CSU Taxation Law: Income, Deductions, Fringe Benefits Assignment

VerifiedAdded on 2023/01/16

|13

|3165

|53

Homework Assignment

AI Summary

This taxation law assignment analyzes two key scenarios. The first assesses John's income from employment and the accounting firm's liability for fringe benefits tax, referencing relevant sections of the ITAA 1997 and FBTAA 1986, along with case law like Scott v FCT and Calvert v Wainwright. The second scenario examines Mechel Pty Ltd's deductions for cost of goods sold, exclusive distribution rights, and car lease expenses, applying section 8-1 and 40-880 of the ITAA 1997 and other relevant regulations. The assignment covers issues like assessable income, expense payment fringe benefits, business deductions, and capital gains tax, providing a detailed application of tax law principles to practical situations.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Rule:.......................................................................................................................................6

Application:............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Rule:.......................................................................................................................................6

Application:............................................................................................................................8

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

Is the taxpayer accountable for assessment under the “section 6-5, ITAA 1997” for

the income derived from the employment? Is the accounting firm liable for expense payment

fringe benefit tax under “section 20, FBTAA 1986”?

Rule:

As per “section 6 (1), ITAA 1936” income obtained from the private exertion or the

income obtained from the private exertion signifies earnings obtained from remunerations,

wages, fees, commissions, bonus received as employee or profits obtained from business

activities1. According to “section 6-5, ITAA 1997” usually most of the income made by the

taxpayer is treated as ordinary income. As stated under “Scott v FCT (1935)” income should

not be seen as term of art and receipts must be viewed as earnings in adherence with the

usage of mankind and ordinary concepts2.

Voluntary payments would be treated as earnings given that there is adequate nexus

with the revenue making activities of the taxpayer. Similarly, in “Calvert v Wainwright

(1947)” tips that are received by the taxi driver was considered as income because it was

from the revenue producing activities of the taxi-driver3. As a general rule, when a simple

winning from prizes is earned then it is not held as income. But may be held as income if

there are adequate nexus with income earning activities of taxpayers. In “Kelly v FCT

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in Scott v. Commissioner of Taxation, in

Elaborating the Meaning of Income for the Purposes of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

3 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Answer to question 1:

Issues:

Is the taxpayer accountable for assessment under the “section 6-5, ITAA 1997” for

the income derived from the employment? Is the accounting firm liable for expense payment

fringe benefit tax under “section 20, FBTAA 1986”?

Rule:

As per “section 6 (1), ITAA 1936” income obtained from the private exertion or the

income obtained from the private exertion signifies earnings obtained from remunerations,

wages, fees, commissions, bonus received as employee or profits obtained from business

activities1. According to “section 6-5, ITAA 1997” usually most of the income made by the

taxpayer is treated as ordinary income. As stated under “Scott v FCT (1935)” income should

not be seen as term of art and receipts must be viewed as earnings in adherence with the

usage of mankind and ordinary concepts2.

Voluntary payments would be treated as earnings given that there is adequate nexus

with the revenue making activities of the taxpayer. Similarly, in “Calvert v Wainwright

(1947)” tips that are received by the taxi driver was considered as income because it was

from the revenue producing activities of the taxi-driver3. As a general rule, when a simple

winning from prizes is earned then it is not held as income. But may be held as income if

there are adequate nexus with income earning activities of taxpayers. In “Kelly v FCT

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in Scott v. Commissioner of Taxation, in

Elaborating the Meaning of Income for the Purposes of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

3 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

(1985)” the monetary award received by footballer player for best player was treated as

income because it is related to employment by club and his use of skill.

A gain that are treated as the mere gift is not an income. As held in “Hayes v FCT

(1956)” shares received in the company by the previous boss was not the income4.

Accordingly, there must be an adequate relation amid the benefit derived and personal

exertion. Salary and wages are held as personal exertion income. As held in “Dean v FCT

(1997)” remuneration payment made to employees for being employed after the takeover was

treated as income.

The reconciliation rule under “section 6-25 (2)” explains that if the sum is both the

ordinary and statutory earnings then the rules relating to statutory income prevails apart from

any contrary intention is given5. Alternatively, if the employer gives any kind of fringe

benefit to the employee then the benefit would not be taxable for employee under “section

23L, ITAA 1936” but the employer would be liable for fringe benefit tax on the value of

benefit given.

According to “section 20, FBTAA 1986” the expense payment fringe benefit happens

when the employer makes the payment to the employee to discharge in parts or whole of the

obligations of another person to pay the sum to the third person in relation to the expenses

occurred by the employee or recipient6. The expense payment fringe benefit happens when

the employer reimburses the employee in relation to the expenses occurred.

4 Sadiq, Kerrie. Australian Tax Law Cases 2018. Thomson Reuters, 2018.

5 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford University Press,

2018.

6 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax Tchrs. Ass'n 13 (2018): 307.

(1985)” the monetary award received by footballer player for best player was treated as

income because it is related to employment by club and his use of skill.

A gain that are treated as the mere gift is not an income. As held in “Hayes v FCT

(1956)” shares received in the company by the previous boss was not the income4.

Accordingly, there must be an adequate relation amid the benefit derived and personal

exertion. Salary and wages are held as personal exertion income. As held in “Dean v FCT

(1997)” remuneration payment made to employees for being employed after the takeover was

treated as income.

The reconciliation rule under “section 6-25 (2)” explains that if the sum is both the

ordinary and statutory earnings then the rules relating to statutory income prevails apart from

any contrary intention is given5. Alternatively, if the employer gives any kind of fringe

benefit to the employee then the benefit would not be taxable for employee under “section

23L, ITAA 1936” but the employer would be liable for fringe benefit tax on the value of

benefit given.

According to “section 20, FBTAA 1986” the expense payment fringe benefit happens

when the employer makes the payment to the employee to discharge in parts or whole of the

obligations of another person to pay the sum to the third person in relation to the expenses

occurred by the employee or recipient6. The expense payment fringe benefit happens when

the employer reimburses the employee in relation to the expenses occurred.

4 Sadiq, Kerrie. Australian Tax Law Cases 2018. Thomson Reuters, 2018.

5 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford University Press,

2018.

6 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Application:

As evident John being the student at CSU worked at the local restaurant and was paid

$18.00 per hour for a five hour shift every week. Referring to “section 6 (1), ITAA 1936” the

wages earned by John from working as waiter at local restaurant amounts to income from

personal exertion. Citing “Scott v FCT (1935)” the wages received constitutes ordinary

income and would be assessable under “section 6-5, ITAA 1997”.

Later John received tips from diners that varied between $30-$50. Citing “Calvert v

Wainwright (1947)” tips that are received by the John was considered as assessable income

under “section 6-5, ITAA 1997” because it was from the revenue producing activities by

working as waiter. He also received award of $200 for being the employee of the month.

Denoting the decision made in “Kelly v FCT (1985)” the monetary award received by John

for best employee should be treated as assessable income under “section 6-5, ITAA 1997”

because it is related to employment with restaurant7. Finally, on leaving the restaurant the

employer gave John with a farewell gift of champagne bottle that valued $150. Citing

“Hayes v FCT (1956)” the champagne bottle constitutes a mere gift that does not possess the

character of income.

During February 2013, John joined the accounting firm with the yearly salary of

$60,000. He also received a singed on bonus of $2,000 upon joining the employment. Citing

the case of “Dean v FCT (1997)” the remuneration and signed on fees from employment

would be treated as assessable income under “section 6-5, ITAA 1997”8.

7 Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law 2016." Australian Year Book of International

Law 35 (2018): 353.

8 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Application:

As evident John being the student at CSU worked at the local restaurant and was paid

$18.00 per hour for a five hour shift every week. Referring to “section 6 (1), ITAA 1936” the

wages earned by John from working as waiter at local restaurant amounts to income from

personal exertion. Citing “Scott v FCT (1935)” the wages received constitutes ordinary

income and would be assessable under “section 6-5, ITAA 1997”.

Later John received tips from diners that varied between $30-$50. Citing “Calvert v

Wainwright (1947)” tips that are received by the John was considered as assessable income

under “section 6-5, ITAA 1997” because it was from the revenue producing activities by

working as waiter. He also received award of $200 for being the employee of the month.

Denoting the decision made in “Kelly v FCT (1985)” the monetary award received by John

for best employee should be treated as assessable income under “section 6-5, ITAA 1997”

because it is related to employment with restaurant7. Finally, on leaving the restaurant the

employer gave John with a farewell gift of champagne bottle that valued $150. Citing

“Hayes v FCT (1956)” the champagne bottle constitutes a mere gift that does not possess the

character of income.

During February 2013, John joined the accounting firm with the yearly salary of

$60,000. He also received a singed on bonus of $2,000 upon joining the employment. Citing

the case of “Dean v FCT (1997)” the remuneration and signed on fees from employment

would be treated as assessable income under “section 6-5, ITAA 1997”8.

7 Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law 2016." Australian Year Book of International

Law 35 (2018): 353.

8 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

5TAXATION LAW

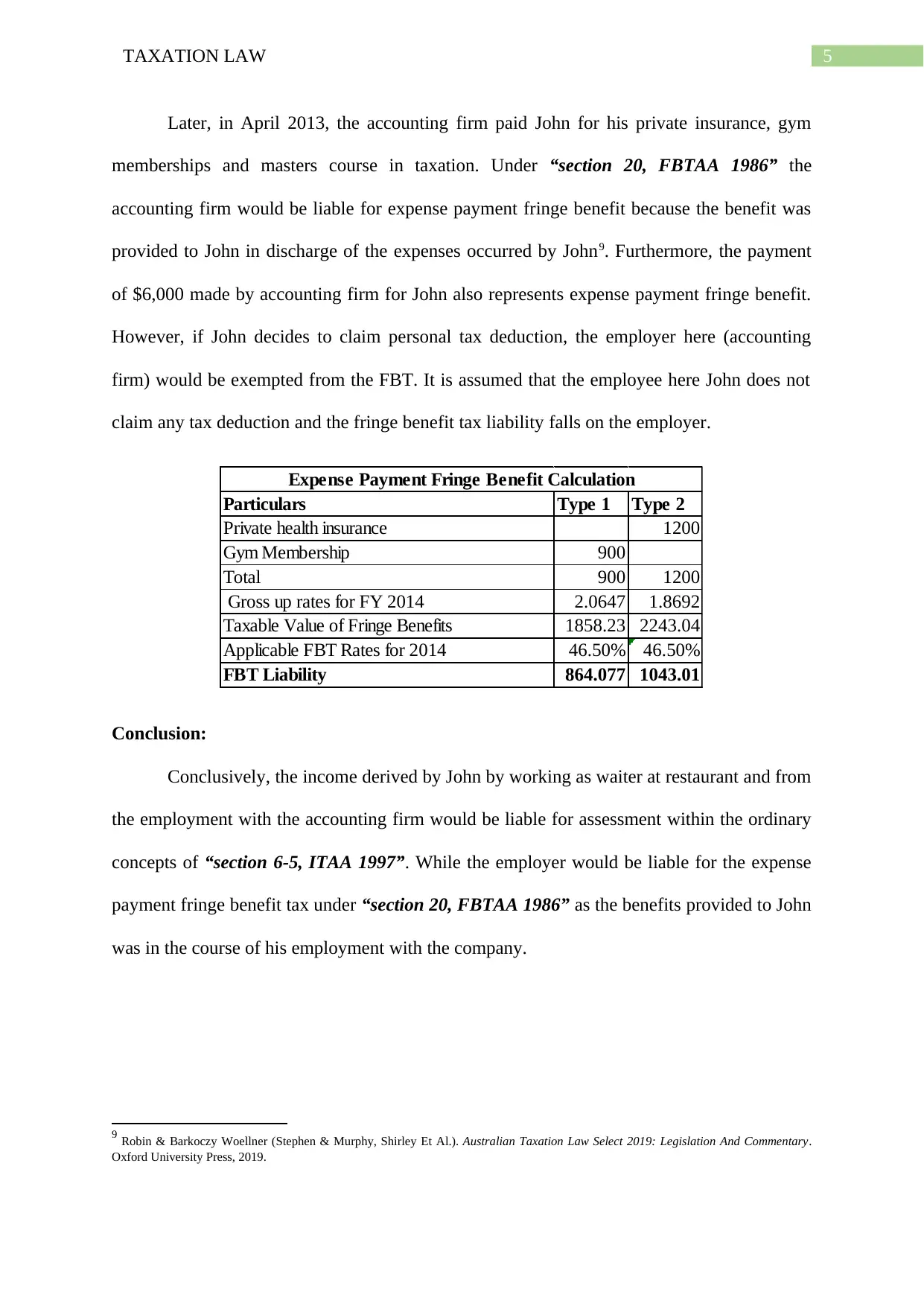

Later, in April 2013, the accounting firm paid John for his private insurance, gym

memberships and masters course in taxation. Under “section 20, FBTAA 1986” the

accounting firm would be liable for expense payment fringe benefit because the benefit was

provided to John in discharge of the expenses occurred by John9. Furthermore, the payment

of $6,000 made by accounting firm for John also represents expense payment fringe benefit.

However, if John decides to claim personal tax deduction, the employer here (accounting

firm) would be exempted from the FBT. It is assumed that the employee here John does not

claim any tax deduction and the fringe benefit tax liability falls on the employer.

Particulars Type 1 Type 2

Private health insurance 1200

Gym Membership 900

Total 900 1200

Gross up rates for FY 2014 2.0647 1.8692

Taxable Value of Fringe Benefits 1858.23 2243.04

Applicable FBT Rates for 2014 46.50% 46.50%

FBT Liability 864.077 1043.01

Expense Payment Fringe Benefit Calculation

Conclusion:

Conclusively, the income derived by John by working as waiter at restaurant and from

the employment with the accounting firm would be liable for assessment within the ordinary

concepts of “section 6-5, ITAA 1997”. While the employer would be liable for the expense

payment fringe benefit tax under “section 20, FBTAA 1986” as the benefits provided to John

was in the course of his employment with the company.

9 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law Select 2019: Legislation And Commentary.

Oxford University Press, 2019.

Later, in April 2013, the accounting firm paid John for his private insurance, gym

memberships and masters course in taxation. Under “section 20, FBTAA 1986” the

accounting firm would be liable for expense payment fringe benefit because the benefit was

provided to John in discharge of the expenses occurred by John9. Furthermore, the payment

of $6,000 made by accounting firm for John also represents expense payment fringe benefit.

However, if John decides to claim personal tax deduction, the employer here (accounting

firm) would be exempted from the FBT. It is assumed that the employee here John does not

claim any tax deduction and the fringe benefit tax liability falls on the employer.

Particulars Type 1 Type 2

Private health insurance 1200

Gym Membership 900

Total 900 1200

Gross up rates for FY 2014 2.0647 1.8692

Taxable Value of Fringe Benefits 1858.23 2243.04

Applicable FBT Rates for 2014 46.50% 46.50%

FBT Liability 864.077 1043.01

Expense Payment Fringe Benefit Calculation

Conclusion:

Conclusively, the income derived by John by working as waiter at restaurant and from

the employment with the accounting firm would be liable for assessment within the ordinary

concepts of “section 6-5, ITAA 1997”. While the employer would be liable for the expense

payment fringe benefit tax under “section 20, FBTAA 1986” as the benefits provided to John

was in the course of his employment with the company.

9 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law Select 2019: Legislation And Commentary.

Oxford University Press, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issues:

Are the taxpayers allowed to claim deduction relating to the expenses that are

occurred during the ordinary business course under legislative provision of “section 8-1,

ITAA 1997”?

Rule:

Business entities are allowed to claim deduction for bulk of the cost that is incurred in

running their business as this helps in reducing the overall taxable income10. Taxpayer’s may

be also eligible for certain kind of concessions, offsets and rebates that helps in lowering the

overall amount of tax payable. This includes the cost of sales that is incurred by the business.

As per the “section 40-880”, the taxpayers are allowed to claim deduction in the

equal shares over the period of five income years commencing from the year in which the

business incurs the capital expenditure11. The taxpayer should note that the capital

expenditure should be related to the business and should be in respect of the business that are

to be carried on.

As defined under the “section 8-1, ITAA 1997” a taxpayer is permitted to claim

deduction for majority of the expenditure that are occurred in running the business as long as

the expenditure are related directly to the income producing activities12. The taxpayers are

required to adhere with the golden rules for claiming the business expenditure. If any part of

the expenses is occurred for private purpose, then only business portion of the expenses are

10 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

12 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and Investment Planning 2016 Edition. McGraw-Hill

Education, 2015.

Answer to question 2:

Issues:

Are the taxpayers allowed to claim deduction relating to the expenses that are

occurred during the ordinary business course under legislative provision of “section 8-1,

ITAA 1997”?

Rule:

Business entities are allowed to claim deduction for bulk of the cost that is incurred in

running their business as this helps in reducing the overall taxable income10. Taxpayer’s may

be also eligible for certain kind of concessions, offsets and rebates that helps in lowering the

overall amount of tax payable. This includes the cost of sales that is incurred by the business.

As per the “section 40-880”, the taxpayers are allowed to claim deduction in the

equal shares over the period of five income years commencing from the year in which the

business incurs the capital expenditure11. The taxpayer should note that the capital

expenditure should be related to the business and should be in respect of the business that are

to be carried on.

As defined under the “section 8-1, ITAA 1997” a taxpayer is permitted to claim

deduction for majority of the expenditure that are occurred in running the business as long as

the expenditure are related directly to the income producing activities12. The taxpayers are

required to adhere with the golden rules for claiming the business expenditure. If any part of

the expenses is occurred for private purpose, then only business portion of the expenses are

10 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

12 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and Investment Planning 2016 Edition. McGraw-Hill

Education, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

allowed to claim deduction. As per the section 40-30 depreciating assets represents the assets

that has the effective life and it is reasonable anticipated to be decline in value over the time.

As defined under the “taxation ruling of 93/30” where the home office constitutes

the place of business a relevant portion of both types of expenditure would be considered tax

deductible. The taxpayers are usually permitted to claim deduction for the work related

portion of heating and electricity costs13. The taxpayers are usually permitted to depreciate

the cost of items namely the desks, bookshelves that are used for the purpose of work. As

held in “Swinford v FCT (1984)” the court allowed the taxpayer with the deduction for the

portion of rent paid for the flat where the taxpayer had dedicated a separate room for work

purpose.

According to the ATO a taxpayer may make the net capital gains or loss if they

business goodwill is disposed through sale or transfer. The capital gains tax is only payable

upon the increase in the value of the goodwill. As a small business, the taxpayer can obtain

the eligible capital gains tax concession on the assets that are used to perform the business.

The taxpayers should satisfy the eligibility conditions to access the concessions. This

includes the following;

a. 15 Year exemption

b. 50% active asset reduction

c. Retirement exemption

d. Rollover

The taxpayers are however required to denote that 50% Capital gains tax discount is

not applicable for the company.

13 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's guidance." Taxation in Australia52.11

(2018): 608.

allowed to claim deduction. As per the section 40-30 depreciating assets represents the assets

that has the effective life and it is reasonable anticipated to be decline in value over the time.

As defined under the “taxation ruling of 93/30” where the home office constitutes

the place of business a relevant portion of both types of expenditure would be considered tax

deductible. The taxpayers are usually permitted to claim deduction for the work related

portion of heating and electricity costs13. The taxpayers are usually permitted to depreciate

the cost of items namely the desks, bookshelves that are used for the purpose of work. As

held in “Swinford v FCT (1984)” the court allowed the taxpayer with the deduction for the

portion of rent paid for the flat where the taxpayer had dedicated a separate room for work

purpose.

According to the ATO a taxpayer may make the net capital gains or loss if they

business goodwill is disposed through sale or transfer. The capital gains tax is only payable

upon the increase in the value of the goodwill. As a small business, the taxpayer can obtain

the eligible capital gains tax concession on the assets that are used to perform the business.

The taxpayers should satisfy the eligibility conditions to access the concessions. This

includes the following;

a. 15 Year exemption

b. 50% active asset reduction

c. Retirement exemption

d. Rollover

The taxpayers are however required to denote that 50% Capital gains tax discount is

not applicable for the company.

13 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's guidance." Taxation in Australia52.11

(2018): 608.

8TAXATION LAW

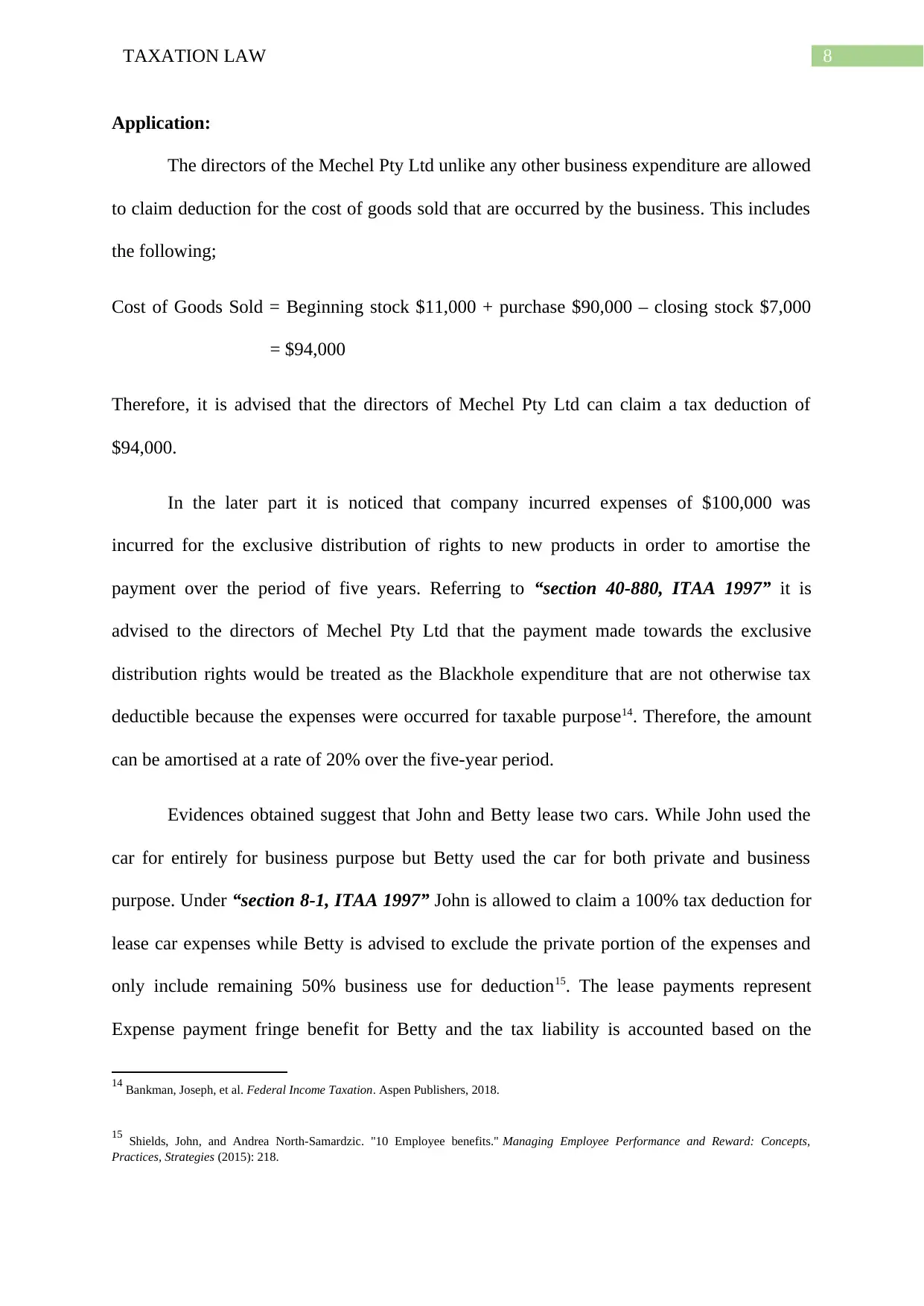

Application:

The directors of the Mechel Pty Ltd unlike any other business expenditure are allowed

to claim deduction for the cost of goods sold that are occurred by the business. This includes

the following;

Cost of Goods Sold = Beginning stock $11,000 + purchase $90,000 – closing stock $7,000

= $94,000

Therefore, it is advised that the directors of Mechel Pty Ltd can claim a tax deduction of

$94,000.

In the later part it is noticed that company incurred expenses of $100,000 was

incurred for the exclusive distribution of rights to new products in order to amortise the

payment over the period of five years. Referring to “section 40-880, ITAA 1997” it is

advised to the directors of Mechel Pty Ltd that the payment made towards the exclusive

distribution rights would be treated as the Blackhole expenditure that are not otherwise tax

deductible because the expenses were occurred for taxable purpose14. Therefore, the amount

can be amortised at a rate of 20% over the five-year period.

Evidences obtained suggest that John and Betty lease two cars. While John used the

car for entirely for business purpose but Betty used the car for both private and business

purpose. Under “section 8-1, ITAA 1997” John is allowed to claim a 100% tax deduction for

lease car expenses while Betty is advised to exclude the private portion of the expenses and

only include remaining 50% business use for deduction15. The lease payments represent

Expense payment fringe benefit for Betty and the tax liability is accounted based on the

14 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

15 Shields, John, and Andrea North-Samardzic. "10 Employee benefits." Managing Employee Performance and Reward: Concepts,

Practices, Strategies (2015): 218.

Application:

The directors of the Mechel Pty Ltd unlike any other business expenditure are allowed

to claim deduction for the cost of goods sold that are occurred by the business. This includes

the following;

Cost of Goods Sold = Beginning stock $11,000 + purchase $90,000 – closing stock $7,000

= $94,000

Therefore, it is advised that the directors of Mechel Pty Ltd can claim a tax deduction of

$94,000.

In the later part it is noticed that company incurred expenses of $100,000 was

incurred for the exclusive distribution of rights to new products in order to amortise the

payment over the period of five years. Referring to “section 40-880, ITAA 1997” it is

advised to the directors of Mechel Pty Ltd that the payment made towards the exclusive

distribution rights would be treated as the Blackhole expenditure that are not otherwise tax

deductible because the expenses were occurred for taxable purpose14. Therefore, the amount

can be amortised at a rate of 20% over the five-year period.

Evidences obtained suggest that John and Betty lease two cars. While John used the

car for entirely for business purpose but Betty used the car for both private and business

purpose. Under “section 8-1, ITAA 1997” John is allowed to claim a 100% tax deduction for

lease car expenses while Betty is advised to exclude the private portion of the expenses and

only include remaining 50% business use for deduction15. The lease payments represent

Expense payment fringe benefit for Betty and the tax liability is accounted based on the

14 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

15 Shields, John, and Andrea North-Samardzic. "10 Employee benefits." Managing Employee Performance and Reward: Concepts,

Practices, Strategies (2015): 218.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

chargeable value of the benefit provided. Later, the expenses related to construction of

storage facility was reported. Under section 40-30 the storage facility is entirely tax

deductible and the depreciation can be claimed over the years.

The home office expenses include the administrative expenses occurred by the

taxpayer for business purpose. Citing “Swinford v FCT (1984)” the directors can claim a

1/7th portion of the council rates, electricity charges and telephone purpose16. While the

remaining 6/7th portion of the council rates is paid by the company. Therefore, the expenses

may be treated as the fringe benefit and would be subjected to Fringe benefit tax. However,

for the telephone charges the claims can be limited to business portion only depending upon

the actual business calls made during the period.

Later, it was noticed Oz-Mart Ltd made the offer of purchasing the business. An advice

can be made to the directors of Mechel Pty Ltd by stating that capital gains would be payable

by the directors upon the increase in value of business goodwill. Nevertheless, the directors

of Mechel Pty Ltd can obtain the small business CGT concessions to lower or disregard the

capital gains tax given the business meets the following conditions

a. 15 Year exemption

b. 50% active asset reduction

c. Retirement exemption

d. Rollover

It is advised that the directors can obtain reduction of capital gains tax under this regime.

16 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation. Wolters Kluwer Law & Business, 2015.

chargeable value of the benefit provided. Later, the expenses related to construction of

storage facility was reported. Under section 40-30 the storage facility is entirely tax

deductible and the depreciation can be claimed over the years.

The home office expenses include the administrative expenses occurred by the

taxpayer for business purpose. Citing “Swinford v FCT (1984)” the directors can claim a

1/7th portion of the council rates, electricity charges and telephone purpose16. While the

remaining 6/7th portion of the council rates is paid by the company. Therefore, the expenses

may be treated as the fringe benefit and would be subjected to Fringe benefit tax. However,

for the telephone charges the claims can be limited to business portion only depending upon

the actual business calls made during the period.

Later, it was noticed Oz-Mart Ltd made the offer of purchasing the business. An advice

can be made to the directors of Mechel Pty Ltd by stating that capital gains would be payable

by the directors upon the increase in value of business goodwill. Nevertheless, the directors

of Mechel Pty Ltd can obtain the small business CGT concessions to lower or disregard the

capital gains tax given the business meets the following conditions

a. 15 Year exemption

b. 50% active asset reduction

c. Retirement exemption

d. Rollover

It is advised that the directors can obtain reduction of capital gains tax under this regime.

16 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation. Wolters Kluwer Law & Business, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Conclusion:

On a conclusive note the directors can claim deduction for the cost of goods sold,

home office expenses and blackhole expenses. Furthermore, if the directors accept the offer

of selling the business then they can obtain the small business CGT concession.

Conclusion:

On a conclusive note the directors can claim deduction for the cost of goods sold,

home office expenses and blackhole expenses. Furthermore, if the directors accept the offer

of selling the business then they can obtain the small business CGT concession.

11TAXATION LAW

References:

Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education, 2015.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Kerrie. Australian Tax Law Cases 2018. Thomson Reuters, 2018.

References:

Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education, 2015.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Kerrie. Australian Tax Law Cases 2018. Thomson Reuters, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.