Taxation Law Assignment: Partnership, Fringe Benefits, and Tax

VerifiedAdded on 2023/04/24

|12

|2661

|103

Homework Assignment

AI Summary

This taxation law assignment addresses two key questions. The first question involves determining the net income of a partnership, analyzing business transactions, allowable deductions (such as car expenses, electricity bills, and repairs), and disallowed expenses (like private consumption drawings), with detailed calculations of receipts, expenses, and net income. The second question focuses on fringe benefits tax (FBT), specifically expense payment and housing fringe benefits, explaining relevant legislation (FBTA Act 1986) and applying it to scenarios involving payments for an employee's child's school fees and the provision of accommodation. The solution includes computations for the taxable value of the fringe benefits.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1

Issues:

The issues involves establishing the net income of the partnerships under “division 5

of the Partnership Act 1936”.

Rule:

Denoting the explanation made in “division 5 of ITAA 1936” a partnership is not held

as the distinct entity under the general law and the partnership does not pays tax. Instead it is

the partners that pays tax on the distributed profits from the partnership (Lee 2015). The net

income of the partnership is determined under “section 90” as if the partners are Australian

resident. The definition of partnership refers to the carrying on the business as partners that is

in receipt of the ordinary income or statutory income together under “section 995-1 (1),

ITAA 1997”.

Importantly under “section 6-5, ITAA 1997” a receipt is not treated as the ordinary

income until and unless it meets certain perquisites (Mumford 2017). This includes that the

receipts should be cash or convertible into cash and it should be real gain to the taxpayer.

“Section 6-5 of ITAA 1997” defines ordinary income as the income in respect of the ordinary

concepts. As held in “Scott v CT (1935)” ordinary income is interpreted in accordance with

the ordinary concepts.

As a general rule “section 8-1” possess the potential of being implemented to any

taxpayer (Borden 2015). Under “section 8-1”, a loss or the expenses may be allowed for

income tax deduction if the outgoings are incurred in producing the taxable income or it is

necessarily occurred while carrying on the business for obtaining or producing the taxable

income. The court in “Amalgamated Zinc Ltd v FCT (1935)” held that the gaining or

Answer to question 1

Issues:

The issues involves establishing the net income of the partnerships under “division 5

of the Partnership Act 1936”.

Rule:

Denoting the explanation made in “division 5 of ITAA 1936” a partnership is not held

as the distinct entity under the general law and the partnership does not pays tax. Instead it is

the partners that pays tax on the distributed profits from the partnership (Lee 2015). The net

income of the partnership is determined under “section 90” as if the partners are Australian

resident. The definition of partnership refers to the carrying on the business as partners that is

in receipt of the ordinary income or statutory income together under “section 995-1 (1),

ITAA 1997”.

Importantly under “section 6-5, ITAA 1997” a receipt is not treated as the ordinary

income until and unless it meets certain perquisites (Mumford 2017). This includes that the

receipts should be cash or convertible into cash and it should be real gain to the taxpayer.

“Section 6-5 of ITAA 1997” defines ordinary income as the income in respect of the ordinary

concepts. As held in “Scott v CT (1935)” ordinary income is interpreted in accordance with

the ordinary concepts.

As a general rule “section 8-1” possess the potential of being implemented to any

taxpayer (Borden 2015). Under “section 8-1”, a loss or the expenses may be allowed for

income tax deduction if the outgoings are incurred in producing the taxable income or it is

necessarily occurred while carrying on the business for obtaining or producing the taxable

income. The court in “Amalgamated Zinc Ltd v FCT (1935)” held that the gaining or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

generating assessable income must be interpreted in the due course of producing the taxable

income (Mellon 2016).

While an expenses or losses is not allowed for deduction under the general deduction

rule given the expenses meets the negative limbs of “section 8-1 (2)”. This includes the

expenses that are capital or private or domestic in nature (McNulty and McCouch 2015).

“Subsection 25-10” allows a deduction for outgoings incurred for repairs on the

premises or the depreciating assets that is used for generating taxable income (Picciotto

2015). As per “section 25-10” certain forms of repairs are considered as repairs such as

painting the plant or the business premises to resolve the current corrosion and also to prevent

the premises from deteriorating further.

Costs incurred on replacing the items of permanent fixtures that is installed on the

premises for producing income is held as deductible repairs under “section 25-10”. However,

the replacement should be of worn out unit by the new unit of identical design for restoring

the efficiency function and should not involve improvement (Sikka 2017). Finally, ATO

states that a taxpayer is allowed to claim deduction for the cost of business assets installed on

the premises that is below $20000. An immediate deduction is permitted to taxpayer under

this circumstances.

Applications:

The mixed business carried on by Daniel and Olivia is termed as partnership under

“division 5 of ITAA 1936”. In other words, Daniel and Olivia are carrying on the business as

partners that is in receipt of the ordinary income or statutory income together under “section

995-1 (1), ITAA 1997”.

For the duration of partnership their business transactions included the cash receipts

from sale and debtors payments. Referring to “Scott v CT (1935)” these receipts are treated

generating assessable income must be interpreted in the due course of producing the taxable

income (Mellon 2016).

While an expenses or losses is not allowed for deduction under the general deduction

rule given the expenses meets the negative limbs of “section 8-1 (2)”. This includes the

expenses that are capital or private or domestic in nature (McNulty and McCouch 2015).

“Subsection 25-10” allows a deduction for outgoings incurred for repairs on the

premises or the depreciating assets that is used for generating taxable income (Picciotto

2015). As per “section 25-10” certain forms of repairs are considered as repairs such as

painting the plant or the business premises to resolve the current corrosion and also to prevent

the premises from deteriorating further.

Costs incurred on replacing the items of permanent fixtures that is installed on the

premises for producing income is held as deductible repairs under “section 25-10”. However,

the replacement should be of worn out unit by the new unit of identical design for restoring

the efficiency function and should not involve improvement (Sikka 2017). Finally, ATO

states that a taxpayer is allowed to claim deduction for the cost of business assets installed on

the premises that is below $20000. An immediate deduction is permitted to taxpayer under

this circumstances.

Applications:

The mixed business carried on by Daniel and Olivia is termed as partnership under

“division 5 of ITAA 1936”. In other words, Daniel and Olivia are carrying on the business as

partners that is in receipt of the ordinary income or statutory income together under “section

995-1 (1), ITAA 1997”.

For the duration of partnership their business transactions included the cash receipts

from sale and debtors payments. Referring to “Scott v CT (1935)” these receipts are treated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

as the ordinary income under “section 6-5, ITAA 1997” (von Haldenwang and von Schiller

2016).

Additionally, for the duration of partnership their business transactions also included

outgoings such as car expenses, electricity bill, rates, insurance etc. Citing the interpretation

of “Amalgamated Zinc Ltd v FCT (1935)” these partnership expenses are treated as

allowable deduction because they are incurred in the due course of producing the taxable

income.

Daniel and Olivia also withdrawn cash and took items from the bottle shops for their

private consumption. The drawings made by each Daniel and Olivia is excluded from

deductions because these expenses meets the negative limbs of “section 8-1 (2)” which is

private or domestic in nature.

Repairs and maintenance expenses in the form of shop painting and refrigerator motor

replacement was made from the partnership business. The shop painting is allowed for

deduction under “section 25-10” because the painting was done on business premises to

resolve the current corrosion and also to prevent the premises from deteriorating further.

Furthermore, replacing the refrigerator motor parts also amounts to deductible repairs under

“section 25-10” because the replacement was for the worn out unit by a new unit of matching

design for restoring the efficiency function of the refrigerator. Finally, the purchase of new

restaurant freezer will be allowed for immediate deduction because the cost of asset is below

the ATO prescribed limit of $20,000 and it is entirely used for business purpose.

as the ordinary income under “section 6-5, ITAA 1997” (von Haldenwang and von Schiller

2016).

Additionally, for the duration of partnership their business transactions also included

outgoings such as car expenses, electricity bill, rates, insurance etc. Citing the interpretation

of “Amalgamated Zinc Ltd v FCT (1935)” these partnership expenses are treated as

allowable deduction because they are incurred in the due course of producing the taxable

income.

Daniel and Olivia also withdrawn cash and took items from the bottle shops for their

private consumption. The drawings made by each Daniel and Olivia is excluded from

deductions because these expenses meets the negative limbs of “section 8-1 (2)” which is

private or domestic in nature.

Repairs and maintenance expenses in the form of shop painting and refrigerator motor

replacement was made from the partnership business. The shop painting is allowed for

deduction under “section 25-10” because the painting was done on business premises to

resolve the current corrosion and also to prevent the premises from deteriorating further.

Furthermore, replacing the refrigerator motor parts also amounts to deductible repairs under

“section 25-10” because the replacement was for the worn out unit by a new unit of matching

design for restoring the efficiency function of the refrigerator. Finally, the purchase of new

restaurant freezer will be allowed for immediate deduction because the cost of asset is below

the ATO prescribed limit of $20,000 and it is entirely used for business purpose.

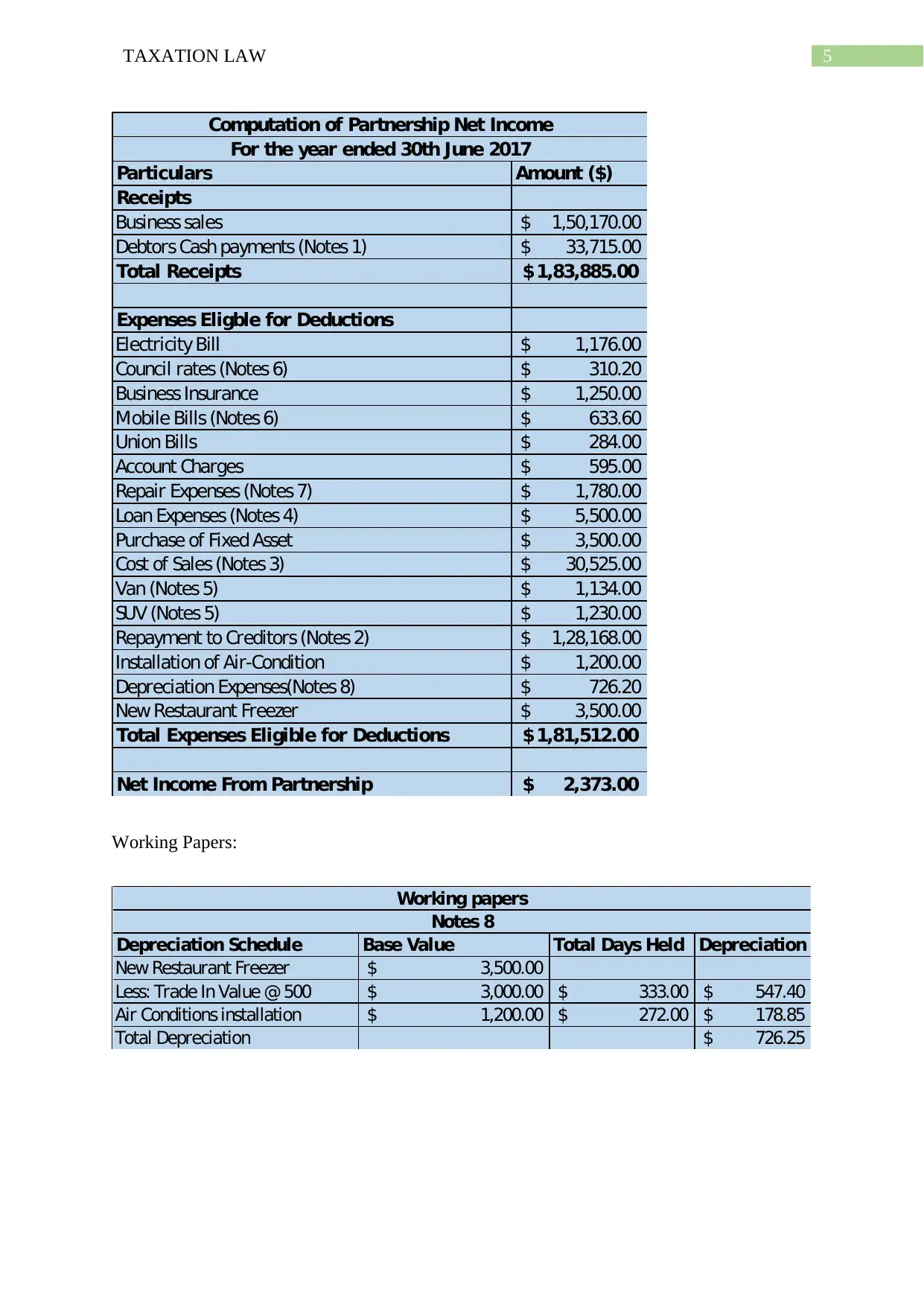

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

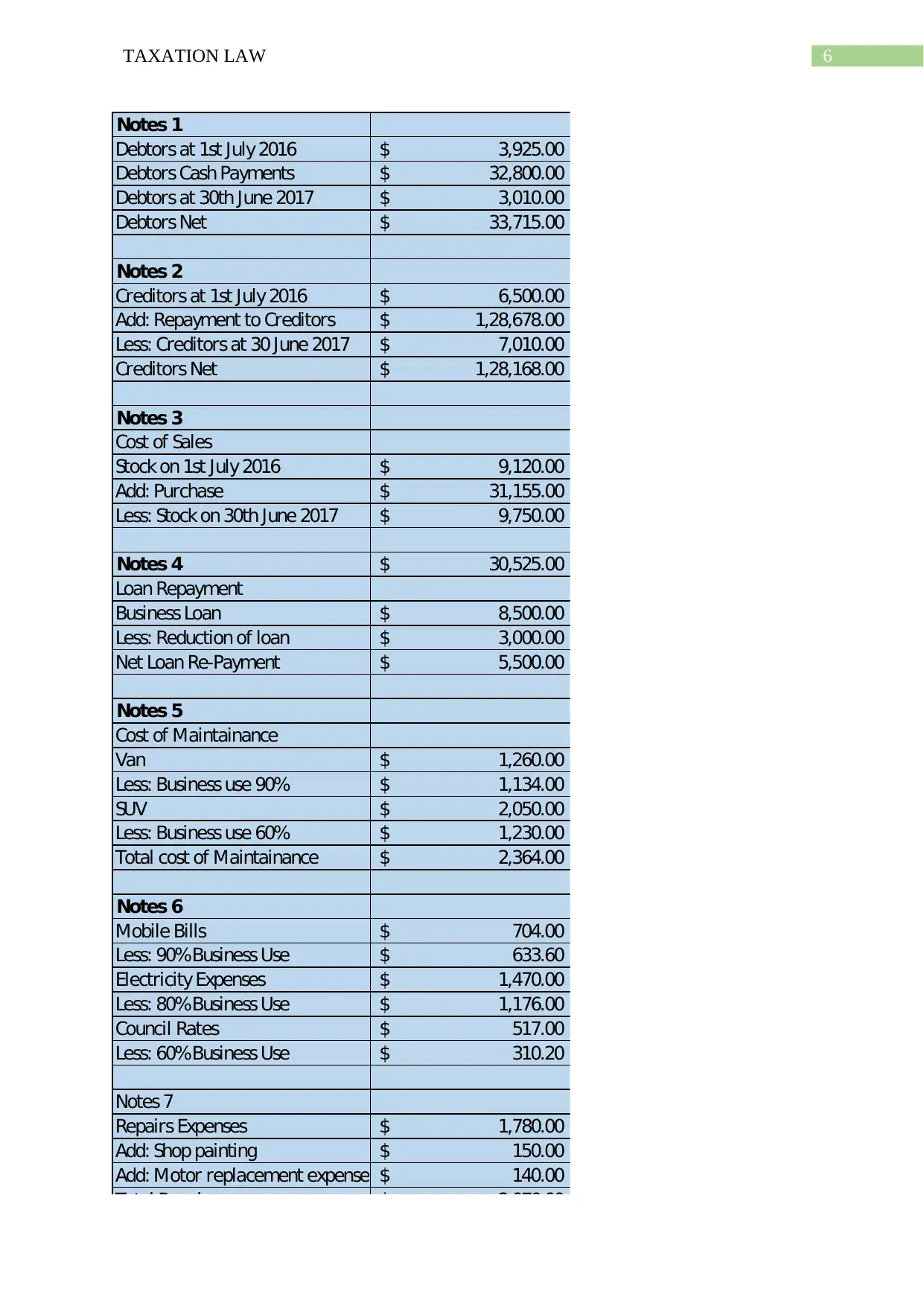

6TAXATION LAW

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Conclusion:

The income made by the partners under partnership will be distributed with reference

to “section 92 of the ITAA 1936” and will be accountable for paying tax on such

distributions made.

Answer to question 2:

Issues:

Whether making any payment for discharging of the whole or in portion the

obligation of the person gives rise to the expense payment fringe benefit under “sec 20,

FBTA Act 1986”?

Rule:

There is an explanation made under the “sec 20, FBTA Act 1986” that when it is

found that the provider or the employer makes the payment on behalf of the recipient for

discharging of the obligations either in parts or wholly for paying the amount to the third

party in relation to the expenses that is occurred by the recipient gives rise to expense

payment fringe benefit (Ashcraft 2016). An expense payment fringe benefit also arises when

the recipient is reimbursed by the employer either in full or in parts in relation to the amount

of expenses that is occurred by the recipient.

An explanation has been regarding the taxable value of expense payment FBT under

“sec 23 of FBTA Act 1986”. In view of that, the chargeable amount includes the value

provided to the recipient during the year of taxation relating to the expenses payment fringe

benefit occurred through the taxation year (Soled and Thomas 2016). In other words, the

taxable value of the expenses payment fringe benefit refers to the amount that the employer

pays or reimburses to the employee.

Conclusion:

The income made by the partners under partnership will be distributed with reference

to “section 92 of the ITAA 1936” and will be accountable for paying tax on such

distributions made.

Answer to question 2:

Issues:

Whether making any payment for discharging of the whole or in portion the

obligation of the person gives rise to the expense payment fringe benefit under “sec 20,

FBTA Act 1986”?

Rule:

There is an explanation made under the “sec 20, FBTA Act 1986” that when it is

found that the provider or the employer makes the payment on behalf of the recipient for

discharging of the obligations either in parts or wholly for paying the amount to the third

party in relation to the expenses that is occurred by the recipient gives rise to expense

payment fringe benefit (Ashcraft 2016). An expense payment fringe benefit also arises when

the recipient is reimbursed by the employer either in full or in parts in relation to the amount

of expenses that is occurred by the recipient.

An explanation has been regarding the taxable value of expense payment FBT under

“sec 23 of FBTA Act 1986”. In view of that, the chargeable amount includes the value

provided to the recipient during the year of taxation relating to the expenses payment fringe

benefit occurred through the taxation year (Soled and Thomas 2016). In other words, the

taxable value of the expenses payment fringe benefit refers to the amount that the employer

pays or reimburses to the employee.

8TAXATION LAW

According to the subsistence of “sect 25, FBTA Act 1986” a housing fringe benefit

occurs for whole or part of the year of taxation when the employer grants the housing rights

to the employee shall be taken to have constituted a benefit that is provided by the employer

to the recipient during the year of taxation (Givati 2015).

In order to determine the market value of the housing right under “section 27, FBTA

Act 1986” the market value of the employee’s present right to accommodation in relation the

housing fringe benefit where the employee is entitled in respect of the housing right that

requires the employee to make payment to the second person (Mallone 2016). This includes

the payment made in discharge of either full or in parts as the obligation of the person to the

amount to the third person in respect of the expenditure occurred by the employee.

Application:

In context of John employed as the senior executive with the printing firm is paid by

his employer for his child school fees. The child school fees is provided by the employer as

the part of his remuneration package that amounts to $15,000. In pursuant to “sec 20, FBTA

Act 1986” the employer here makes the payment on behalf of John for discharging of the

obligations in respect of his child school to the third party in relation to the expenses that is

occurred by the recipient. This ultimately gives rise to expense payment fringe benefit for the

employer of John under “sec 20, FBTA Act 1986” (Givati 2015).

In view of that, the chargeable amount includes the value provided to the John during

the year of taxation by the employer, relates to the expenses payment fringe benefit occurred

throughout the taxation year. In other words, the employer of John will be liable taxable

value of the expenses payment fringe benefit under “section 23, FBTA Act 1986” that the

employer paid as the part of John remuneration package.

According to the subsistence of “sect 25, FBTA Act 1986” a housing fringe benefit

occurs for whole or part of the year of taxation when the employer grants the housing rights

to the employee shall be taken to have constituted a benefit that is provided by the employer

to the recipient during the year of taxation (Givati 2015).

In order to determine the market value of the housing right under “section 27, FBTA

Act 1986” the market value of the employee’s present right to accommodation in relation the

housing fringe benefit where the employee is entitled in respect of the housing right that

requires the employee to make payment to the second person (Mallone 2016). This includes

the payment made in discharge of either full or in parts as the obligation of the person to the

amount to the third person in respect of the expenditure occurred by the employee.

Application:

In context of John employed as the senior executive with the printing firm is paid by

his employer for his child school fees. The child school fees is provided by the employer as

the part of his remuneration package that amounts to $15,000. In pursuant to “sec 20, FBTA

Act 1986” the employer here makes the payment on behalf of John for discharging of the

obligations in respect of his child school to the third party in relation to the expenses that is

occurred by the recipient. This ultimately gives rise to expense payment fringe benefit for the

employer of John under “sec 20, FBTA Act 1986” (Givati 2015).

In view of that, the chargeable amount includes the value provided to the John during

the year of taxation by the employer, relates to the expenses payment fringe benefit occurred

throughout the taxation year. In other words, the employer of John will be liable taxable

value of the expenses payment fringe benefit under “section 23, FBTA Act 1986” that the

employer paid as the part of John remuneration package.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

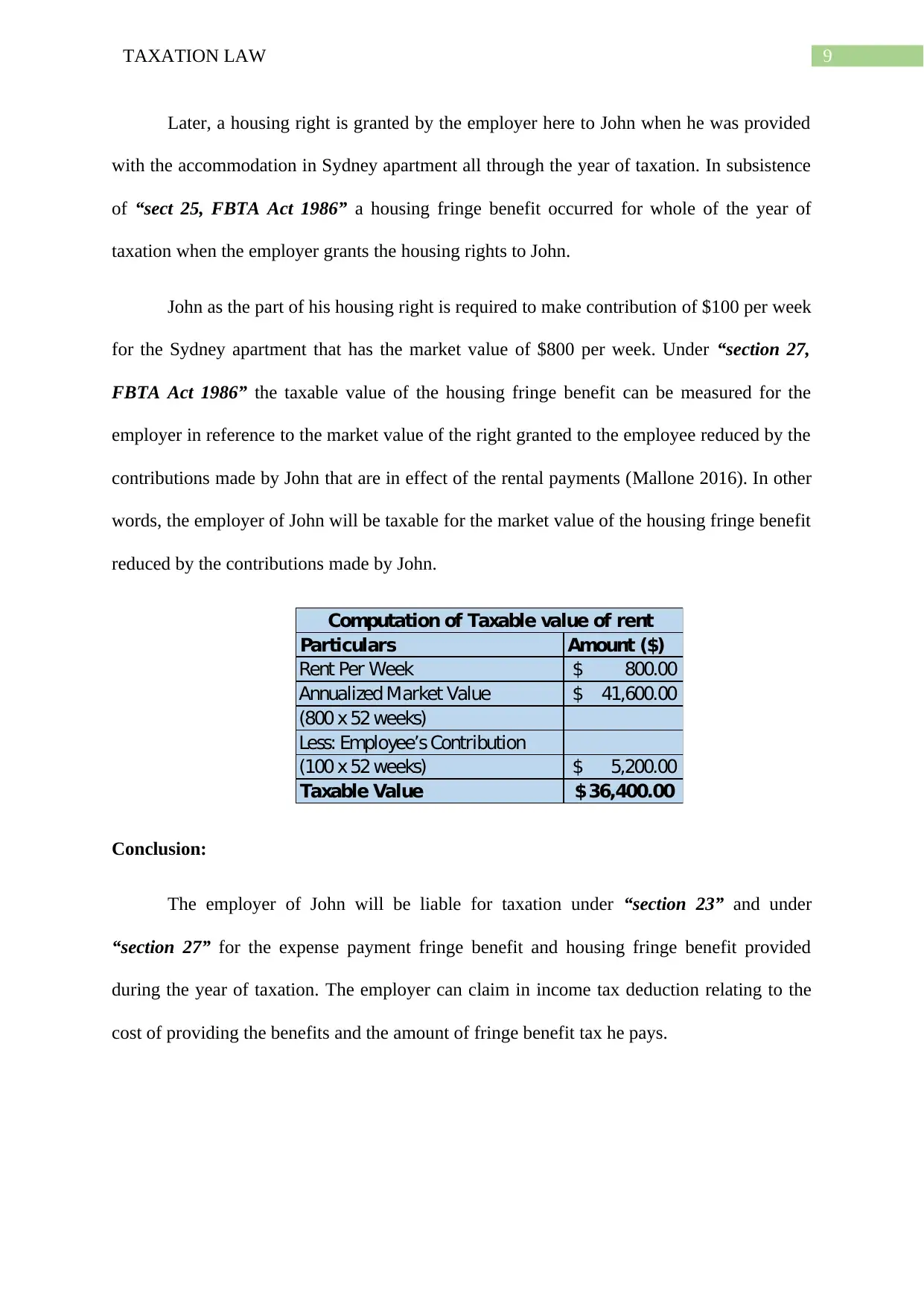

Later, a housing right is granted by the employer here to John when he was provided

with the accommodation in Sydney apartment all through the year of taxation. In subsistence

of “sect 25, FBTA Act 1986” a housing fringe benefit occurred for whole of the year of

taxation when the employer grants the housing rights to John.

John as the part of his housing right is required to make contribution of $100 per week

for the Sydney apartment that has the market value of $800 per week. Under “section 27,

FBTA Act 1986” the taxable value of the housing fringe benefit can be measured for the

employer in reference to the market value of the right granted to the employee reduced by the

contributions made by John that are in effect of the rental payments (Mallone 2016). In other

words, the employer of John will be taxable for the market value of the housing fringe benefit

reduced by the contributions made by John.

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer of John will be liable for taxation under “section 23” and under

“section 27” for the expense payment fringe benefit and housing fringe benefit provided

during the year of taxation. The employer can claim in income tax deduction relating to the

cost of providing the benefits and the amount of fringe benefit tax he pays.

Later, a housing right is granted by the employer here to John when he was provided

with the accommodation in Sydney apartment all through the year of taxation. In subsistence

of “sect 25, FBTA Act 1986” a housing fringe benefit occurred for whole of the year of

taxation when the employer grants the housing rights to John.

John as the part of his housing right is required to make contribution of $100 per week

for the Sydney apartment that has the market value of $800 per week. Under “section 27,

FBTA Act 1986” the taxable value of the housing fringe benefit can be measured for the

employer in reference to the market value of the right granted to the employee reduced by the

contributions made by John that are in effect of the rental payments (Mallone 2016). In other

words, the employer of John will be taxable for the market value of the housing fringe benefit

reduced by the contributions made by John.

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer of John will be liable for taxation under “section 23” and under

“section 27” for the expense payment fringe benefit and housing fringe benefit provided

during the year of taxation. The employer can claim in income tax deduction relating to the

cost of providing the benefits and the amount of fringe benefit tax he pays.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Ashcraft, K.L., 2016. Fringe benefits? Revisi (ti) ng the relationship between feminism and

Critical Management Studies. In The Routledge companion to critical management

studies (p. 93). Routledge.

Borden, B.T., 2015. Rethinking the Tax-Revenue Effect of REIT Taxation. Fla. Tax Rev., 17,

p.527.

Givati, Y., 2015. Googling a Free Lunch: The Taxation of Fringe Benefits. Tax L. Rev., 69,

p.275.

Lee, N., 2015. Revenue law: principles and practice. Bloomsbury Publishing.

Mallone, G., 2016. New tax incentives on occupational welfare benefits in the budgetary law

for 2016: new opportunities for workers and employers. Social Policies, 3(2), pp.359-362.

McNulty, J. and McCouch, G., 2015. Federal estate and gift taxation in a nutshell. West

Academic.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Picciotto, S., 2015. Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), pp.165-184.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Soled, J.A. and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

References:

Ashcraft, K.L., 2016. Fringe benefits? Revisi (ti) ng the relationship between feminism and

Critical Management Studies. In The Routledge companion to critical management

studies (p. 93). Routledge.

Borden, B.T., 2015. Rethinking the Tax-Revenue Effect of REIT Taxation. Fla. Tax Rev., 17,

p.527.

Givati, Y., 2015. Googling a Free Lunch: The Taxation of Fringe Benefits. Tax L. Rev., 69,

p.275.

Lee, N., 2015. Revenue law: principles and practice. Bloomsbury Publishing.

Mallone, G., 2016. New tax incentives on occupational welfare benefits in the budgetary law

for 2016: new opportunities for workers and employers. Social Policies, 3(2), pp.359-362.

McNulty, J. and McCouch, G., 2015. Federal estate and gift taxation in a nutshell. West

Academic.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Picciotto, S., 2015. Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), pp.165-184.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Soled, J.A. and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

11TAXATION LAW

von Haldenwang, C. and von Schiller, A., 2016. The politics of taxation: introduction to the

special section. The Journal of Development Studies, 52(12), pp.1685-1688.

von Haldenwang, C. and von Schiller, A., 2016. The politics of taxation: introduction to the

special section. The Journal of Development Studies, 52(12), pp.1685-1688.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.