TLAW 303: Taxation Law Assignment - Income Tax Calculations, 2018

VerifiedAdded on 2023/06/03

|7

|1478

|85

Homework Assignment

AI Summary

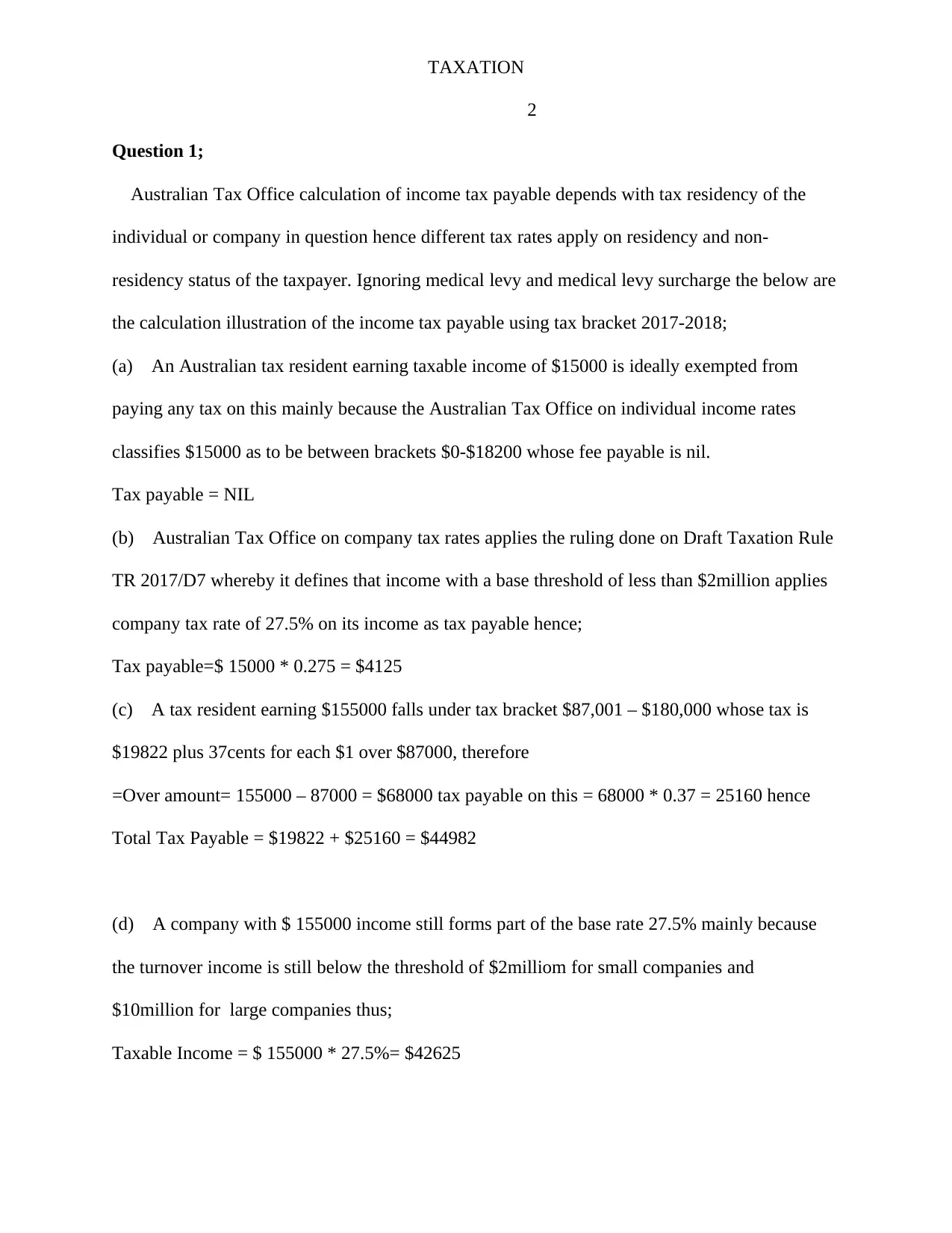

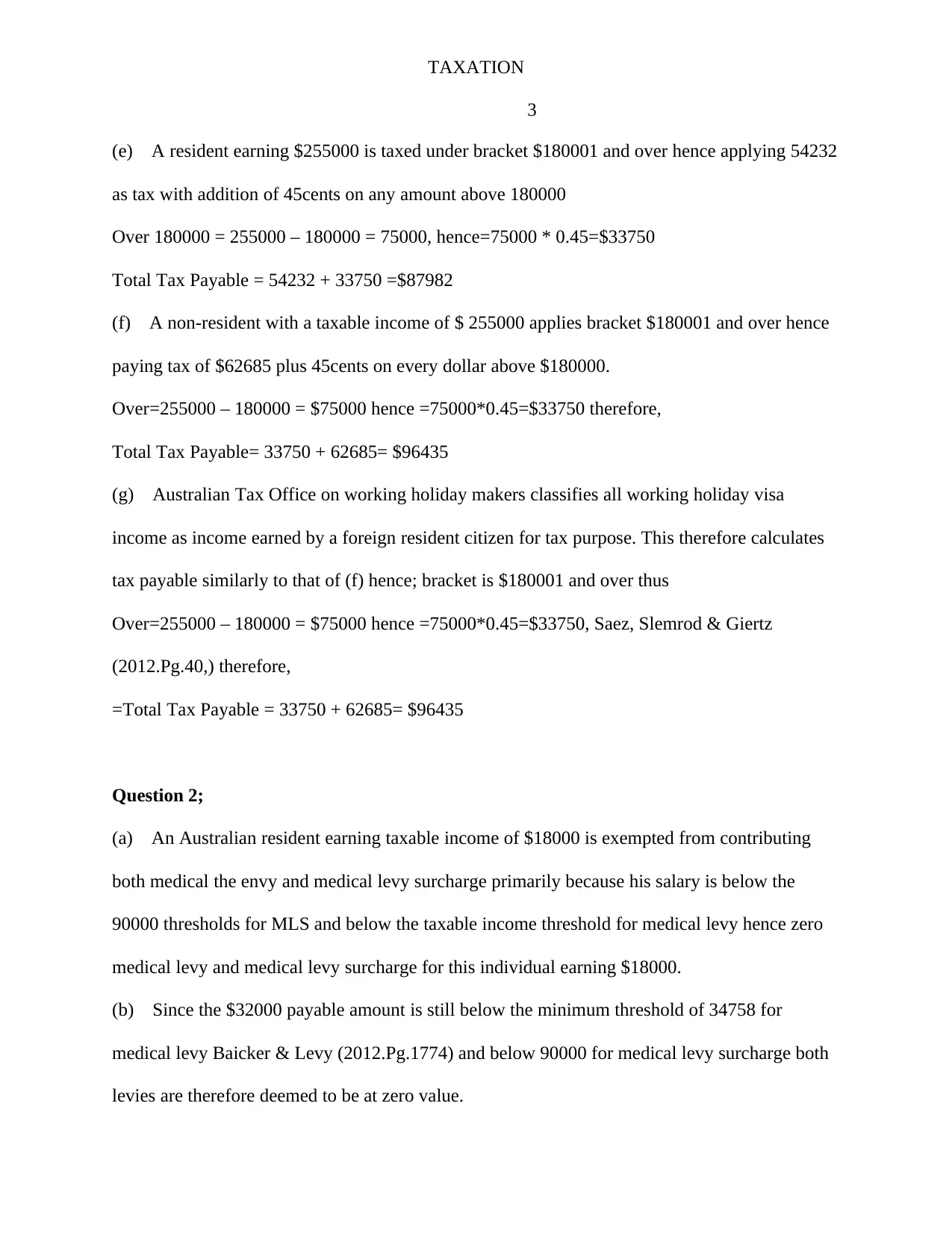

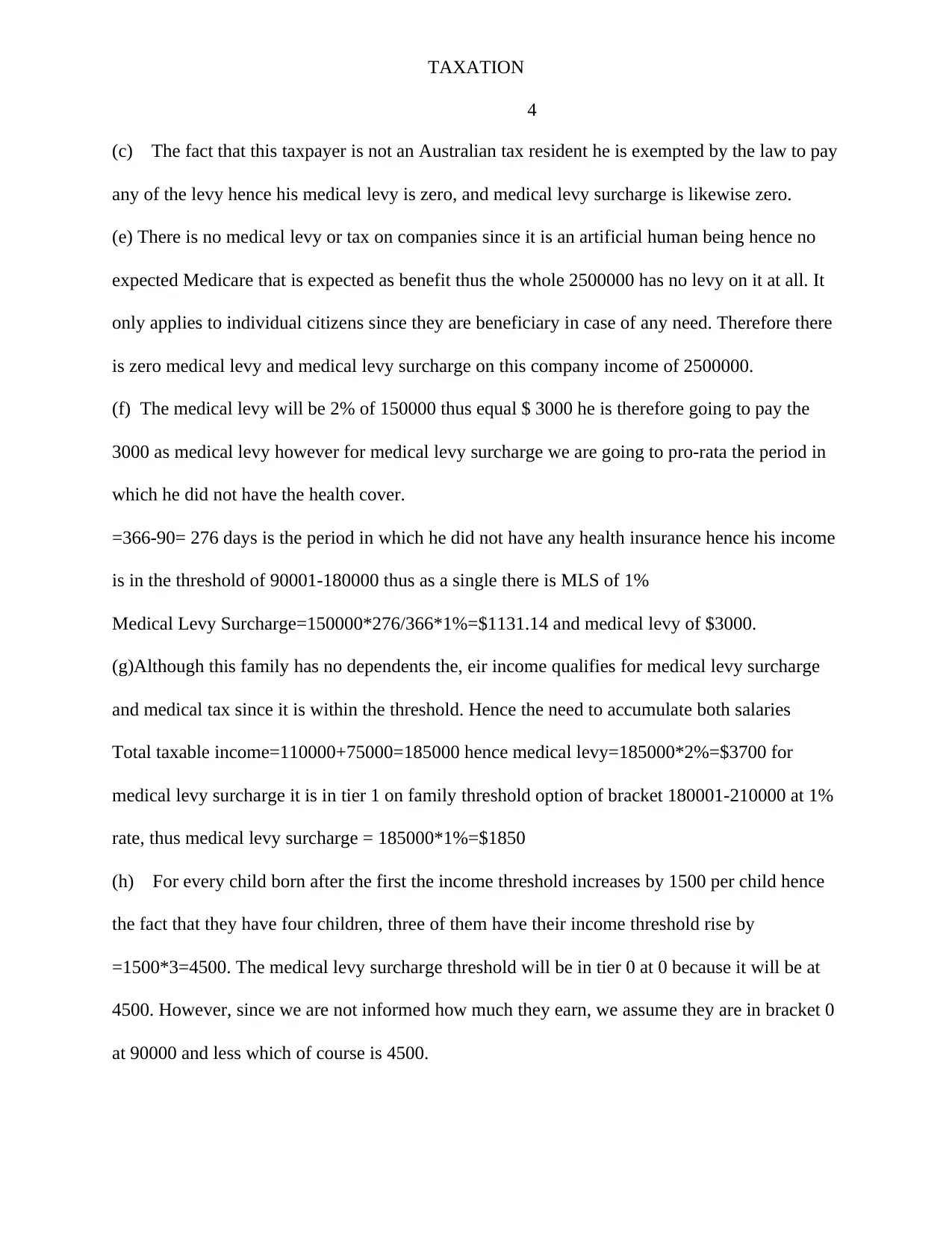

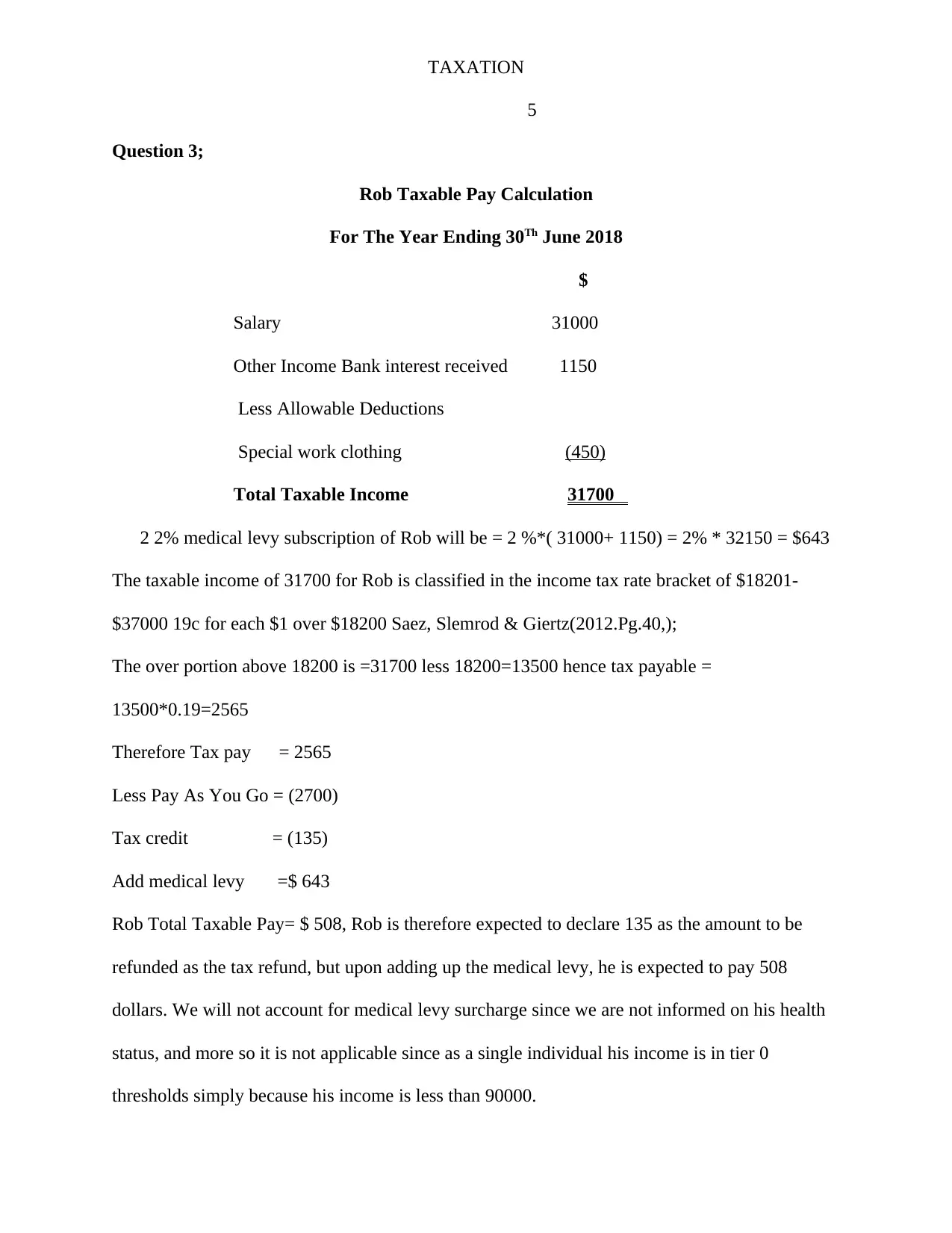

This assignment solution addresses four income tax calculation questions based on Australian taxation law for the year ending June 30, 2018. Question 1 calculates income tax payable for various scenarios, including residents, non-residents, and companies with different taxable incomes, ignoring the Medicare levy. Question 2 focuses on the calculation of Medicare levy and Medicare levy surcharge for different taxpayers, considering income thresholds and residency status. Question 3 calculates Rob's taxable pay, income tax, and medical levy, determining his tax refund or payment. Question 4 calculates imputation credit, tax burden on dividends, and total tax payable for an individual receiving dividends and salary, also considering the medical levy. The solution provides detailed calculations and references relevant legislative provisions to determine tax liabilities.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.