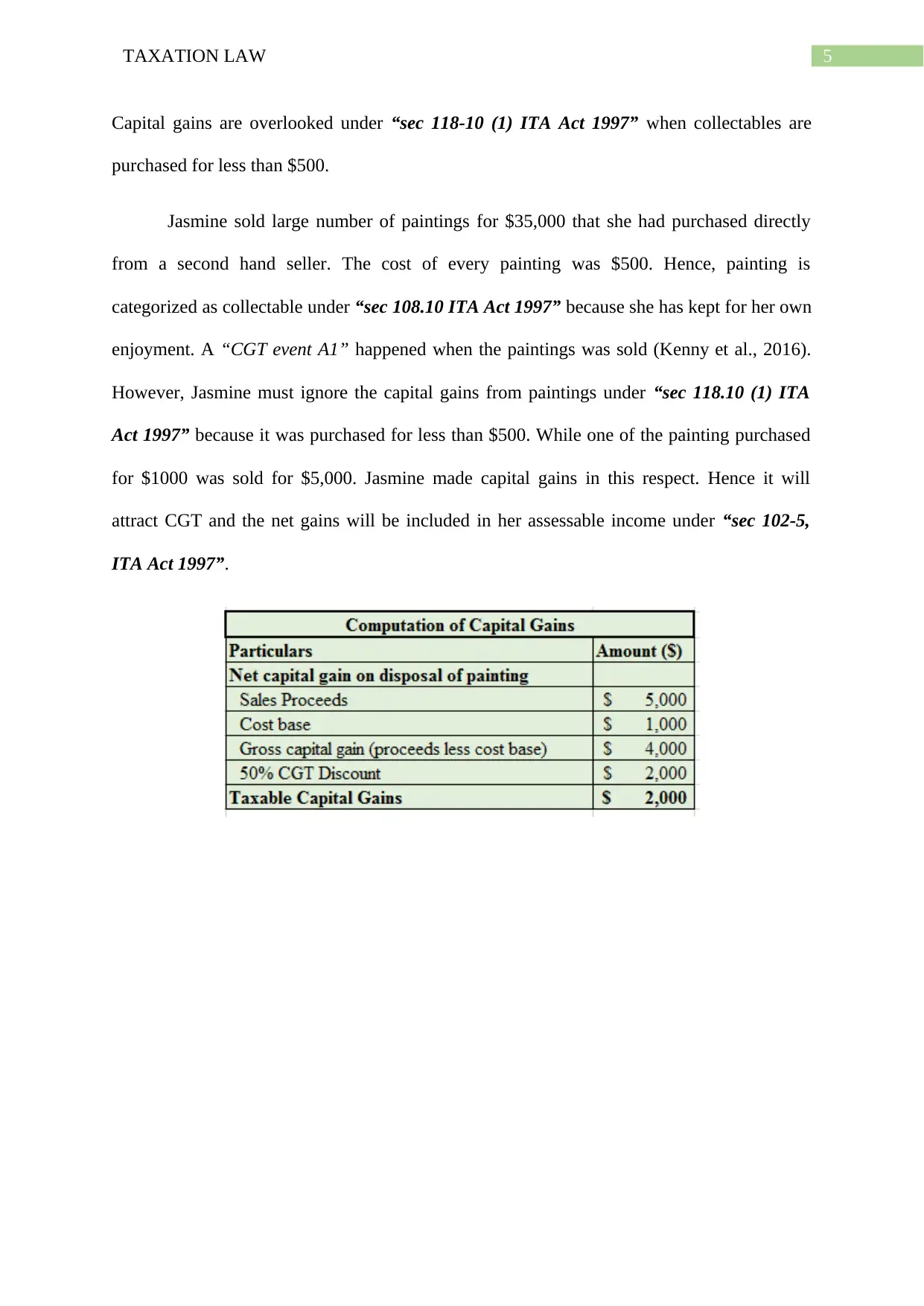

Jasmine sold large number of paintings for $35,000 that she had purchased directly

from a second hand seller. The cost of every painting was $500. Hence, painting is

categorized as collectable under “sec 108.10 ITA Act 1997” because she has kept for her own

enjoyment. A “CGT event A1” happened when the paintings was sold (Kenny et al., 2016).

However, Jasmine must ignore the capital gains from paintings under “sec 118.10 (1) ITA

Act 1997” because it was purchased for less than $500. While one of the painting purchased

for $1000 was sold for $5,000. Jasmine made capital gains in this respect. Hence it will

attract CGT and the net gains will be included in her assessable income under “sec 102-5,

ITA Act 1997”.

Capital gains are overlooked under “sec 118-10 (1) ITA Act 1997” when collectables are

purchased for less than $500.

Jasmine sold large number of paintings for $35,000 that she had purchased directly

from a second hand seller. The cost of every painting was $500. Hence, painting is

categorized as collectable under “sec 108.10 ITA Act 1997” because she has kept for her own

enjoyment. A “CGT event A1” happened when the paintings was sold (Kenny et al., 2016).

However, Jasmine must ignore the capital gains from paintings under “sec 118.10 (1) ITA

Act 1997” because it was purchased for less than $500. While one of the painting purchased

for $1000 was sold for $5,000. Jasmine made capital gains in this respect. Hence it will

attract CGT and the net gains will be included in her assessable income under “sec 102-5,

ITA Act 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issues:

The central issue to the subject is associated with the deduction for the amount that is

equivalent to the decline in value for the income year of the depreciating asset that was held

by the taxpayer under “sec 40-25 (1), ITA Act 97”.

Laws:

“Div 40 ITA Act 1997” provides explanation to the taxpayer regarding the capital

allowance regimes. Within “sec 40.30 ITA Act 1997” the provision of capital allowance is

applicable to majority of the depreciating assets that does not amounts to any capital works.

Within the “Div 40 ITA Act 1997” the general provisions relating to the capital allowance is

permissible as claim for all the taxpayers (Sadiq & Marsden, 2014). In addition to this, under

“subdiv 40-E” all the taxpayers apart from the SBE taxpayers, is allowed to use the specific

lower value asset provision to make the claim for higher depreciation.

The central provision of the “sec 40-25 (1) ITA Act 1997” all the taxpayers are

provided with the permission of deducting a sum that is equal to the “fall in value” or

depreciation during the income year relating to the depreciating asset that is held by them for

any time period throughout the year. While “sec 40-30 (1)”, says that a depreciating asset

amounts those asset that has very limited effective life (Brown et al., 2014). This type of asset

are projected to fall in respect of their values over the time period till it is used.

While “sec 40-25 (7) ITA Act 1997” articulates that the assessable purpose represents

the purpose of generating assessable income and also comprises of the purpose of exploring

and prospecting of the depreciating asset that is held throughout the year (Novek, 2016).

Capital allowance regime given in “division 40 ITA Act 1997” lists down that a deduction

Answer to question 2:

Issues:

The central issue to the subject is associated with the deduction for the amount that is

equivalent to the decline in value for the income year of the depreciating asset that was held

by the taxpayer under “sec 40-25 (1), ITA Act 97”.

Laws:

“Div 40 ITA Act 1997” provides explanation to the taxpayer regarding the capital

allowance regimes. Within “sec 40.30 ITA Act 1997” the provision of capital allowance is

applicable to majority of the depreciating assets that does not amounts to any capital works.

Within the “Div 40 ITA Act 1997” the general provisions relating to the capital allowance is

permissible as claim for all the taxpayers (Sadiq & Marsden, 2014). In addition to this, under

“subdiv 40-E” all the taxpayers apart from the SBE taxpayers, is allowed to use the specific

lower value asset provision to make the claim for higher depreciation.

The central provision of the “sec 40-25 (1) ITA Act 1997” all the taxpayers are

provided with the permission of deducting a sum that is equal to the “fall in value” or

depreciation during the income year relating to the depreciating asset that is held by them for

any time period throughout the year. While “sec 40-30 (1)”, says that a depreciating asset

amounts those asset that has very limited effective life (Brown et al., 2014). This type of asset

are projected to fall in respect of their values over the time period till it is used.

While “sec 40-25 (7) ITA Act 1997” articulates that the assessable purpose represents

the purpose of generating assessable income and also comprises of the purpose of exploring

and prospecting of the depreciating asset that is held throughout the year (Novek, 2016).

Capital allowance regime given in “division 40 ITA Act 1997” lists down that a deduction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

relating to the decline in value of the depreciating asset for the income year is only allowed

for claim by person that has held the asset throughout the income year. Under “sec 45-40

ITA Act 1997” a depreciating asset usually takes into the account the concept of plant. The

law court in “Yarmouth v France (1887)” explained the ordinary meaning of plant which

includes device of any kind used by a business man for conducting the business activities

(Walrut, 2015).

In the meantime “sec 40-60 ITA Act 1997” provides relevant dates under the capital

allowance regime. The start time for decline in value of the depreciating asset commences

when it is first used by the taxpayer or the asset has been installed by the taxpayer as ready

for taxable business usage (Meadmore, 2016). The taxpayers are required to denote that they

are only allowed to claim depreciation based on the assets cost base. Meanwhile, the rules of

computing the cost of asset is contained within “Subdiv 40-C”. As a common rule, the cost

would not comprise of the purchase price but would take note of the incidental costs as well

as any delivery cost that is occurred while installing the depreciating asset. The taxpayer

should notably denote that any kind of added expenses that is occurred towards rearranging

or removing the other plant for accommodating the new plant might also be included in the

cost base of the asset.

The present legislation of “sec 40.175 ITA Act 1997” classifies the depreciating asset

cost under two elements. The exact rule concerned with working out the first element is given

in “sec 40.180 ITA Act 1997”. While “subsection 40.180 ITA Act 1997” provides direction

that this element must be worked out when the taxpayer begins holding the asset (Kennedy,

2016). “Sec 40.180 ITA Act 1997” says that the first element normally involves the purchase

price that is paid while purchasing the asset. Meanwhile, “sec 40.190 ITA Act 1997” is

primarily associated with the second element that generally involves the delivery costs,

installation and capital improvements that is made to the asset.

relating to the decline in value of the depreciating asset for the income year is only allowed

for claim by person that has held the asset throughout the income year. Under “sec 45-40

ITA Act 1997” a depreciating asset usually takes into the account the concept of plant. The

law court in “Yarmouth v France (1887)” explained the ordinary meaning of plant which

includes device of any kind used by a business man for conducting the business activities

(Walrut, 2015).

In the meantime “sec 40-60 ITA Act 1997” provides relevant dates under the capital

allowance regime. The start time for decline in value of the depreciating asset commences

when it is first used by the taxpayer or the asset has been installed by the taxpayer as ready

for taxable business usage (Meadmore, 2016). The taxpayers are required to denote that they

are only allowed to claim depreciation based on the assets cost base. Meanwhile, the rules of

computing the cost of asset is contained within “Subdiv 40-C”. As a common rule, the cost

would not comprise of the purchase price but would take note of the incidental costs as well

as any delivery cost that is occurred while installing the depreciating asset. The taxpayer

should notably denote that any kind of added expenses that is occurred towards rearranging

or removing the other plant for accommodating the new plant might also be included in the

cost base of the asset.

The present legislation of “sec 40.175 ITA Act 1997” classifies the depreciating asset

cost under two elements. The exact rule concerned with working out the first element is given

in “sec 40.180 ITA Act 1997”. While “subsection 40.180 ITA Act 1997” provides direction

that this element must be worked out when the taxpayer begins holding the asset (Kennedy,

2016). “Sec 40.180 ITA Act 1997” says that the first element normally involves the purchase

price that is paid while purchasing the asset. Meanwhile, “sec 40.190 ITA Act 1997” is

primarily associated with the second element that generally involves the delivery costs,

installation and capital improvements that is made to the asset.

8TAXATION LAW

Application:

The scenario evidences of the case suggest that John produces certified BMW parts.

He is the owner of motor vehicle parts and accessories manufacturing company. On one

occasion he visited Germany to inspect the CNC machine. Additionally, following the

successful inspection he purchased the asset for $300,000. The machine was finally installed

on 15th January and John incurred an installation cost of $25,000. Under “sec 40.30 (1) ITA

Act 1997” the CNC machine is a depreciating asset because the machine has the limited

effective life. Quoting the case of “Yarmouth v France (1887)” the machine is also

estimated to fall in value based on its usage (Meadmore, 2016). Furthermore, the CNC

machine also satisfies the condition given in “section 40.25 (7) ITA Act 1997” because the

machine was exclusively purchased by John for producing the assessable business earnings.

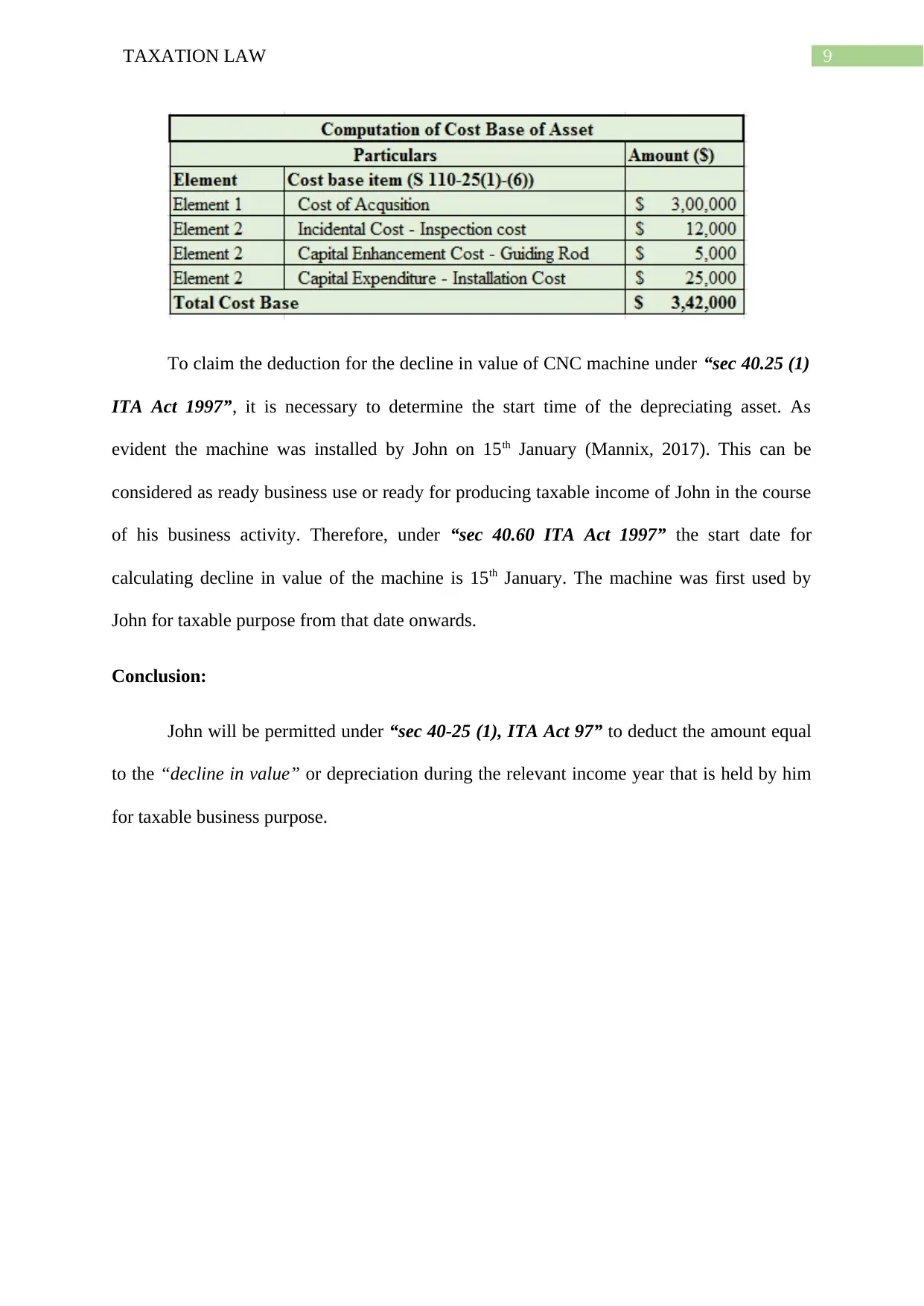

To determine the cost base of machinery reference to the rule contained within

“Subdiv 40-C” has been referred. Under the first element, the purchase price paid by John for

purchasing the machine will be included for determining the “decline in value” of the asset.

The sum of $300,000 paid by John for the acquisition of CNC machine will be included

under first element of “sec 40.180 ITA Act 1997”.

John also incurred an installation cost of $25,000 to install the machine. He also

incurred a sum of $5,000 for installing a guiding rod for making the CNC machine more

effective. Referring to the “sec 40.190 ITA Act 1997” the second element cost base of CNC

machine would include the installation cost and cost occurred for adding a guiding rod.

Application:

The scenario evidences of the case suggest that John produces certified BMW parts.

He is the owner of motor vehicle parts and accessories manufacturing company. On one

occasion he visited Germany to inspect the CNC machine. Additionally, following the

successful inspection he purchased the asset for $300,000. The machine was finally installed

on 15th January and John incurred an installation cost of $25,000. Under “sec 40.30 (1) ITA

Act 1997” the CNC machine is a depreciating asset because the machine has the limited

effective life. Quoting the case of “Yarmouth v France (1887)” the machine is also

estimated to fall in value based on its usage (Meadmore, 2016). Furthermore, the CNC

machine also satisfies the condition given in “section 40.25 (7) ITA Act 1997” because the

machine was exclusively purchased by John for producing the assessable business earnings.

To determine the cost base of machinery reference to the rule contained within

“Subdiv 40-C” has been referred. Under the first element, the purchase price paid by John for

purchasing the machine will be included for determining the “decline in value” of the asset.

The sum of $300,000 paid by John for the acquisition of CNC machine will be included

under first element of “sec 40.180 ITA Act 1997”.

John also incurred an installation cost of $25,000 to install the machine. He also

incurred a sum of $5,000 for installing a guiding rod for making the CNC machine more

effective. Referring to the “sec 40.190 ITA Act 1997” the second element cost base of CNC

machine would include the installation cost and cost occurred for adding a guiding rod.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

To claim the deduction for the decline in value of CNC machine under “sec 40.25 (1)

ITA Act 1997”, it is necessary to determine the start time of the depreciating asset. As

evident the machine was installed by John on 15th January (Mannix, 2017). This can be

considered as ready business use or ready for producing taxable income of John in the course

of his business activity. Therefore, under “sec 40.60 ITA Act 1997” the start date for

calculating decline in value of the machine is 15th January. The machine was first used by

John for taxable purpose from that date onwards.

Conclusion:

John will be permitted under “sec 40-25 (1), ITA Act 97” to deduct the amount equal

to the “decline in value” or depreciation during the relevant income year that is held by him

for taxable business purpose.

To claim the deduction for the decline in value of CNC machine under “sec 40.25 (1)

ITA Act 1997”, it is necessary to determine the start time of the depreciating asset. As

evident the machine was installed by John on 15th January (Mannix, 2017). This can be

considered as ready business use or ready for producing taxable income of John in the course

of his business activity. Therefore, under “sec 40.60 ITA Act 1997” the start date for

calculating decline in value of the machine is 15th January. The machine was first used by

John for taxable purpose from that date onwards.

Conclusion:

John will be permitted under “sec 40-25 (1), ITA Act 97” to deduct the amount equal

to the “decline in value” or depreciation during the relevant income year that is held by him

for taxable business purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Armstrong, M. (2016). CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, p. Mondaq Business Briefing, March 11, 2016.

Brown, P., Ferguson, A., & Sherry, S. (2014). Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), 783-808.

Friend, R. (2014). The CGT small business concessions: Issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), 108-137.

Hay-Bartlem, S. (2017). CGT relief, 2016 Budget changes and SMSFs - Do I need to

commute back to accumulation phase to access relief? Mondaq Business Briefing, p.

Mondaq Business Briefing, May 17, 2017.

Ingram, P. (2016). Tax files: More than meets the eye - the new 'foreign resident capital gains

tax withholding regime'. Bulletin (Law Society of South Australia), 38(5), 36-37.

Kennedy, A. (2016). New regime for withholding CGT when purchasing Australian land.

Mondaq Business Briefing, p. Mondaq Business Briefing, Feb 8, 2016.

Kenny, P., Blissenden, M., & Villios, S. (2016). Australian tax 2016.

Lam, D., & Whitney, A. (2016). Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), 84.

Mahar, F. (2016). The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

16-20.

Mannix, J. (2017). An introduction to capital gains tax. Sydney: Butterworths.

Meadmore, J. (2016). How earn-out arrangements are affected by amended capital gains tax

rules. Mondaq Business Briefing, p. Mondaq Business Briefing, May 9, 2016.

References:

Armstrong, M. (2016). CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, p. Mondaq Business Briefing, March 11, 2016.

Brown, P., Ferguson, A., & Sherry, S. (2014). Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), 783-808.

Friend, R. (2014). The CGT small business concessions: Issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), 108-137.

Hay-Bartlem, S. (2017). CGT relief, 2016 Budget changes and SMSFs - Do I need to

commute back to accumulation phase to access relief? Mondaq Business Briefing, p.

Mondaq Business Briefing, May 17, 2017.

Ingram, P. (2016). Tax files: More than meets the eye - the new 'foreign resident capital gains

tax withholding regime'. Bulletin (Law Society of South Australia), 38(5), 36-37.

Kennedy, A. (2016). New regime for withholding CGT when purchasing Australian land.

Mondaq Business Briefing, p. Mondaq Business Briefing, Feb 8, 2016.

Kenny, P., Blissenden, M., & Villios, S. (2016). Australian tax 2016.

Lam, D., & Whitney, A. (2016). Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), 84.

Mahar, F. (2016). The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

16-20.

Mannix, J. (2017). An introduction to capital gains tax. Sydney: Butterworths.

Meadmore, J. (2016). How earn-out arrangements are affected by amended capital gains tax

rules. Mondaq Business Briefing, p. Mondaq Business Briefing, May 9, 2016.

11TAXATION LAW

Novek, C. (2016). Investors guide to capital gains tax and land tax. Mondaq Business

Briefing, p. Mondaq Business Briefing, July 18, 2016.

Phan, L. (2016). Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, p. Mondaq Business Briefing, Sept 29, 2016.

Sadiq, K., & Marsden, S. (2014). The small business CGT concessions: Evidence from the

perspective of the tax practitioner. Revenue Law Journal, 24, 1-21.

Walrut, B. (2015). Capital gains tax and death. Bulletin (Law Society of South Australia),

34(11), 26-28.

Novek, C. (2016). Investors guide to capital gains tax and land tax. Mondaq Business

Briefing, p. Mondaq Business Briefing, July 18, 2016.

Phan, L. (2016). Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, p. Mondaq Business Briefing, Sept 29, 2016.

Sadiq, K., & Marsden, S. (2014). The small business CGT concessions: Evidence from the

perspective of the tax practitioner. Revenue Law Journal, 24, 1-21.

Walrut, B. (2015). Capital gains tax and death. Bulletin (Law Society of South Australia),

34(11), 26-28.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.