LAWS20060 Taxation Law: Comprehensive Analysis of Australian Tax

VerifiedAdded on 2023/06/08

|14

|2898

|154

Report

AI Summary

This report provides a comprehensive analysis of key concepts in Australian taxation law. It addresses various aspects including the purpose of taxation, equity in taxation, calculation of taxable income, progressive tax systems, and the treatment of allowances. The report also examines the residency test for taxation purposes, determining whether an individual is considered an Australian resident based on factors such as physical presence, family ties, and intention to reside. Furthermore, it delves into the calculation of income tax, assessable income, and deductible expenses, referencing relevant sections of the Income Tax Assessment Act and relevant case law. The analysis extends to the characteristics of a business for tax purposes and the deductibility of various business expenses. The document is available on Desklib, which provides a platform with past papers and solved assignments for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer 1....................................................................................................................................2

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................7

Answer 5....................................................................................................................................8

Answer 6....................................................................................................................................9

References................................................................................................................................12

Table of Contents

Answer 1....................................................................................................................................2

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................7

Answer 5....................................................................................................................................8

Answer 6....................................................................................................................................9

References................................................................................................................................12

2TAXATION LAW

Answer 1

Answer A

Tax is considered to be compulsory contribution towards supporting the government to

operate. This is levied on property, persons, commodities, transactions and income. Thus the

primary purpose of taxation is to provide financial resources to the government so that it can

operate efficiently (Barkoczy 2016).

Answer B

Equity with respect to the discussion of a good taxation system does not signify treating

equally. This means that person having the higher income has to be taxed more as compared

to a person having a lower income so as to maintain a social balance in society. If all incomes

are equally taxed it would be unfair on the part of those who have a lower income (Becker,

Reimer and Rust 2015).

Answer C

According to section 4-15 of the Income Tax Assessment Act 1997 taxable income can be

worked out in three steps. The first step include adding all assessable income for the year.

Step two includes adding all the applicable deductions under division 8 and the final step is to

deduct from the assessable income the deductions unless they exceed (Devos and Zackrisson

2015).

Answer D

A progressive tax system aims at achieving equality with respect to the taxes imposed onto

individuals. In this system more tax is imposed in the persons who have a higher income as

compared to those who have a lower income. This reduces the burden of taxation from low

income groups and trigger income equality (Becker, Reimer and Rust 2015).

Answer 1

Answer A

Tax is considered to be compulsory contribution towards supporting the government to

operate. This is levied on property, persons, commodities, transactions and income. Thus the

primary purpose of taxation is to provide financial resources to the government so that it can

operate efficiently (Barkoczy 2016).

Answer B

Equity with respect to the discussion of a good taxation system does not signify treating

equally. This means that person having the higher income has to be taxed more as compared

to a person having a lower income so as to maintain a social balance in society. If all incomes

are equally taxed it would be unfair on the part of those who have a lower income (Becker,

Reimer and Rust 2015).

Answer C

According to section 4-15 of the Income Tax Assessment Act 1997 taxable income can be

worked out in three steps. The first step include adding all assessable income for the year.

Step two includes adding all the applicable deductions under division 8 and the final step is to

deduct from the assessable income the deductions unless they exceed (Devos and Zackrisson

2015).

Answer D

A progressive tax system aims at achieving equality with respect to the taxes imposed onto

individuals. In this system more tax is imposed in the persons who have a higher income as

compared to those who have a lower income. This reduces the burden of taxation from low

income groups and trigger income equality (Becker, Reimer and Rust 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

.

Answer E

Section 15.2 of the Income Tax Assessment Act 1997 includes the value of allowances in

assessable income.

Answer F

Taxation Ruling TR 2004/15 deals with the question that whether a company which has not

been incorporated in Australia is a resident for taxation purpose of Australia

Answer G

The two divisions which provides for deduction of capital expenditure in the ITAA 97 are

Subdivision 40H and Subdivision 40I

Answer H

The applicable tax rate for a taxpayer who has $80,000 of taxable income in 2017/18 is 0%

till $18200, 19% till $37000 and 32.5% for income above $37000 till $87000. Thus his tax

would be $3572+ (80000-37001)*32.5 which is $17546.68

Answer I

Sub-divisions of Income Tax Assessment Act 1997 list the provisions that treat amounts as

Non Assessable Non Exempt income are subdivision 50A and 50B

Answer J

The applicable rate for motor vehicles with an engine capacity over 2500cc is 63 cents

(Becker, Reimer and Rust 2015).

.

.

Answer E

Section 15.2 of the Income Tax Assessment Act 1997 includes the value of allowances in

assessable income.

Answer F

Taxation Ruling TR 2004/15 deals with the question that whether a company which has not

been incorporated in Australia is a resident for taxation purpose of Australia

Answer G

The two divisions which provides for deduction of capital expenditure in the ITAA 97 are

Subdivision 40H and Subdivision 40I

Answer H

The applicable tax rate for a taxpayer who has $80,000 of taxable income in 2017/18 is 0%

till $18200, 19% till $37000 and 32.5% for income above $37000 till $87000. Thus his tax

would be $3572+ (80000-37001)*32.5 which is $17546.68

Answer I

Sub-divisions of Income Tax Assessment Act 1997 list the provisions that treat amounts as

Non Assessable Non Exempt income are subdivision 50A and 50B

Answer J

The applicable rate for motor vehicles with an engine capacity over 2500cc is 63 cents

(Becker, Reimer and Rust 2015).

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer 2

Issue

The issue in the situation is to determine whether Martelle is an Australian resident for tax

purpose or not.

Rule

There are various tests which are applied in situations to identify whether a person is an

Australia resident for tax purpose or not. These tests include the resides test and the

permanent place of abode test (TR 98/17 and TR IT 2650). The test analyzes the physical

presence of the person in Australia, presence of family or economic tie, duration and

frequency of visit, intention of visit, location and maintenance of assets, permanent home and

employment ties (Evans, Lignier and Tran-Nam 2016). The 183 day test states that if a

person stays in Australia for more than 183 days they are considered to be residents. However

the ATO will not hold such person as a resident of Australia for taxation purpose if such

person has a place of abode outside Australia and does not have the intention to take up

residency (Becker, Reimer and Rust 2015).

The definition or resident has been provided by ITAA 1936 via section 6(1). A person will be

a resident if he or she resides in Australia with respect to the general meaning of reside. Any

single factor is not enough to prove the residency of a person. In FC of T v. Pechey 75 ATC

4083; (1975) 5 ATR 322 it had been stated by the court that a person will have the intention

to stay in Australia if they reside for a time which is more than the time required to do the

work.

It has been provided by s 6-5 and 6-10 that resident tax payers are to pay taxes on all incomes

made by them irrespective of from where they have been sourced.

Application

Answer 2

Issue

The issue in the situation is to determine whether Martelle is an Australian resident for tax

purpose or not.

Rule

There are various tests which are applied in situations to identify whether a person is an

Australia resident for tax purpose or not. These tests include the resides test and the

permanent place of abode test (TR 98/17 and TR IT 2650). The test analyzes the physical

presence of the person in Australia, presence of family or economic tie, duration and

frequency of visit, intention of visit, location and maintenance of assets, permanent home and

employment ties (Evans, Lignier and Tran-Nam 2016). The 183 day test states that if a

person stays in Australia for more than 183 days they are considered to be residents. However

the ATO will not hold such person as a resident of Australia for taxation purpose if such

person has a place of abode outside Australia and does not have the intention to take up

residency (Becker, Reimer and Rust 2015).

The definition or resident has been provided by ITAA 1936 via section 6(1). A person will be

a resident if he or she resides in Australia with respect to the general meaning of reside. Any

single factor is not enough to prove the residency of a person. In FC of T v. Pechey 75 ATC

4083; (1975) 5 ATR 322 it had been stated by the court that a person will have the intention

to stay in Australia if they reside for a time which is more than the time required to do the

work.

It has been provided by s 6-5 and 6-10 that resident tax payers are to pay taxes on all incomes

made by them irrespective of from where they have been sourced.

Application

5TAXATION LAW

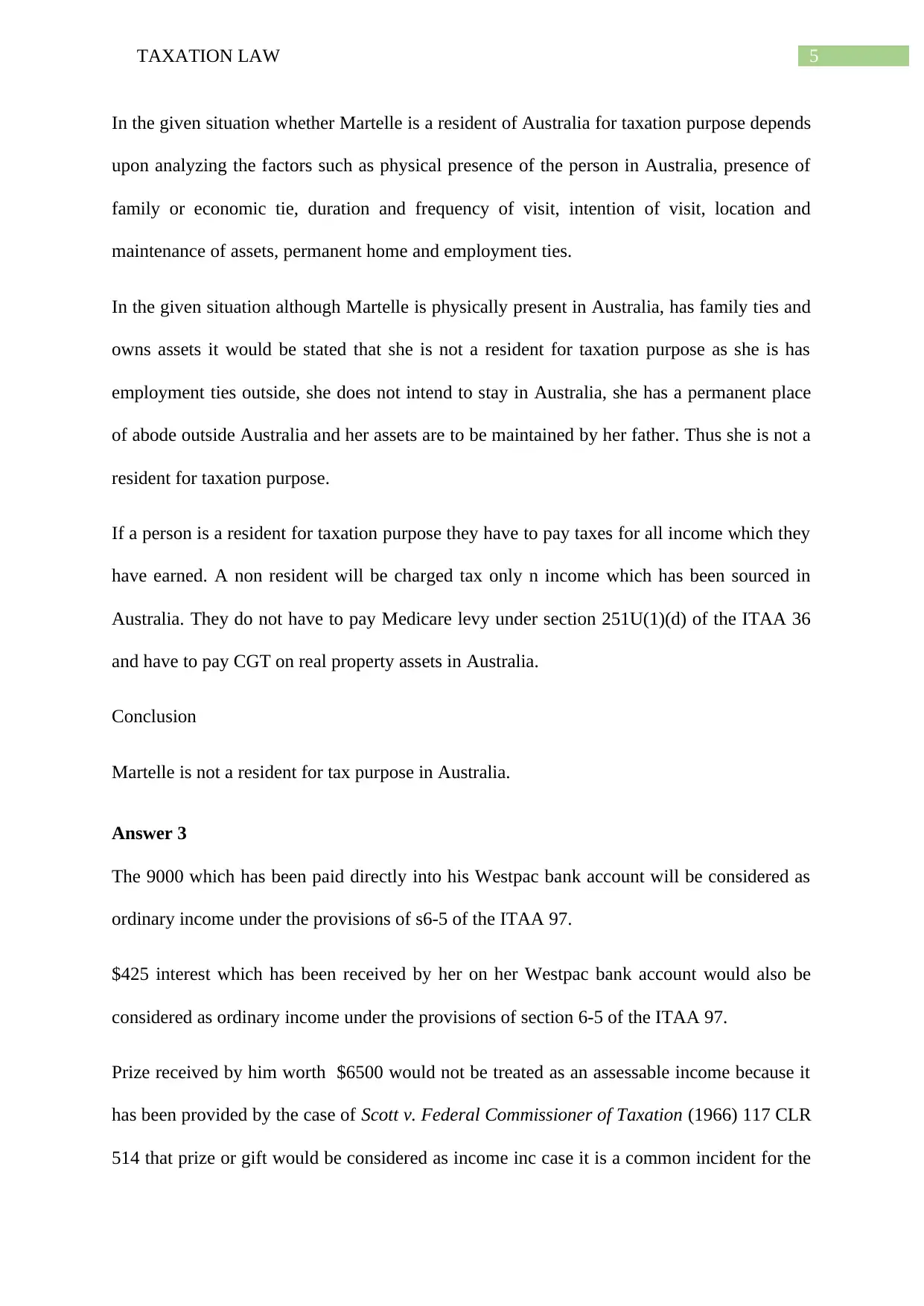

In the given situation whether Martelle is a resident of Australia for taxation purpose depends

upon analyzing the factors such as physical presence of the person in Australia, presence of

family or economic tie, duration and frequency of visit, intention of visit, location and

maintenance of assets, permanent home and employment ties.

In the given situation although Martelle is physically present in Australia, has family ties and

owns assets it would be stated that she is not a resident for taxation purpose as she is has

employment ties outside, she does not intend to stay in Australia, she has a permanent place

of abode outside Australia and her assets are to be maintained by her father. Thus she is not a

resident for taxation purpose.

If a person is a resident for taxation purpose they have to pay taxes for all income which they

have earned. A non resident will be charged tax only n income which has been sourced in

Australia. They do not have to pay Medicare levy under section 251U(1)(d) of the ITAA 36

and have to pay CGT on real property assets in Australia.

Conclusion

Martelle is not a resident for tax purpose in Australia.

Answer 3

The 9000 which has been paid directly into his Westpac bank account will be considered as

ordinary income under the provisions of s6-5 of the ITAA 97.

$425 interest which has been received by her on her Westpac bank account would also be

considered as ordinary income under the provisions of section 6-5 of the ITAA 97.

Prize received by him worth $6500 would not be treated as an assessable income because it

has been provided by the case of Scott v. Federal Commissioner of Taxation (1966) 117 CLR

514 that prize or gift would be considered as income inc case it is a common incident for the

In the given situation whether Martelle is a resident of Australia for taxation purpose depends

upon analyzing the factors such as physical presence of the person in Australia, presence of

family or economic tie, duration and frequency of visit, intention of visit, location and

maintenance of assets, permanent home and employment ties.

In the given situation although Martelle is physically present in Australia, has family ties and

owns assets it would be stated that she is not a resident for taxation purpose as she is has

employment ties outside, she does not intend to stay in Australia, she has a permanent place

of abode outside Australia and her assets are to be maintained by her father. Thus she is not a

resident for taxation purpose.

If a person is a resident for taxation purpose they have to pay taxes for all income which they

have earned. A non resident will be charged tax only n income which has been sourced in

Australia. They do not have to pay Medicare levy under section 251U(1)(d) of the ITAA 36

and have to pay CGT on real property assets in Australia.

Conclusion

Martelle is not a resident for tax purpose in Australia.

Answer 3

The 9000 which has been paid directly into his Westpac bank account will be considered as

ordinary income under the provisions of s6-5 of the ITAA 97.

$425 interest which has been received by her on her Westpac bank account would also be

considered as ordinary income under the provisions of section 6-5 of the ITAA 97.

Prize received by him worth $6500 would not be treated as an assessable income because it

has been provided by the case of Scott v. Federal Commissioner of Taxation (1966) 117 CLR

514 that prize or gift would be considered as income inc case it is a common incident for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

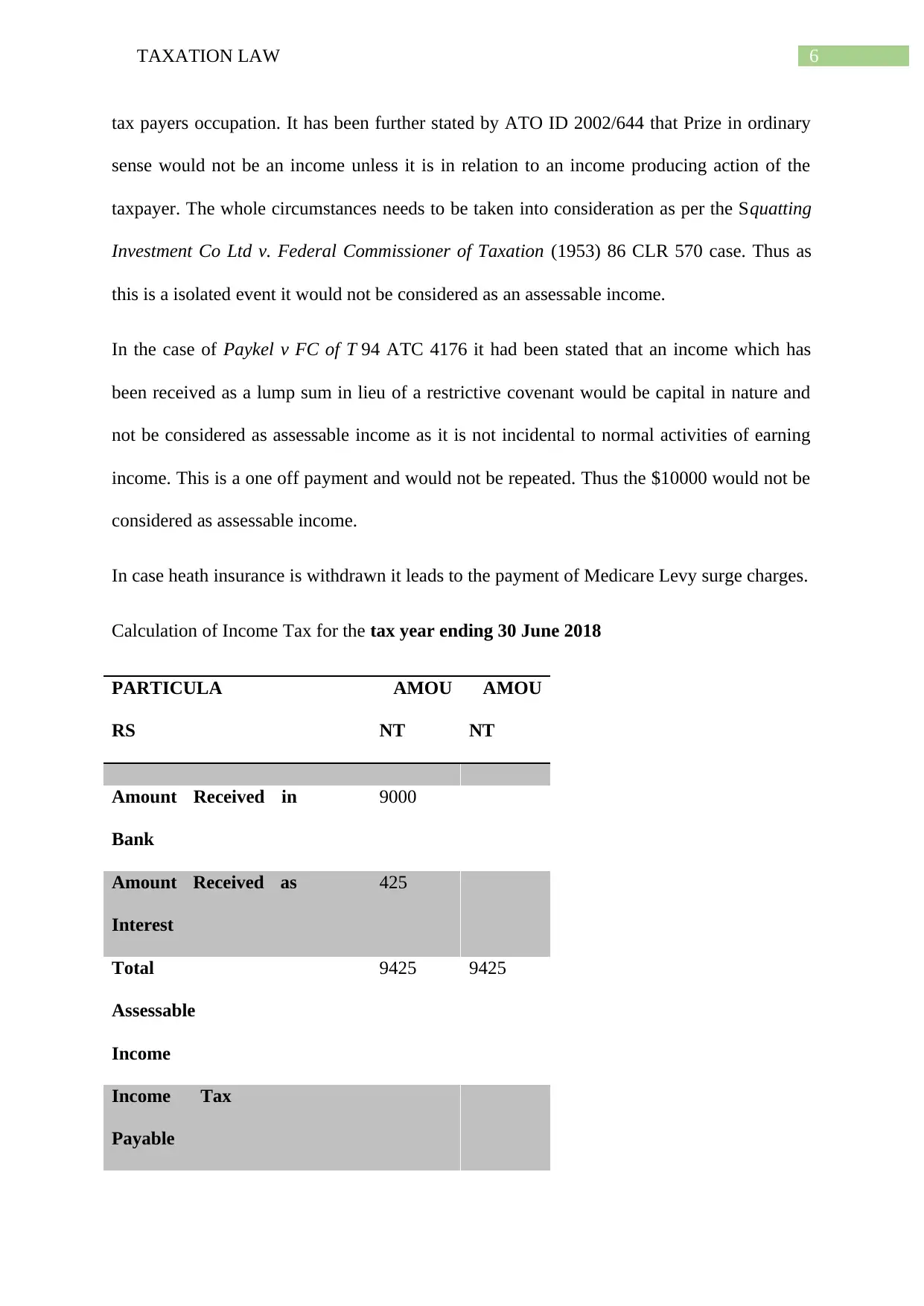

tax payers occupation. It has been further stated by ATO ID 2002/644 that Prize in ordinary

sense would not be an income unless it is in relation to an income producing action of the

taxpayer. The whole circumstances needs to be taken into consideration as per the Squatting

Investment Co Ltd v. Federal Commissioner of Taxation (1953) 86 CLR 570 case. Thus as

this is a isolated event it would not be considered as an assessable income.

In the case of Paykel v FC of T 94 ATC 4176 it had been stated that an income which has

been received as a lump sum in lieu of a restrictive covenant would be capital in nature and

not be considered as assessable income as it is not incidental to normal activities of earning

income. This is a one off payment and would not be repeated. Thus the $10000 would not be

considered as assessable income.

In case heath insurance is withdrawn it leads to the payment of Medicare Levy surge charges.

Calculation of Income Tax for the tax year ending 30 June 2018

PARTICULA

RS

AMOU

NT

AMOU

NT

Amount Received in

Bank

9000

Amount Received as

Interest

425

Total

Assessable

Income

9425 9425

Income Tax

Payable

tax payers occupation. It has been further stated by ATO ID 2002/644 that Prize in ordinary

sense would not be an income unless it is in relation to an income producing action of the

taxpayer. The whole circumstances needs to be taken into consideration as per the Squatting

Investment Co Ltd v. Federal Commissioner of Taxation (1953) 86 CLR 570 case. Thus as

this is a isolated event it would not be considered as an assessable income.

In the case of Paykel v FC of T 94 ATC 4176 it had been stated that an income which has

been received as a lump sum in lieu of a restrictive covenant would be capital in nature and

not be considered as assessable income as it is not incidental to normal activities of earning

income. This is a one off payment and would not be repeated. Thus the $10000 would not be

considered as assessable income.

In case heath insurance is withdrawn it leads to the payment of Medicare Levy surge charges.

Calculation of Income Tax for the tax year ending 30 June 2018

PARTICULA

RS

AMOU

NT

AMOU

NT

Amount Received in

Bank

9000

Amount Received as

Interest

425

Total

Assessable

Income

9425 9425

Income Tax

Payable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

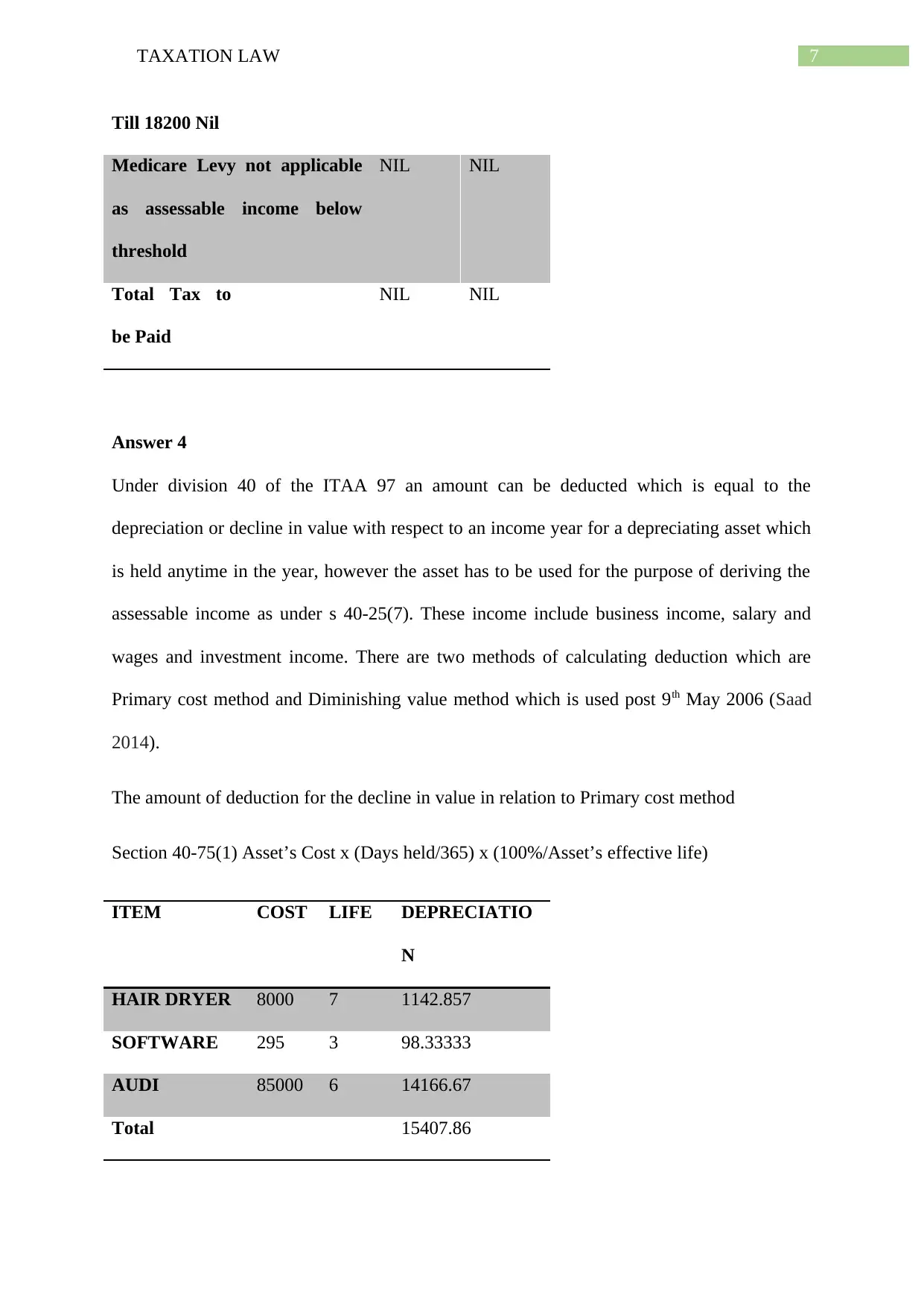

Till 18200 Nil

Medicare Levy not applicable

as assessable income below

threshold

NIL NIL

Total Tax to

be Paid

NIL NIL

Answer 4

Under division 40 of the ITAA 97 an amount can be deducted which is equal to the

depreciation or decline in value with respect to an income year for a depreciating asset which

is held anytime in the year, however the asset has to be used for the purpose of deriving the

assessable income as under s 40-25(7). These income include business income, salary and

wages and investment income. There are two methods of calculating deduction which are

Primary cost method and Diminishing value method which is used post 9th May 2006 (Saad

2014).

The amount of deduction for the decline in value in relation to Primary cost method

Section 40-75(1) Asset’s Cost x (Days held/365) x (100%/Asset’s effective life)

ITEM COST LIFE DEPRECIATIO

N

HAIR DRYER 8000 7 1142.857

SOFTWARE 295 3 98.33333

AUDI 85000 6 14166.67

Total 15407.86

Till 18200 Nil

Medicare Levy not applicable

as assessable income below

threshold

NIL NIL

Total Tax to

be Paid

NIL NIL

Answer 4

Under division 40 of the ITAA 97 an amount can be deducted which is equal to the

depreciation or decline in value with respect to an income year for a depreciating asset which

is held anytime in the year, however the asset has to be used for the purpose of deriving the

assessable income as under s 40-25(7). These income include business income, salary and

wages and investment income. There are two methods of calculating deduction which are

Primary cost method and Diminishing value method which is used post 9th May 2006 (Saad

2014).

The amount of deduction for the decline in value in relation to Primary cost method

Section 40-75(1) Asset’s Cost x (Days held/365) x (100%/Asset’s effective life)

ITEM COST LIFE DEPRECIATIO

N

HAIR DRYER 8000 7 1142.857

SOFTWARE 295 3 98.33333

AUDI 85000 6 14166.67

Total 15407.86

8TAXATION LAW

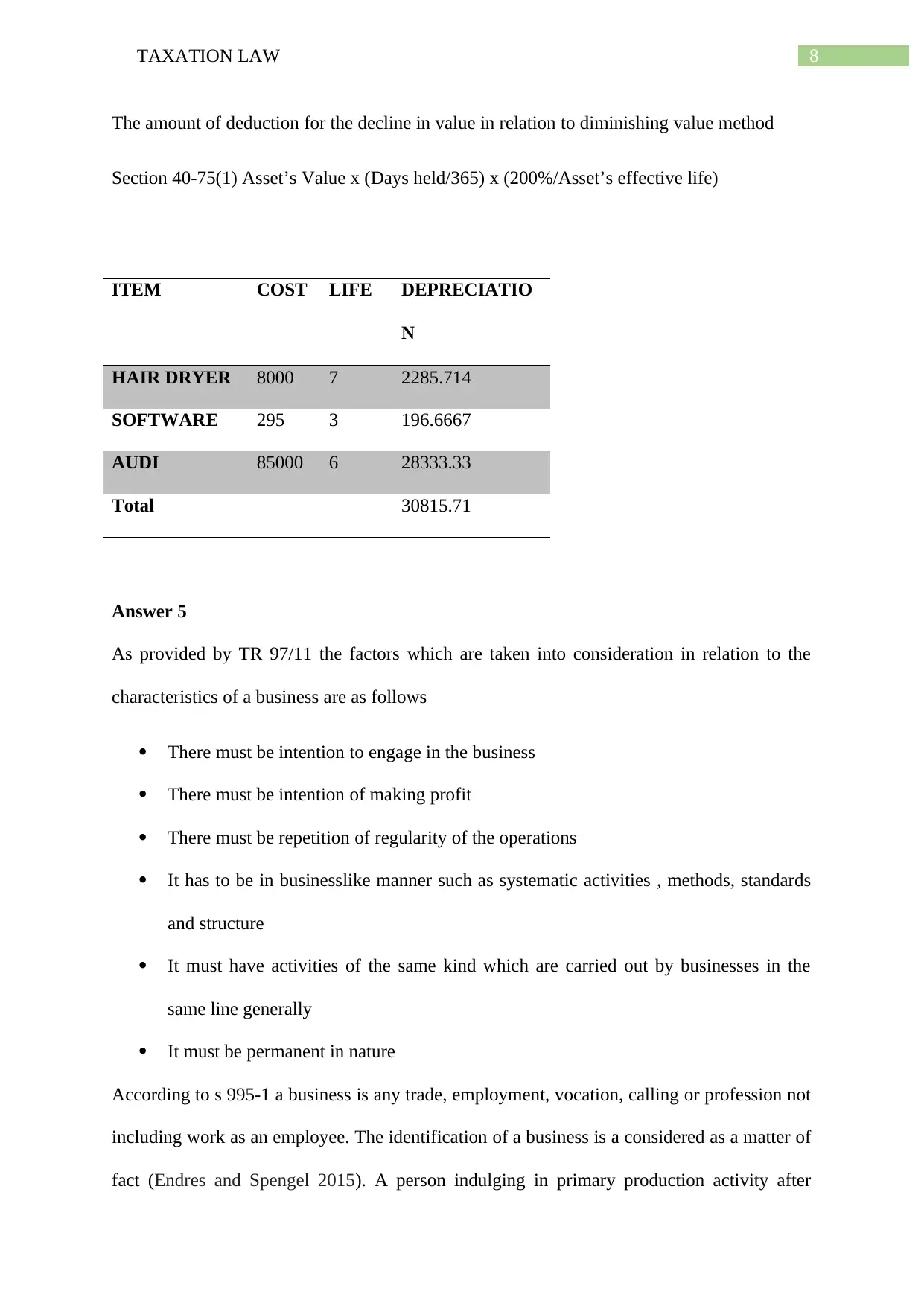

The amount of deduction for the decline in value in relation to diminishing value method

Section 40-75(1) Asset’s Value x (Days held/365) x (200%/Asset’s effective life)

ITEM COST LIFE DEPRECIATIO

N

HAIR DRYER 8000 7 2285.714

SOFTWARE 295 3 196.6667

AUDI 85000 6 28333.33

Total 30815.71

Answer 5

As provided by TR 97/11 the factors which are taken into consideration in relation to the

characteristics of a business are as follows

There must be intention to engage in the business

There must be intention of making profit

There must be repetition of regularity of the operations

It has to be in businesslike manner such as systematic activities , methods, standards

and structure

It must have activities of the same kind which are carried out by businesses in the

same line generally

It must be permanent in nature

According to s 995-1 a business is any trade, employment, vocation, calling or profession not

including work as an employee. The identification of a business is a considered as a matter of

fact (Endres and Spengel 2015). A person indulging in primary production activity after

The amount of deduction for the decline in value in relation to diminishing value method

Section 40-75(1) Asset’s Value x (Days held/365) x (200%/Asset’s effective life)

ITEM COST LIFE DEPRECIATIO

N

HAIR DRYER 8000 7 2285.714

SOFTWARE 295 3 196.6667

AUDI 85000 6 28333.33

Total 30815.71

Answer 5

As provided by TR 97/11 the factors which are taken into consideration in relation to the

characteristics of a business are as follows

There must be intention to engage in the business

There must be intention of making profit

There must be repetition of regularity of the operations

It has to be in businesslike manner such as systematic activities , methods, standards

and structure

It must have activities of the same kind which are carried out by businesses in the

same line generally

It must be permanent in nature

According to s 995-1 a business is any trade, employment, vocation, calling or profession not

including work as an employee. The identification of a business is a considered as a matter of

fact (Endres and Spengel 2015). A person indulging in primary production activity after

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

retirement is considered to have been carrying out a business even where he was a naval

officer in the case of FC of T v Ferguson 1979.

Thus in the given situation the above factors needs to be taken into consideration by Julie if

she wants to ensure that her ‘new business’ is interpreted as such by the ATO. For example in

the case of Case P67 82 ATC 317 stated in Taxation Ruling TR 2005/1 a person was held to

be carrying out a business of photography where he gave 12% of his total time in clicking

photos for the purpose of making a profit.

Answer 6

a) The salary cost of $300000 will be a deductible expense under the provisions of s 8-1

general deductions as it has been used for the purpose of gaining the business

assessable income.

b) This expense is subjected to the discretion of the ATO to be regarded as reasonable or

not as it is a expense which has been paid to a relative. It has been provided by section

26-35(1) of ITAA 1936 that the deduction of an amount made to a related entity can

be done as far as the commissioner considers it reasonable taking into consideration

age, nature if duty, hours word, total remuneration and wages claimed as deduction.

In this case also the amount of $4000 would be subjected to the consideration of the

commissioner. It is likely that $4000 is excessive for nine hours of work for a person

studying graphic designing.

c) The general rule under div 32 and section 32-5 state that a loss or outgoing for

providing entertainment is nit generally deductible with respect to s 8-1 of the ITAA

97. These expenses can only be claimed if they are for the purpose of gaining the

assessable income such as advertisement cost. Thus in the given situation the $900 on

membership to the local bowls club where he entertains clients is not deductible.

retirement is considered to have been carrying out a business even where he was a naval

officer in the case of FC of T v Ferguson 1979.

Thus in the given situation the above factors needs to be taken into consideration by Julie if

she wants to ensure that her ‘new business’ is interpreted as such by the ATO. For example in

the case of Case P67 82 ATC 317 stated in Taxation Ruling TR 2005/1 a person was held to

be carrying out a business of photography where he gave 12% of his total time in clicking

photos for the purpose of making a profit.

Answer 6

a) The salary cost of $300000 will be a deductible expense under the provisions of s 8-1

general deductions as it has been used for the purpose of gaining the business

assessable income.

b) This expense is subjected to the discretion of the ATO to be regarded as reasonable or

not as it is a expense which has been paid to a relative. It has been provided by section

26-35(1) of ITAA 1936 that the deduction of an amount made to a related entity can

be done as far as the commissioner considers it reasonable taking into consideration

age, nature if duty, hours word, total remuneration and wages claimed as deduction.

In this case also the amount of $4000 would be subjected to the consideration of the

commissioner. It is likely that $4000 is excessive for nine hours of work for a person

studying graphic designing.

c) The general rule under div 32 and section 32-5 state that a loss or outgoing for

providing entertainment is nit generally deductible with respect to s 8-1 of the ITAA

97. These expenses can only be claimed if they are for the purpose of gaining the

assessable income such as advertisement cost. Thus in the given situation the $900 on

membership to the local bowls club where he entertains clients is not deductible.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

d) Non-Deductible- this income would be not be deductible under the provisions of

section 8-1 of the ITAA 97 as it has no nexus of earning the assessable income. The

expenditure is not satisfying the positive limb as it is not incidental or relevant to gain

the assessable income.

e) Non-Deductible this income would be not be deductible under the provisions of

section 8-1 of the ITAA 97 as it has no nexus of earning the assessable income. The

expenditure is not satisfying the positive limb as it is not incidental or relevant to gain

the assessable income.

f) Deductible – this interest would be deductible as under the provisions of section 8-1

of the ITAA 97 as it has nexus of earning the assessable income and the interest is

paid in relation to it. The expenditure is satisfying the positive limb as it is not

incidental or relevant to gain the assessable income and no negative limb is trigged.

The provisions have also been discussed by the case of FC of T v. Smith 92 ATC

4380; (1992) 23 ATR 494.

g) Non-Deductible- This is because Travelling form home to work is considered an

expense of domestic or private nature and thus it would trigger the negative limb of

section 8-2 of the ITAA 97. The provisions had also been discussed in the case of FC

of T v. Lunnet 1958 where the court stated that traveling expenses for and two work

cannot be claimed as deductable as they do not have any nexus or perceived

connection with gaining the assessable income.

h) 80% deductible – Phone call expenses are considered to be of a private and domestic

nature and thus not deductible under section 8-2 of the ITAA 97. However if there is

evidence that such expenses have been incurred in relation to work then proportion to

which they have been used for work is deductible. Thus here as the phone is claimed

to be used 80% for work related issues, the expenses would be 80% deductible.

d) Non-Deductible- this income would be not be deductible under the provisions of

section 8-1 of the ITAA 97 as it has no nexus of earning the assessable income. The

expenditure is not satisfying the positive limb as it is not incidental or relevant to gain

the assessable income.

e) Non-Deductible this income would be not be deductible under the provisions of

section 8-1 of the ITAA 97 as it has no nexus of earning the assessable income. The

expenditure is not satisfying the positive limb as it is not incidental or relevant to gain

the assessable income.

f) Deductible – this interest would be deductible as under the provisions of section 8-1

of the ITAA 97 as it has nexus of earning the assessable income and the interest is

paid in relation to it. The expenditure is satisfying the positive limb as it is not

incidental or relevant to gain the assessable income and no negative limb is trigged.

The provisions have also been discussed by the case of FC of T v. Smith 92 ATC

4380; (1992) 23 ATR 494.

g) Non-Deductible- This is because Travelling form home to work is considered an

expense of domestic or private nature and thus it would trigger the negative limb of

section 8-2 of the ITAA 97. The provisions had also been discussed in the case of FC

of T v. Lunnet 1958 where the court stated that traveling expenses for and two work

cannot be claimed as deductable as they do not have any nexus or perceived

connection with gaining the assessable income.

h) 80% deductible – Phone call expenses are considered to be of a private and domestic

nature and thus not deductible under section 8-2 of the ITAA 97. However if there is

evidence that such expenses have been incurred in relation to work then proportion to

which they have been used for work is deductible. Thus here as the phone is claimed

to be used 80% for work related issues, the expenses would be 80% deductible.

11TAXATION LAW

i) Deductible, this is because the expenses have been incurred for the purpose of gaining

business income. The marketing conference is associated to business. Therefore the

positive limb if section 8-1 of the ITAA 97 will make the expenses deductible.

j) Deductible- under the provisions of section 25-5(1) of the ITAA 97 expenses incurred

in relation to the management of tax affairs are deductible. Thus $500 would also be

deductible.

i) Deductible, this is because the expenses have been incurred for the purpose of gaining

business income. The marketing conference is associated to business. Therefore the

positive limb if section 8-1 of the ITAA 97 will make the expenses deductible.

j) Deductible- under the provisions of section 25-5(1) of the ITAA 97 expenses incurred

in relation to the management of tax affairs are deductible. Thus $500 would also be

deductible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.