Taxation Law Assignment: Analysis of Tax Laws and Cases

VerifiedAdded on 2019/10/31

|14

|2942

|445

Homework Assignment

AI Summary

This taxation law assignment delves into several key areas of tax law. The assignment begins by analyzing whether a taxpayer can offset capital losses, referencing relevant sections of the ITAA 1997. It then explores the computation of Fringe Benefit Tax (FBT) under the Fringe Benefit Tax Act 1986, including relevant taxation rulings. The assignment further examines the distribution of losses in the context of rental property ownership, considering case law and taxation rulings. The fourth section addresses tax avoidance principles, referencing the IRC v Duke of Westminster case. Finally, the assignment evaluates the application of subsection 6 (1) of the ITAA 1997 concerning timber curtailment. Each section includes a discussion of the issue, relevant laws, applications, and conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications...............................................................................................................................3

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 3:.................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................8

Answer to question 4:.................................................................................................................8

Answer to question 5:.................................................................................................................9

Issue:..........................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications...............................................................................................................................3

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 3:.................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................8

Answer to question 4:.................................................................................................................8

Answer to question 5:.................................................................................................................9

Issue:..........................................................................................................................................9

2TAXATION LAW

Laws:..........................................................................................................................................9

Application:................................................................................................................................9

Conclusion:..............................................................................................................................11

Reference list:...........................................................................................................................12

Laws:..........................................................................................................................................9

Application:................................................................................................................................9

Conclusion:..............................................................................................................................11

Reference list:...........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

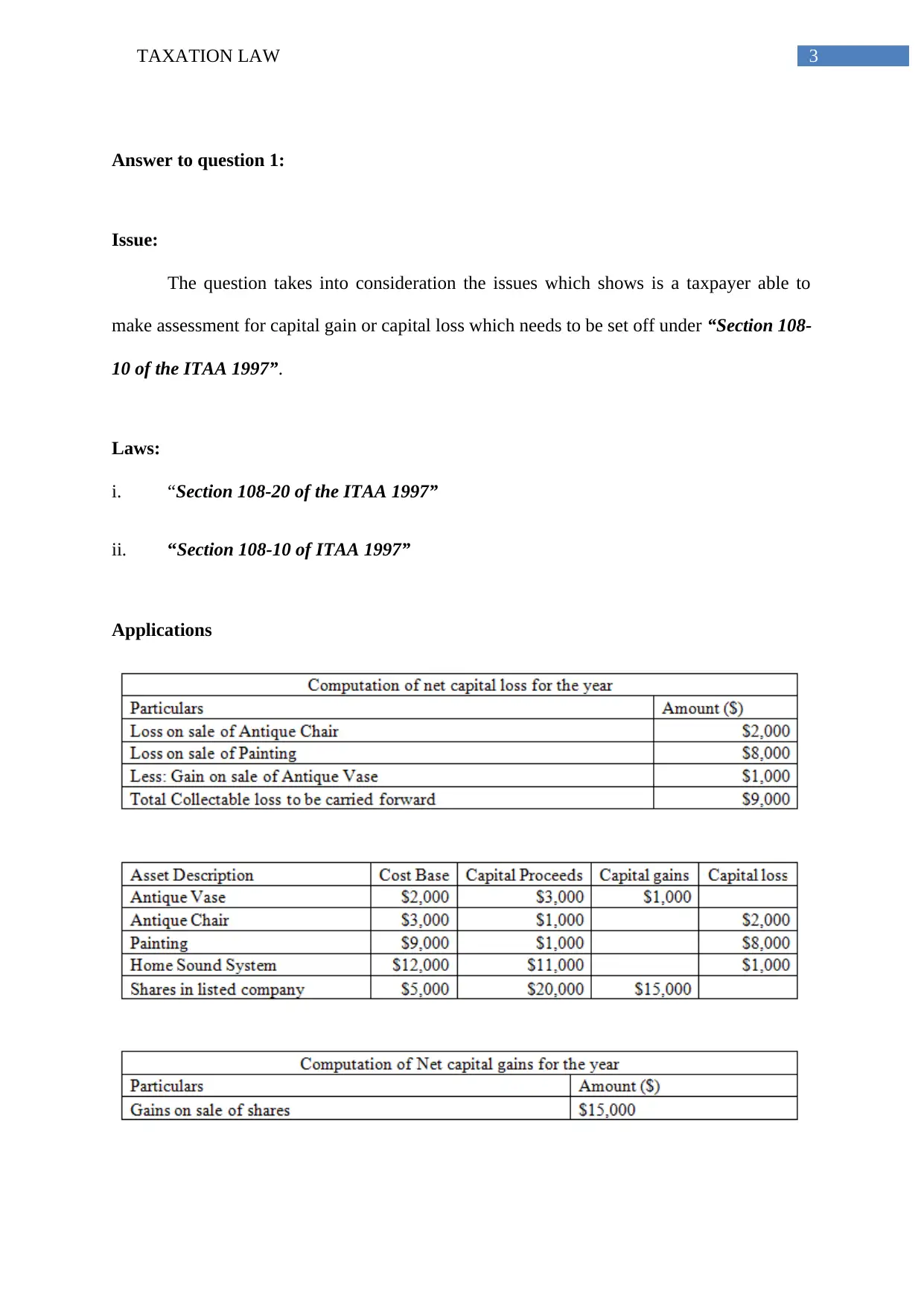

Answer to question 1:

Issue:

The question takes into consideration the issues which shows is a taxpayer able to

make assessment for capital gain or capital loss which needs to be set off under “Section 108-

10 of the ITAA 1997”.

Laws:

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Applications

Answer to question 1:

Issue:

The question takes into consideration the issues which shows is a taxpayer able to

make assessment for capital gain or capital loss which needs to be set off under “Section 108-

10 of the ITAA 1997”.

Laws:

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Application:

The present circumstance of the tax payer has been state on the losses which has been

sustained as per the sale of the sound system which has been not seen to be approved for the

purpose of set off. This has been mainly depicted due to the losses which have taken place

due to the selling of the home sound system as it is having the characteristics of personal

asset and will not be allowed for set off. The main form of the guiding ruling has been

suggested with “section 108-10 of ITAA 1997” providing the main evidence which are seen

to be collectible in nature and not considered for offsetting of ordinary gains obtained with

the selling of the shares and will not be allowed for the setting off. The “section 108-10 of

the ITAA 1997”, has been identified with the consistency. It has been further discerned that

Eric has been able to produce the profit in terms of the sale of the assets which are ordinary in

nature with no existence in any form with the pertinent reductions. This has been

consequently seen with the capital gains for Eric observed with $15,000 (Rootes 2014).

Conclusion:

The various conversations has showed that Eric was not able to set off the loss

sustained with the collectibles and solely derived from the selling off the assets and are seen

to be ordinary in nature.

Answer to question 2:

Issue:

The introduction of the issue has been able to deal with the computation of the FBT

has been defined with the “fringe benefit act as per 1986” (Tiến and Mba 2013).

Application:

The present circumstance of the tax payer has been state on the losses which has been

sustained as per the sale of the sound system which has been not seen to be approved for the

purpose of set off. This has been mainly depicted due to the losses which have taken place

due to the selling of the home sound system as it is having the characteristics of personal

asset and will not be allowed for set off. The main form of the guiding ruling has been

suggested with “section 108-10 of ITAA 1997” providing the main evidence which are seen

to be collectible in nature and not considered for offsetting of ordinary gains obtained with

the selling of the shares and will not be allowed for the setting off. The “section 108-10 of

the ITAA 1997”, has been identified with the consistency. It has been further discerned that

Eric has been able to produce the profit in terms of the sale of the assets which are ordinary in

nature with no existence in any form with the pertinent reductions. This has been

consequently seen with the capital gains for Eric observed with $15,000 (Rootes 2014).

Conclusion:

The various conversations has showed that Eric was not able to set off the loss

sustained with the collectibles and solely derived from the selling off the assets and are seen

to be ordinary in nature.

Answer to question 2:

Issue:

The introduction of the issue has been able to deal with the computation of the FBT

has been defined with the “fringe benefit act as per 1986” (Tiến and Mba 2013).

5TAXATION LAW

Laws:

i. “Fringe Benefit Tax Act 1986”

ii. “Taxation Rulings TR 93/6”

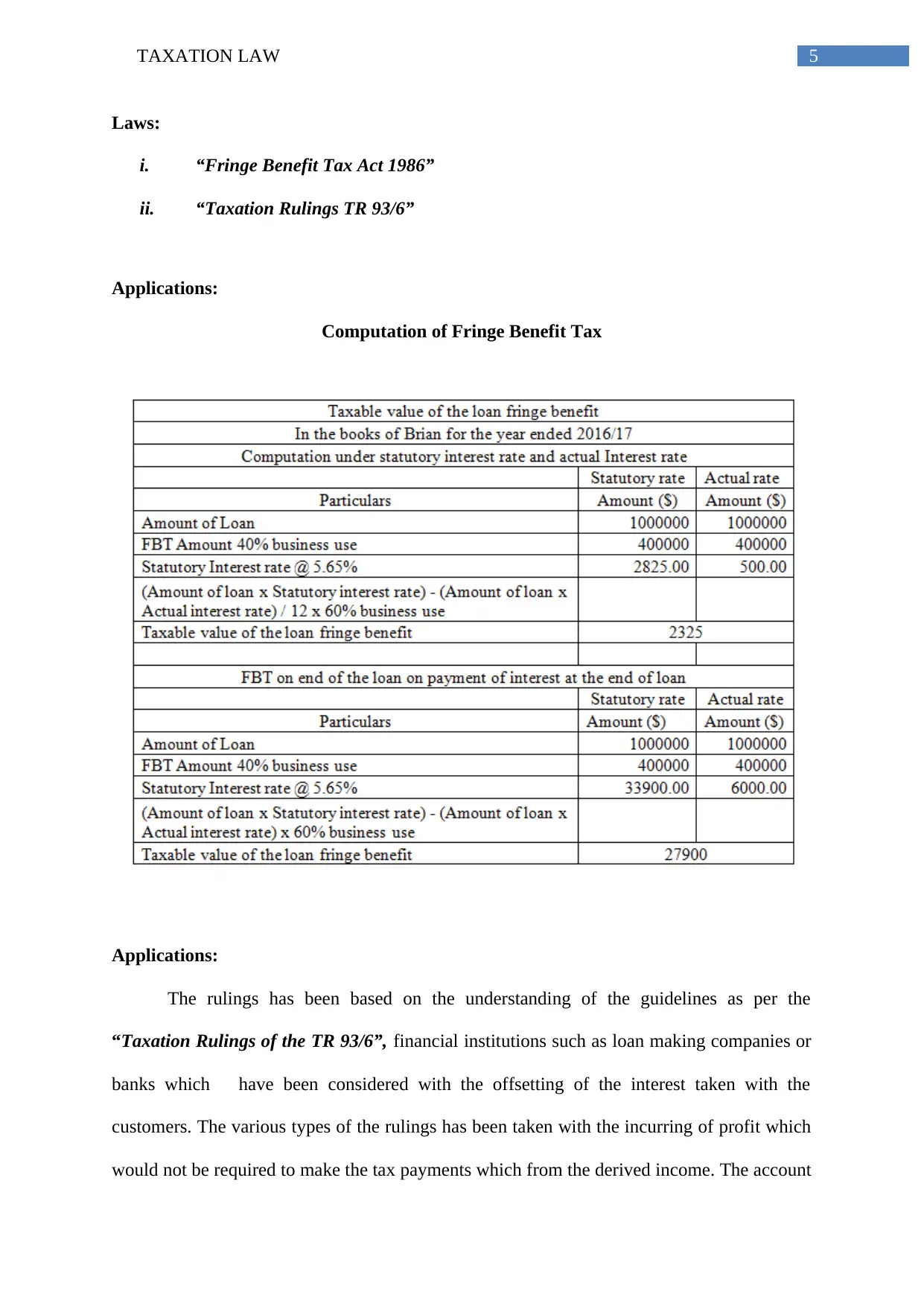

Applications:

Computation of Fringe Benefit Tax

Applications:

The rulings has been based on the understanding of the guidelines as per the

“Taxation Rulings of the TR 93/6”, financial institutions such as loan making companies or

banks which have been considered with the offsetting of the interest taken with the

customers. The various types of the rulings has been taken with the incurring of profit which

would not be required to make the tax payments which from the derived income. The account

Laws:

i. “Fringe Benefit Tax Act 1986”

ii. “Taxation Rulings TR 93/6”

Applications:

Computation of Fringe Benefit Tax

Applications:

The rulings has been based on the understanding of the guidelines as per the

“Taxation Rulings of the TR 93/6”, financial institutions such as loan making companies or

banks which have been considered with the offsetting of the interest taken with the

customers. The various types of the rulings has been taken with the incurring of profit which

would not be required to make the tax payments which from the derived income. The account

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

of the guidelines which has been defined under the “Taxation Ruling of the 93/6” as per the

circumstance which showed that Brain has been able to discharge the amount from the bank

based on the payment of the interest at the end loan period and as Brian has been not

identified with the will to pay tax (Armstrong et al. 2015).

Conclusion:

The given conversation has showed the understanding of the loan interest which is

seen to be payable at the end of the loan period and not income tax needs to be paid to the

bank.

Answer to question 3:

Issue:

The given matter has been seen to be associated with the distribution of loss which is

sustained as per the ownership by the tax payers along with the context of the rental property.

Laws:

i. “FC of T v McDonald”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation ruling TR 93/23”

Applications:

The main conformity with the “Taxation Ruling TR 93/32”, seen with the rulings

which has been provided with the different types of the explanations based on the income or

the loss derived with the property rent and the joint property owners. Additionally, the

various types of the discussions have been able to show the guidelines gauging as per the

of the guidelines which has been defined under the “Taxation Ruling of the 93/6” as per the

circumstance which showed that Brain has been able to discharge the amount from the bank

based on the payment of the interest at the end loan period and as Brian has been not

identified with the will to pay tax (Armstrong et al. 2015).

Conclusion:

The given conversation has showed the understanding of the loan interest which is

seen to be payable at the end of the loan period and not income tax needs to be paid to the

bank.

Answer to question 3:

Issue:

The given matter has been seen to be associated with the distribution of loss which is

sustained as per the ownership by the tax payers along with the context of the rental property.

Laws:

i. “FC of T v McDonald”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation ruling TR 93/23”

Applications:

The main conformity with the “Taxation Ruling TR 93/32”, seen with the rulings

which has been provided with the different types of the explanations based on the income or

the loss derived with the property rent and the joint property owners. Additionally, the

various types of the discussions have been able to show the guidelines gauging as per the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

assessable position of the co-owners and is not seen to be accountable for the purpose of

carrying of the business as per the defined objectives. In the given context Jack and Jill has

been able to evaluate the various types of the considerations which has been able to show the

assessable position as per the rented property. In the given context Jack has been seen to be

eligible with 10% of the profits derived from the Jill in getting of 90% of the rented property

(Richardson, Taylor and Wright 2014).

The various types of the considerations has been further seen to be defined under the

“TR 92/32”, with the joint ownership considered with the property rented as per the

partnership and defined as per the general notion of the general law. The ruling has been

further seen to not include the various types of the joint ownership of any business which has

been able to comply with the taxable income. The loss of the income has been seen to be

sustained with the ownership of the rented property with the foundation of the income tax and

was not taken into account as per the partnership and the principles of the general law

(Hasseldine and Morris 2013).

The taxation ruling has been further able to state about the ruling of the “TR 92/32”

which has been provided with the explanation has per the joint ownership of the property

rented and not treated as per the partnership with the general law. The agreement of the

partnership has been taken with Jack and Jill who has been contained with the written, ethical

or oral agreement, which is not seen to be having any effect on the share of the income as per

the property rented (Taylor, Richardson and Taplin 2015). The clause of the agreement has

been accountable with 100% of the total loss which has been derived as per the rental

property. It has been further discerned that the various types of the considerations for the case

of “FC of T v McDonald (1987)”, has been considered with the agreement as per the Mr

McDonald entitled with 25% of the profits, on the contrary McDonald has been seen to be

entitled with 25% of the profits whereas Mrs McDonald is seen to be acquiring 75% of the

assessable position of the co-owners and is not seen to be accountable for the purpose of

carrying of the business as per the defined objectives. In the given context Jack and Jill has

been able to evaluate the various types of the considerations which has been able to show the

assessable position as per the rented property. In the given context Jack has been seen to be

eligible with 10% of the profits derived from the Jill in getting of 90% of the rented property

(Richardson, Taylor and Wright 2014).

The various types of the considerations has been further seen to be defined under the

“TR 92/32”, with the joint ownership considered with the property rented as per the

partnership and defined as per the general notion of the general law. The ruling has been

further seen to not include the various types of the joint ownership of any business which has

been able to comply with the taxable income. The loss of the income has been seen to be

sustained with the ownership of the rented property with the foundation of the income tax and

was not taken into account as per the partnership and the principles of the general law

(Hasseldine and Morris 2013).

The taxation ruling has been further able to state about the ruling of the “TR 92/32”

which has been provided with the explanation has per the joint ownership of the property

rented and not treated as per the partnership with the general law. The agreement of the

partnership has been taken with Jack and Jill who has been contained with the written, ethical

or oral agreement, which is not seen to be having any effect on the share of the income as per

the property rented (Taylor, Richardson and Taplin 2015). The clause of the agreement has

been accountable with 100% of the total loss which has been derived as per the rental

property. It has been further discerned that the various types of the considerations for the case

of “FC of T v McDonald (1987)”, has been considered with the agreement as per the Mr

McDonald entitled with 25% of the profits, on the contrary McDonald has been seen to be

entitled with 25% of the profits whereas Mrs McDonald is seen to be acquiring 75% of the

8TAXATION LAW

total profit derived from the property. The loss of Mr McDonald needs to be shouldered with

100% of the total loss. The same has been primarily done as per the advancement of the

income to wife and indemnifying such loss (Whait 2014).

Comparably, the present aspect of the partnership has been seen to be taken between

Jack and Jill and this partnership is not considered as per the legal aspects and the losses

arising with such rented property, which needs to be shared between them equally (Taylor

and Richardson 2014).

Conclusion:

The discussion of the scenario has been seen to be understood as per the share of loss

arising out of Jack and Jill considered on equal basis with the joint ownership and does not

account for the partnership.

Answer to question 4:

The most important ruling of the subject has been further able to decide of the

avoidance of tax which has been accepted with the legal case laws of “IRC v Duke

Westminster (1936)”. It has been further discerned that the wages to Duke of Westminster

has been seen to be considered on weekly basis and the same has been entered into the

contract with the drew up of the covenant agreement which has been made with an equivalent

amount. Despite of this, Gardener has yet received the amount identical to the wages,

however Duke has been able to particularly gained with the benefits of the tax and the

amount of the wages which has been gained in advantage with the tax benefits stated under

the law and applied at the same time when the covenant has been able to reduce the liability

of Duke to surtax (Permani 2013). The given case has been able to define the eligibility of the

individual for the various affairs of the taxation seen with the sole objective of assigning of

total profit derived from the property. The loss of Mr McDonald needs to be shouldered with

100% of the total loss. The same has been primarily done as per the advancement of the

income to wife and indemnifying such loss (Whait 2014).

Comparably, the present aspect of the partnership has been seen to be taken between

Jack and Jill and this partnership is not considered as per the legal aspects and the losses

arising with such rented property, which needs to be shared between them equally (Taylor

and Richardson 2014).

Conclusion:

The discussion of the scenario has been seen to be understood as per the share of loss

arising out of Jack and Jill considered on equal basis with the joint ownership and does not

account for the partnership.

Answer to question 4:

The most important ruling of the subject has been further able to decide of the

avoidance of tax which has been accepted with the legal case laws of “IRC v Duke

Westminster (1936)”. It has been further discerned that the wages to Duke of Westminster

has been seen to be considered on weekly basis and the same has been entered into the

contract with the drew up of the covenant agreement which has been made with an equivalent

amount. Despite of this, Gardener has yet received the amount identical to the wages,

however Duke has been able to particularly gained with the benefits of the tax and the

amount of the wages which has been gained in advantage with the tax benefits stated under

the law and applied at the same time when the covenant has been able to reduce the liability

of Duke to surtax (Permani 2013). The given case has been able to define the eligibility of the

individual for the various affairs of the taxation seen with the sole objective of assigning of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

appropriate laws which would have been otherwise lower. The individual cannot be eligible

in order to make payment for the increased taxation amount.

The present age principle has been further able to define the purpose of obtaining of

the result with ingenuity of not forcing the individual to pay the increased sum of the tax.

The various decisions of the individual have been seen with the opportunity to reduce the tax

liability in agreement of the financial framework with the law (Lennox, Lisowsky and

Pittman 2013).

Answer to question 5:

Issue:

the important question has shown with the application of “subsection 6 (1) of the

ITAA 1997” for the curtailment of timber.

Laws:

i. “Subsection 6 (1) of the ITAA 1936”

ii. “McCauley v FC of T”

Application:

Based on the present assessment it has been seen that Bill has been considered to be

owner of the land with several pine trees. In the initial stages the land has been subjected to

clearance for grazing sheep however on being approached by the logging companies, which

has agreed to pay a total amount of $1000 for every 100 meter of the timber acquired from

logging of the firm form the Bill’s land (Richardson, Taylor and Lanis 2015).

appropriate laws which would have been otherwise lower. The individual cannot be eligible

in order to make payment for the increased taxation amount.

The present age principle has been further able to define the purpose of obtaining of

the result with ingenuity of not forcing the individual to pay the increased sum of the tax.

The various decisions of the individual have been seen with the opportunity to reduce the tax

liability in agreement of the financial framework with the law (Lennox, Lisowsky and

Pittman 2013).

Answer to question 5:

Issue:

the important question has shown with the application of “subsection 6 (1) of the

ITAA 1997” for the curtailment of timber.

Laws:

i. “Subsection 6 (1) of the ITAA 1936”

ii. “McCauley v FC of T”

Application:

Based on the present assessment it has been seen that Bill has been considered to be

owner of the land with several pine trees. In the initial stages the land has been subjected to

clearance for grazing sheep however on being approached by the logging companies, which

has agreed to pay a total amount of $1000 for every 100 meter of the timber acquired from

logging of the firm form the Bill’s land (Richardson, Taylor and Lanis 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

The “Taxation ruling TR 95/6”, has been seen to determine the income tax rulings

based on the activities taken from the primary production and forestry. It has further defined

that the various types of the considerations made with the individual deriving income has

been further defined based on the forestry activities which is assessable. The various rulings

have been further seen to be applicable as per the individual taxpayers, who are seen to

indulge in the various types of the forestry activities like disposing of timber. The

consideration of the explanation as per “Subsection 6 (1) of the ITAA 1936”, the individual

taxpayer is seen to be associated with the operations of forest and the same needs to be

treated as per the producer of income tax and the forest activities which are viewed with the

performing of the business activities (Meng and Pham 2017).

The primary production activities has been further seen to be referred with the

planting of the trees and tending down of the trees in a particular plantation as per

“subsection 6 (1) of the ITAA 1997” aimed to be considered as per the cutting down of the

vegetation. As per the present context, the primary production for tending down of the pine

trees has been considered with the large portion of the land which is owned by him. In

addition to this, the forest operations are seen to be usually considered for the operations with

the planting or tending of the trees in the vegetation and taxpayer was not seen to originally

plant the trees.

Based on the context of the above the explanation, Bill has not seen to plant trees and

the sum is received with the selling of the timber and the same which has been considered for

the assessment. Despite of this, the sales has been comprised with the portion of assets having

commercial values and receipts of the taxable income considered as per “subsection 36 (1)”.

The alternate scenario has been further seen to be regarded with the taxpayer paying a

large amount of $50,000 by the simple assignment of the right for the logging company to cut

The “Taxation ruling TR 95/6”, has been seen to determine the income tax rulings

based on the activities taken from the primary production and forestry. It has further defined

that the various types of the considerations made with the individual deriving income has

been further defined based on the forestry activities which is assessable. The various rulings

have been further seen to be applicable as per the individual taxpayers, who are seen to

indulge in the various types of the forestry activities like disposing of timber. The

consideration of the explanation as per “Subsection 6 (1) of the ITAA 1936”, the individual

taxpayer is seen to be associated with the operations of forest and the same needs to be

treated as per the producer of income tax and the forest activities which are viewed with the

performing of the business activities (Meng and Pham 2017).

The primary production activities has been further seen to be referred with the

planting of the trees and tending down of the trees in a particular plantation as per

“subsection 6 (1) of the ITAA 1997” aimed to be considered as per the cutting down of the

vegetation. As per the present context, the primary production for tending down of the pine

trees has been considered with the large portion of the land which is owned by him. In

addition to this, the forest operations are seen to be usually considered for the operations with

the planting or tending of the trees in the vegetation and taxpayer was not seen to originally

plant the trees.

Based on the context of the above the explanation, Bill has not seen to plant trees and

the sum is received with the selling of the timber and the same which has been considered for

the assessment. Despite of this, the sales has been comprised with the portion of assets having

commercial values and receipts of the taxable income considered as per “subsection 36 (1)”.

The alternate scenario has been further seen to be regarded with the taxpayer paying a

large amount of $50,000 by the simple assignment of the right for the logging company to cut

11TAXATION LAW

down the necessary quantities which has been able to receive the timber considered under

“Royalties”. As defined in section 26 (f), the loyalties has been seen to be tending of the

timber and the same will be treated in the assessable income included in the income year. The

various types of the royalties received by Bill have been considered with felling of timber and

the same is to be treated with the carrying of the forest business operations. Considering the

rulings under the case of “McCauley v The Federal Commissioner of Taxation”, the

payments have been procured with assignment through the right of tending the timber.

Henceforth, the total amount will received by Bill in the various types of the alternative

scenario considered from the selling of timber and which needs to be included in the taxable

income comparable to “section 26 (f)” (Hasseldine and Morris 2013).

Conclusion:

The aforementioned analysis has been seen to be considered based on the amount

defined with the amount received by Bill and the consideration has been seen to be based on

the alternative scenario for the sum received for the granting right and the amount which

needs to be treated as royalties.

down the necessary quantities which has been able to receive the timber considered under

“Royalties”. As defined in section 26 (f), the loyalties has been seen to be tending of the

timber and the same will be treated in the assessable income included in the income year. The

various types of the royalties received by Bill have been considered with felling of timber and

the same is to be treated with the carrying of the forest business operations. Considering the

rulings under the case of “McCauley v The Federal Commissioner of Taxation”, the

payments have been procured with assignment through the right of tending the timber.

Henceforth, the total amount will received by Bill in the various types of the alternative

scenario considered from the selling of timber and which needs to be included in the taxable

income comparable to “section 26 (f)” (Hasseldine and Morris 2013).

Conclusion:

The aforementioned analysis has been seen to be considered based on the amount

defined with the amount received by Bill and the consideration has been seen to be based on

the alternative scenario for the sum received for the granting right and the amount which

needs to be treated as royalties.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.