Taxation Law Assignment: Deductions, GST and Taxable Income

VerifiedAdded on 2020/03/28

|13

|1825

|447

Homework Assignment

AI Summary

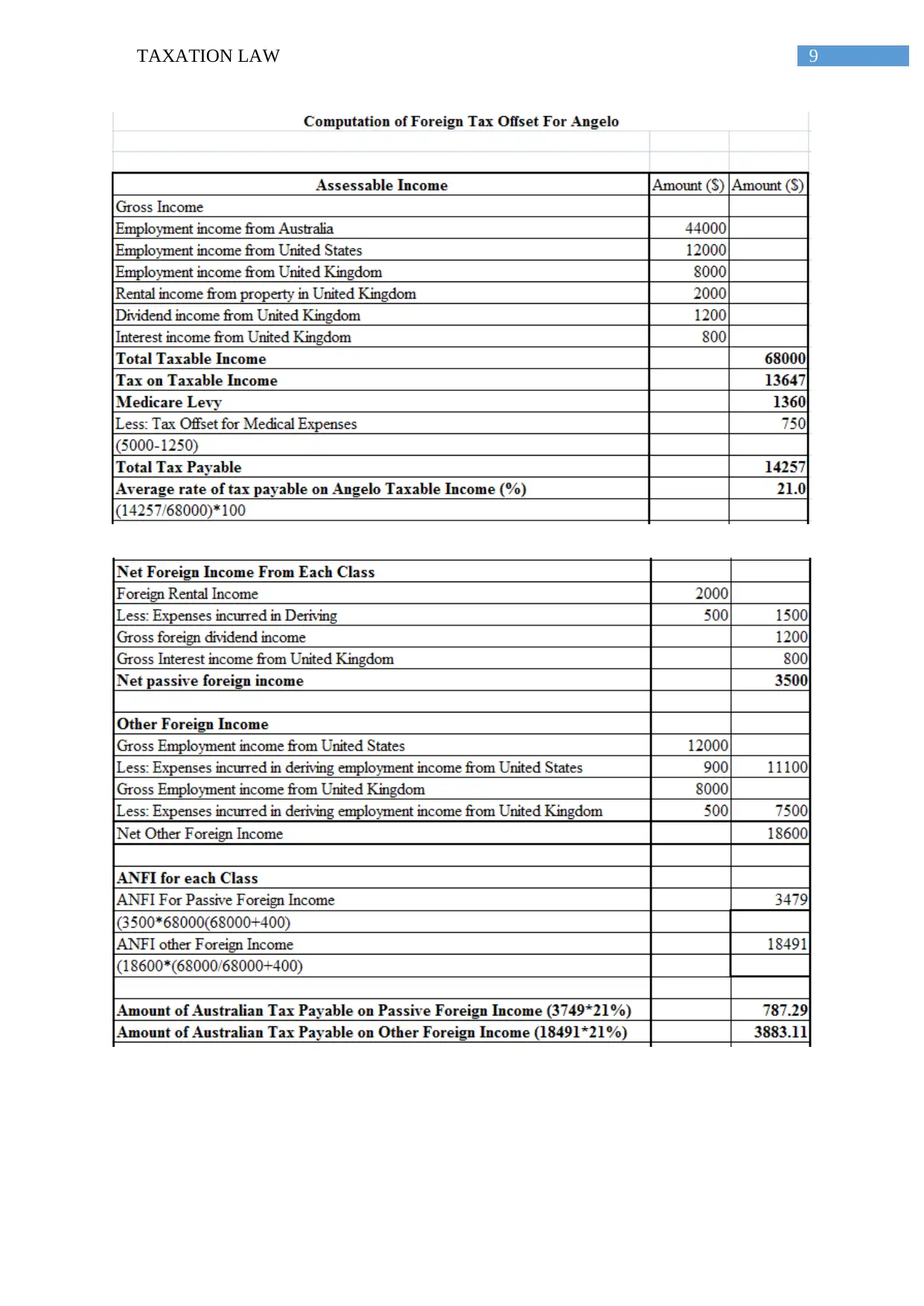

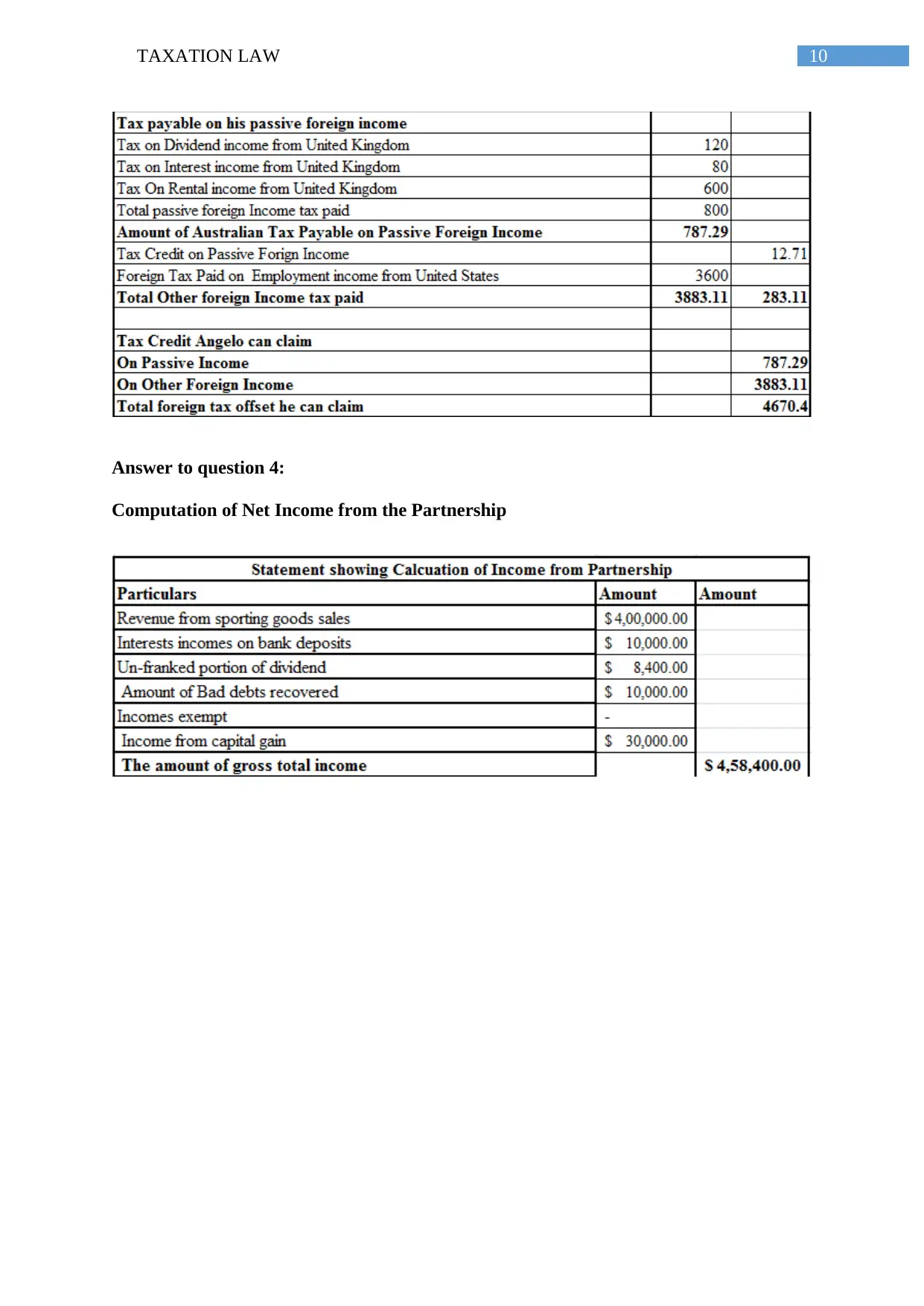

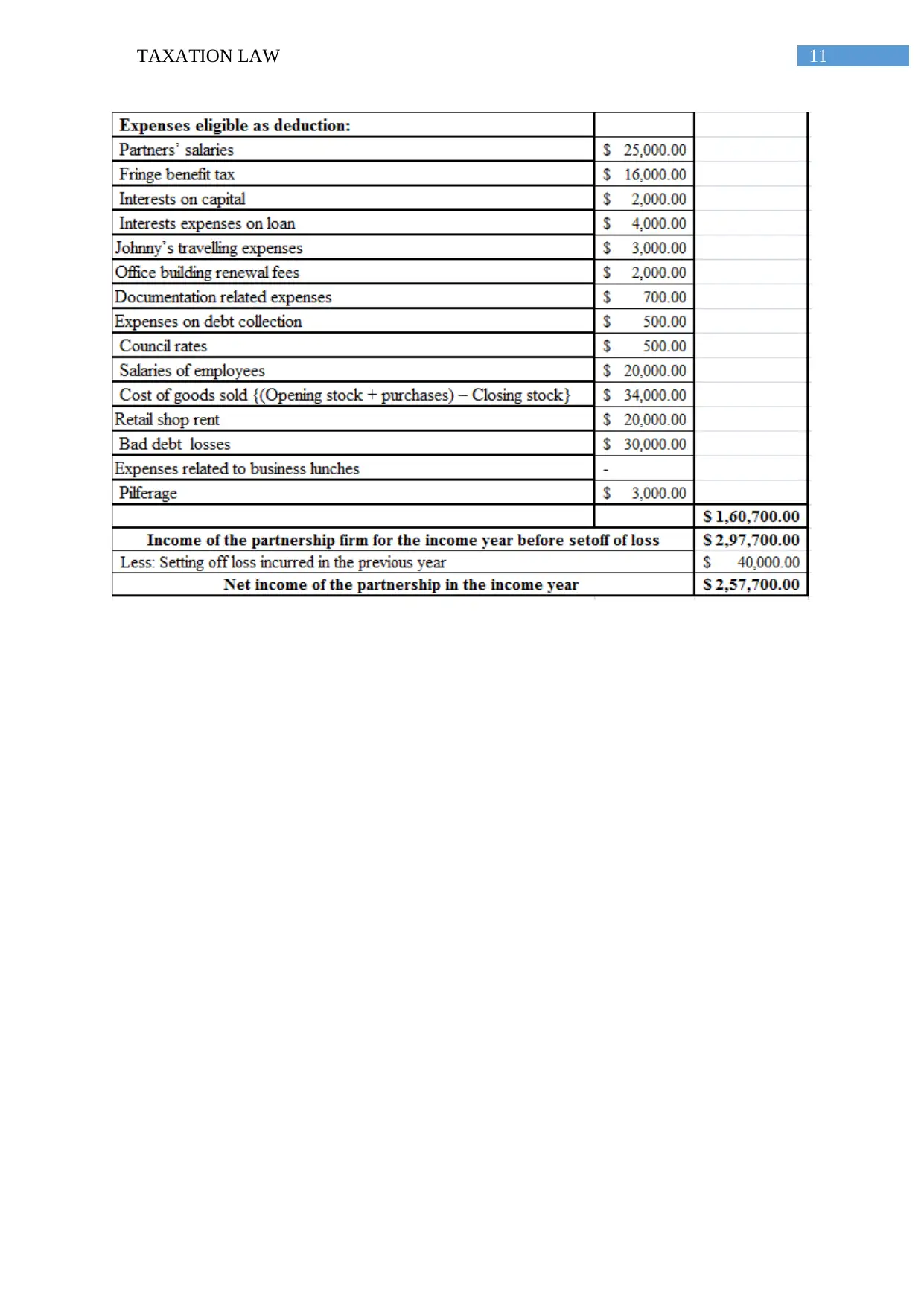

This taxation law assignment provides a comprehensive analysis of several key areas within Australian taxation law. The assignment begins by examining allowable deductions, referencing relevant legislation such as the ITAA 1997 and case law, including British Insulated & Helsby Cables and taxation rulings. It explores the deductibility of expenses related to moving machinery, asset revaluation for insurance, legal expenditures for opposing winding up petitions, and solicitor services. The assignment further delves into Goods and Services Tax (GST), analyzing input tax credits and the application of GST rulings, particularly GSTR 2006/3, within the context of the GST Act 1999. The solution includes a computation of Angelo's taxable income and net income from a partnership, providing a practical application of the taxation principles discussed. The analysis incorporates relevant case law and rulings to support the conclusions on each issue.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.