Taxation Law Assignment

VerifiedAdded on 2019/11/12

|12

|1786

|370

Homework Assignment

AI Summary

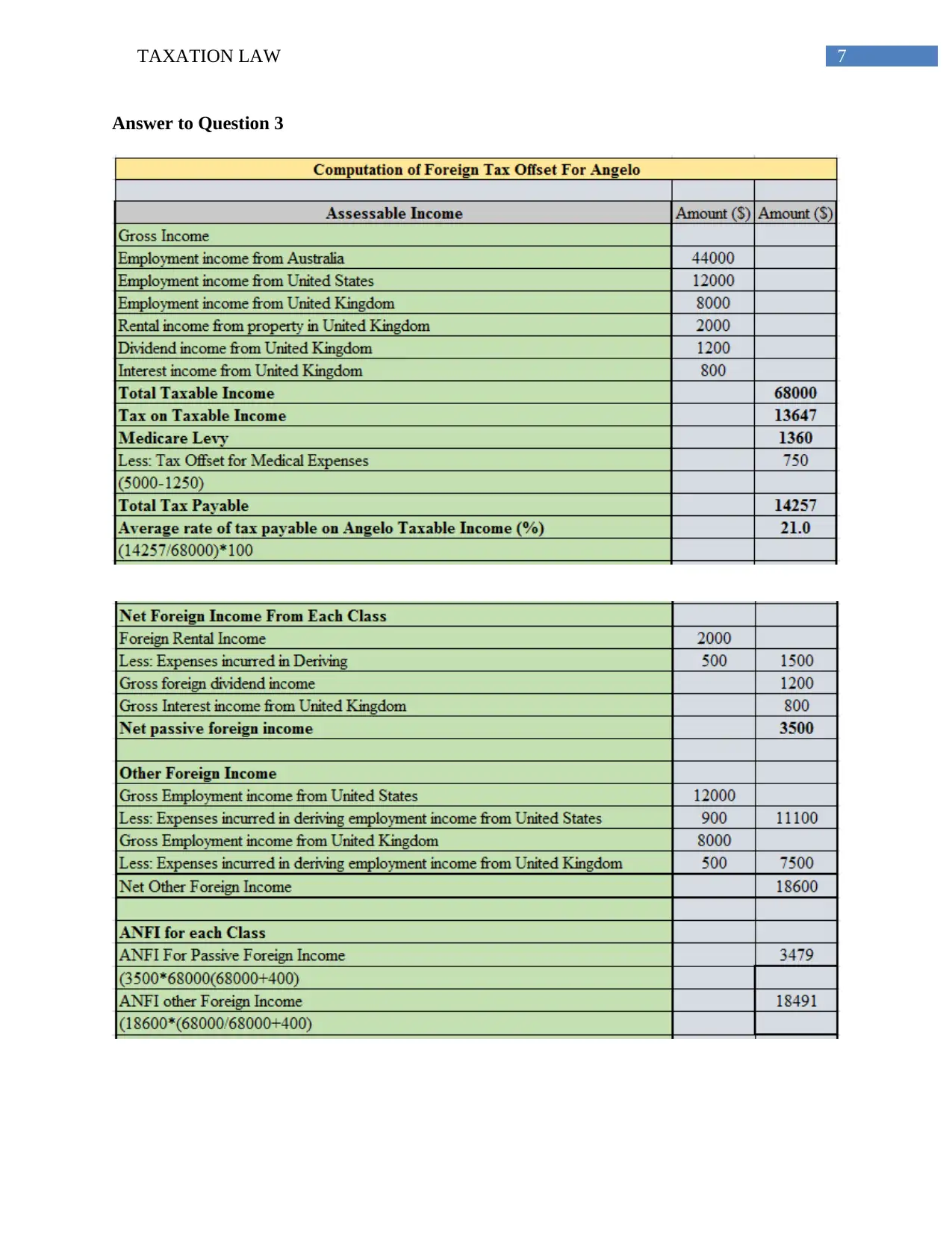

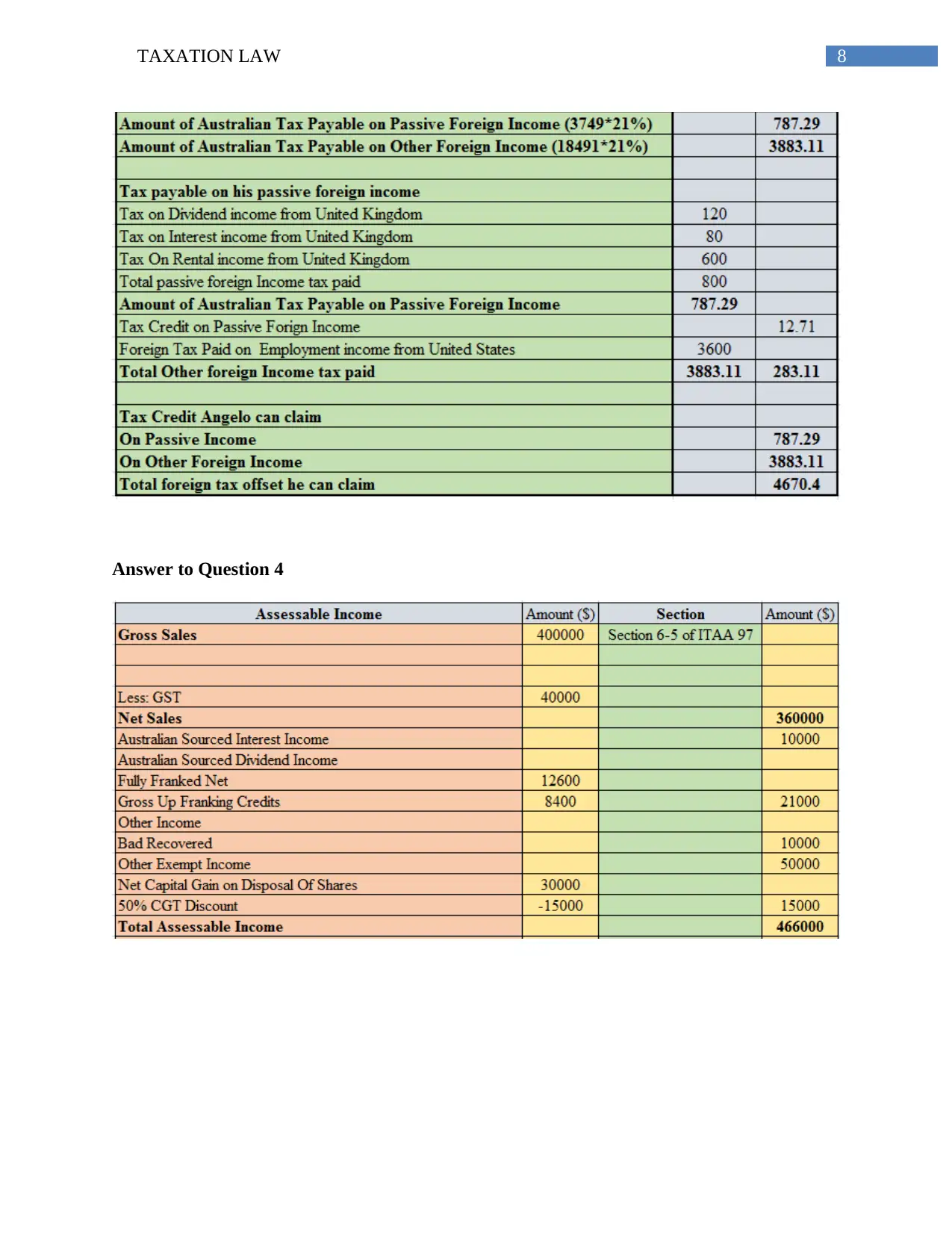

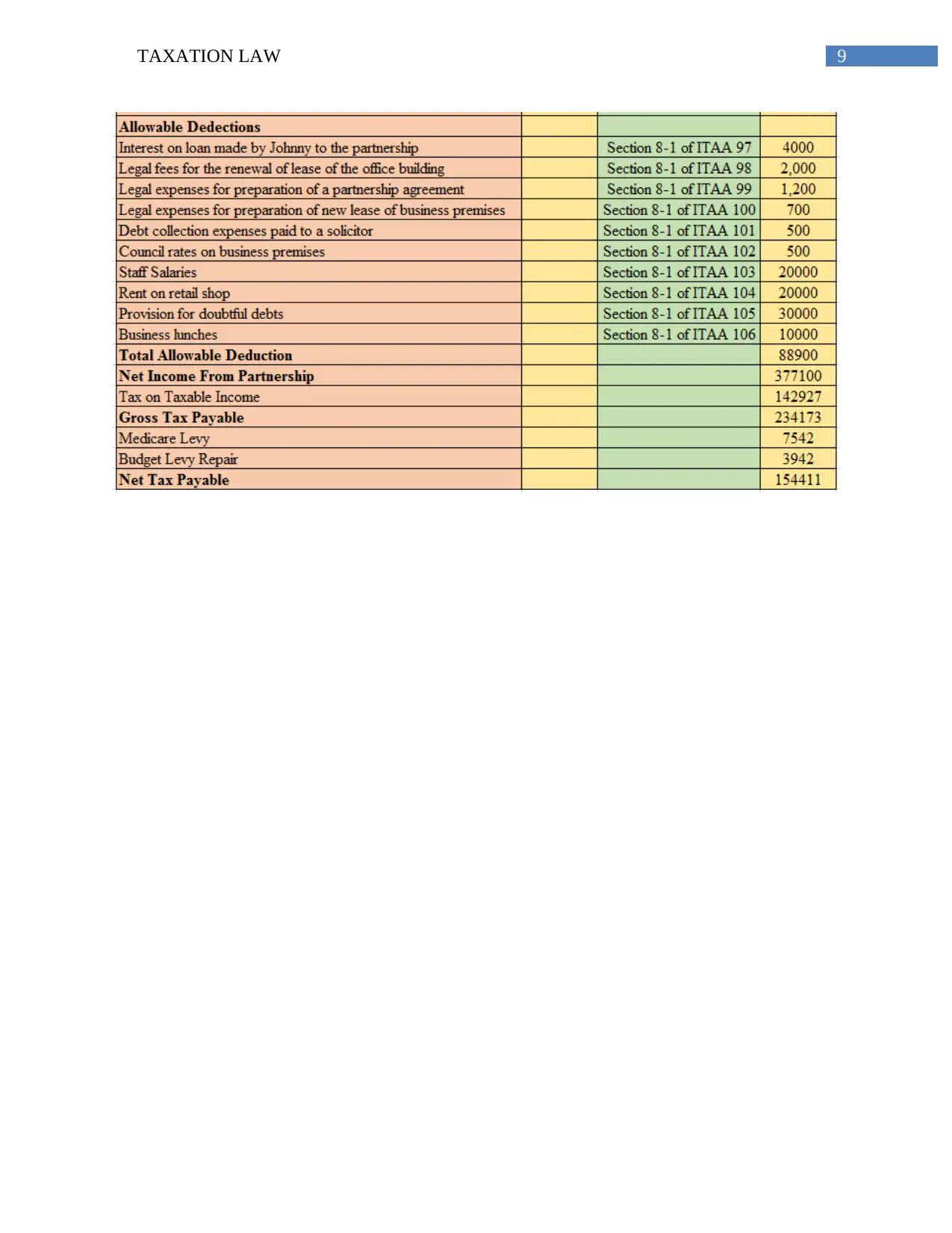

This assignment addresses several questions related to Australian taxation law, specifically focusing on allowable deductions under Section 8-1 of the ITAA 1997 and input tax credit under the GSTR Act 1999. The first question involves analyzing various expenditure scenarios to determine their deductibility, considering relevant legislation, case law (e.g., British Insulated & Helsby Cables, FC of T v Snowden and Wilson Pty Ltd), and taxation rulings. The second question focuses on determining the input tax credit eligibility for Big Bank Limited concerning advertisement expenses, referencing paragraphs 11-5, 15-5, subsection 15-25 of the GST Act 1999, GSTR 2006/3, and the case of Ronpibon Tin NL v. FC of T. The remaining questions (3 and 4) are not fully answered in the provided content. The assignment demonstrates a comprehensive understanding of relevant legislation and case law in applying taxation principles to real-world scenarios. The website offers this solved assignment as a resource for students.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.