Taxation Law Assignment: Analysis of Taxable Income and Deductions

VerifiedAdded on 2020/03/02

|12

|1894

|41

Homework Assignment

AI Summary

This taxation law assignment provides detailed solutions to four key questions, covering various aspects of Australian taxation. Question 1 analyzes four different scenarios related to allowable deductions under section 8-1 of the Income Tax Assessment Act 1997 (ITAA 1997), addressing issues such as moving machinery costs, asset revaluation, legal expenses for winding up a company, and legal expenses for business functions. Question 2 focuses on claiming input tax credits for advertising expenses under the Goods and Services Tax Ruling (GSTR) Act 1999, specifically referencing GSTR 2006/3 and the case of Ronpibon Tin NL v. FC of T. Question 3 delves into the computation of a foreign tax offset for an individual, including the calculation of assessable income, tax payable, and tax credits for income sourced from different countries (Australia, the United States, and the United Kingdom). Question 4 focuses on the computation of net income from a partnership, detailing the calculation of assessable income, allowable deductions, and the resulting net income. The assignment includes relevant legislation, case references, and detailed calculations to support the solutions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Question 1:.................................................................................................................................3

Answer to scenario 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to Scenario 2:................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Answer to Scenario 3:................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to Scenario 4:................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Table of Contents

Question 1:.................................................................................................................................3

Answer to scenario 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to Scenario 2:................................................................................................................3

Issue:..........................................................................................................................................3

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................4

Answer to Scenario 3:................................................................................................................4

Issue:..........................................................................................................................................4

Legislation:.................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to Scenario 4:................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

2TAXATION LAW

Conclusion:................................................................................................................................5

Question 2:.................................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer to question 4:.................................................................................................................9

Reference List:.........................................................................................................................11

Conclusion:................................................................................................................................5

Question 2:.................................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer to question 4:.................................................................................................................9

Reference List:.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Question 1:

Answer to scenario 1:

Issue:

The present issue determines whether the allowable deductions will be allowed for the

cost of moving machinery to a new site.

Legislation:

a. British Insulated & Helsby Cables

b. Section 8-1 of the Income Tax Assessment Act 1997

Application:

The cost of moving the machinery to new site is considered as capital and no

deductions will be allowable under 8-1 of the Income Tax Assessment Act 1997. Citing the

reference of British Insulated & Helsby Cables the transportation cost is referred as the

enduring advantage on business premises by moving the depreciable asset. Therefore, the

cost involved in moving the mercenary to a new site is not allowable for deductions.

Conclusion:

To conclude with, moving of fixed asset represents an increase in the cost of item for

depreciation and cannot be allowed for deductions under section 8-1 of the ITAA 1997.

Answer to Scenario 2:

Issue:

The issue determines whether the revaluation of asset to the effect of insurance shall

be allowed as deductions under section 8-1 of the Income Tax Assessment Act 1997.

Question 1:

Answer to scenario 1:

Issue:

The present issue determines whether the allowable deductions will be allowed for the

cost of moving machinery to a new site.

Legislation:

a. British Insulated & Helsby Cables

b. Section 8-1 of the Income Tax Assessment Act 1997

Application:

The cost of moving the machinery to new site is considered as capital and no

deductions will be allowable under 8-1 of the Income Tax Assessment Act 1997. Citing the

reference of British Insulated & Helsby Cables the transportation cost is referred as the

enduring advantage on business premises by moving the depreciable asset. Therefore, the

cost involved in moving the mercenary to a new site is not allowable for deductions.

Conclusion:

To conclude with, moving of fixed asset represents an increase in the cost of item for

depreciation and cannot be allowed for deductions under section 8-1 of the ITAA 1997.

Answer to Scenario 2:

Issue:

The issue determines whether the revaluation of asset to the effect of insurance shall

be allowed as deductions under section 8-1 of the Income Tax Assessment Act 1997.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Legislation:

a. Section 8-1 of the Income Tax Assessment Act 1997

Application:

In the existing situation cost of revaluating asset in respect of the insurance cover are

probably incurred as recurring in nature and deductions will be allowable under section 8-1 of

the ITAA 1997.

Conclusion:

The expenditure incurred will be considered allowable for deductions because they

are recurring in nature and meets the criterion of deduction under section 8-1 of the ITAA

1997.

Answer to Scenario 3:

Issue:

The existing issue determines whether any allowable deductions is available for

expenses occurred on opposing a petition for winding up of a company under section 8-1 of

the ITAA 1997.

Legislation:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application:

Legal cost is usually considered as deductible if it is occurred in the act of deriving

the taxable income. As held in FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

expenses that are unusual and the taxpayer on previous circumstances has not incurred the

same such expenses are not prevented from deductions. With reference to section 8-1 of the

Legislation:

a. Section 8-1 of the Income Tax Assessment Act 1997

Application:

In the existing situation cost of revaluating asset in respect of the insurance cover are

probably incurred as recurring in nature and deductions will be allowable under section 8-1 of

the ITAA 1997.

Conclusion:

The expenditure incurred will be considered allowable for deductions because they

are recurring in nature and meets the criterion of deduction under section 8-1 of the ITAA

1997.

Answer to Scenario 3:

Issue:

The existing issue determines whether any allowable deductions is available for

expenses occurred on opposing a petition for winding up of a company under section 8-1 of

the ITAA 1997.

Legislation:

a. Section 8-1 of the Income Tax Assessment Act 1997

b. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application:

Legal cost is usually considered as deductible if it is occurred in the act of deriving

the taxable income. As held in FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

expenses that are unusual and the taxpayer on previous circumstances has not incurred the

same such expenses are not prevented from deductions. With reference to section 8-1 of the

5TAXATION LAW

ITAA 1997 legal expenses for winding up of a business will not be regarded for deductions

because they are not incurred for carrying the business activities.

Conclusion:

To conclude with, the cost of opposing the petition for winding up the company

would be considered as non-allowable deductions under section 8-1 of the ITAA 1997.

Answer to Scenario 4:

Issue:

The present scenario is associated with determining whether the legal expenses

occurred for service of a solicitor in business functions will be regarded as allowable

deductions under section 8-1 of the ITAA 1997.

Legislation:

a. section 8-1 of the Income Tax Assessment Act 1997

Application:

In conformity with the section 8-1 of the Income Tax Assessment Act 1997, when the

expense is occurred for deriving business income will be considered as allowable deductions.

In the current scenario, it is understood that the legal expenditure have an association with

business in producing the assessable income and would be regarded for allowable deductions.

Conclusion:

Legal fee occurred for generating the business income shall be regarded as allowable

deductions in respect of section 8-1 of the ITAA 1997.

ITAA 1997 legal expenses for winding up of a business will not be regarded for deductions

because they are not incurred for carrying the business activities.

Conclusion:

To conclude with, the cost of opposing the petition for winding up the company

would be considered as non-allowable deductions under section 8-1 of the ITAA 1997.

Answer to Scenario 4:

Issue:

The present scenario is associated with determining whether the legal expenses

occurred for service of a solicitor in business functions will be regarded as allowable

deductions under section 8-1 of the ITAA 1997.

Legislation:

a. section 8-1 of the Income Tax Assessment Act 1997

Application:

In conformity with the section 8-1 of the Income Tax Assessment Act 1997, when the

expense is occurred for deriving business income will be considered as allowable deductions.

In the current scenario, it is understood that the legal expenditure have an association with

business in producing the assessable income and would be regarded for allowable deductions.

Conclusion:

Legal fee occurred for generating the business income shall be regarded as allowable

deductions in respect of section 8-1 of the ITAA 1997.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Question 2:

Issue:

The current issue is associated with claiming input tax credit for the advertising

expenses incurred under the GSTR Act 1999.

Legislation:

a. Goods and Service taxation ruling of GSTR 2006/3

b. Ronpibon Tin NL v. FC of T

c. GSTR Act 1999

Application:

As per the Goods and Service taxation ruling of GSTR 2006/3, guidance has been

provided on the method to arrive at the input tax credits and adjustment for any form of

change in use by the monetary supplies under the Tax System of Goods and Service Act

1999. From the present case study it is understood that Big Bank Ltd has incurred an expense

of $1,650,000 that was inclusive of GST on advertising. In the existing scenario of Big Bank

Ltd Goods and Service taxation ruling of GSTR 2006/3 is relevant or necessary for

registration. As Big Bank Ltd made the financial supplies that were beyond the financial

threshold limit of financial acquisition, it will be eligible for input tax credits. If an entity is

registered under the GST Act 1999, GST will be payable by the entity on the taxable supplies

made by it.

As held in Ronpibon Tin NL v. FC of T the guiding principle of “extent” and “to the

extent” is applicable in the interpretation of GST legislation. This consists of the requirement

where the apportionment methodology has been undertaken to be fair and reasonable in the

present context of Big Bank Ltd.

Question 2:

Issue:

The current issue is associated with claiming input tax credit for the advertising

expenses incurred under the GSTR Act 1999.

Legislation:

a. Goods and Service taxation ruling of GSTR 2006/3

b. Ronpibon Tin NL v. FC of T

c. GSTR Act 1999

Application:

As per the Goods and Service taxation ruling of GSTR 2006/3, guidance has been

provided on the method to arrive at the input tax credits and adjustment for any form of

change in use by the monetary supplies under the Tax System of Goods and Service Act

1999. From the present case study it is understood that Big Bank Ltd has incurred an expense

of $1,650,000 that was inclusive of GST on advertising. In the existing scenario of Big Bank

Ltd Goods and Service taxation ruling of GSTR 2006/3 is relevant or necessary for

registration. As Big Bank Ltd made the financial supplies that were beyond the financial

threshold limit of financial acquisition, it will be eligible for input tax credits. If an entity is

registered under the GST Act 1999, GST will be payable by the entity on the taxable supplies

made by it.

As held in Ronpibon Tin NL v. FC of T the guiding principle of “extent” and “to the

extent” is applicable in the interpretation of GST legislation. This consists of the requirement

where the apportionment methodology has been undertaken to be fair and reasonable in the

present context of Big Bank Ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

As stated under section 11-15 or 15-10 an importation consideration is that if an

entity makes creditable supplies for input tax credit it will be considered creditable. Big Bank

Ltd incurred advertising expenditure for purpose of creditable acquisition. Therefore, in

compliance with the GSTR ruling of 2006/3 Big Bank Ltd made the acquisition of supplies

that was greater than the threshold limit of financial acquisition. Therefore, Big Bank Ltd

would be considered eligible for input tax credit for the GST supplies made.

Conclusion:

To conclude with, it can be said that Big Bank Ltd shall be considered for input tax

credit under the GSTR 2006/13 for the advertising expenses occurred for the purpose of

creditable acquisition.

As stated under section 11-15 or 15-10 an importation consideration is that if an

entity makes creditable supplies for input tax credit it will be considered creditable. Big Bank

Ltd incurred advertising expenditure for purpose of creditable acquisition. Therefore, in

compliance with the GSTR ruling of 2006/3 Big Bank Ltd made the acquisition of supplies

that was greater than the threshold limit of financial acquisition. Therefore, Big Bank Ltd

would be considered eligible for input tax credit for the GST supplies made.

Conclusion:

To conclude with, it can be said that Big Bank Ltd shall be considered for input tax

credit under the GSTR 2006/13 for the advertising expenses occurred for the purpose of

creditable acquisition.

8TAXATION LAW

Answer to question 3:

Determination of Angelo’s Foreign Tax Offset

Computation of Foreign Tax Offset For Angelo

Assessable Income

Amount

($)

Amount

($)

Gross Income

Employment income from Australia 44000

Employment income from United States 12000

Employment income from United Kingdom 8000

Rental income from property in United Kingdom 2000

Dividend income from United Kingdom 1200

Interest income from United Kingdom 800

Total Taxable Income 68000

Tax on Taxable Income 13647

Medicare Levy 1360

Less: Tax Offset for Medical Expenses 750

(5000-1250)

Total Tax Payable 14257

Average rate of tax payable on Angelo Taxable Income (%) 21.0

(14257/68000)*100

Net Foreign Income From Each Class

Foreign Rental Income 2000

Less: Expenses incurred in Deriving 500 1500

Gross foreign dividend income 1200

Gross Interest income from United Kingdom 800

Net passive foreign income 3500

Other Foreign Income

Gross Employment income from United States 12000

Less: Expenses incurred in deriving employment income from

United States 900 11100

Gross Employment income from United Kingdom 8000

Less: Expenses incurred in deriving employment income from

United Kingdom 500 7500

Net Other Foreign Income 18600

ANFI for each Class

Answer to question 3:

Determination of Angelo’s Foreign Tax Offset

Computation of Foreign Tax Offset For Angelo

Assessable Income

Amount

($)

Amount

($)

Gross Income

Employment income from Australia 44000

Employment income from United States 12000

Employment income from United Kingdom 8000

Rental income from property in United Kingdom 2000

Dividend income from United Kingdom 1200

Interest income from United Kingdom 800

Total Taxable Income 68000

Tax on Taxable Income 13647

Medicare Levy 1360

Less: Tax Offset for Medical Expenses 750

(5000-1250)

Total Tax Payable 14257

Average rate of tax payable on Angelo Taxable Income (%) 21.0

(14257/68000)*100

Net Foreign Income From Each Class

Foreign Rental Income 2000

Less: Expenses incurred in Deriving 500 1500

Gross foreign dividend income 1200

Gross Interest income from United Kingdom 800

Net passive foreign income 3500

Other Foreign Income

Gross Employment income from United States 12000

Less: Expenses incurred in deriving employment income from

United States 900 11100

Gross Employment income from United Kingdom 8000

Less: Expenses incurred in deriving employment income from

United Kingdom 500 7500

Net Other Foreign Income 18600

ANFI for each Class

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

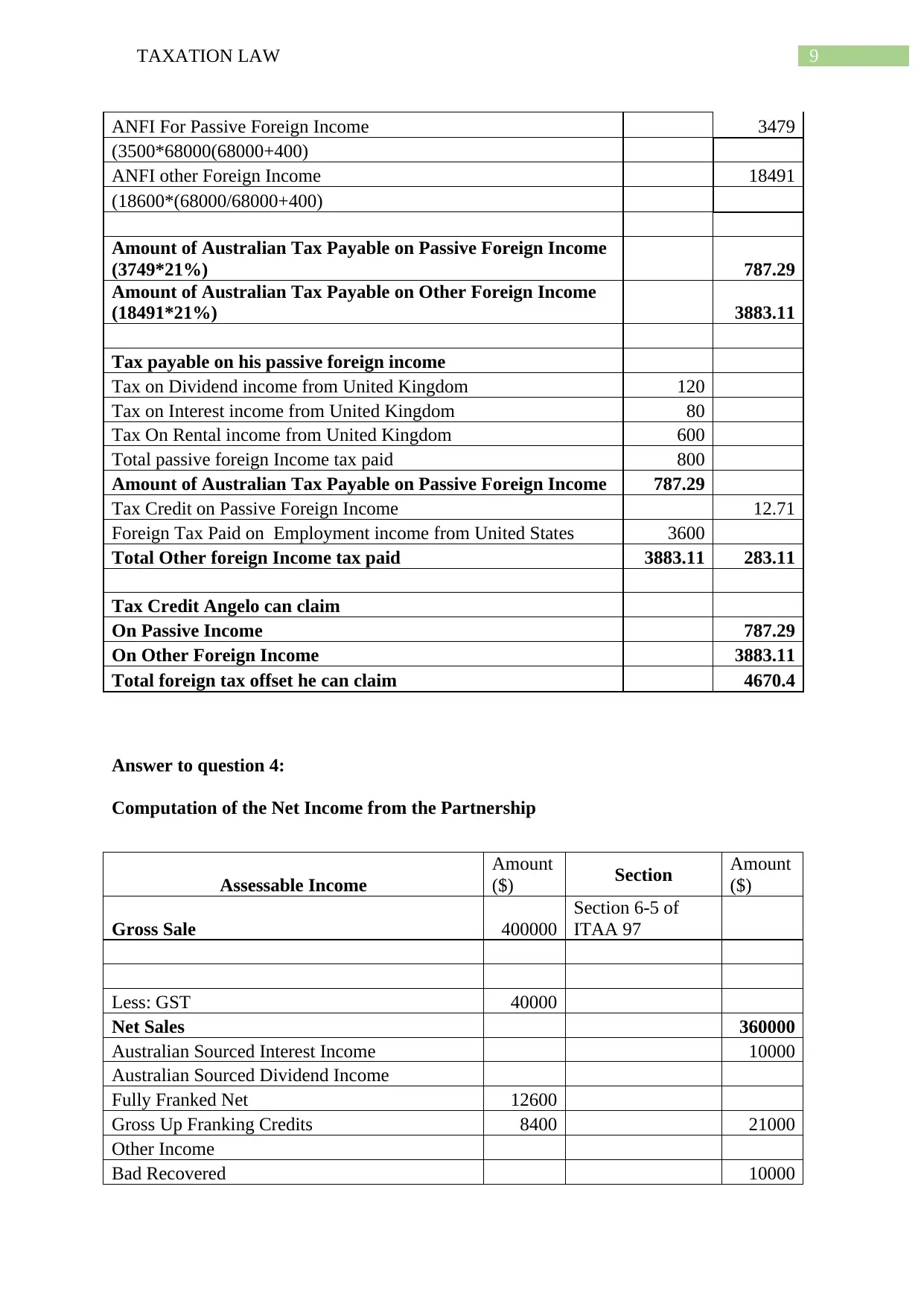

9TAXATION LAW

ANFI For Passive Foreign Income 3479

(3500*68000(68000+400)

ANFI other Foreign Income 18491

(18600*(68000/68000+400)

Amount of Australian Tax Payable on Passive Foreign Income

(3749*21%) 787.29

Amount of Australian Tax Payable on Other Foreign Income

(18491*21%) 3883.11

Tax payable on his passive foreign income

Tax on Dividend income from United Kingdom 120

Tax on Interest income from United Kingdom 80

Tax On Rental income from United Kingdom 600

Total passive foreign Income tax paid 800

Amount of Australian Tax Payable on Passive Foreign Income 787.29

Tax Credit on Passive Foreign Income 12.71

Foreign Tax Paid on Employment income from United States 3600

Total Other foreign Income tax paid 3883.11 283.11

Tax Credit Angelo can claim

On Passive Income 787.29

On Other Foreign Income 3883.11

Total foreign tax offset he can claim 4670.4

Answer to question 4:

Computation of the Net Income from the Partnership

Assessable Income

Amount

($) Section Amount

($)

Gross Sale 400000

Section 6-5 of

ITAA 97

Less: GST 40000

Net Sales 360000

Australian Sourced Interest Income 10000

Australian Sourced Dividend Income

Fully Franked Net 12600

Gross Up Franking Credits 8400 21000

Other Income

Bad Recovered 10000

ANFI For Passive Foreign Income 3479

(3500*68000(68000+400)

ANFI other Foreign Income 18491

(18600*(68000/68000+400)

Amount of Australian Tax Payable on Passive Foreign Income

(3749*21%) 787.29

Amount of Australian Tax Payable on Other Foreign Income

(18491*21%) 3883.11

Tax payable on his passive foreign income

Tax on Dividend income from United Kingdom 120

Tax on Interest income from United Kingdom 80

Tax On Rental income from United Kingdom 600

Total passive foreign Income tax paid 800

Amount of Australian Tax Payable on Passive Foreign Income 787.29

Tax Credit on Passive Foreign Income 12.71

Foreign Tax Paid on Employment income from United States 3600

Total Other foreign Income tax paid 3883.11 283.11

Tax Credit Angelo can claim

On Passive Income 787.29

On Other Foreign Income 3883.11

Total foreign tax offset he can claim 4670.4

Answer to question 4:

Computation of the Net Income from the Partnership

Assessable Income

Amount

($) Section Amount

($)

Gross Sale 400000

Section 6-5 of

ITAA 97

Less: GST 40000

Net Sales 360000

Australian Sourced Interest Income 10000

Australian Sourced Dividend Income

Fully Franked Net 12600

Gross Up Franking Credits 8400 21000

Other Income

Bad Recovered 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

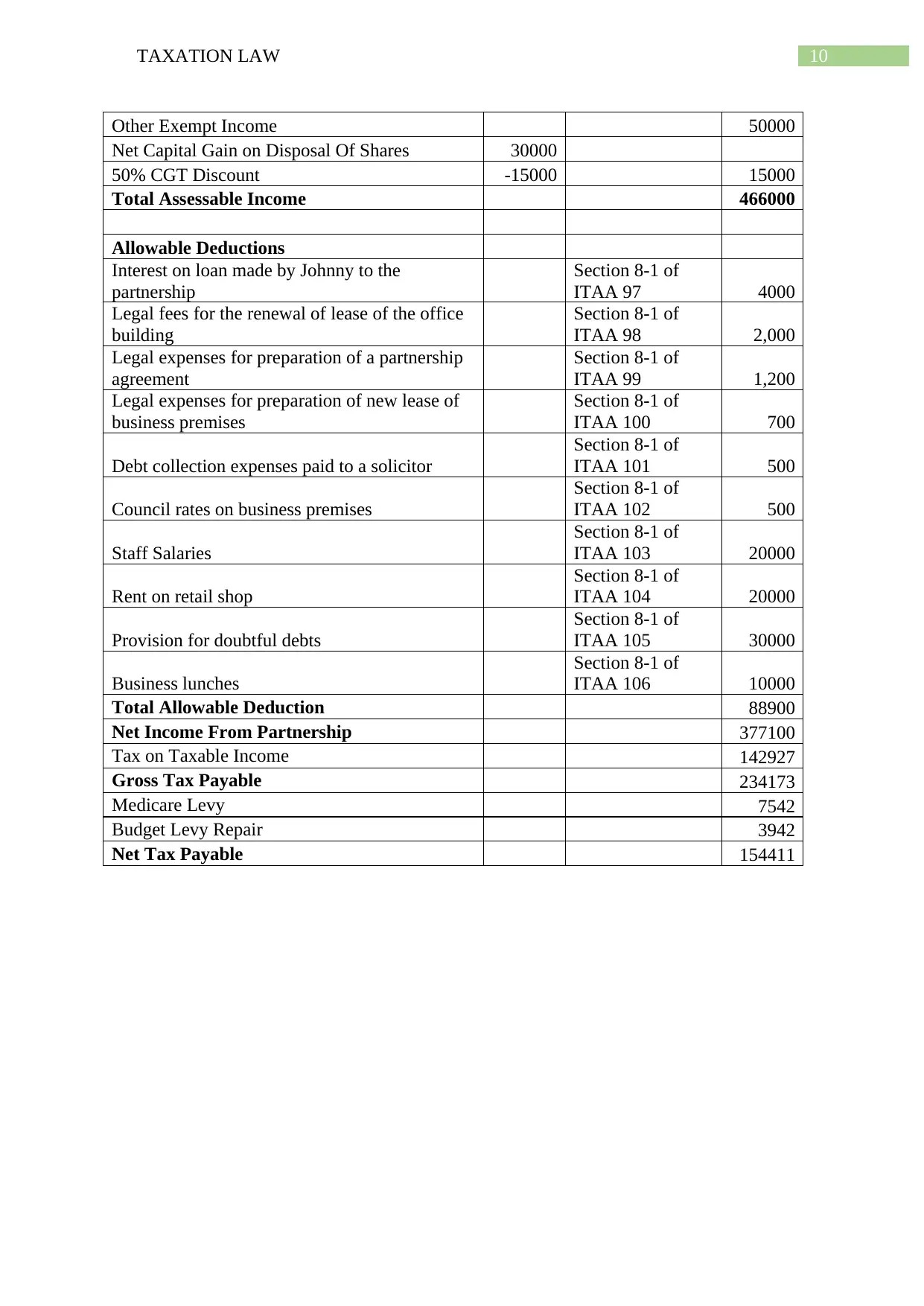

10TAXATION LAW

Other Exempt Income 50000

Net Capital Gain on Disposal Of Shares 30000

50% CGT Discount -15000 15000

Total Assessable Income 466000

Allowable Deductions

Interest on loan made by Johnny to the

partnership

Section 8-1 of

ITAA 97 4000

Legal fees for the renewal of lease of the office

building

Section 8-1 of

ITAA 98 2,000

Legal expenses for preparation of a partnership

agreement

Section 8-1 of

ITAA 99 1,200

Legal expenses for preparation of new lease of

business premises

Section 8-1 of

ITAA 100 700

Debt collection expenses paid to a solicitor

Section 8-1 of

ITAA 101 500

Council rates on business premises

Section 8-1 of

ITAA 102 500

Staff Salaries

Section 8-1 of

ITAA 103 20000

Rent on retail shop

Section 8-1 of

ITAA 104 20000

Provision for doubtful debts

Section 8-1 of

ITAA 105 30000

Business lunches

Section 8-1 of

ITAA 106 10000

Total Allowable Deduction 88900

Net Income From Partnership 377100

Tax on Taxable Income 142927

Gross Tax Payable 234173

Medicare Levy 7542

Budget Levy Repair 3942

Net Tax Payable 154411

Other Exempt Income 50000

Net Capital Gain on Disposal Of Shares 30000

50% CGT Discount -15000 15000

Total Assessable Income 466000

Allowable Deductions

Interest on loan made by Johnny to the

partnership

Section 8-1 of

ITAA 97 4000

Legal fees for the renewal of lease of the office

building

Section 8-1 of

ITAA 98 2,000

Legal expenses for preparation of a partnership

agreement

Section 8-1 of

ITAA 99 1,200

Legal expenses for preparation of new lease of

business premises

Section 8-1 of

ITAA 100 700

Debt collection expenses paid to a solicitor

Section 8-1 of

ITAA 101 500

Council rates on business premises

Section 8-1 of

ITAA 102 500

Staff Salaries

Section 8-1 of

ITAA 103 20000

Rent on retail shop

Section 8-1 of

ITAA 104 20000

Provision for doubtful debts

Section 8-1 of

ITAA 105 30000

Business lunches

Section 8-1 of

ITAA 106 10000

Total Allowable Deduction 88900

Net Income From Partnership 377100

Tax on Taxable Income 142927

Gross Tax Payable 234173

Medicare Levy 7542

Budget Levy Repair 3942

Net Tax Payable 154411

11TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2014. Concepts in Federal Taxation 2015. Cengage

Learning.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Tran-Nam, B., Evans, C. and Lignier, P., 2014. Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F., 29, p.137.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2014. Concepts in Federal Taxation 2015. Cengage

Learning.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Tran-Nam, B., Evans, C. and Lignier, P., 2014. Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F., 29, p.137.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.