Taxation Law 101 Assignment: Income, Deductions, and Tax

VerifiedAdded on 2021/05/30

|14

|2683

|327

Homework Assignment

AI Summary

This taxation law assignment addresses several key areas of Australian taxation. Question 1 defines discretionary trusts and their tax implications for beneficiaries, including minors. Question 2 analyzes the assessable income of individuals from partnership and employment, detailing relevant sections of the ITAA 1997 and case law regarding deductions and income characterization. Question 3 examines the tax liabilities of a business, including assessable income from sales and dividends, and allowable deductions for expenses like salaries, council rates, and asset purchases, including the application of the small business asset write-off. Question 4 includes a franking account reconciliation, an analysis of the deductibility of legal expenses, and the non-deductibility of childcare expenses, referencing relevant case law and legislation. The assignment provides detailed calculations and conclusions for each scenario, offering a comprehensive overview of tax principles and their practical application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................6

Answer to Question 4.................................................................................................................8

Answer to 4 A:...........................................................................................................................8

Answer to 4 B:...........................................................................................................................8

Answer to 4 C:...........................................................................................................................9

Answer to D:............................................................................................................................10

Reference List:.........................................................................................................................12

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................6

Answer to Question 4.................................................................................................................8

Answer to 4 A:...........................................................................................................................8

Answer to 4 B:...........................................................................................................................8

Answer to 4 C:...........................................................................................................................9

Answer to D:............................................................................................................................10

Reference List:.........................................................................................................................12

2TAXATION LAW

Answer to question 1

The term discretionary trust can be defined as the trust which is usually used to

ascertain where the trustee has the discretion as how the income of the trust or the capital of

the is distributed between the benefits that are named of the classes of beneficiaries (Woellner

et al. 2016). According to the Australian taxation office the net income of the trust is taxable

income during the year in which it was earned based on the assumptions that trustee is the

resident. The beneficiary of the trust is entitled to trust income during the year of income

where they have been or by the end of year with the immediate right to demand for the

payment.

According to the Australian taxation office trustee pays the tax on behalf of the noon-

resident beneficiaries and those that are minors depending upon the share of the trust net

income (Barkoczy 2016). As evident from the case study it can be stated that the Steve and

Suzy are the beneficiaries of the trust while the John and Michelle are minor of the trustee.

As evident the beneficiaries of the trust Steve and Suzy derived net income from trust that is

taxable in the hands of the beneficiaries depending upon the share of the company.

Additionally, the minor of the trustee are John and Michelle that are aged below the 18 years.

As Michele and John are minors of the trust, in that case Steve and Suzy the trustee of

the trust would be required to pay the taxes on their behalf based on the share of the trust net

income (Basu 2016). The beneficiaries would be required to pay the taxes by declaring the

share of the trust’s net income in their own tax return. Additionally, the trust of the trust

namely Steve and Suzy would be levied taxes based on the trust income at the highest

marginal tax rate which is applicable to the individuals of the trust. Following the principles

of “Federal Commissioner of Taxation v Bamford (2010) ATC 20-170” it is understood that

Answer to question 1

The term discretionary trust can be defined as the trust which is usually used to

ascertain where the trustee has the discretion as how the income of the trust or the capital of

the is distributed between the benefits that are named of the classes of beneficiaries (Woellner

et al. 2016). According to the Australian taxation office the net income of the trust is taxable

income during the year in which it was earned based on the assumptions that trustee is the

resident. The beneficiary of the trust is entitled to trust income during the year of income

where they have been or by the end of year with the immediate right to demand for the

payment.

According to the Australian taxation office trustee pays the tax on behalf of the noon-

resident beneficiaries and those that are minors depending upon the share of the trust net

income (Barkoczy 2016). As evident from the case study it can be stated that the Steve and

Suzy are the beneficiaries of the trust while the John and Michelle are minor of the trustee.

As evident the beneficiaries of the trust Steve and Suzy derived net income from trust that is

taxable in the hands of the beneficiaries depending upon the share of the company.

Additionally, the minor of the trustee are John and Michelle that are aged below the 18 years.

As Michele and John are minors of the trust, in that case Steve and Suzy the trustee of

the trust would be required to pay the taxes on their behalf based on the share of the trust net

income (Basu 2016). The beneficiaries would be required to pay the taxes by declaring the

share of the trust’s net income in their own tax return. Additionally, the trust of the trust

namely Steve and Suzy would be levied taxes based on the trust income at the highest

marginal tax rate which is applicable to the individuals of the trust. Following the principles

of “Federal Commissioner of Taxation v Bamford (2010) ATC 20-170” it is understood that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

the income of the trust is in accordance with the trust estate based on the trust law principles

(Jones and Rhoades-Catanach 2015).

Answer to question 2:

Issues:

The present issue is associated with the determination of the assessable income of the

taxpayer from the income derived through partnership and income from employment as well.

Laws:

“Section 6-1 of the ITAA 1997”

“Scott v Federal Commissioner of Taxation (1935)”

“Section 6-5 of the ITAA 1997”

“Lunney v Federal Commissioner of Taxation”

“section 8-1 of the ITAA 1997”

“Section 25-10 of the ITAA 1997”

“Rhodesia Railways v Federal Commissioner of Taxation”

Application:

As per “section 6-1 of the ITAA 1997” an individual deriving income from personal

exertion refers to the income that are obtained through the salaries or wages, allowances of

any form of money that is derived from the business that are carried on by the taxpayer either

along through the partnership (Miller and Oats 2016). As held in the case of “Scott v Federal

Commissioner of Taxation (1935)” income that are obtained from the personal sources or

through the ordinary concepts would be considered taxable. Similarly, an individual under

“section 6-1 of the ITAA 1997” is allowed to claim deductions relating to the expenses that

the income of the trust is in accordance with the trust estate based on the trust law principles

(Jones and Rhoades-Catanach 2015).

Answer to question 2:

Issues:

The present issue is associated with the determination of the assessable income of the

taxpayer from the income derived through partnership and income from employment as well.

Laws:

“Section 6-1 of the ITAA 1997”

“Scott v Federal Commissioner of Taxation (1935)”

“Section 6-5 of the ITAA 1997”

“Lunney v Federal Commissioner of Taxation”

“section 8-1 of the ITAA 1997”

“Section 25-10 of the ITAA 1997”

“Rhodesia Railways v Federal Commissioner of Taxation”

Application:

As per “section 6-1 of the ITAA 1997” an individual deriving income from personal

exertion refers to the income that are obtained through the salaries or wages, allowances of

any form of money that is derived from the business that are carried on by the taxpayer either

along through the partnership (Miller and Oats 2016). As held in the case of “Scott v Federal

Commissioner of Taxation (1935)” income that are obtained from the personal sources or

through the ordinary concepts would be considered taxable. Similarly, an individual under

“section 6-1 of the ITAA 1997” is allowed to claim deductions relating to the expenses that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

are occurred in producing the taxable income (Christie 2015). As evident in the situation of

Jenny and Robert the income that are obtained from the partnership business would be

considered for assessment based on “section 6-5 of the ITAA 1997”. The receipts of

partnership would constitute ordinary income and would be included for assessment purpose.

An instances was reported where the partnership incurred a bank fees of $2,000 in

order to discharge the bank mortgage. According to “Lunney v Federal Commissioner of

Taxation” it is necessary to determine the character of the outgoings that is sufficient in

determining the necessary prerequisite of the derivation of the taxable income (Becker,

Reimer and Rust 2015). Similarly, under “section 8-1 of the ITAA 1997” the bank interest

that is incurred by Jenny and Roberts would be held as allowable deduction since it was

incurred in gaining the taxable income.

On the other evidences gained from the case study suggest that the Roberta obtained

income from clerk. With reference to “Section 6-5 of the ITAA 1997” the receipt from

employment of clerk by Roberta would be held for assessment.

“Section 25-10 of the ITAA 1997” an individual is allowed to deduct expenditure that

they incur for the purpose of repair to the depreciating assets that is entirely used for the

purpose of generating income (Bankman et al. 2017). However, the section does not allow a

person to obtain deductions relating to the capital expenses that are occurred.

According to the “taxation ruling of TR 97/23” repairs that involves significant

replacement are not allowed as deductions. The court of law in “Rhodesia Railways v

Federal Commissioner of Taxation” explained that expenses that are in the nature of capital

are not allowed as deductions (McDaniel 2017). Similarly, in the situation of partnership

business carried on Jenny and Roberta expenses of $500 that were incurred in replacing the

part of the machinery cannot be allowed as deductions since was capital in nature.

are occurred in producing the taxable income (Christie 2015). As evident in the situation of

Jenny and Robert the income that are obtained from the partnership business would be

considered for assessment based on “section 6-5 of the ITAA 1997”. The receipts of

partnership would constitute ordinary income and would be included for assessment purpose.

An instances was reported where the partnership incurred a bank fees of $2,000 in

order to discharge the bank mortgage. According to “Lunney v Federal Commissioner of

Taxation” it is necessary to determine the character of the outgoings that is sufficient in

determining the necessary prerequisite of the derivation of the taxable income (Becker,

Reimer and Rust 2015). Similarly, under “section 8-1 of the ITAA 1997” the bank interest

that is incurred by Jenny and Roberts would be held as allowable deduction since it was

incurred in gaining the taxable income.

On the other evidences gained from the case study suggest that the Roberta obtained

income from clerk. With reference to “Section 6-5 of the ITAA 1997” the receipt from

employment of clerk by Roberta would be held for assessment.

“Section 25-10 of the ITAA 1997” an individual is allowed to deduct expenditure that

they incur for the purpose of repair to the depreciating assets that is entirely used for the

purpose of generating income (Bankman et al. 2017). However, the section does not allow a

person to obtain deductions relating to the capital expenses that are occurred.

According to the “taxation ruling of TR 97/23” repairs that involves significant

replacement are not allowed as deductions. The court of law in “Rhodesia Railways v

Federal Commissioner of Taxation” explained that expenses that are in the nature of capital

are not allowed as deductions (McDaniel 2017). Similarly, in the situation of partnership

business carried on Jenny and Roberta expenses of $500 that were incurred in replacing the

part of the machinery cannot be allowed as deductions since was capital in nature.

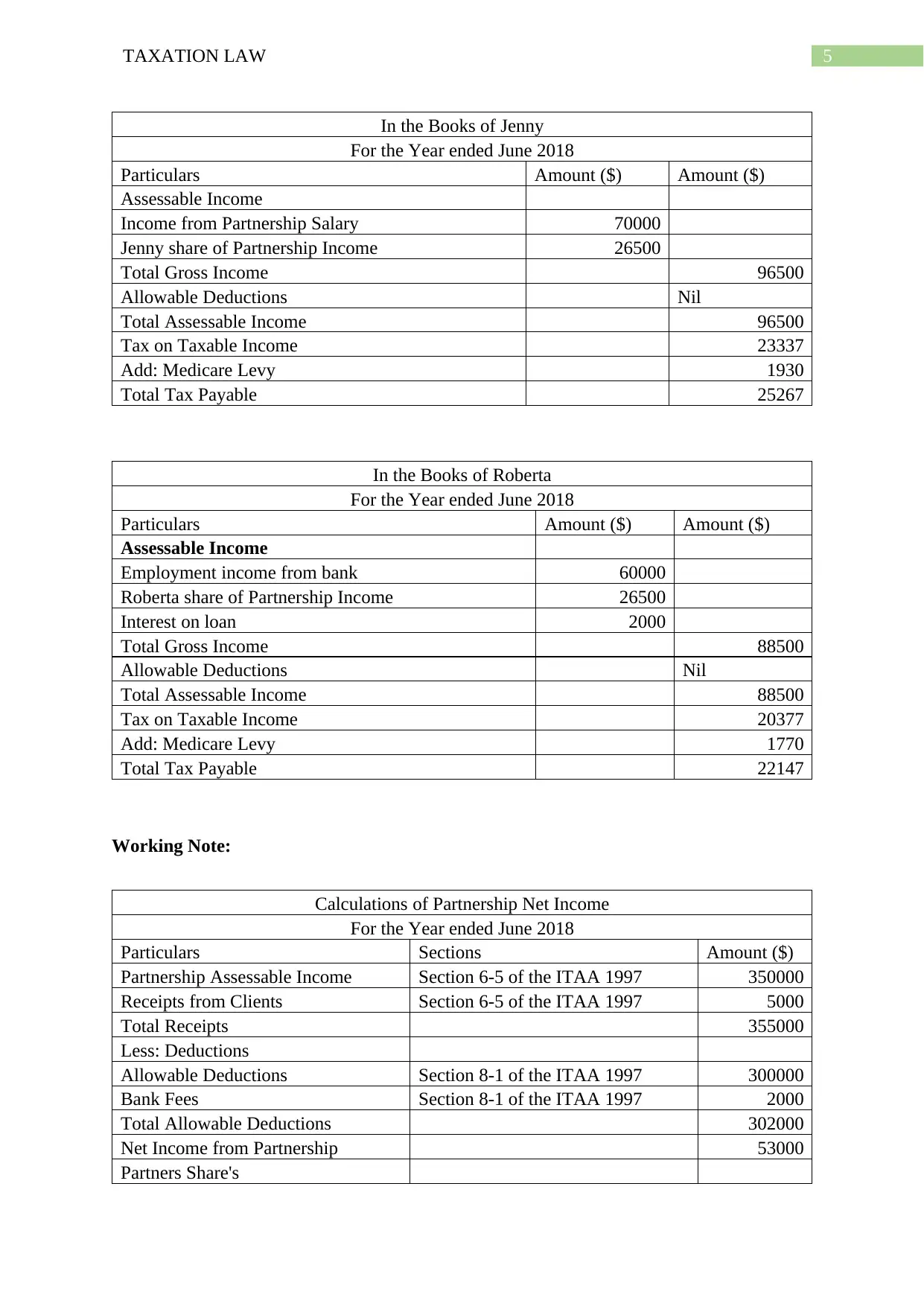

5TAXATION LAW

In the Books of Jenny

For the Year ended June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Income from Partnership Salary 70000

Jenny share of Partnership Income 26500

Total Gross Income 96500

Allowable Deductions Nil

Total Assessable Income 96500

Tax on Taxable Income 23337

Add: Medicare Levy 1930

Total Tax Payable 25267

In the Books of Roberta

For the Year ended June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Employment income from bank 60000

Roberta share of Partnership Income 26500

Interest on loan 2000

Total Gross Income 88500

Allowable Deductions Nil

Total Assessable Income 88500

Tax on Taxable Income 20377

Add: Medicare Levy 1770

Total Tax Payable 22147

Working Note:

Calculations of Partnership Net Income

For the Year ended June 2018

Particulars Sections Amount ($)

Partnership Assessable Income Section 6-5 of the ITAA 1997 350000

Receipts from Clients Section 6-5 of the ITAA 1997 5000

Total Receipts 355000

Less: Deductions

Allowable Deductions Section 8-1 of the ITAA 1997 300000

Bank Fees Section 8-1 of the ITAA 1997 2000

Total Allowable Deductions 302000

Net Income from Partnership 53000

Partners Share's

In the Books of Jenny

For the Year ended June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Income from Partnership Salary 70000

Jenny share of Partnership Income 26500

Total Gross Income 96500

Allowable Deductions Nil

Total Assessable Income 96500

Tax on Taxable Income 23337

Add: Medicare Levy 1930

Total Tax Payable 25267

In the Books of Roberta

For the Year ended June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Employment income from bank 60000

Roberta share of Partnership Income 26500

Interest on loan 2000

Total Gross Income 88500

Allowable Deductions Nil

Total Assessable Income 88500

Tax on Taxable Income 20377

Add: Medicare Levy 1770

Total Tax Payable 22147

Working Note:

Calculations of Partnership Net Income

For the Year ended June 2018

Particulars Sections Amount ($)

Partnership Assessable Income Section 6-5 of the ITAA 1997 350000

Receipts from Clients Section 6-5 of the ITAA 1997 5000

Total Receipts 355000

Less: Deductions

Allowable Deductions Section 8-1 of the ITAA 1997 300000

Bank Fees Section 8-1 of the ITAA 1997 2000

Total Allowable Deductions 302000

Net Income from Partnership 53000

Partners Share's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Jenny (1/2) 26500

Roberta (1/2) 26500

Conclusion:

It can be concluded by stating that the expenses such as bank fees paid to discharge

the partnership borrowings would be allowed as deductions under “section 8-1 of the ITAA

1997”. On the other hand, the income that are derived by the partners will be held taxable

under “section 6-5 of the ITAA 1997”.

Answer to question 3:

Issue:

The current issue is based on determining the deductibility of the expenses incurred

and the income that is earned by the Kustom Kitchens during the course of business.

Laws:

“Section 6-5 of the ITAA 1997”

“Section 6-1 of the ITAA 1997”

“Section 8-1 of the ITAA 1997”

Applications:

With reference to “section 6-5 of the ITAA 1997” income derived from the ordinary

sources are held taxable (Murphy and Higgins 2016). Similarly, the receipt from the sales that

are derived would be considered taxable based on the ordinary concepts of “section 6-1 of

the ITAA 1997”. According to “section 8-1 of the ITAA 1997” an individual is allowed to

claim deductions under the positive limbs given the expenses are incurred in gaining the

taxable income (Wilson 2015). The council rates that are paid by the business forms the part

of deductions and will be allowed as deductions “section 8-1 of the ITAA 1997”. The

Jenny (1/2) 26500

Roberta (1/2) 26500

Conclusion:

It can be concluded by stating that the expenses such as bank fees paid to discharge

the partnership borrowings would be allowed as deductions under “section 8-1 of the ITAA

1997”. On the other hand, the income that are derived by the partners will be held taxable

under “section 6-5 of the ITAA 1997”.

Answer to question 3:

Issue:

The current issue is based on determining the deductibility of the expenses incurred

and the income that is earned by the Kustom Kitchens during the course of business.

Laws:

“Section 6-5 of the ITAA 1997”

“Section 6-1 of the ITAA 1997”

“Section 8-1 of the ITAA 1997”

Applications:

With reference to “section 6-5 of the ITAA 1997” income derived from the ordinary

sources are held taxable (Murphy and Higgins 2016). Similarly, the receipt from the sales that

are derived would be considered taxable based on the ordinary concepts of “section 6-1 of

the ITAA 1997”. According to “section 8-1 of the ITAA 1997” an individual is allowed to

claim deductions under the positive limbs given the expenses are incurred in gaining the

taxable income (Wilson 2015). The council rates that are paid by the business forms the part

of deductions and will be allowed as deductions “section 8-1 of the ITAA 1997”. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

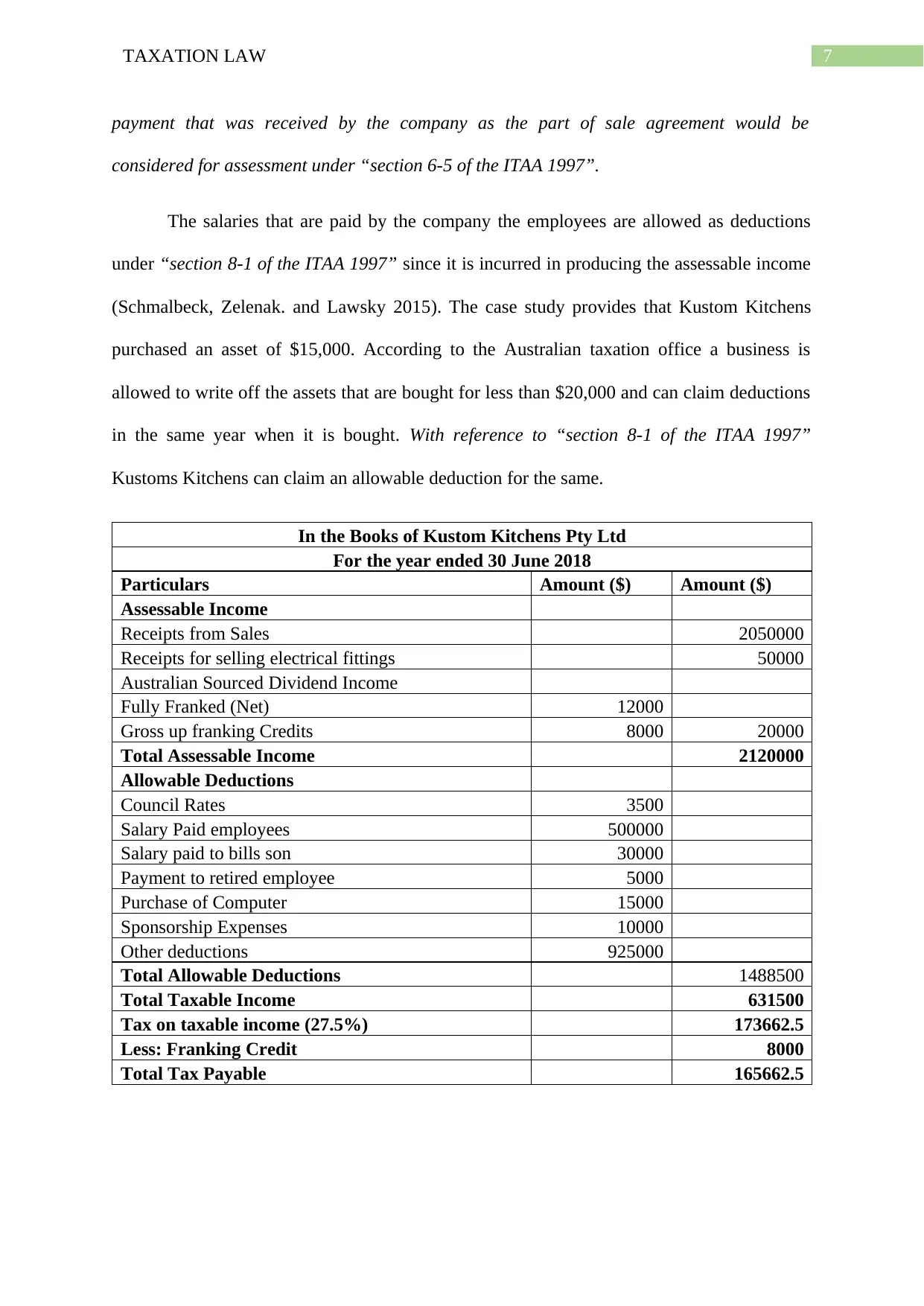

payment that was received by the company as the part of sale agreement would be

considered for assessment under “section 6-5 of the ITAA 1997”.

The salaries that are paid by the company the employees are allowed as deductions

under “section 8-1 of the ITAA 1997” since it is incurred in producing the assessable income

(Schmalbeck, Zelenak. and Lawsky 2015). The case study provides that Kustom Kitchens

purchased an asset of $15,000. According to the Australian taxation office a business is

allowed to write off the assets that are bought for less than $20,000 and can claim deductions

in the same year when it is bought. With reference to “section 8-1 of the ITAA 1997”

Kustoms Kitchens can claim an allowable deduction for the same.

In the Books of Kustom Kitchens Pty Ltd

For the year ended 30 June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Receipts from Sales 2050000

Receipts for selling electrical fittings 50000

Australian Sourced Dividend Income

Fully Franked (Net) 12000

Gross up franking Credits 8000 20000

Total Assessable Income 2120000

Allowable Deductions

Council Rates 3500

Salary Paid employees 500000

Salary paid to bills son 30000

Payment to retired employee 5000

Purchase of Computer 15000

Sponsorship Expenses 10000

Other deductions 925000

Total Allowable Deductions 1488500

Total Taxable Income 631500

Tax on taxable income (27.5%) 173662.5

Less: Franking Credit 8000

Total Tax Payable 165662.5

payment that was received by the company as the part of sale agreement would be

considered for assessment under “section 6-5 of the ITAA 1997”.

The salaries that are paid by the company the employees are allowed as deductions

under “section 8-1 of the ITAA 1997” since it is incurred in producing the assessable income

(Schmalbeck, Zelenak. and Lawsky 2015). The case study provides that Kustom Kitchens

purchased an asset of $15,000. According to the Australian taxation office a business is

allowed to write off the assets that are bought for less than $20,000 and can claim deductions

in the same year when it is bought. With reference to “section 8-1 of the ITAA 1997”

Kustoms Kitchens can claim an allowable deduction for the same.

In the Books of Kustom Kitchens Pty Ltd

For the year ended 30 June 2018

Particulars Amount ($) Amount ($)

Assessable Income

Receipts from Sales 2050000

Receipts for selling electrical fittings 50000

Australian Sourced Dividend Income

Fully Franked (Net) 12000

Gross up franking Credits 8000 20000

Total Assessable Income 2120000

Allowable Deductions

Council Rates 3500

Salary Paid employees 500000

Salary paid to bills son 30000

Payment to retired employee 5000

Purchase of Computer 15000

Sponsorship Expenses 10000

Other deductions 925000

Total Allowable Deductions 1488500

Total Taxable Income 631500

Tax on taxable income (27.5%) 173662.5

Less: Franking Credit 8000

Total Tax Payable 165662.5

8TAXATION LAW

Conclusion:

Conclusively the income that are obtained by the taxpayer will be held assessable

under “section 6-5 of the ITAA 1997” and the expenses incurred would be allowed for

deductions under “section 8-1 of the ITAA 1997”.

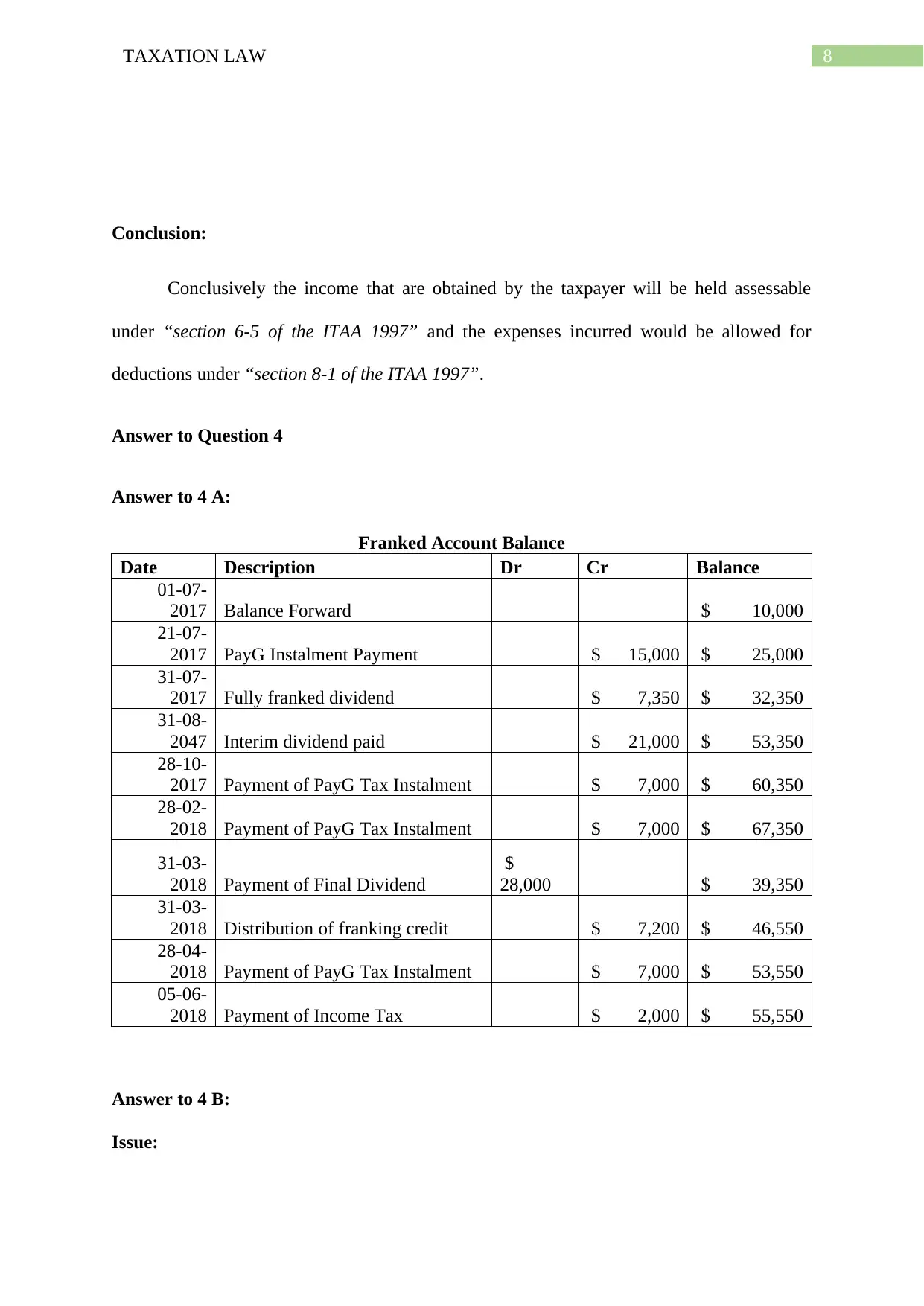

Answer to Question 4

Answer to 4 A:

Franked Account Balance

Date Description Dr Cr Balance

01-07-

2017 Balance Forward $ 10,000

21-07-

2017 PayG Instalment Payment $ 15,000 $ 25,000

31-07-

2017 Fully franked dividend $ 7,350 $ 32,350

31-08-

2047 Interim dividend paid $ 21,000 $ 53,350

28-10-

2017 Payment of PayG Tax Instalment $ 7,000 $ 60,350

28-02-

2018 Payment of PayG Tax Instalment $ 7,000 $ 67,350

31-03-

2018 Payment of Final Dividend

$

28,000 $ 39,350

31-03-

2018 Distribution of franking credit $ 7,200 $ 46,550

28-04-

2018 Payment of PayG Tax Instalment $ 7,000 $ 53,550

05-06-

2018 Payment of Income Tax $ 2,000 $ 55,550

Answer to 4 B:

Issue:

Conclusion:

Conclusively the income that are obtained by the taxpayer will be held assessable

under “section 6-5 of the ITAA 1997” and the expenses incurred would be allowed for

deductions under “section 8-1 of the ITAA 1997”.

Answer to Question 4

Answer to 4 A:

Franked Account Balance

Date Description Dr Cr Balance

01-07-

2017 Balance Forward $ 10,000

21-07-

2017 PayG Instalment Payment $ 15,000 $ 25,000

31-07-

2017 Fully franked dividend $ 7,350 $ 32,350

31-08-

2047 Interim dividend paid $ 21,000 $ 53,350

28-10-

2017 Payment of PayG Tax Instalment $ 7,000 $ 60,350

28-02-

2018 Payment of PayG Tax Instalment $ 7,000 $ 67,350

31-03-

2018 Payment of Final Dividend

$

28,000 $ 39,350

31-03-

2018 Distribution of franking credit $ 7,200 $ 46,550

28-04-

2018 Payment of PayG Tax Instalment $ 7,000 $ 53,550

05-06-

2018 Payment of Income Tax $ 2,000 $ 55,550

Answer to 4 B:

Issue:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Are the taxpayer allowed to claim deductions for legal expenses that are incurred in

producing the taxable income under “section 8-1 of the ITAA 1997”.

Laws:

“Section 8-1 of the ITAA 1997”

“Herald Weekly Times v FCT (1932)”

Applications:

Usually “section 8-1 of the ITAA 1997” legal expenses are incurred in gaining or

producing the taxable income or incurred relation to any business activities are held as

allowable deductions (Schmalbeck et al. 2015). Referring to the case of “Herald Weekly

Times v FCT (1932)” the legal expenses incurred by Amusement Pty Ltd would be allowed

as deductions under “section 8-1 of the ITAA 1997” since it was incurred in gaining or

producing the taxable income.

Conclusion:

The legal expenses incurred by Amusement Pty Ltd is related to the derivation of

business income and would be considered as assessable income under “section 8-1 of the

ITAA 1997”.

Answer to 4 C:

Issue:

Is the taxpayer allowed to claim deductions relating to the expenses occurred for the

childcare under “section 8-1 of the ITAA 1997”?

Laws:

Lodge v FCT

Are the taxpayer allowed to claim deductions for legal expenses that are incurred in

producing the taxable income under “section 8-1 of the ITAA 1997”.

Laws:

“Section 8-1 of the ITAA 1997”

“Herald Weekly Times v FCT (1932)”

Applications:

Usually “section 8-1 of the ITAA 1997” legal expenses are incurred in gaining or

producing the taxable income or incurred relation to any business activities are held as

allowable deductions (Schmalbeck et al. 2015). Referring to the case of “Herald Weekly

Times v FCT (1932)” the legal expenses incurred by Amusement Pty Ltd would be allowed

as deductions under “section 8-1 of the ITAA 1997” since it was incurred in gaining or

producing the taxable income.

Conclusion:

The legal expenses incurred by Amusement Pty Ltd is related to the derivation of

business income and would be considered as assessable income under “section 8-1 of the

ITAA 1997”.

Answer to 4 C:

Issue:

Is the taxpayer allowed to claim deductions relating to the expenses occurred for the

childcare under “section 8-1 of the ITAA 1997”?

Laws:

Lodge v FCT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Section 8-1 of the ITAA 1997 Section 8-1 (2) of the ITAA 1997

Applications:

“Section 8-1 (2) of the ITAA 1997” explains that expenses that are private or domestic

in nature are non-allowable under both the positive and second negative limbs. The court of

law in “Lodge v FCT” denied the taxpayer to claim deductions for expenses incurred in

childcare expenses (Wilson 2015). Similarly, the child care centre expenses incurred by Eve

will not allowed for deductions under “section 8-1 of the ITAA 1997” since it was private in

nature.

Conclusion:

On a conclusive note the child care expenses incurred by Eve are non-allowable

deductions under “section 8-1 of the ITAA 1997” since it was private in nature.

Answer to D:

Issues:

Is taxpayer allowed to claim deductions for expenses paid for subscription to trade

union under “section 8-1 of the ITAA 1997”?

Laws:

F.C of T v Gordon

“Section 8-1 of the ITAA 1997”

Applications:

“Section 8-1 of the ITAA 1997” provides that subscriptions to trade unions are

allowed as deductions since it is incurred in gaining the assessable income. The law court in

Section 8-1 of the ITAA 1997 Section 8-1 (2) of the ITAA 1997

Applications:

“Section 8-1 (2) of the ITAA 1997” explains that expenses that are private or domestic

in nature are non-allowable under both the positive and second negative limbs. The court of

law in “Lodge v FCT” denied the taxpayer to claim deductions for expenses incurred in

childcare expenses (Wilson 2015). Similarly, the child care centre expenses incurred by Eve

will not allowed for deductions under “section 8-1 of the ITAA 1997” since it was private in

nature.

Conclusion:

On a conclusive note the child care expenses incurred by Eve are non-allowable

deductions under “section 8-1 of the ITAA 1997” since it was private in nature.

Answer to D:

Issues:

Is taxpayer allowed to claim deductions for expenses paid for subscription to trade

union under “section 8-1 of the ITAA 1997”?

Laws:

F.C of T v Gordon

“Section 8-1 of the ITAA 1997”

Applications:

“Section 8-1 of the ITAA 1997” provides that subscriptions to trade unions are

allowed as deductions since it is incurred in gaining the assessable income. The law court in

11TAXATION LAW

“F.C of T v Gordon” stated that subscription paid by the taxpayer to trade union are

considered for deductions (McDaniel 2017). The subscriptions paid by the manufacturers to

the Australian Manufacturer Worker Union will be allowed as deductions under section

“Section 8-1 of the ITAA 1997”.

Conclusion:

On a conclusive the expenses of the trade union subscriptions are in the course of

gaining assessable hence it would be allowed for taxation.

“F.C of T v Gordon” stated that subscription paid by the taxpayer to trade union are

considered for deductions (McDaniel 2017). The subscriptions paid by the manufacturers to

the Australian Manufacturer Worker Union will be allowed as deductions under section

“Section 8-1 of the ITAA 1997”.

Conclusion:

On a conclusive the expenses of the trade union subscriptions are in the course of

gaining assessable hence it would be allowed for taxation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.