Taxation Theory, Practice & Law: HI6028 Assignment Solution

VerifiedAdded on 2020/04/01

|10

|1937

|118

Homework Assignment

AI Summary

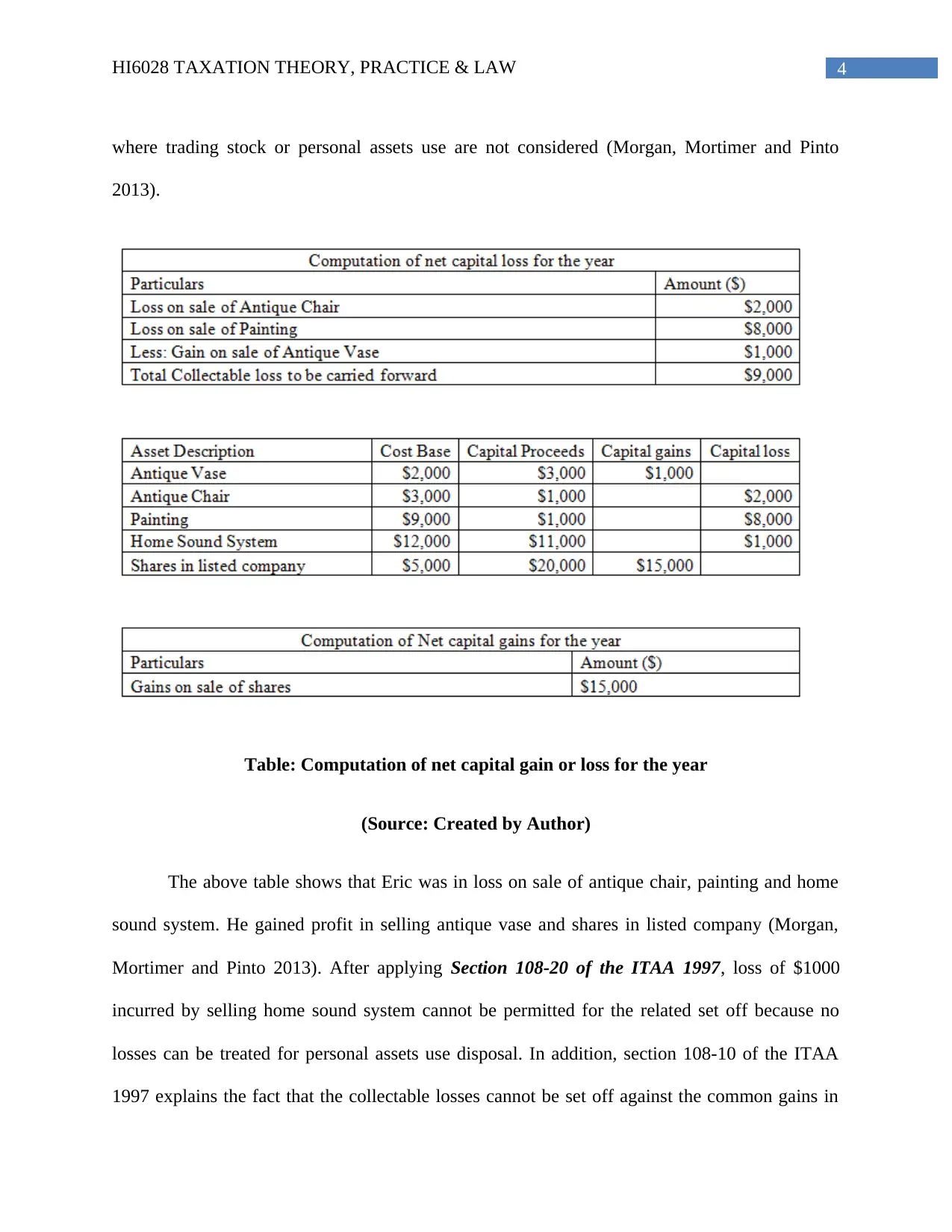

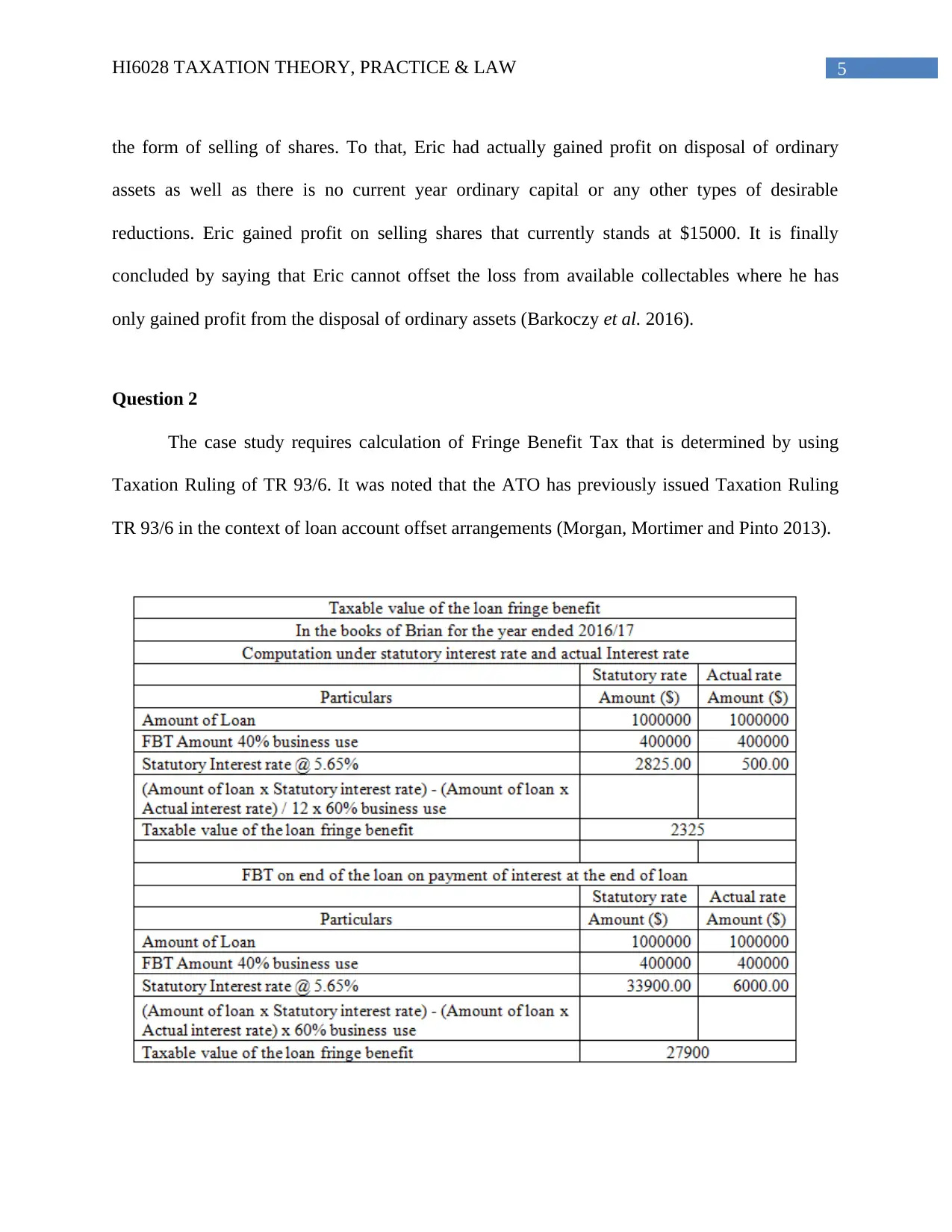

This assignment solution for HI6028 Taxation Theory, Practice & Law addresses five key questions related to tax assessment. The first question calculates net capital gains or losses from asset sales, referencing Section 108-20 and 108-10 of the ITAA 1997. The second question calculates Fringe Benefit Tax using Taxation Ruling TR 93/6. The third question analyzes the allocation of rental property losses between joint owners, Jack and Jill, referencing Section 51 of the ITAA 1997. The fourth question explores tax avoidance principles, citing IRC v Duke of Westminster (1936) Act AC 1. The fifth question assesses income from the sale of felled timber, referencing Subsection 6 (1) of the Income Tax Assessment 1936. The assignment provides detailed calculations, legal references, and conclusions for each scenario, offering a comprehensive understanding of Australian taxation law.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.