Holmes Institute HI6028 Taxation Law Assignment: CGT, Income, Loans

VerifiedAdded on 2023/03/31

|10

|2221

|145

Homework Assignment

AI Summary

This assignment addresses key aspects of Australian taxation law, including capital gains tax (CGT), income assessment, and the tax implications of loans. The first question analyzes CGT calculations for various assets, considering indexation methods and exemptions. The second question examines income from personal exertion, differentiating it from capital gains based on ITAA 1997 provisions, with examples of writing and manuscript sales. The third question evaluates the tax impact of a loan from a father to his son, considering interest payments, gift tax rebates, and the potential for the loan to be treated as assessable income. The assignment demonstrates an understanding of relevant legislation and principles through the analysis of real-life scenarios.

Taxation Theory, Practice &

Law

Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1...........................................................................................................................................................3

Question 2...........................................................................................................................................................6

Question 3:..........................................................................................................................................................7

Conclusion..........................................................................................................................................................8

References..........................................................................................................................................................9

Question 1...........................................................................................................................................................3

Question 2...........................................................................................................................................................6

Question 3:..........................................................................................................................................................7

Conclusion..........................................................................................................................................................8

References..........................................................................................................................................................9

Question 1

Capital gain tax incurs at the time of sale of any capital asset in the current year which is

purchased by an asessee in previous year (ATO, 2016). The variation in the selling and

purchasing price of capital asset is known as capital gain or loss. The tax which is liable to

pay on capital gain, termed as capital gain tax and must be paid in its current financial year.

There are different laws and regulations which are applied to assess capital gain tax in

Australia. Any capital assets which were purchased after 20th September 1985 are covered

under the capital gain tax regime (Faccio and Xu, 2015). Helen, who is a fashion designer,

seeking some advice related to capital gain tax consequences, as she has made some

transactions in her business. Provisions related to the capital gain are covered under this. The

Rate for capital gain tax is defined in the Australian tax regulatory is 23.5% but this is

applicable when an asset is captured by the assessee for twelve months or more (Evans,

Minas and Lim, 2015). The other provision is that there should be availed 50% discount on

the assets which are purchased by the assessee after 21st September 1999. Indexation

method is applied on the capital assets which are purchased before 21st September 1999 but

for the assets which are purchased after 21st September, 1999, in that case, both method can

be used by the assessee and chose any of them which could give least capital gain tax

(Edmonds, 2015).

As discussed the provisions and laws for the capital gain tax, all assets given in question 1

are purchased before 21st September 1999 and are treated under the Indexation method

(ATO, 2016). And for that purpose, there is a strong need to understand indexation method.

By using this method, assessee try to identify the purchasing cost of the capital asset in

present market in order to calculate capital gain tax (Martin, 2019). For that purpose

indexation factor is calculated by using consumer price index (CPI). Formula to calculate that

is as follows:

Indexation factor = CPI of the time in which CGT occurred/ CPI of the time or quarter the

asset was purchased

1. CGT on Antique Panting bought in 1985-

Capital gain tax incurs at the time of sale of any capital asset in the current year which is

purchased by an asessee in previous year (ATO, 2016). The variation in the selling and

purchasing price of capital asset is known as capital gain or loss. The tax which is liable to

pay on capital gain, termed as capital gain tax and must be paid in its current financial year.

There are different laws and regulations which are applied to assess capital gain tax in

Australia. Any capital assets which were purchased after 20th September 1985 are covered

under the capital gain tax regime (Faccio and Xu, 2015). Helen, who is a fashion designer,

seeking some advice related to capital gain tax consequences, as she has made some

transactions in her business. Provisions related to the capital gain are covered under this. The

Rate for capital gain tax is defined in the Australian tax regulatory is 23.5% but this is

applicable when an asset is captured by the assessee for twelve months or more (Evans,

Minas and Lim, 2015). The other provision is that there should be availed 50% discount on

the assets which are purchased by the assessee after 21st September 1999. Indexation

method is applied on the capital assets which are purchased before 21st September 1999 but

for the assets which are purchased after 21st September, 1999, in that case, both method can

be used by the assessee and chose any of them which could give least capital gain tax

(Edmonds, 2015).

As discussed the provisions and laws for the capital gain tax, all assets given in question 1

are purchased before 21st September 1999 and are treated under the Indexation method

(ATO, 2016). And for that purpose, there is a strong need to understand indexation method.

By using this method, assessee try to identify the purchasing cost of the capital asset in

present market in order to calculate capital gain tax (Martin, 2019). For that purpose

indexation factor is calculated by using consumer price index (CPI). Formula to calculate that

is as follows:

Indexation factor = CPI of the time in which CGT occurred/ CPI of the time or quarter the

asset was purchased

1. CGT on Antique Panting bought in 1985-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the regulations of Australian taxation, any capital asset which is purchased before 20th

September 1985 exempted from capital gain tax. This law of discount and the rate of capital gain tax

both are not applicable on capital assets purchased before the aforesaid time period (ATO, 2016). In

the given question the antique impressionism painting was purchased by helon’s father in February

1985 which is exempted from capital gain tax. Therefore there will be no CGT applicable in this

transaction (Minas, Lim and Evans, 2018).

2. CGT on Historical sculpture-

In the given question sculpture was purchased on December 1993 for $5500 which is before

21st September 1999. It is sold on 1st January 2018 for $6000. Therefore it will be treated

under indexation method. For the calculation of CGT we first find out the purchasing cost as

per the current period by using Consumer price index (Barkoczy, S. 2016).

Cost of purchase under indexation method= CPI of 1993/ CPI of 2018*purchase price

= 112.6/61.2*5500

= 10120

Capital gain or loss= Cost of purchase- selling price

= 10120-6000= (4120)

In this case Helen is occurring capital loss of $4120 which she can settle from her capital

gains of current year or can carry forward to next assessment year.

3. CGT on jewellery purchased in 1987-

This antique jewellery piece was bought on October 1987 for $14000. Indexation method will

be applicable to calculate CGT by using CPI (Smith, 2015). Calculation is as follows-

Cost of purchase under indexation method= 112.6/47.6*14000=33117

Capital gain or loss= Cost of purchase- selling price

=33117-13000= (20117)

September 1985 exempted from capital gain tax. This law of discount and the rate of capital gain tax

both are not applicable on capital assets purchased before the aforesaid time period (ATO, 2016). In

the given question the antique impressionism painting was purchased by helon’s father in February

1985 which is exempted from capital gain tax. Therefore there will be no CGT applicable in this

transaction (Minas, Lim and Evans, 2018).

2. CGT on Historical sculpture-

In the given question sculpture was purchased on December 1993 for $5500 which is before

21st September 1999. It is sold on 1st January 2018 for $6000. Therefore it will be treated

under indexation method. For the calculation of CGT we first find out the purchasing cost as

per the current period by using Consumer price index (Barkoczy, S. 2016).

Cost of purchase under indexation method= CPI of 1993/ CPI of 2018*purchase price

= 112.6/61.2*5500

= 10120

Capital gain or loss= Cost of purchase- selling price

= 10120-6000= (4120)

In this case Helen is occurring capital loss of $4120 which she can settle from her capital

gains of current year or can carry forward to next assessment year.

3. CGT on jewellery purchased in 1987-

This antique jewellery piece was bought on October 1987 for $14000. Indexation method will

be applicable to calculate CGT by using CPI (Smith, 2015). Calculation is as follows-

Cost of purchase under indexation method= 112.6/47.6*14000=33117

Capital gain or loss= Cost of purchase- selling price

=33117-13000= (20117)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

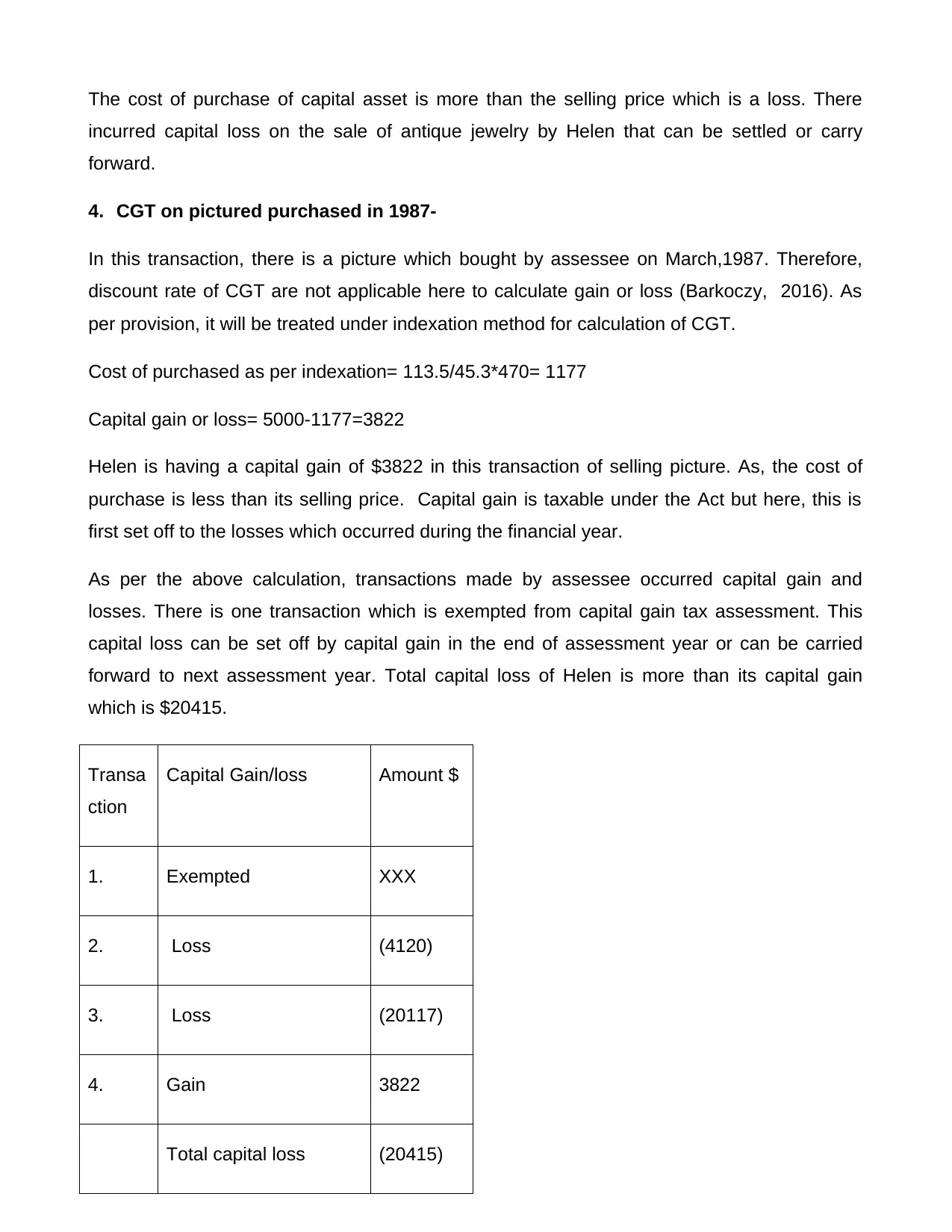

The cost of purchase of capital asset is more than the selling price which is a loss. There

incurred capital loss on the sale of antique jewelry by Helen that can be settled or carry

forward.

4. CGT on pictured purchased in 1987-

In this transaction, there is a picture which bought by assessee on March,1987. Therefore,

discount rate of CGT are not applicable here to calculate gain or loss (Barkoczy, 2016). As

per provision, it will be treated under indexation method for calculation of CGT.

Cost of purchased as per indexation= 113.5/45.3*470= 1177

Capital gain or loss= 5000-1177=3822

Helen is having a capital gain of $3822 in this transaction of selling picture. As, the cost of

purchase is less than its selling price. Capital gain is taxable under the Act but here, this is

first set off to the losses which occurred during the financial year.

As per the above calculation, transactions made by assessee occurred capital gain and

losses. There is one transaction which is exempted from capital gain tax assessment. This

capital loss can be set off by capital gain in the end of assessment year or can be carried

forward to next assessment year. Total capital loss of Helen is more than its capital gain

which is $20415.

Transa

ction

Capital Gain/loss Amount $

1. Exempted XXX

2. Loss (4120)

3. Loss (20117)

4. Gain 3822

Total capital loss (20415)

incurred capital loss on the sale of antique jewelry by Helen that can be settled or carry

forward.

4. CGT on pictured purchased in 1987-

In this transaction, there is a picture which bought by assessee on March,1987. Therefore,

discount rate of CGT are not applicable here to calculate gain or loss (Barkoczy, 2016). As

per provision, it will be treated under indexation method for calculation of CGT.

Cost of purchased as per indexation= 113.5/45.3*470= 1177

Capital gain or loss= 5000-1177=3822

Helen is having a capital gain of $3822 in this transaction of selling picture. As, the cost of

purchase is less than its selling price. Capital gain is taxable under the Act but here, this is

first set off to the losses which occurred during the financial year.

As per the above calculation, transactions made by assessee occurred capital gain and

losses. There is one transaction which is exempted from capital gain tax assessment. This

capital loss can be set off by capital gain in the end of assessment year or can be carried

forward to next assessment year. Total capital loss of Helen is more than its capital gain

which is $20415.

Transa

ction

Capital Gain/loss Amount $

1. Exempted XXX

2. Loss (4120)

3. Loss (20117)

4. Gain 3822

Total capital loss (20415)

So we can state that Helen is having a capital loss of $20415 after settling off her capital gain

which can be carrying forward in the next assessment year.

Question 2

Income Tax Assessment Act 1997 includes various laws and provisions which are used in

calculating and assessing different transactions (Barkoczy, 2016). These are defined various

types of incomes which are included in ordinary income. Ordinary income includes salary,

wages, income earned from business and disposes of property, getting any grant or subsidy.

Incomes from fees or commission are also included in ordinary income. Section 393(10) of

ITAA 1997 includes income from personal exertion having its provisions.

First situation

Barbara is a researcher of economics and has good skills that she got to offer by the Eco

Book Ltd to write a book (Filatova, 2014). She received a payment of $13400 for her skills of

writing and this is her income considered as income by personal exertion (Brabazon, 2019).

There are several cases which prove that income received as the result of the skills made by

the assessee to write a book or journal is not treated as capital income or gain. In the case of

“Brent v FCT (1971) 125 CLR 418” in which there is written the book “husband story of life”

the income earned was treated as income from personal exertion which proves that it is not

any kind of capital gain. Barbara is also having income by her skills which makes it income

from personal exertion and do not make it count in capital gain.

Barbara received her second payment of $4350 from the selling of the manuscript of her book

“Principles of Economics”. This payment was received by her because of her skills and talent

which makes it income by personal exertion and not to be treated as a capital gain (Burgess,

T.2013). The above case is also an example of this as in the writer has sold the life story of

her husband and income of her was not treated as a capital gain (Auerbach and Hassett,

2015).

which can be carrying forward in the next assessment year.

Question 2

Income Tax Assessment Act 1997 includes various laws and provisions which are used in

calculating and assessing different transactions (Barkoczy, 2016). These are defined various

types of incomes which are included in ordinary income. Ordinary income includes salary,

wages, income earned from business and disposes of property, getting any grant or subsidy.

Incomes from fees or commission are also included in ordinary income. Section 393(10) of

ITAA 1997 includes income from personal exertion having its provisions.

First situation

Barbara is a researcher of economics and has good skills that she got to offer by the Eco

Book Ltd to write a book (Filatova, 2014). She received a payment of $13400 for her skills of

writing and this is her income considered as income by personal exertion (Brabazon, 2019).

There are several cases which prove that income received as the result of the skills made by

the assessee to write a book or journal is not treated as capital income or gain. In the case of

“Brent v FCT (1971) 125 CLR 418” in which there is written the book “husband story of life”

the income earned was treated as income from personal exertion which proves that it is not

any kind of capital gain. Barbara is also having income by her skills which makes it income

from personal exertion and do not make it count in capital gain.

Barbara received her second payment of $4350 from the selling of the manuscript of her book

“Principles of Economics”. This payment was received by her because of her skills and talent

which makes it income by personal exertion and not to be treated as a capital gain (Burgess,

T.2013). The above case is also an example of this as in the writer has sold the life story of

her husband and income of her was not treated as a capital gain (Auerbach and Hassett,

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The third payment was received by Barbara of $3200 for collection of interview manuscript

meanwhile writing the book. This is fairly income from her skills and is also a part of her

writing work which makes it income from personal exertion.

Second Scenario

In the second situation where it is assumed that Barbara has written the book “Principle of

Economics” before signing the contract. In this case, there will be a no different way to assess

the income she earns (Braunerhjelm and Eklund, 2014). Her skills and talent are reasons

behind her income which makes it income from personal exertion. In case she chooses to self

publish her books and direct sale them in case she is getting income from royalties. But in this

case, there is no difference as she writes a book before or after signing the contract.

Question 3:

Impact of this assessment on Patrick’s income

Patrick has given $52000 to his son David for his newly started business without any written

agreement and agreed on a term to repay $58000 at ending of the fifth year. This will be

treated as a loan and not as a gift to son and will not be included in assessable income but

the in case of the return of money with the interest there is required some adjustments

(Weber, 2014). In the laws and regulations of Australian taxation authorities, there is a law

which makes the repayment of loans and advances from children to their parents make it

taxable from the hands of parents. This makes it taxable in the hands of Patrick at the year he

received the money.

In case David repays its debts at the end of the fifth year then the difference of $6000 (58000-

52000) will be added in the assessable income of Patrick. This money will not be treated as a

gift and will be shown (Edmonds, 2015). But in this case, David has made full payment at the

end of the second year with an interest of 5% of total money landed. He is now liable to pay

tax on the money he received in form of interest and it will be added in his assessable

income.

David paid $2400(6000/5*2) as interest with payment of money given by his father. In this

case, Patrick is liable to pay tax on this interest income. Payment has been made by cheque

which makes a different in the assessment of Patrick. This money from his son can be treated

meanwhile writing the book. This is fairly income from her skills and is also a part of her

writing work which makes it income from personal exertion.

Second Scenario

In the second situation where it is assumed that Barbara has written the book “Principle of

Economics” before signing the contract. In this case, there will be a no different way to assess

the income she earns (Braunerhjelm and Eklund, 2014). Her skills and talent are reasons

behind her income which makes it income from personal exertion. In case she chooses to self

publish her books and direct sale them in case she is getting income from royalties. But in this

case, there is no difference as she writes a book before or after signing the contract.

Question 3:

Impact of this assessment on Patrick’s income

Patrick has given $52000 to his son David for his newly started business without any written

agreement and agreed on a term to repay $58000 at ending of the fifth year. This will be

treated as a loan and not as a gift to son and will not be included in assessable income but

the in case of the return of money with the interest there is required some adjustments

(Weber, 2014). In the laws and regulations of Australian taxation authorities, there is a law

which makes the repayment of loans and advances from children to their parents make it

taxable from the hands of parents. This makes it taxable in the hands of Patrick at the year he

received the money.

In case David repays its debts at the end of the fifth year then the difference of $6000 (58000-

52000) will be added in the assessable income of Patrick. This money will not be treated as a

gift and will be shown (Edmonds, 2015). But in this case, David has made full payment at the

end of the second year with an interest of 5% of total money landed. He is now liable to pay

tax on the money he received in form of interest and it will be added in his assessable

income.

David paid $2400(6000/5*2) as interest with payment of money given by his father. In this

case, Patrick is liable to pay tax on this interest income. Payment has been made by cheque

which makes a different in the assessment of Patrick. This money from his son can be treated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as a gift or pension to his father because of no legal documentation of loan and can be

assessed as taxable income (Arnold, 2019). Payment by cheque will make this a one-sided

transaction and will now demand any proof of landing of money to David.

There are provided many rebates which can be used and one of them is from gift tax. $10000

per year or $30000 in five years whichever is less is provided by the tax authorities as a

rebate (Pellegrinoa, Perbolib and Squillerod, 2019). Patrick can avail that and amount more

than that would be assessable as his taxable income. So after analyzing the whole scenario,

we can state that the income will be included in the assessable income of patric and he can

avail rebates related to gift income.

Conclusion

In the present taxation scenario, there are various regulations which makes it possible to

understand different situations and ways to assess them. This report has provided a brief

knowledge of capital gain tax, income from exertion and other incomes and their ways to

assessment in Australia. The first question covers queries related to capital gain tax and ways

to calculate in different case scenario. Income from personal exertion is defined in the second

question and its assessment according to ITAA 1997. The third question covers the effect of

the different transaction on the assessment of personal income according to income tax

regularities of Australia. As we can conclude this report is brief knowledge of Australian tax

laws.

assessed as taxable income (Arnold, 2019). Payment by cheque will make this a one-sided

transaction and will now demand any proof of landing of money to David.

There are provided many rebates which can be used and one of them is from gift tax. $10000

per year or $30000 in five years whichever is less is provided by the tax authorities as a

rebate (Pellegrinoa, Perbolib and Squillerod, 2019). Patrick can avail that and amount more

than that would be assessable as his taxable income. So after analyzing the whole scenario,

we can state that the income will be included in the assessable income of patric and he can

avail rebates related to gift income.

Conclusion

In the present taxation scenario, there are various regulations which makes it possible to

understand different situations and ways to assess them. This report has provided a brief

knowledge of capital gain tax, income from exertion and other incomes and their ways to

assessment in Australia. The first question covers queries related to capital gain tax and ways

to calculate in different case scenario. Income from personal exertion is defined in the second

question and its assessment according to ITAA 1997. The third question covers the effect of

the different transaction on the assessment of personal income according to income tax

regularities of Australia. As we can conclude this report is brief knowledge of Australian tax

laws.

References

Arnold, B.J., 2019. International tax primer. Kluwer Law International BV.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42. Australia, 53(8), p.420.

Barkoczy, S. 2016. Foundation of Taxation Law. 8th ed. Melbourne: Oxford University Press.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design.Cambridge University Press.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl.

TaxF., 30, p.393

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of theory,

practice and perspectives for climate adaptation policy. Environmental science & policy, 37,

pp.227-242.

Martin, F., 2019. Unincorporated associations: Legal and tax consequences. Taxation in

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance: Revised

theory and test on the corporate law market. Academy of Management Journal, 59(1),

pp.330-351.

Arnold, B.J., 2019. International tax primer. Kluwer Law International BV.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42. Australia, 53(8), p.420.

Barkoczy, S. 2016. Foundation of Taxation Law. 8th ed. Melbourne: Oxford University Press.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design.Cambridge University Press.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl.

TaxF., 30, p.393

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of theory,

practice and perspectives for climate adaptation policy. Environmental science & policy, 37,

pp.227-242.

Martin, F., 2019. Unincorporated associations: Legal and tax consequences. Taxation in

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance: Revised

theory and test on the corporate law market. Academy of Management Journal, 59(1),

pp.330-351.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pellegrinoa, S., Perbolib, G. and Squillerod, G., 2019. Balancing the Equity-efficiency Trade-

off in Personal Income Taxation: An Evolutionary Approach.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Online

ATO Tax Calculator, 2016. [Online]. Available at: http://atotaxcalculator.com.au/.

Consumer price index, 2016 [Online]. Available at: <https://www.ato.gov.au/Rates/Consumer-

price-index/.

Income tax: residency status of individuals entering Australia, 2016. [Online] Available at:

http://law.ato.gov.au/atolaw/view.htm?Docid=TXR/TR9817/NAT/ATO/00001.

off in Personal Income Taxation: An Evolutionary Approach.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Online

ATO Tax Calculator, 2016. [Online]. Available at: http://atotaxcalculator.com.au/.

Consumer price index, 2016 [Online]. Available at: <https://www.ato.gov.au/Rates/Consumer-

price-index/.

Income tax: residency status of individuals entering Australia, 2016. [Online] Available at:

http://law.ato.gov.au/atolaw/view.htm?Docid=TXR/TR9817/NAT/ATO/00001.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.