Taxation and Law Assessment 2: Income, Deductions, Tax and Offsets

VerifiedAdded on 2023/06/14

|9

|1376

|75

Homework Assignment

AI Summary

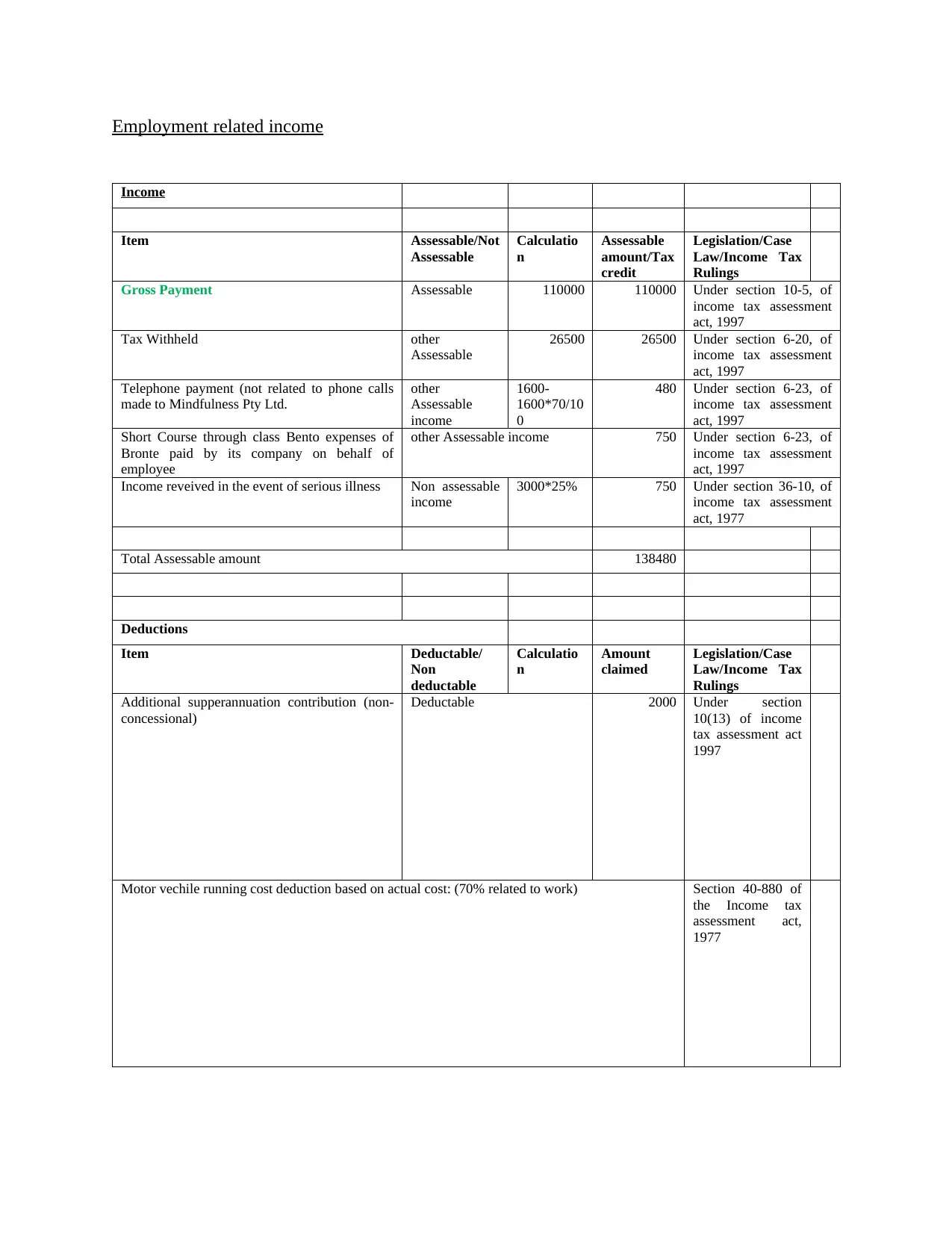

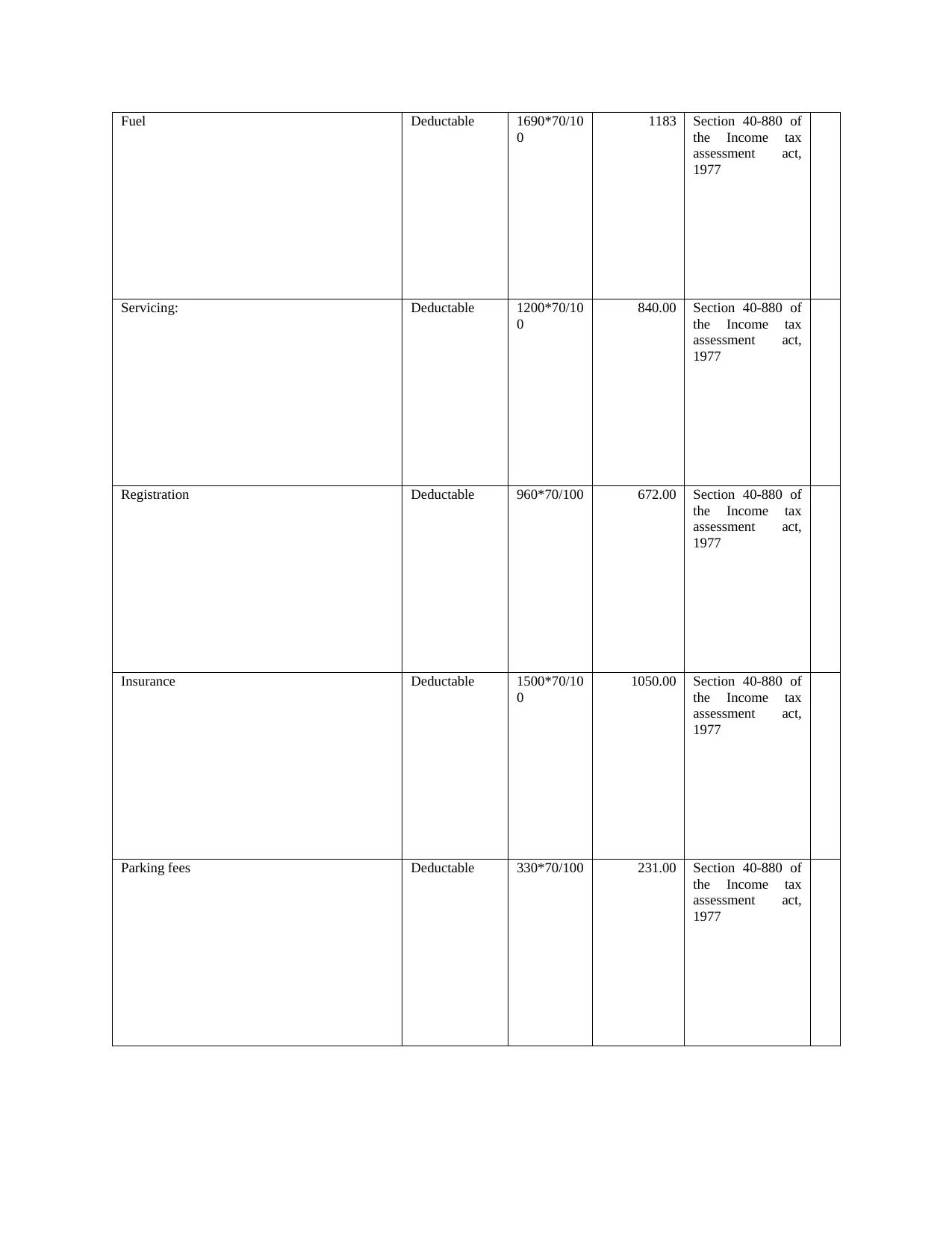

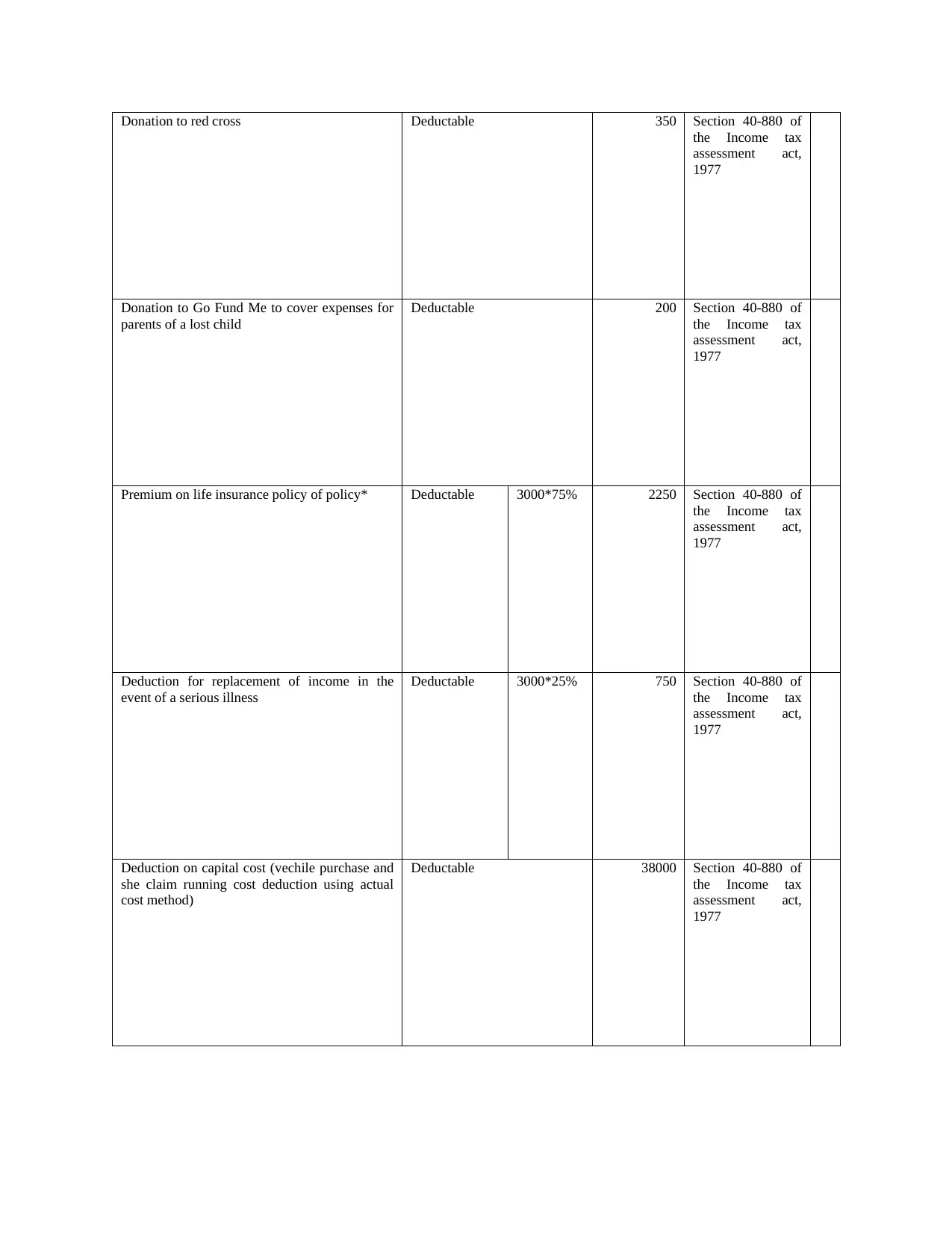

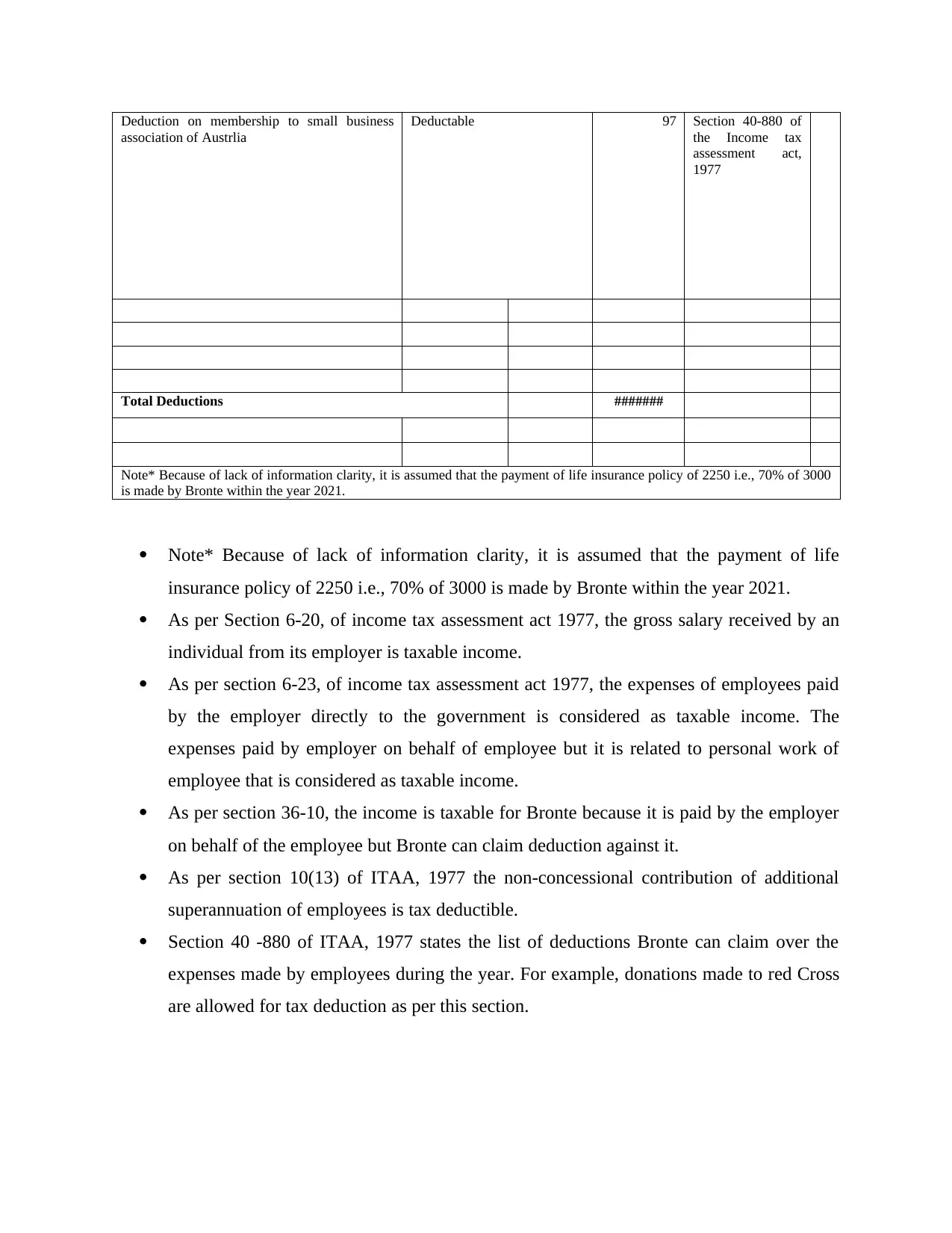

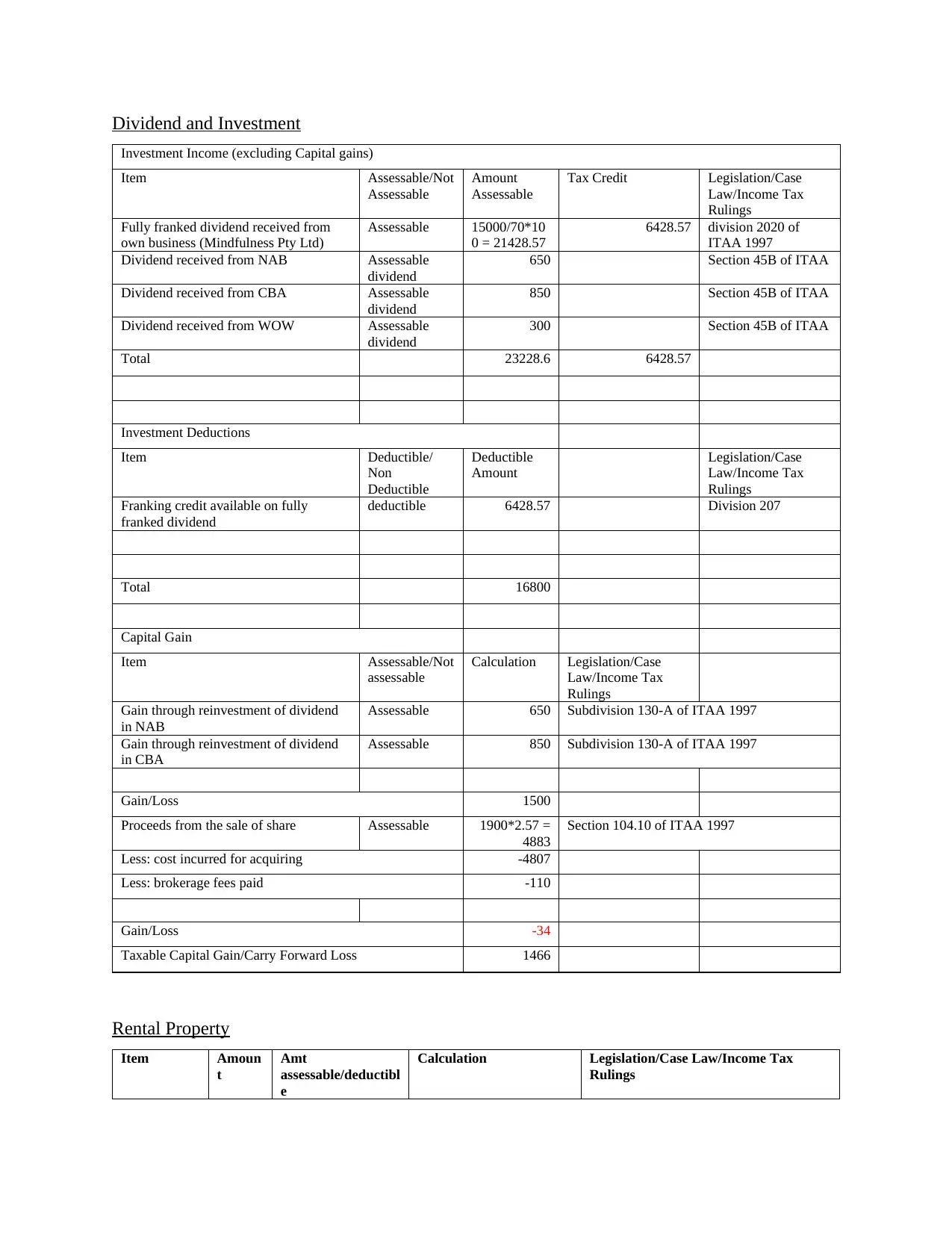

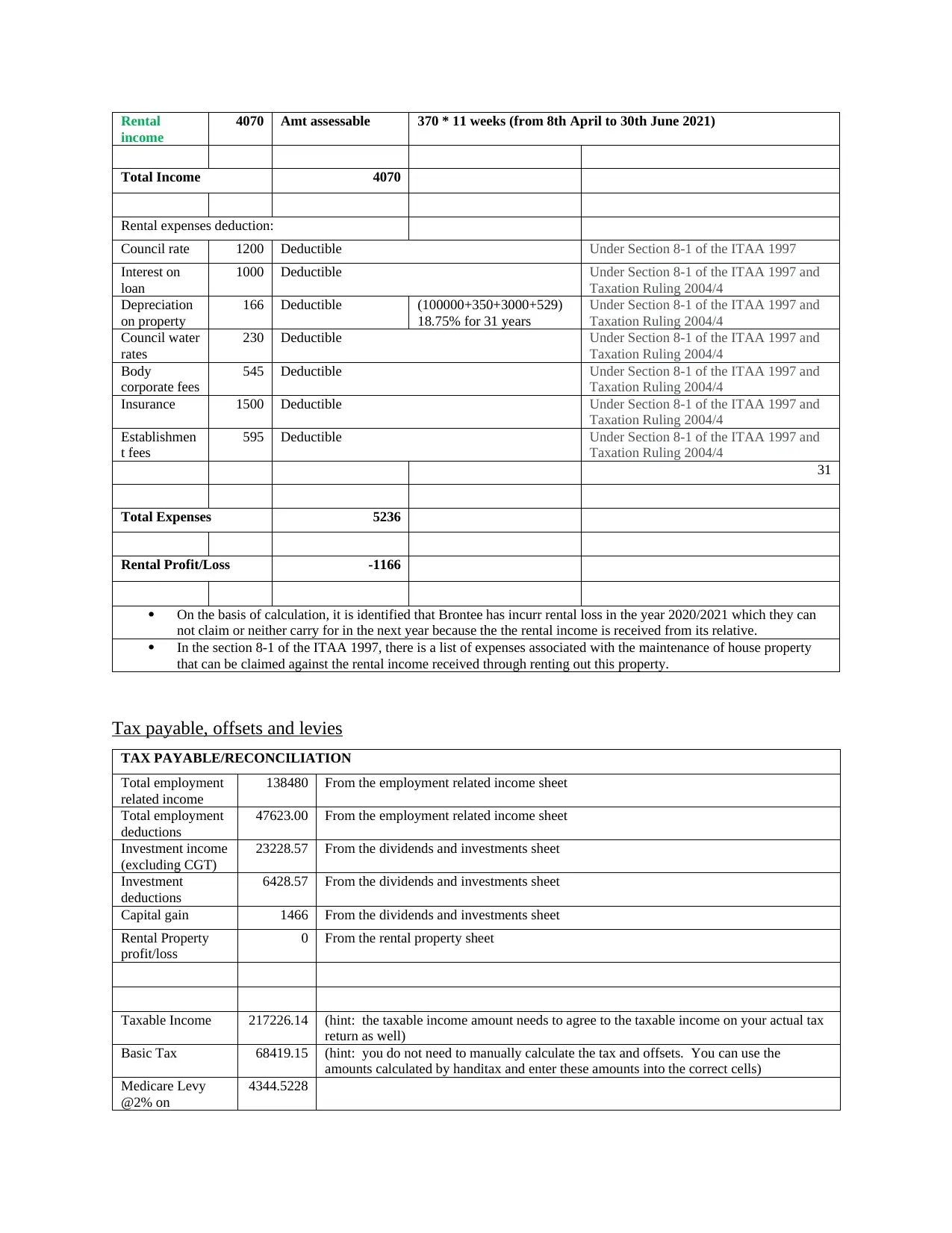

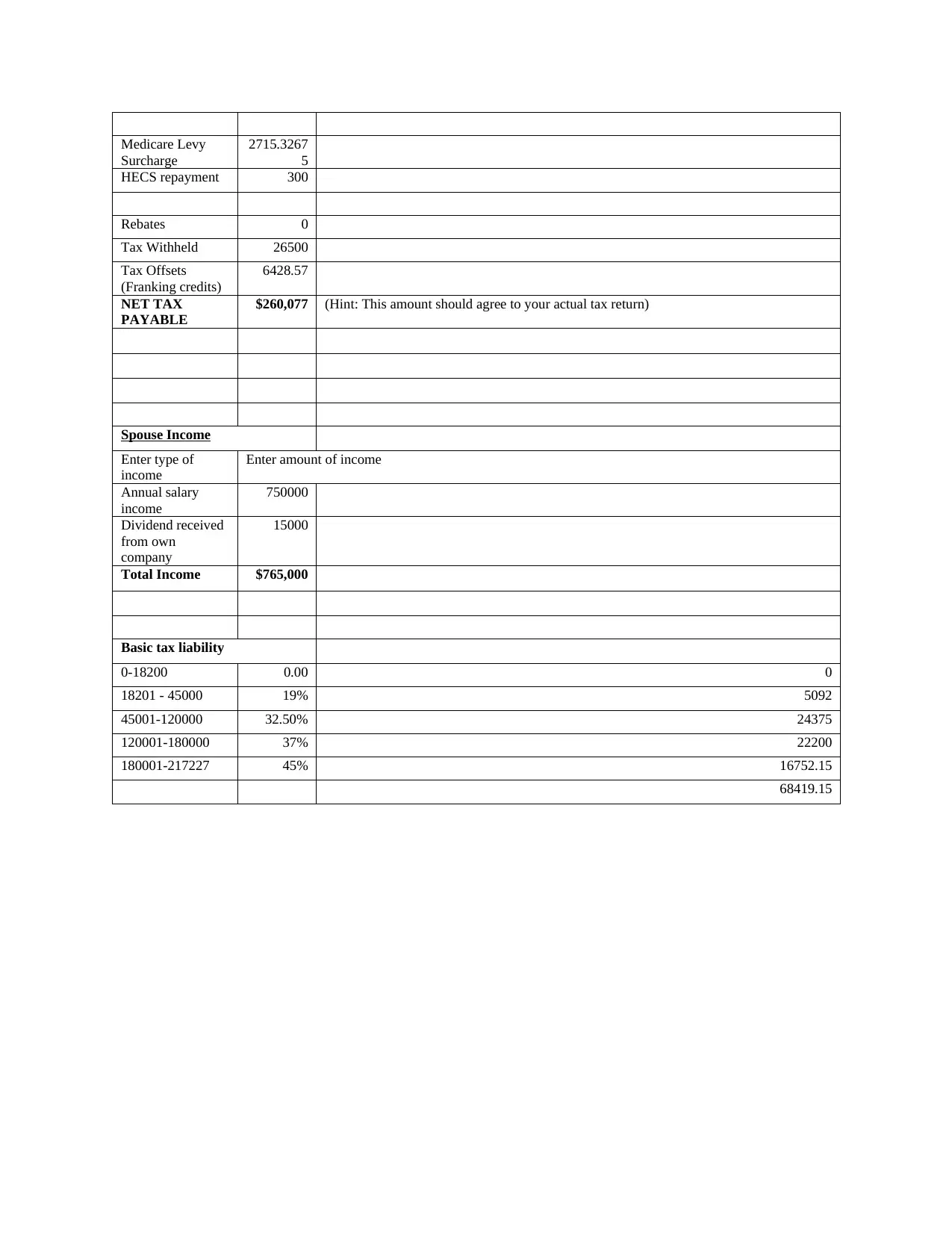

This document provides a detailed solution to a Taxation and Law assignment, focusing on the calculation of income tax, deductions, offsets, and levies. It covers various aspects of employment-related income, including assessable and non-assessable items, and deductible expenses such as superannuation contributions and motor vehicle costs. The solution also addresses dividend and investment income, including franking credits and capital gains, as well as rental property income and expenses. Relevant legislation and income tax rulings are cited throughout to support the calculations and explanations. The final section reconciles income, deductions, and offsets to determine the net tax payable, considering factors like Medicare Levy and HECS repayments. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.