University Taxation Law Assignment: ACC3TAX S2 2019 Analysis

VerifiedAdded on 2022/10/17

|16

|1872

|336

Homework Assignment

AI Summary

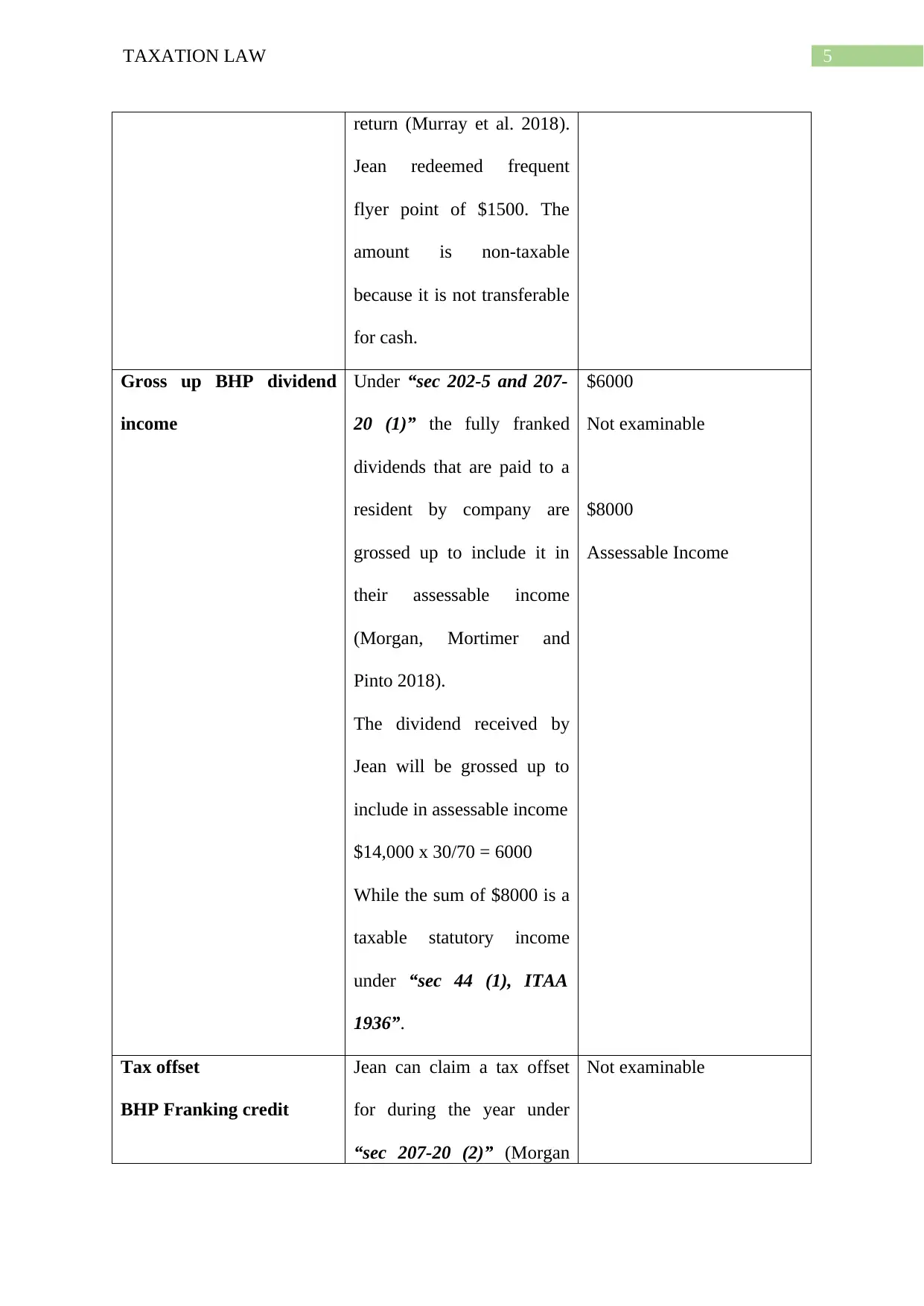

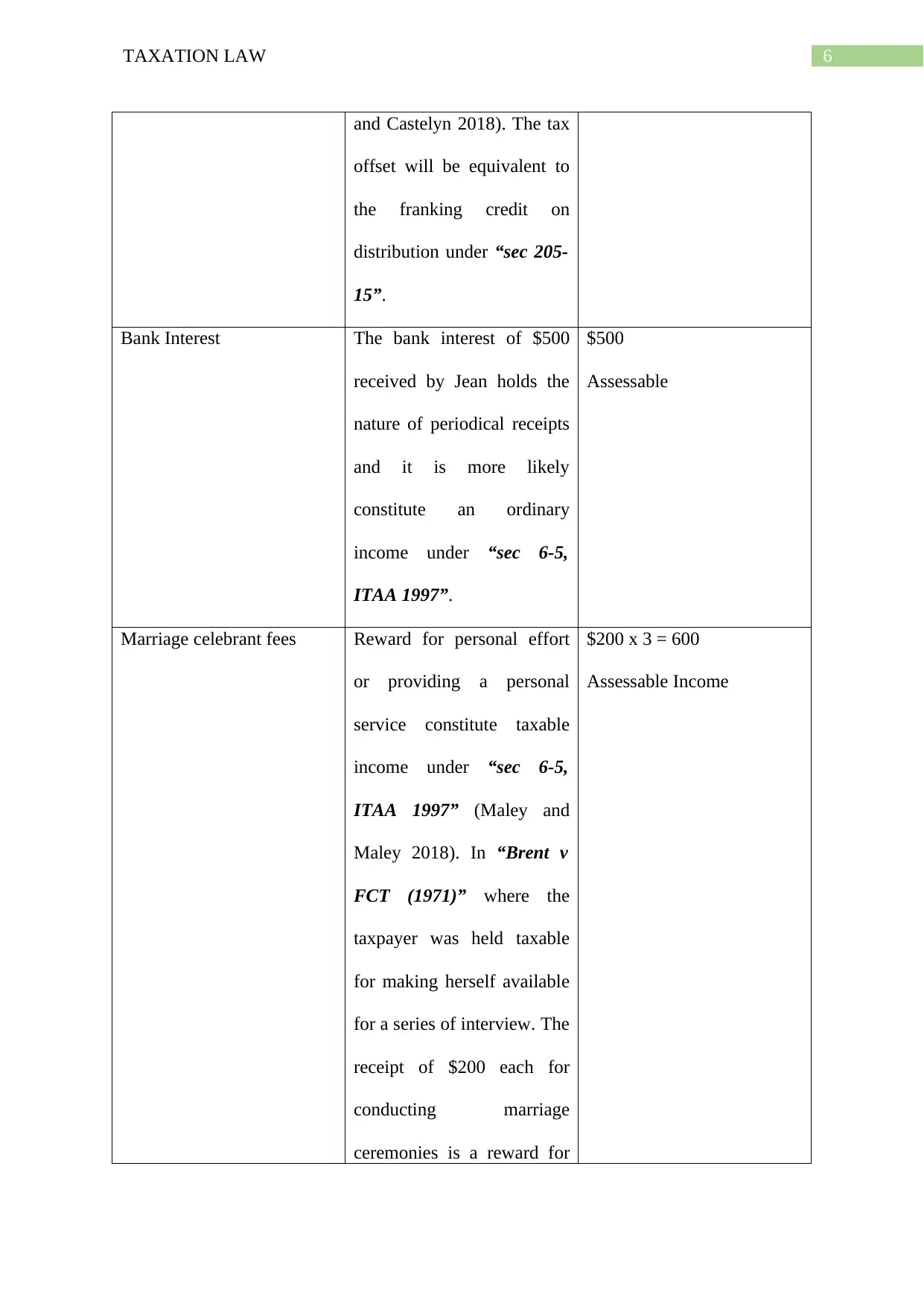

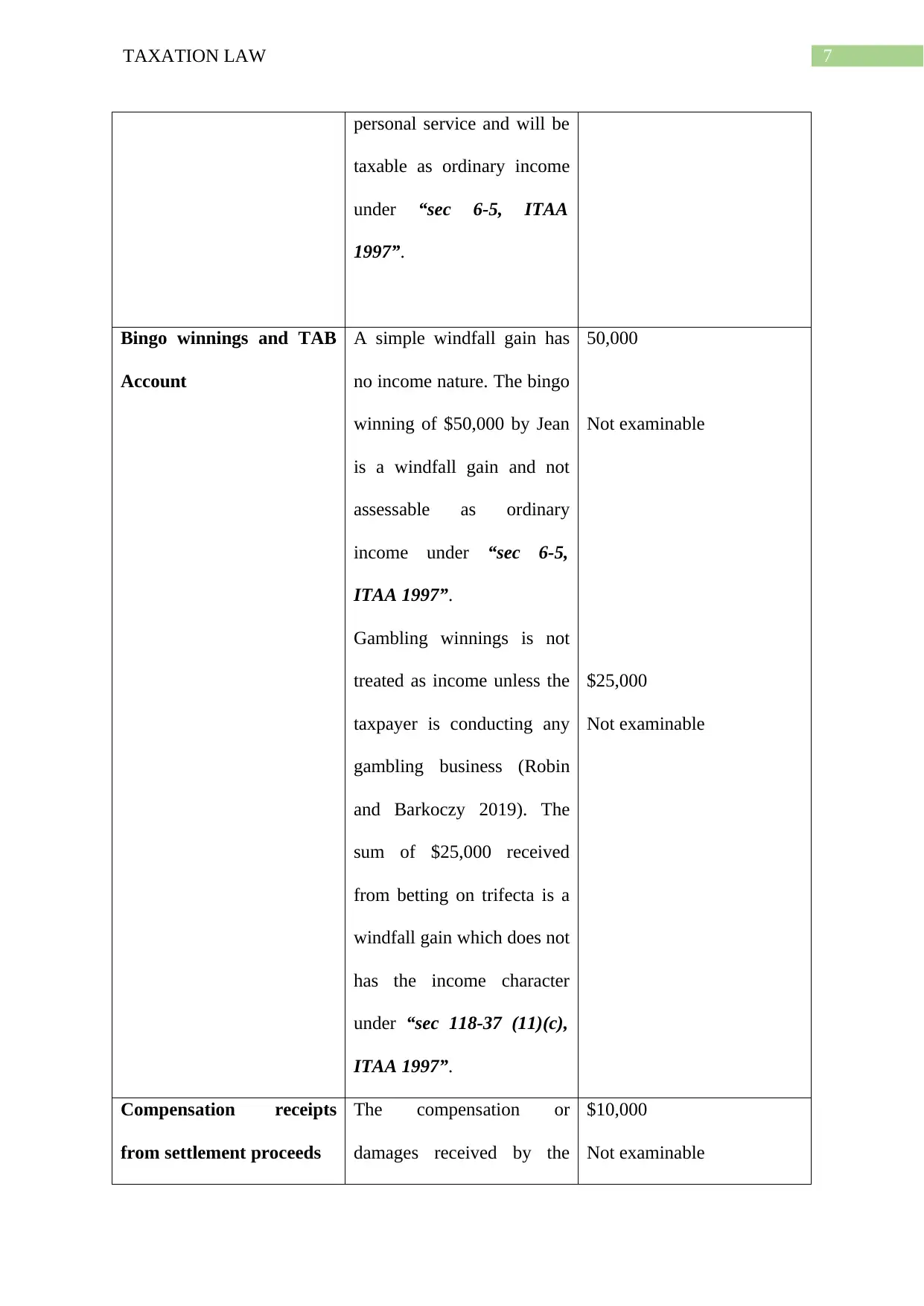

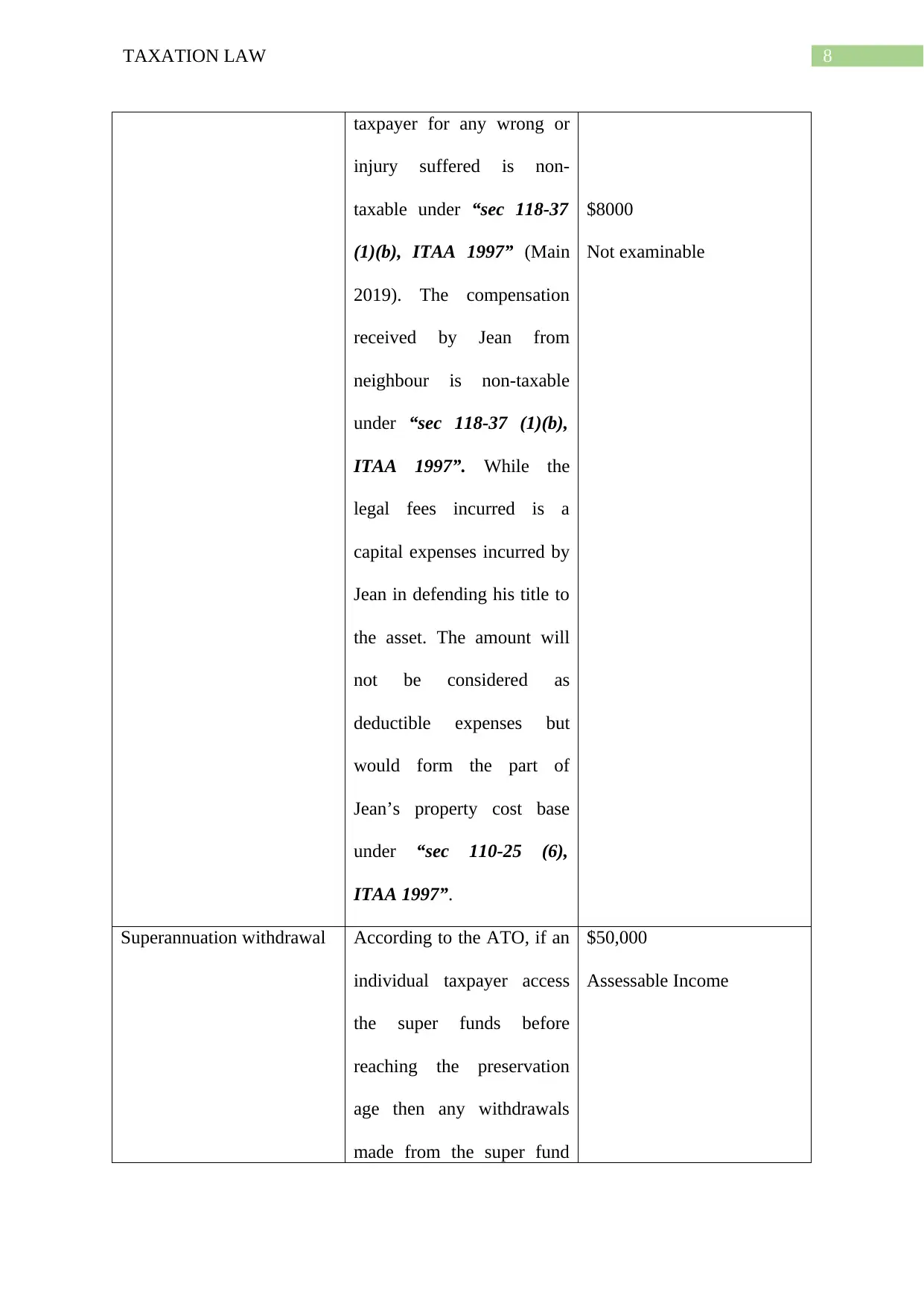

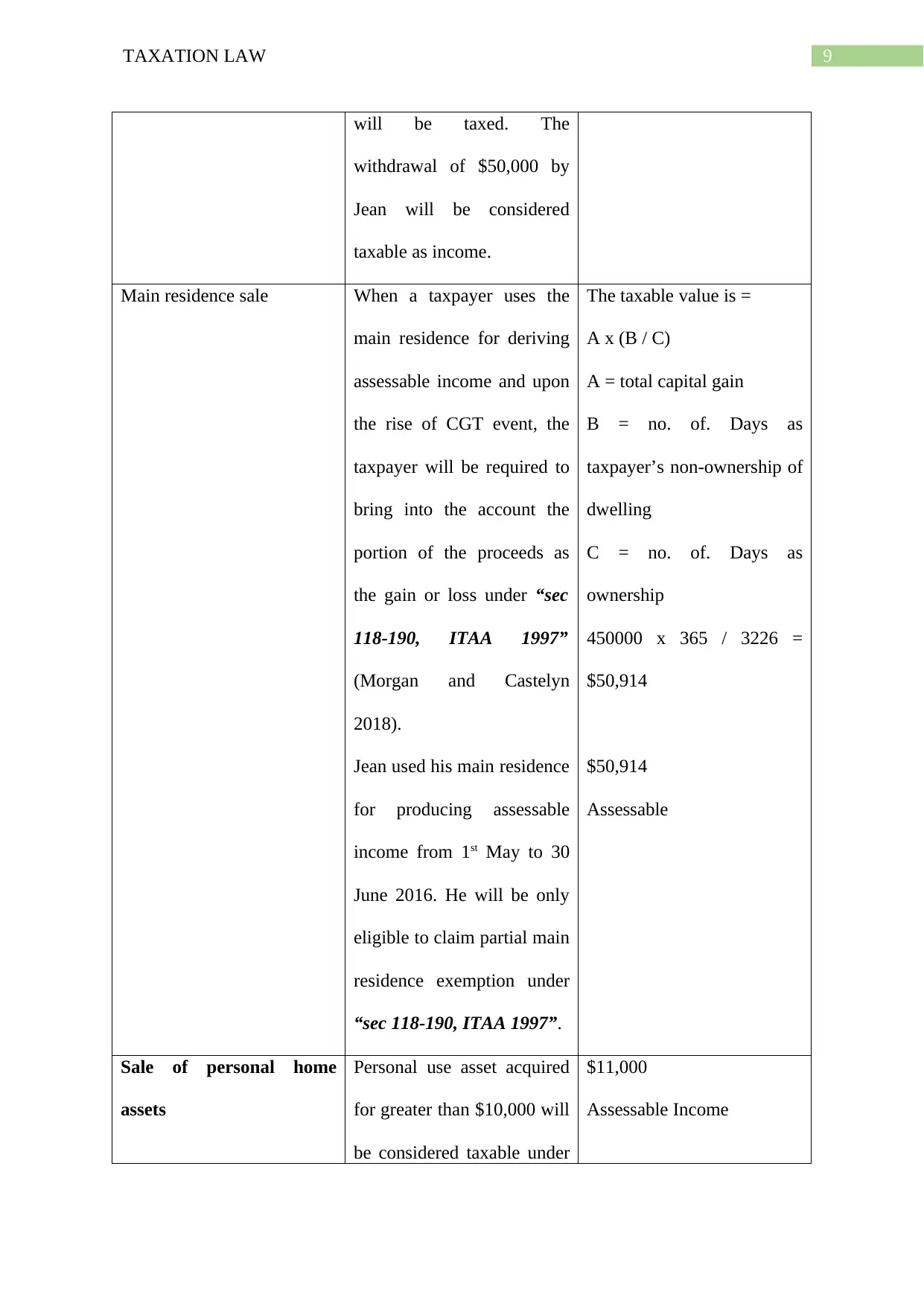

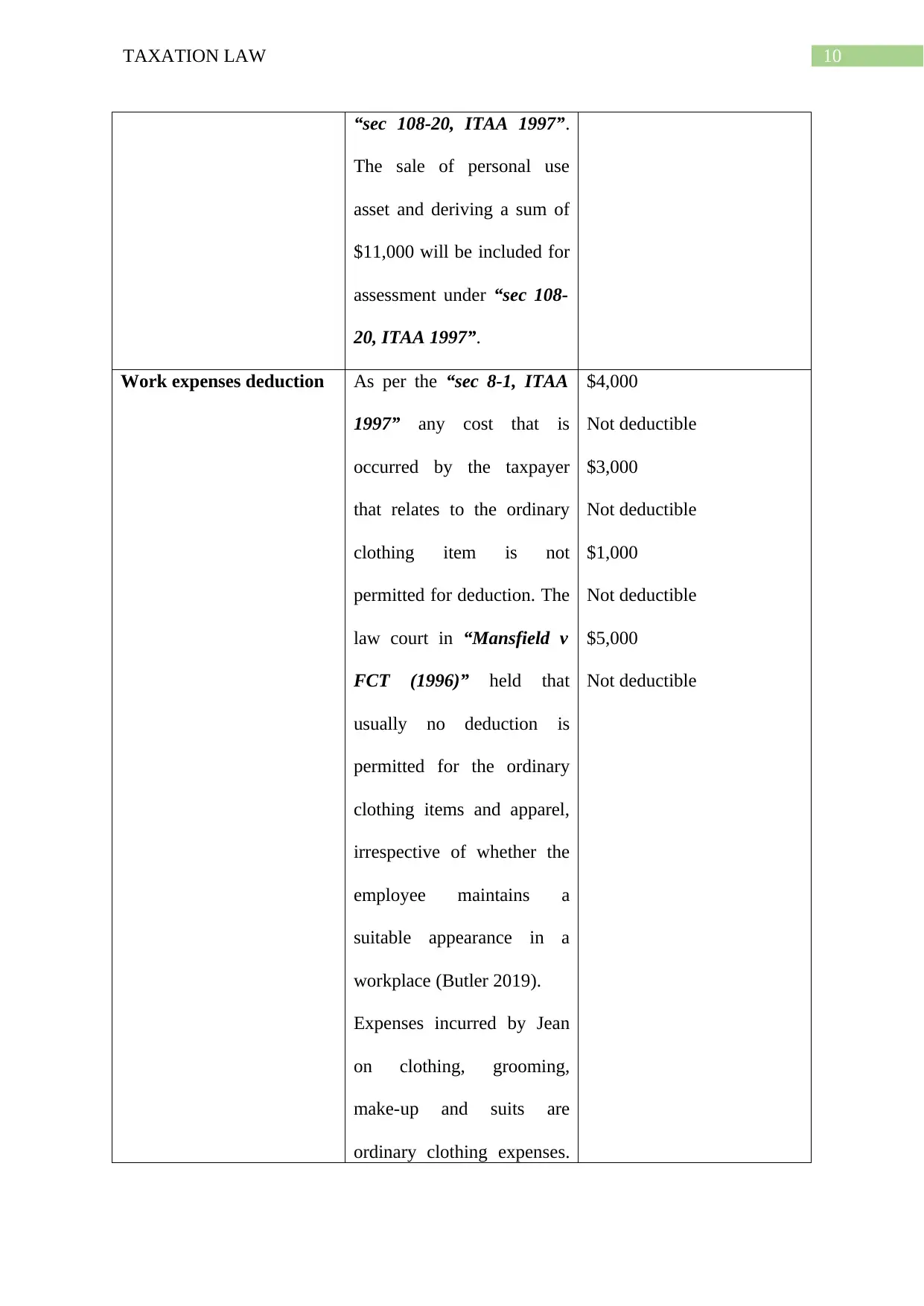

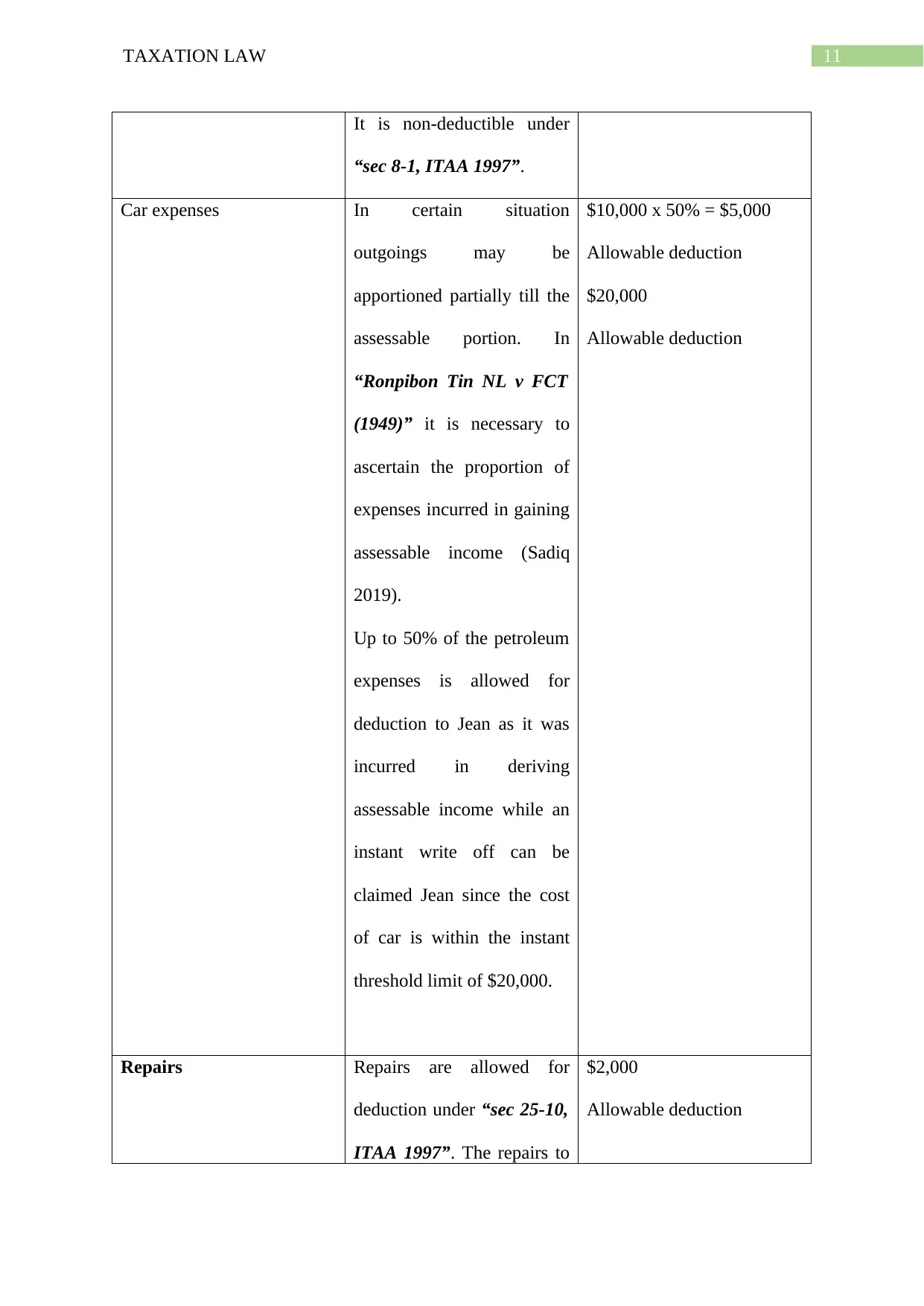

This document presents a comprehensive solution to a taxation law assignment, likely for an ACC3TAX course. The assignment analyzes various income sources, including wages, allowances, and dividends, determining their assessability under Australian tax law. It covers topics such as personal service income, entertainment allowances, unused leave, gifts, lump sum payments, and the treatment of frequent flyer points. The solution also addresses dividend income, bank interest, marriage celebrant fees, bingo winnings, compensation receipts, superannuation withdrawals, and the sale of a main residence. Furthermore, it examines work expenses, car expenses, and repair deductions. The document provides detailed explanations of relevant legislation, including the ITAA 1936 and ITAA 1997, and incorporates case law to support its analysis. The assignment concludes with a list of cited references, demonstrating a thorough understanding of taxation principles and their application to the given scenario. The solution is structured to address specific issues, providing the relevant law, reasoning, and the calculated amount for each item, making it a useful resource for students studying taxation law.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.