Taxation Law Assignment - University Name, Semester 1, 2024

VerifiedAdded on 2020/04/07

|10

|2754

|243

Homework Assignment

AI Summary

This Taxation Law assignment solution addresses several tax-related scenarios. Question 1 examines the tax implications of capital gains from the sale of personal assets and collectibles, calculating net capital gains or losses. Question 2 analyzes the tax treatment of an incidental benefit, specifically a low-interest loan, determining the assessable amount. Question 3 explores the tax implications for a couple owning a rental property, considering the allocation of profits and losses. Question 4 discusses tax avoidance and the Westminster principle. Finally, Question 5 provides advice on the tax implications of income received from a logging company. The solution provides detailed analysis, supporting evidence, and conclusions for each question.

1

Taxation LAW

<Student ID>

<Student Name>

<University Name>

Taxation LAW

<Student ID>

<Student Name>

<University Name>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Question 1...................................................................................................................................................3

Introduction.............................................................................................................................................3

Critical analysis.......................................................................................................................................3

Supporting evidence................................................................................................................................3

Conclusion...............................................................................................................................................4

Question 2...................................................................................................................................................4

Introduction.............................................................................................................................................4

Critical analysis.......................................................................................................................................4

Supporting evidence................................................................................................................................5

Conclusion...............................................................................................................................................5

Question 3...................................................................................................................................................6

Introduction.............................................................................................................................................6

Critical analysis.......................................................................................................................................6

Supporting evidence................................................................................................................................6

Conclusion...............................................................................................................................................7

Question 4...................................................................................................................................................7

Introduction.............................................................................................................................................7

Critical analysis.......................................................................................................................................7

Supporting evidence................................................................................................................................7

Conclusion...............................................................................................................................................8

Question 5...................................................................................................................................................8

Introduction.............................................................................................................................................8

Critical thinking.......................................................................................................................................8

Supporting evidence................................................................................................................................8

Conclusion...............................................................................................................................................9

References...................................................................................................................................................9

Contents

Question 1...................................................................................................................................................3

Introduction.............................................................................................................................................3

Critical analysis.......................................................................................................................................3

Supporting evidence................................................................................................................................3

Conclusion...............................................................................................................................................4

Question 2...................................................................................................................................................4

Introduction.............................................................................................................................................4

Critical analysis.......................................................................................................................................4

Supporting evidence................................................................................................................................5

Conclusion...............................................................................................................................................5

Question 3...................................................................................................................................................6

Introduction.............................................................................................................................................6

Critical analysis.......................................................................................................................................6

Supporting evidence................................................................................................................................6

Conclusion...............................................................................................................................................7

Question 4...................................................................................................................................................7

Introduction.............................................................................................................................................7

Critical analysis.......................................................................................................................................7

Supporting evidence................................................................................................................................7

Conclusion...............................................................................................................................................8

Question 5...................................................................................................................................................8

Introduction.............................................................................................................................................8

Critical thinking.......................................................................................................................................8

Supporting evidence................................................................................................................................8

Conclusion...............................................................................................................................................9

References...................................................................................................................................................9

3

Question 1

Introduction

Eric has delineated examples of getting resources over the most recent one year. The ownership

of the benefits with Eric thus can be noticed as that was legitimate for a period not as much as a

year. The worries regarding the taxability of capital pickup for this situation can be

acknowledged just because of the state of the advantage's offering cost being more noteworthy

than the cost base at which it was obtained. One critical condition that could be seen on the

account of the Eric is the failure to acquire indexation advantage since the benefits were held for

not as much as a year (Coase, 2012).

Critical analysis

The advantages which are bought by people for satisfying individual destinations or delight and

amusement could be named as resources for individual utilize. Collectibles are excluded from the

benefits implied for individual utilize. The offer of advantages that have acquirement costs under

$10000 can't be liable to tax assessment of the capital benefits picked up from benefits. The

benefits obtained by Eric for individual utilize incorporate the offers of a recorded organization

at the cost of $5000 and the home sound framework at $12000 (Gale et al., 2011).

The advantages which are obtained for satisfying extra targets, for example, self-efficacies and in

addition giving happiness similarly as if there should be an occurrence of individual resources.

The capital additions gained from the offer of collectibles acquired at costs equivalent to or

under $500 can't be liable to the tax assessment. Eric acquired the collectibles which incorporate,

an antique vase at the price of $2000, an antique chair at the price of $3000 and a painting at the

price of $9000 (Hayek, 2012).

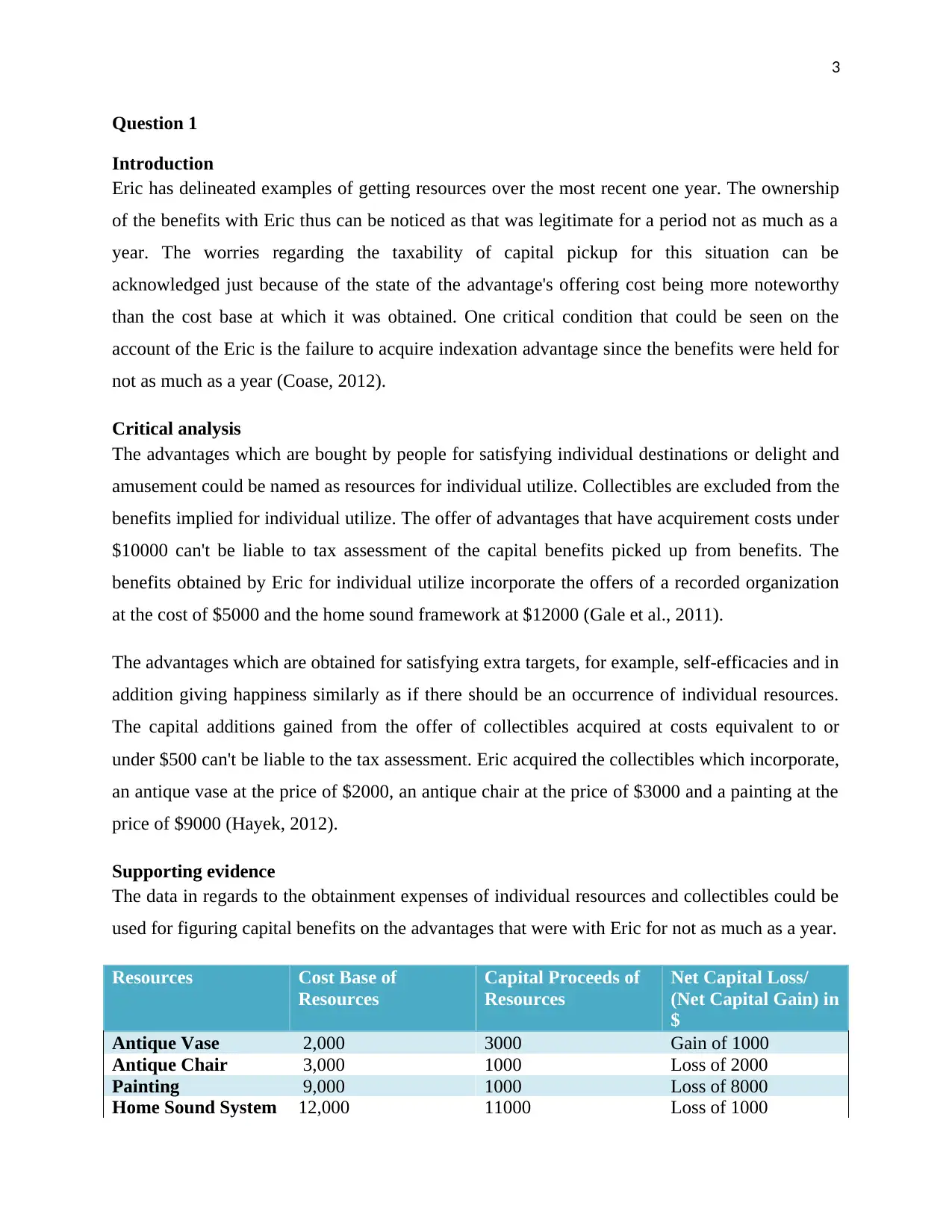

Supporting evidence

The data in regards to the obtainment expenses of individual resources and collectibles could be

used for figuring capital benefits on the advantages that were with Eric for not as much as a year.

Resources Cost Base of

Resources

Capital Proceeds of

Resources

Net Capital Loss/

(Net Capital Gain) in

$

Antique Vase 2,000 3000 Gain of 1000

Antique Chair 3,000 1000 Loss of 2000

Painting 9,000 1000 Loss of 8000

Home Sound System 12,000 11000 Loss of 1000

Question 1

Introduction

Eric has delineated examples of getting resources over the most recent one year. The ownership

of the benefits with Eric thus can be noticed as that was legitimate for a period not as much as a

year. The worries regarding the taxability of capital pickup for this situation can be

acknowledged just because of the state of the advantage's offering cost being more noteworthy

than the cost base at which it was obtained. One critical condition that could be seen on the

account of the Eric is the failure to acquire indexation advantage since the benefits were held for

not as much as a year (Coase, 2012).

Critical analysis

The advantages which are bought by people for satisfying individual destinations or delight and

amusement could be named as resources for individual utilize. Collectibles are excluded from the

benefits implied for individual utilize. The offer of advantages that have acquirement costs under

$10000 can't be liable to tax assessment of the capital benefits picked up from benefits. The

benefits obtained by Eric for individual utilize incorporate the offers of a recorded organization

at the cost of $5000 and the home sound framework at $12000 (Gale et al., 2011).

The advantages which are obtained for satisfying extra targets, for example, self-efficacies and in

addition giving happiness similarly as if there should be an occurrence of individual resources.

The capital additions gained from the offer of collectibles acquired at costs equivalent to or

under $500 can't be liable to the tax assessment. Eric acquired the collectibles which incorporate,

an antique vase at the price of $2000, an antique chair at the price of $3000 and a painting at the

price of $9000 (Hayek, 2012).

Supporting evidence

The data in regards to the obtainment expenses of individual resources and collectibles could be

used for figuring capital benefits on the advantages that were with Eric for not as much as a year.

Resources Cost Base of

Resources

Capital Proceeds of

Resources

Net Capital Loss/

(Net Capital Gain) in

$

Antique Vase 2,000 3000 Gain of 1000

Antique Chair 3,000 1000 Loss of 2000

Painting 9,000 1000 Loss of 8000

Home Sound System 12,000 11000 Loss of 1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

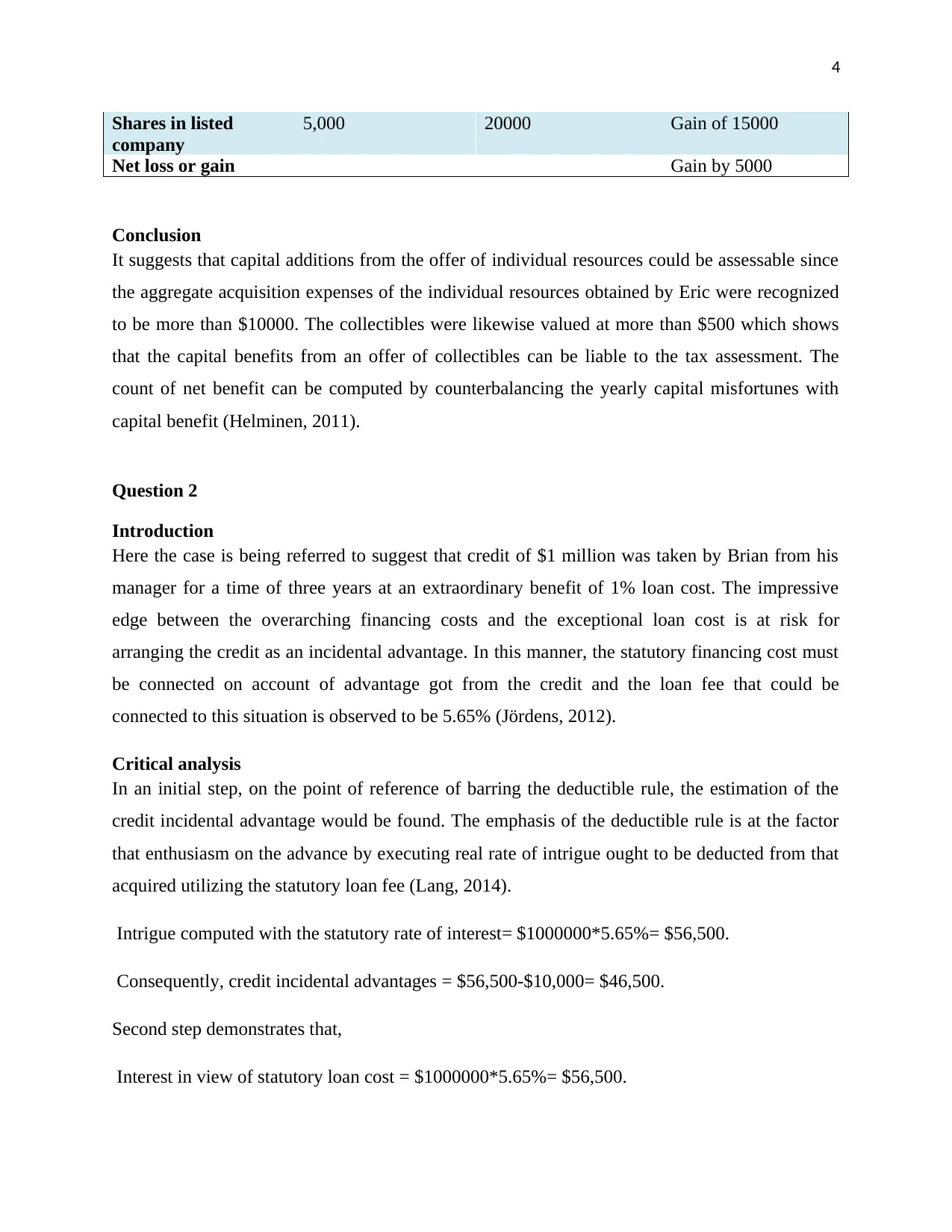

Shares in listed

company

5,000 20000 Gain of 15000

Net loss or gain Gain by 5000

Conclusion

It suggests that capital additions from the offer of individual resources could be assessable since

the aggregate acquisition expenses of the individual resources obtained by Eric were recognized

to be more than $10000. The collectibles were likewise valued at more than $500 which shows

that the capital benefits from an offer of collectibles can be liable to the tax assessment. The

count of net benefit can be computed by counterbalancing the yearly capital misfortunes with

capital benefit (Helminen, 2011).

Question 2

Introduction

Here the case is being referred to suggest that credit of $1 million was taken by Brian from his

manager for a time of three years at an extraordinary benefit of 1% loan cost. The impressive

edge between the overarching financing costs and the exceptional loan cost is at risk for

arranging the credit as an incidental advantage. In this manner, the statutory financing cost must

be connected on account of advantage got from the credit and the loan fee that could be

connected to this situation is observed to be 5.65% (Jördens, 2012).

Critical analysis

In an initial step, on the point of reference of barring the deductible rule, the estimation of the

credit incidental advantage would be found. The emphasis of the deductible rule is at the factor

that enthusiasm on the advance by executing real rate of intrigue ought to be deducted from that

acquired utilizing the statutory loan fee (Lang, 2014).

Intrigue computed with the statutory rate of interest= $1000000*5.65%= $56,500.

Consequently, credit incidental advantages = $56,500-$10,000= $46,500.

Second step demonstrates that,

Interest in view of statutory loan cost = $1000000*5.65%= $56,500.

Shares in listed

company

5,000 20000 Gain of 15000

Net loss or gain Gain by 5000

Conclusion

It suggests that capital additions from the offer of individual resources could be assessable since

the aggregate acquisition expenses of the individual resources obtained by Eric were recognized

to be more than $10000. The collectibles were likewise valued at more than $500 which shows

that the capital benefits from an offer of collectibles can be liable to the tax assessment. The

count of net benefit can be computed by counterbalancing the yearly capital misfortunes with

capital benefit (Helminen, 2011).

Question 2

Introduction

Here the case is being referred to suggest that credit of $1 million was taken by Brian from his

manager for a time of three years at an extraordinary benefit of 1% loan cost. The impressive

edge between the overarching financing costs and the exceptional loan cost is at risk for

arranging the credit as an incidental advantage. In this manner, the statutory financing cost must

be connected on account of advantage got from the credit and the loan fee that could be

connected to this situation is observed to be 5.65% (Jördens, 2012).

Critical analysis

In an initial step, on the point of reference of barring the deductible rule, the estimation of the

credit incidental advantage would be found. The emphasis of the deductible rule is at the factor

that enthusiasm on the advance by executing real rate of intrigue ought to be deducted from that

acquired utilizing the statutory loan fee (Lang, 2014).

Intrigue computed with the statutory rate of interest= $1000000*5.65%= $56,500.

Consequently, credit incidental advantages = $56,500-$10,000= $46,500.

Second step demonstrates that,

Interest in view of statutory loan cost = $1000000*5.65%= $56,500.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The supposition at this stage depends on the factor that the intrigue would be genuine sum

payable. Third Step is about, Brian, who has contributed 40% of the credit to address his future

commitments and thus,

Tax-deductible intrigue cost = $56,500*40%= $22,600 which can be viewed as theoretical. In

the fourth Step, the genuine duty deductible intrigue cost can be computed

On the intrigue in light of the real rate of intrigue which is: $10000*40%= $4000.

In fifth Step, it’s seen that, the subtraction of genuine duty deductible intrigue cost

From the theoretical figure could be introduced as, $22,600-$4000= $18,600.

Supporting evidence

The last tax collection sum payable by Brian could be ascertained through deducting the figure

acquired in the fifth step from the credit incidental advantages built up in the initial step. Along

these lines,

Last assessment sum = $46,500-$18,600= $27,900.

Conclusion

At the end of the time of the termination period of the advance if the interest is paid, then the

considered period is assessed from the occurrence when the intrigue is payable. Despite what

might be expected, if the intrigue is paid in regularly scheduled payments, then the regarded

period is assessed from the time when the installment of interests begins (Lang et al., 2015).

Another case could be considered if Brian is not obliged to reimburse the enthusiasm for which

the approach for computation of net duty payable would be founded on the means portrayed

above with the supposition of a zero percent genuine loan fee.

Question 3

Introduction

In this case, the issue of taxation is detailed as follows: here a couple is involved named Jack and

his wife Jill. Jack is an architect while his wife Jill is a housewife and they have hired the money

for making a purchase of a rental property in the form of joint tenants. So for that, they have

chosen the format of a written agreement in which it is mentioned that Jack is permitted for the

The supposition at this stage depends on the factor that the intrigue would be genuine sum

payable. Third Step is about, Brian, who has contributed 40% of the credit to address his future

commitments and thus,

Tax-deductible intrigue cost = $56,500*40%= $22,600 which can be viewed as theoretical. In

the fourth Step, the genuine duty deductible intrigue cost can be computed

On the intrigue in light of the real rate of intrigue which is: $10000*40%= $4000.

In fifth Step, it’s seen that, the subtraction of genuine duty deductible intrigue cost

From the theoretical figure could be introduced as, $22,600-$4000= $18,600.

Supporting evidence

The last tax collection sum payable by Brian could be ascertained through deducting the figure

acquired in the fifth step from the credit incidental advantages built up in the initial step. Along

these lines,

Last assessment sum = $46,500-$18,600= $27,900.

Conclusion

At the end of the time of the termination period of the advance if the interest is paid, then the

considered period is assessed from the occurrence when the intrigue is payable. Despite what

might be expected, if the intrigue is paid in regularly scheduled payments, then the regarded

period is assessed from the time when the installment of interests begins (Lang et al., 2015).

Another case could be considered if Brian is not obliged to reimburse the enthusiasm for which

the approach for computation of net duty payable would be founded on the means portrayed

above with the supposition of a zero percent genuine loan fee.

Question 3

Introduction

In this case, the issue of taxation is detailed as follows: here a couple is involved named Jack and

his wife Jill. Jack is an architect while his wife Jill is a housewife and they have hired the money

for making a purchase of a rental property in the form of joint tenants. So for that, they have

chosen the format of a written agreement in which it is mentioned that Jack is permitted for the

6

10 percent of the profits gained from the entire property and Jill is permitted for the rest of the 90

percent of the profits gained on the property (Miller & Oats, 2016). It is also included in the

agreement that if a loss is generated by the property than Jack is solely responsible for the whole

100 percent of losses. But unfortunately, a loss of 10000 has incurred last year. So the issue here

is how is such kind of loss is owed for tax purposes. If the couple makes a decision of selling the

property how can a capital gain or capital loss can be interpreted.

Critical analysis

The case that is under concern includes a couple, Jack and Jill, who are tied in an assertion over

leasing a property. The basic points of interest that are to be seen here for this particular situation

refer to the dispersion of share of benefit which is 10% for Jack and 90% for Jill and in addition

the rejection of any duties regarding misfortune for Jill. The investment property portrayed a loss

of $10000 a year ago which can be ascribed as the sole duty of Jack. Jack has two potential

alternatives to address the misfortune among which the counterbalancing of misfortune from

Jack's different wellsprings of wage is one (Sadiq et al., 2012). The other arrangement could be

distinguished in conveying the misfortune forward to one more year later on until the offer of the

benefit. Then again, if the property encourages benefits then the gained sum must be

appropriated proportionately among Jack and Jill in the proportion of 1:9.

Supporting evidence

It is additionally fascinating to watch that Jack could likewise balance the loss of $10000 with

the increases from the offer of the property. Along these lines, Jill couldn't be represented any

duties concerning the ramifications of tax assessment on the procedures of the investment

property while Jack needs to accept obligations for misfortunes caused through the property.

Conclusion

From the above discussions regarding the case, it can be concluded that Jack can set off the

misfortunes of a year prior to the present year if there is some compensation connecting from the

offer on the property (Woellner et al., 2011). Likewise, if Jack does not have any pickup in the

present year, such hardship must be borne by him and Jill is free of such obligation. Hence, in

any conditions, the cost treatment can't impact Jill while Jack is under a pledge to hold up under

such setbacks in his books.

10 percent of the profits gained from the entire property and Jill is permitted for the rest of the 90

percent of the profits gained on the property (Miller & Oats, 2016). It is also included in the

agreement that if a loss is generated by the property than Jack is solely responsible for the whole

100 percent of losses. But unfortunately, a loss of 10000 has incurred last year. So the issue here

is how is such kind of loss is owed for tax purposes. If the couple makes a decision of selling the

property how can a capital gain or capital loss can be interpreted.

Critical analysis

The case that is under concern includes a couple, Jack and Jill, who are tied in an assertion over

leasing a property. The basic points of interest that are to be seen here for this particular situation

refer to the dispersion of share of benefit which is 10% for Jack and 90% for Jill and in addition

the rejection of any duties regarding misfortune for Jill. The investment property portrayed a loss

of $10000 a year ago which can be ascribed as the sole duty of Jack. Jack has two potential

alternatives to address the misfortune among which the counterbalancing of misfortune from

Jack's different wellsprings of wage is one (Sadiq et al., 2012). The other arrangement could be

distinguished in conveying the misfortune forward to one more year later on until the offer of the

benefit. Then again, if the property encourages benefits then the gained sum must be

appropriated proportionately among Jack and Jill in the proportion of 1:9.

Supporting evidence

It is additionally fascinating to watch that Jack could likewise balance the loss of $10000 with

the increases from the offer of the property. Along these lines, Jill couldn't be represented any

duties concerning the ramifications of tax assessment on the procedures of the investment

property while Jack needs to accept obligations for misfortunes caused through the property.

Conclusion

From the above discussions regarding the case, it can be concluded that Jack can set off the

misfortunes of a year prior to the present year if there is some compensation connecting from the

offer on the property (Woellner et al., 2011). Likewise, if Jack does not have any pickup in the

present year, such hardship must be borne by him and Jill is free of such obligation. Hence, in

any conditions, the cost treatment can't impact Jill while Jack is under a pledge to hold up under

such setbacks in his books.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Question 4

Introduction

At the core of the tax evasion, the principle of tax avoidance standoff can even be called as the

Web minster principle. Because of the decision taken by it is allowing the corporations and the

individuals in structuring the financial arrangements for reducing the liabilities of tax till the time

these structures are lying in the four comers of the black letter law. It states that by apparently

adopting a purposive construction method for undoing the true nature of transactions that have

been entered into with the only intention of avoiding the ones that are liable to tax legitimately.

Critical analysis

The instance of IRC v Duke of Westminster [1936] AC 1 reflected on the legitimate privilege of

a person to execute lawful means and systems to devalue their net wage toward the finish of a

year. The huge rule that can be seen from the case could be featured as takes after:

The legitimate qualification of a person to actualize key changes in bookkeeping administration

is for diminishing their aggregate wage. Appropriation of moral measures exempts a person from

an installment of extra assessments (Zhang, 2012). Utilization of lawful assets and systems for

diminishing the aggregate wage on which assessment could be ascertained bars the probabilities

of addressing by specialists, for example, the Commissioner of Inland Revenue.

Supporting evidence

In actuality, the use of these above-expressed points of reference in the cutting edge situation

could be addressed by the inductions from new case laws (Miller & Oats, 2016). The use of new

case laws proposes that an association encountering misfortunes could alter its monetary record

insights nearby discounting the settled resources as per wanted esteems.

Conclusion

In any case, it is basic for the association to embrace moral means for maintaining a strategic

distance from any punishing activity. The tenets additionally absolved the exchanges of an

association that help the operational parts of the association from addressing by legitimate

experts.

Question 4

Introduction

At the core of the tax evasion, the principle of tax avoidance standoff can even be called as the

Web minster principle. Because of the decision taken by it is allowing the corporations and the

individuals in structuring the financial arrangements for reducing the liabilities of tax till the time

these structures are lying in the four comers of the black letter law. It states that by apparently

adopting a purposive construction method for undoing the true nature of transactions that have

been entered into with the only intention of avoiding the ones that are liable to tax legitimately.

Critical analysis

The instance of IRC v Duke of Westminster [1936] AC 1 reflected on the legitimate privilege of

a person to execute lawful means and systems to devalue their net wage toward the finish of a

year. The huge rule that can be seen from the case could be featured as takes after:

The legitimate qualification of a person to actualize key changes in bookkeeping administration

is for diminishing their aggregate wage. Appropriation of moral measures exempts a person from

an installment of extra assessments (Zhang, 2012). Utilization of lawful assets and systems for

diminishing the aggregate wage on which assessment could be ascertained bars the probabilities

of addressing by specialists, for example, the Commissioner of Inland Revenue.

Supporting evidence

In actuality, the use of these above-expressed points of reference in the cutting edge situation

could be addressed by the inductions from new case laws (Miller & Oats, 2016). The use of new

case laws proposes that an association encountering misfortunes could alter its monetary record

insights nearby discounting the settled resources as per wanted esteems.

Conclusion

In any case, it is basic for the association to embrace moral means for maintaining a strategic

distance from any punishing activity. The tenets additionally absolved the exchanges of an

association that help the operational parts of the association from addressing by legitimate

experts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Question 5

Introduction

A large plot of land is owned by Bill in which space he has got many tall pine trees. So it is

expected by Bill that he will be using this land for grazing the sheep and hence he wants to clear

it off completely. It has been determined by him that a logging company is ready to pay him with

1000 dollars per day for each and every 100 meters of timber according to the amount they can

take from the land (Helminen, 2011). By not taking into consideration the capitals that are gained

and the issues of tax here it is suggested to give advice to Bill whether he is considered on the

receipts from this kind of arrangement.

Critical thinking

The case to be investigated for tax assessment in this inquiry alludes to the huge land parcel

claimed by Bill that is populated plentifully with huge pine trees. Bill means to change the real

estate parcel with the end goal of sheep brushing for which Bill procured the administrations of a

logging organization. The installment got by Bill from the logging organization demonstrates

two particular situations in which one includes the installment of a singular amount measure of

$50000 for tidying up the enormous pine trees from the property while alternate includes

repeating installments of $1000 for 100 meters of timber cleared by the logging organization.

Supporting evidence

The instance of getting a singular amount measure of $50000 could be accepted as a capital

receipt for Bill close by suggesting the reality of allocating rights to another gathering for cutting

off trees from the property (Gale et al., 2011). Another significant factor that must be considered

for the qualification of the singular amount sum for capital increases assessment can be seen in

the on-time nature of the receipt since the period required for regrowth of trees could be

generous. Hence the points of reference of capital pick up assess suggest that the singular amount

sum named capital receipt can be liable for tax collection. The second case in which Bill gets

repeating receipts suggests that the principles for capital increases charge can't be connected. The

pay got by Bill with repeating receipts would guarantee that the wage would be liable to tax

collection as indicated by typical loan fees.

Question 5

Introduction

A large plot of land is owned by Bill in which space he has got many tall pine trees. So it is

expected by Bill that he will be using this land for grazing the sheep and hence he wants to clear

it off completely. It has been determined by him that a logging company is ready to pay him with

1000 dollars per day for each and every 100 meters of timber according to the amount they can

take from the land (Helminen, 2011). By not taking into consideration the capitals that are gained

and the issues of tax here it is suggested to give advice to Bill whether he is considered on the

receipts from this kind of arrangement.

Critical thinking

The case to be investigated for tax assessment in this inquiry alludes to the huge land parcel

claimed by Bill that is populated plentifully with huge pine trees. Bill means to change the real

estate parcel with the end goal of sheep brushing for which Bill procured the administrations of a

logging organization. The installment got by Bill from the logging organization demonstrates

two particular situations in which one includes the installment of a singular amount measure of

$50000 for tidying up the enormous pine trees from the property while alternate includes

repeating installments of $1000 for 100 meters of timber cleared by the logging organization.

Supporting evidence

The instance of getting a singular amount measure of $50000 could be accepted as a capital

receipt for Bill close by suggesting the reality of allocating rights to another gathering for cutting

off trees from the property (Gale et al., 2011). Another significant factor that must be considered

for the qualification of the singular amount sum for capital increases assessment can be seen in

the on-time nature of the receipt since the period required for regrowth of trees could be

generous. Hence the points of reference of capital pick up assess suggest that the singular amount

sum named capital receipt can be liable for tax collection. The second case in which Bill gets

repeating receipts suggests that the principles for capital increases charge can't be connected. The

pay got by Bill with repeating receipts would guarantee that the wage would be liable to tax

collection as indicated by typical loan fees.

9

Conclusion

Furthermore, in charge evaluation law, when one social occasion pitches favorable position for

another get-together for an idea, the same may be seen as a capital receipt and assessable in his

grip. Instead of this, since the chief case does not attract any capital get a charge, it must be

managed under run of the mill obligation rates and not capital increments.

References

Coase, R.H., 2012. The firm, the market, and the law. University of Chicago press.

Gale, W.G., Hines, J.R. and Slemrod, J. eds., 2011. Rethinking estate and gift taxation.

Brookings Institution Press.

Hayek, F.A., 2012. Law, legislation and liberty: a new statement of the liberal principles of

justice and political economy. Routledge.

Helminen, M., 2011. EU tax law: direct taxation. IBFD.

Jördens, A., 2012. Government, Taxation, and Law. In The Oxford Handbook of Roman Egypt.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2015. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Sadiq, K., Coleman, C., Hanegbi, R., Hart, G., Jogarajan, S., Krever, R., McLaren, J., Obst, W.

and Ting, A., 2012. Principles of taxation law 2012. Thomson Reuters.

Conclusion

Furthermore, in charge evaluation law, when one social occasion pitches favorable position for

another get-together for an idea, the same may be seen as a capital receipt and assessable in his

grip. Instead of this, since the chief case does not attract any capital get a charge, it must be

managed under run of the mill obligation rates and not capital increments.

References

Coase, R.H., 2012. The firm, the market, and the law. University of Chicago press.

Gale, W.G., Hines, J.R. and Slemrod, J. eds., 2011. Rethinking estate and gift taxation.

Brookings Institution Press.

Hayek, F.A., 2012. Law, legislation and liberty: a new statement of the liberal principles of

justice and political economy. Routledge.

Helminen, M., 2011. EU tax law: direct taxation. IBFD.

Jördens, A., 2012. Government, Taxation, and Law. In The Oxford Handbook of Roman Egypt.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2015. Introduction to European tax law

on direct taxation. Linde Verlag GmbH.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Sadiq, K., Coleman, C., Hanegbi, R., Hart, G., Jogarajan, S., Krever, R., McLaren, J., Obst, W.

and Ting, A., 2012. Principles of taxation law 2012. Thomson Reuters.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2011. Australian Taxation Law

Select: legislation and commentary. CCH Australia.

Zhang, S.W., 2012. Theories of taxation law.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2011. Australian Taxation Law

Select: legislation and commentary. CCH Australia.

Zhang, S.W., 2012. Theories of taxation law.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.