Taxation Law: Calculating Andrew Smith's Assessable Income for 2019

VerifiedAdded on 2023/04/11

|6

|620

|293

Report

AI Summary

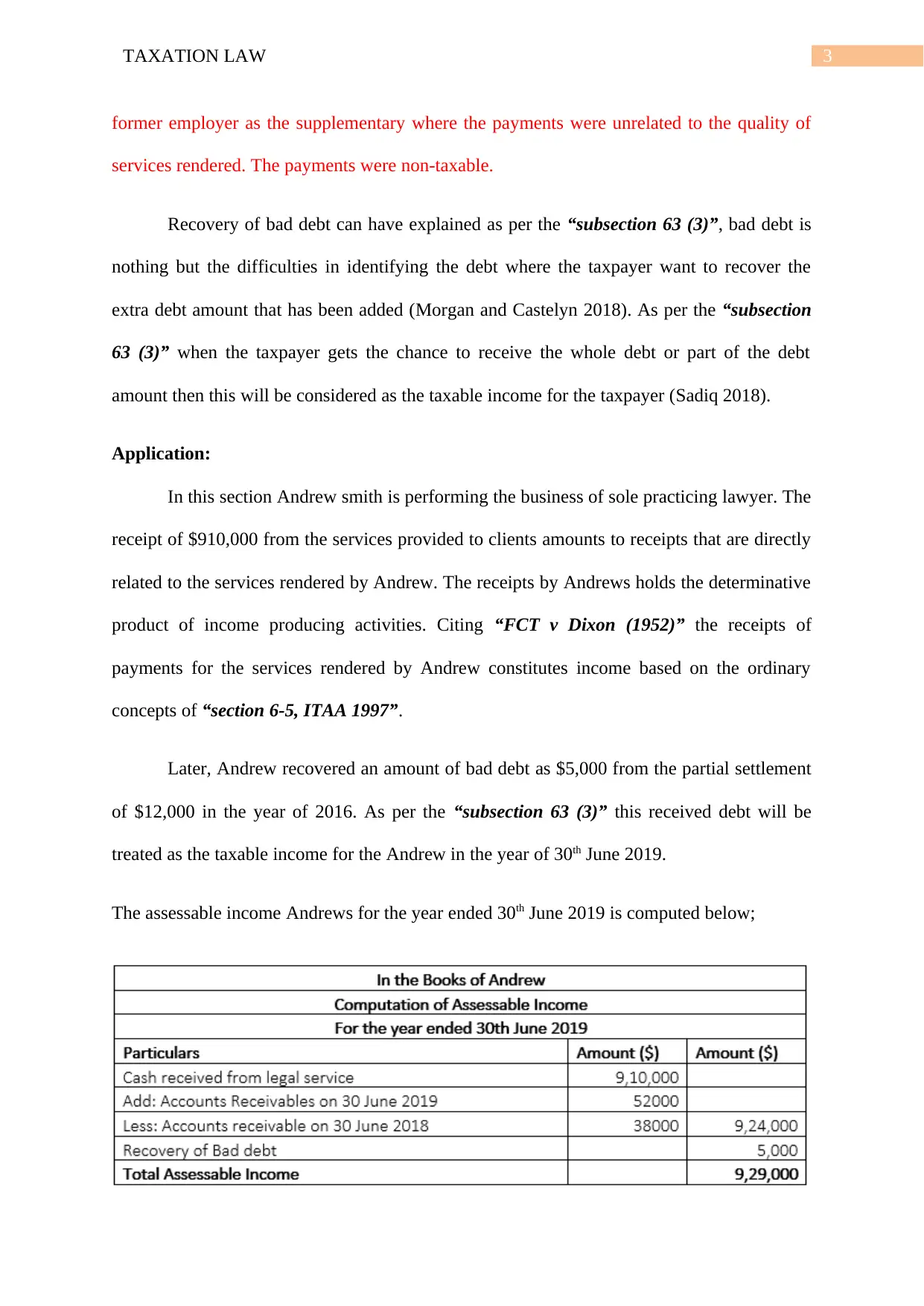

This report provides a detailed calculation of Andrew Smith's assessable income for the year ending June 30, 2019, based on his sole legal practice. It addresses the tax implications of cash received from clients for legal services, accounts receivable, and the recovery of a bad debt. The analysis applies relevant sections of the ITAA 1997, specifically Section 6-5 regarding ordinary income and subsection 63(3) concerning the recovery of bad debts. The report uses the 'cite, describe, apply' approach, referencing case law such as FCT v Dixon (1952) to support the determination of income from services rendered. The recovered bad debt of $5,000 is also assessed as taxable income under legislative provisions, contributing to the final calculation of Andrew's assessable income for the specified year.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.