Taxation Law Assignment - University Name, LAWS20060

VerifiedAdded on 2022/11/30

|17

|3897

|310

Homework Assignment

AI Summary

This taxation law assignment provides comprehensive answers to several questions related to Australian taxation law. The assignment covers various aspects, including tax deductions under section 8-1 of the ITAA 1997, capital gains tax (CGT) events like CGT event B1 and F2, and the application of CGT discounts. The solution analyzes scenarios involving ordinary income, such as prizes and reimbursed expenses, and explores the deductibility of different types of expenses. The assignment references relevant sections of the ITAA 1997, case laws like Amalgamated Zinc Ltd v FCT, and tax rulings to support its arguments. The assignment also includes calculations of capital gains and losses, and the application of the main residence exemption. The document is a student submission providing detailed explanations and legal analysis of taxation principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................5

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................6

Answer E:...............................................................................................................................7

Answer to question 3:.................................................................................................................7

Answer A:..............................................................................................................................7

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................5

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................6

Answer E:...............................................................................................................................7

Answer to question 3:.................................................................................................................7

Answer A:..............................................................................................................................7

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................8

2TAXATION LAW

Answer D:..............................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................10

Answer D:............................................................................................................................11

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................12

Application:..........................................................................................................................13

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

Answer D:..............................................................................................................................9

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................10

Answer D:............................................................................................................................11

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................12

Application:..........................................................................................................................13

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer to A:

A vital topic involving the valuable life of the depreciating asset under “section 40-

100, ITAA 1997” is talked over under the Taxation ruling of TR 2018/14.

Answer B:

A taxpayer is allowed to claim tax offset under the “Division 13 of the ITAA 1997”.

Answer C:

For the year 2018/18 the uppermost extent of tax rate which is applicable on the

resident of Australia amounts to 54,097 + 45c for each $1 above $180,000.

Answer D:

As per “Section 108-20 (2)” the private usage or the personal use asset includes

anything that is held by a person for their own enjoyment purpose1. But it must be noted that

the capital gains made from the private use assets having a purchase cost of less than $10,000

or less is not counted in for taxation purpose under the legislative provision of “section 118-

10 (3), ITAA 1997”.

Answer E:

Agreeing with “section 104-15 (1) of the ITAA 1997” a CGT event B1 takes place when

the taxpayers arranges a contract with another entity on the below stated conditions that2;

a. The right relating to the use of CGT asset under the ownership of a person is given

another entity

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

Answer to question 1:

Answer to A:

A vital topic involving the valuable life of the depreciating asset under “section 40-

100, ITAA 1997” is talked over under the Taxation ruling of TR 2018/14.

Answer B:

A taxpayer is allowed to claim tax offset under the “Division 13 of the ITAA 1997”.

Answer C:

For the year 2018/18 the uppermost extent of tax rate which is applicable on the

resident of Australia amounts to 54,097 + 45c for each $1 above $180,000.

Answer D:

As per “Section 108-20 (2)” the private usage or the personal use asset includes

anything that is held by a person for their own enjoyment purpose1. But it must be noted that

the capital gains made from the private use assets having a purchase cost of less than $10,000

or less is not counted in for taxation purpose under the legislative provision of “section 118-

10 (3), ITAA 1997”.

Answer E:

Agreeing with “section 104-15 (1) of the ITAA 1997” a CGT event B1 takes place when

the taxpayers arranges a contract with another entity on the below stated conditions that2;

a. The right relating to the use of CGT asset under the ownership of a person is given

another entity

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

b. It takes into the account the title which is existent in the asset may pass to some other

entity before the end of contract.

Answer F:

The formula that is given in “section 4-10 (3), ITAA 1997” primarily explains the

method of calculating the total sum of tax that is payable. The formula includes

Income tax = {Taxable Income x Rate} – Tax Offsets

Answer G:

The federal commissioner’s pronouncement in the case of “FC of T v Day 2008 ATC

20-064” stated that the taxpayer was the public servant and a request involving the deduction

of legal outgoings that was sustained by the taxpayer on account of a number of charges that

was bought against him was non-deductible under the “section 8-1, ITAA 1997”3. This is

because the charges against the taxpayer was chiefly for his own concerns and the legal

expense was non-allowable deduction.

Answer H:

Marginal tax and average tax rate differences are given below;

a. The marginal tax is generally paid on the supplementary amount of earnings. The

average tax commonly involves the payment of tax as the percentage of a person

assessable earnings4.

b. It must be noted that average tax includes total summation of tax divided by overall

income. The marginal tax on the other hand take into account the rising volume of tax

which is paid due to the rise in the income.

3 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

4 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

b. It takes into the account the title which is existent in the asset may pass to some other

entity before the end of contract.

Answer F:

The formula that is given in “section 4-10 (3), ITAA 1997” primarily explains the

method of calculating the total sum of tax that is payable. The formula includes

Income tax = {Taxable Income x Rate} – Tax Offsets

Answer G:

The federal commissioner’s pronouncement in the case of “FC of T v Day 2008 ATC

20-064” stated that the taxpayer was the public servant and a request involving the deduction

of legal outgoings that was sustained by the taxpayer on account of a number of charges that

was bought against him was non-deductible under the “section 8-1, ITAA 1997”3. This is

because the charges against the taxpayer was chiefly for his own concerns and the legal

expense was non-allowable deduction.

Answer H:

Marginal tax and average tax rate differences are given below;

a. The marginal tax is generally paid on the supplementary amount of earnings. The

average tax commonly involves the payment of tax as the percentage of a person

assessable earnings4.

b. It must be noted that average tax includes total summation of tax divided by overall

income. The marginal tax on the other hand take into account the rising volume of tax

which is paid due to the rise in the income.

3 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

4 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

5TAXATION LAW

Answer I:

Consumption tax is better understood as the tax that is imposed on the consumption

expenditure on products and services. The tax base of such kind of tax involves the amount of

money that is spend on the consumption. These taxes are generally indirect tax namely the

sales and value added tax.

Answer to question 2:

Answer A:

The taxpayers under “section 8-1 (1))” is permitted to deduct from their calculable

income the outlays up to the point that has arisen in gaining the assessable income. The law

court in “Amalgamated Zinc Ltd v FCT (1935)” stated that deduction is allowed for outlays

that are incurred while producing assessable income5.

The interest that is occurred by Brett against the loan taken to pay the worker wages

should be seen as outgoing that is arisen in producing the taxable income. Referring to

“Amalgamated Zinc Ltd v FCT (1935)” deduction for interest on loan can be obtained by

Brett under “section 8-1, ITAA 1997”.

Answer B:

A loss or outgoing is considered deductible up to the magnitude that it meets either

positive limbs of “section 8-1, ITAA 1997”, or it fails to satisfy any one of the negative

limbs. The court in “Ronpibon Tin v FCT (1949)” considered the apportionment of outlay

that possess dual purpose. Expenses that are both personal and work purpose then only

deduction for work purpose is acceptable6.

5 Krever, Richard E, Australian Taxation Law Cases 2014

6 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

Answer I:

Consumption tax is better understood as the tax that is imposed on the consumption

expenditure on products and services. The tax base of such kind of tax involves the amount of

money that is spend on the consumption. These taxes are generally indirect tax namely the

sales and value added tax.

Answer to question 2:

Answer A:

The taxpayers under “section 8-1 (1))” is permitted to deduct from their calculable

income the outlays up to the point that has arisen in gaining the assessable income. The law

court in “Amalgamated Zinc Ltd v FCT (1935)” stated that deduction is allowed for outlays

that are incurred while producing assessable income5.

The interest that is occurred by Brett against the loan taken to pay the worker wages

should be seen as outgoing that is arisen in producing the taxable income. Referring to

“Amalgamated Zinc Ltd v FCT (1935)” deduction for interest on loan can be obtained by

Brett under “section 8-1, ITAA 1997”.

Answer B:

A loss or outgoing is considered deductible up to the magnitude that it meets either

positive limbs of “section 8-1, ITAA 1997”, or it fails to satisfy any one of the negative

limbs. The court in “Ronpibon Tin v FCT (1949)” considered the apportionment of outlay

that possess dual purpose. Expenses that are both personal and work purpose then only

deduction for work purpose is acceptable6.

5 Krever, Richard E, Australian Taxation Law Cases 2014

6 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Julie occurred a mobile phone costs of $500 where 60% of the calls were work-

related. Referring to “Ronpibon Tin v FCT (1949)” the expenses hold dual purpose and only

deduction for work-related calls will be provided to Julie under “section 8-1, ITAA 1997”.

Answer C:

“Section 8-1 (2)(b)” clarifies that no deduction is acceptable for private and domestic

expenditure. In “Lodge v FCT (1972)” no child care expenses were considered for deduction

for the reason that it was not experienced in producing the assessable income.

Sally is found to have paid $1,200 to babysitter in order to look after her child when

she is away for work. Citing “Lodge v FCT (1972)” no deduction is permissible for

babysitter outlays because it is private payments and non-deductible under “section 8-1 (2)

(b)”.

Answer D:

The provision of “section 8-1” is also applicable where taxpayers incurs loss. In the

same way, the law court permitted deduction to taxpayer in “Charles Moore & Co (WA) Pty

Ltd v FCT (1956)” for the stolen money because it signified weakening to the financial

position of taxpayer.

In light of above description, the theft of $20,000 of goods by Sally’s long-term

worker institute a loss for the business. Citing “Charles Moore & Co (WA) Pty Ltd v FCT

(1956)” the stolen goods represents the depletion in financial situation of Sally. Hereafter, he

can get deduction under general provision of “section 8-1”.

Answer E:

According to “section 8-1, ITAA 1997” outlay occurred in attaining employment are

considered too remote or very early in the making of the assessable earnings. As held in the

“FCT v Maddalena (1971)” the taxpayer was deprived of deduction for cost sustained in

Julie occurred a mobile phone costs of $500 where 60% of the calls were work-

related. Referring to “Ronpibon Tin v FCT (1949)” the expenses hold dual purpose and only

deduction for work-related calls will be provided to Julie under “section 8-1, ITAA 1997”.

Answer C:

“Section 8-1 (2)(b)” clarifies that no deduction is acceptable for private and domestic

expenditure. In “Lodge v FCT (1972)” no child care expenses were considered for deduction

for the reason that it was not experienced in producing the assessable income.

Sally is found to have paid $1,200 to babysitter in order to look after her child when

she is away for work. Citing “Lodge v FCT (1972)” no deduction is permissible for

babysitter outlays because it is private payments and non-deductible under “section 8-1 (2)

(b)”.

Answer D:

The provision of “section 8-1” is also applicable where taxpayers incurs loss. In the

same way, the law court permitted deduction to taxpayer in “Charles Moore & Co (WA) Pty

Ltd v FCT (1956)” for the stolen money because it signified weakening to the financial

position of taxpayer.

In light of above description, the theft of $20,000 of goods by Sally’s long-term

worker institute a loss for the business. Citing “Charles Moore & Co (WA) Pty Ltd v FCT

(1956)” the stolen goods represents the depletion in financial situation of Sally. Hereafter, he

can get deduction under general provision of “section 8-1”.

Answer E:

According to “section 8-1, ITAA 1997” outlay occurred in attaining employment are

considered too remote or very early in the making of the assessable earnings. As held in the

“FCT v Maddalena (1971)” the taxpayer was deprived of deduction for cost sustained in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

getting new employment agreement as it was very early in the production of the assessable

income7.

Similarly, the outlay occurred in contesting the government election along with

spending on the big election party will not be considered as allowable deduction for the

reason that the expenses is very early in the making of the assessable income.

Answer to question 3:

Answer A:

As stated by the ATO when the long term lease is granted by the taxpayers then a

CGT event F2 takes place. A CGT event F2 is only applied when the holder of land grants a

sub-lease of land. The taxpayer can nonetheless obtain the CGT discount in this regard8.

Andy is the owner of land where he offers a five-year lease at a premium value of

$5,0009. Consequently, the granting of sub-lease of land has prompted CGT event F2. Andy

can apply for the CGT discount when selling the land.

Answer B:

A taxpayer when passes the use and enjoyment of title to another entity then a CGT

event B1 is triggered. Upon passing the asset title the capital gains that is made there after the

deduction of the acquisition expenditure gives rise to CGT event B101. Evidently, the case

facts obtained relating to Farm Ltd states that an option for the purchase of land for a value of

7 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia,

2013)

8 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and Investment Planning 2016 Edition.

McGraw-Hill Education, 2015.

9 Sadiq, Kerrie, Principles Of Taxation Law 2014

10 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook Co./Thomson Reuters, 2013)

getting new employment agreement as it was very early in the production of the assessable

income7.

Similarly, the outlay occurred in contesting the government election along with

spending on the big election party will not be considered as allowable deduction for the

reason that the expenses is very early in the making of the assessable income.

Answer to question 3:

Answer A:

As stated by the ATO when the long term lease is granted by the taxpayers then a

CGT event F2 takes place. A CGT event F2 is only applied when the holder of land grants a

sub-lease of land. The taxpayer can nonetheless obtain the CGT discount in this regard8.

Andy is the owner of land where he offers a five-year lease at a premium value of

$5,0009. Consequently, the granting of sub-lease of land has prompted CGT event F2. Andy

can apply for the CGT discount when selling the land.

Answer B:

A taxpayer when passes the use and enjoyment of title to another entity then a CGT

event B1 is triggered. Upon passing the asset title the capital gains that is made there after the

deduction of the acquisition expenditure gives rise to CGT event B101. Evidently, the case

facts obtained relating to Farm Ltd states that an option for the purchase of land for a value of

7 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia,

2013)

8 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and Investment Planning 2016 Edition.

McGraw-Hill Education, 2015.

9 Sadiq, Kerrie, Principles Of Taxation Law 2014

10 Sadiq, Kerrie and Cynthia Coleman, Principles Of Taxation Law 2013 (Lawbook Co./Thomson Reuters, 2013)

8TAXATION LAW

$800,000 was given by John. Therefore, granting of such option has triggered CGT event B1

and John in this case can apply the CGT discount method to compute the capital gains tax for

passing the title to another entity.

Answer C:

The ATO clarifies that the house that is used as main dwelling by the taxpayer does

not draws capital gains tax. But it must be noted that when the house that is used by the

taxpayer as the source for making income then the capital gains that is resulting from the

house upon its sale is only allowed for partial main residence exemption11.

Jamie and Olivia here are the owner of the property which they bought in 2006 and let

it out on rent for deriving rental income. But later in 2008 the property was used as main

dwelling until they sold in 2018. The house was used for both main residence and producing

income. Therefore, a partial main residence exemption is allowed to Jamie and Olivia while

they can also avail 50% CGT discount from the capital gains made.

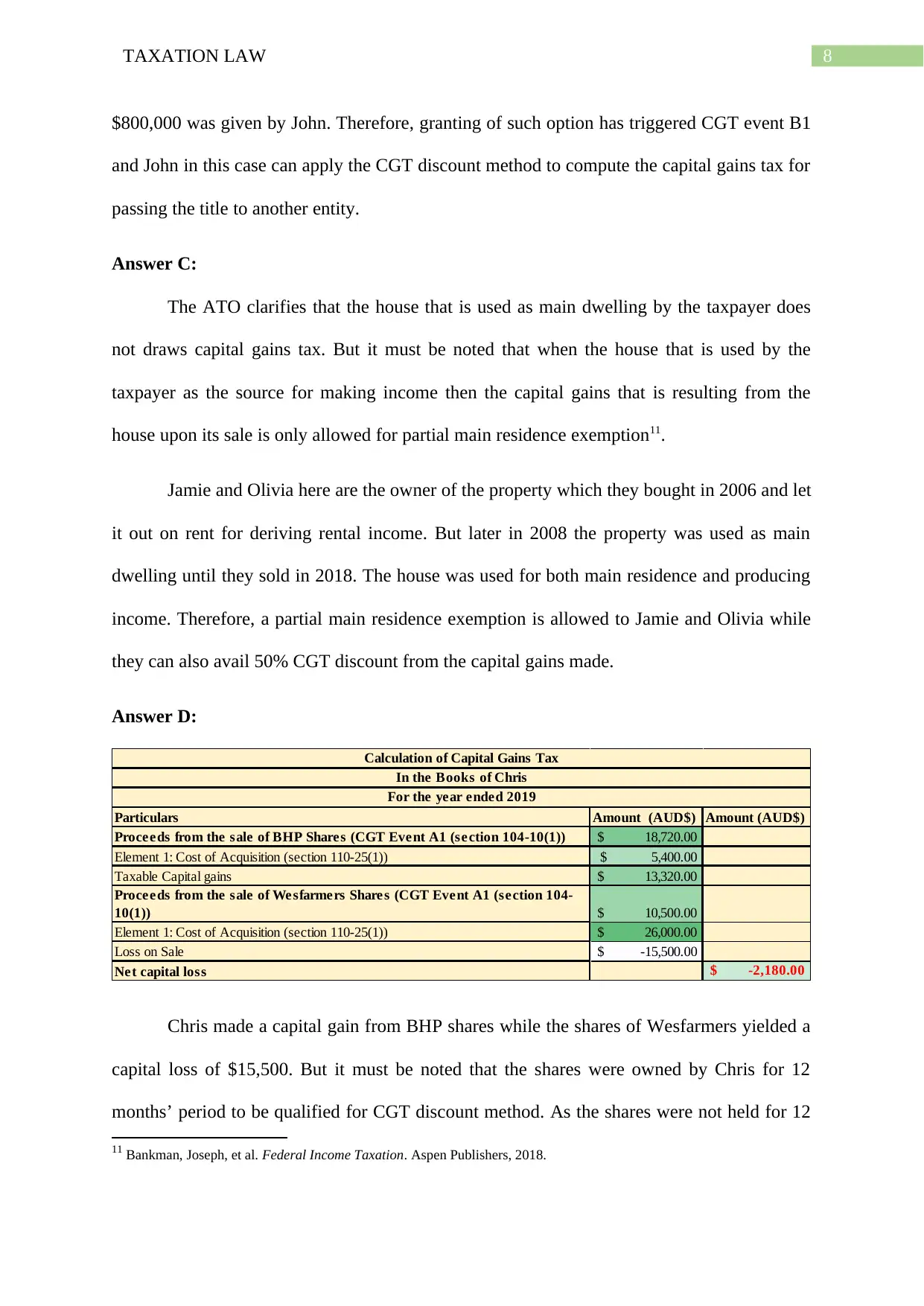

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris made a capital gain from BHP shares while the shares of Wesfarmers yielded a

capital loss of $15,500. But it must be noted that the shares were owned by Chris for 12

months’ period to be qualified for CGT discount method. As the shares were not held for 12

11 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

$800,000 was given by John. Therefore, granting of such option has triggered CGT event B1

and John in this case can apply the CGT discount method to compute the capital gains tax for

passing the title to another entity.

Answer C:

The ATO clarifies that the house that is used as main dwelling by the taxpayer does

not draws capital gains tax. But it must be noted that when the house that is used by the

taxpayer as the source for making income then the capital gains that is resulting from the

house upon its sale is only allowed for partial main residence exemption11.

Jamie and Olivia here are the owner of the property which they bought in 2006 and let

it out on rent for deriving rental income. But later in 2008 the property was used as main

dwelling until they sold in 2018. The house was used for both main residence and producing

income. Therefore, a partial main residence exemption is allowed to Jamie and Olivia while

they can also avail 50% CGT discount from the capital gains made.

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris made a capital gain from BHP shares while the shares of Wesfarmers yielded a

capital loss of $15,500. But it must be noted that the shares were owned by Chris for 12

months’ period to be qualified for CGT discount method. As the shares were not held for 12

11 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

months so no CGT discount will be applied and Chris can carry forward the capital loss to the

subsequent year. While the capital gains will be counted in the taxable income of Chris.

months so no CGT discount will be applied and Chris can carry forward the capital loss to the

subsequent year. While the capital gains will be counted in the taxable income of Chris.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Answer to question 4:

Answer A:

Most notably ordinary prize cannot be categorized as having revenue nature. But it

must be noted that ordinary prizes are considered income when relationship is recognized

with revenue earning activities of taxpayer. In “Stone v FCT (2005)” prize money received

by policewomen was considered income because she was carrying the business of

professional athlete12.

The best TV advertisement prize of $2,000 amounts to ordinary income under

“section 6-5, ITAA 1997” because it is related with the income earning activities of taxpayer.

Answer B:

When an employee is repaid the amount that is incurred for the employer then the

reimbursed amount is not treated as income. Here the taxpayer is given with a travel expenses

of $500 for travelling to Sydney for employment purpose. The taxpayer yet managed save

$380 and only paid 120 for the entire trip. Therefore, the amount of $380 that is saved by

employee will be considered as ordinary income under “section 6-5, ITAA 1997”.

Answer C:

Personal gifts, opposite of the voluntary payments that are incidental to the

employment or services that are rendered is not held to be income. In “Hayes v FCT (1956)”

the receipts of shares by accountant in the company by the earlier business owners was not

held as income. In the same way, the iphone that is given by client amounting to $1000 is not

an income since it is a personal gift13.

12 Woellner, R. H et al, Australian Taxation Law 2014

13 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation. Wolters Kluwer Law &

Business, 2015.

Answer to question 4:

Answer A:

Most notably ordinary prize cannot be categorized as having revenue nature. But it

must be noted that ordinary prizes are considered income when relationship is recognized

with revenue earning activities of taxpayer. In “Stone v FCT (2005)” prize money received

by policewomen was considered income because she was carrying the business of

professional athlete12.

The best TV advertisement prize of $2,000 amounts to ordinary income under

“section 6-5, ITAA 1997” because it is related with the income earning activities of taxpayer.

Answer B:

When an employee is repaid the amount that is incurred for the employer then the

reimbursed amount is not treated as income. Here the taxpayer is given with a travel expenses

of $500 for travelling to Sydney for employment purpose. The taxpayer yet managed save

$380 and only paid 120 for the entire trip. Therefore, the amount of $380 that is saved by

employee will be considered as ordinary income under “section 6-5, ITAA 1997”.

Answer C:

Personal gifts, opposite of the voluntary payments that are incidental to the

employment or services that are rendered is not held to be income. In “Hayes v FCT (1956)”

the receipts of shares by accountant in the company by the earlier business owners was not

held as income. In the same way, the iphone that is given by client amounting to $1000 is not

an income since it is a personal gift13.

12 Woellner, R. H et al, Australian Taxation Law 2014

13 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation. Wolters Kluwer Law &

Business, 2015.

11TAXATION LAW

Answer D:

There could be some circumstances where a person is given lump sum payment and

the amount may be held as assessable income. Representing clarification in “paragraph 118-

37 (1), (b), ITAA 1997” taxpayers are directed to omit the personal injury compensation

suffered on account of accidental or mistaken or illness payment from their assessable

revenue because it does not amount to income14.

In the same way the receipt of $10,000 as the damages for personal injuries suffered

in car accident is a tax exempt amount under “paragraph 118-37 (1), (b), ITAA 1997”.

Therefore, no tax is to be paid on such receipts.

Answer E:

There could be some situations when a person may be anticipating to derive income

on the upcoming or the future time period based on present entitlement of deriving income.

Such kind of anticipation is considered to remote too provide any form of nexus with the

current income year15. Shares for $5 has been purchased by the taxpayer on 30th June. The

value of shares increased to trend at $7.50. It can be stated no income is derived because the

shares are not sold and the future anticipated income is considered to be too remote to offer

any form of nexus with the current income year.

14 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

15 Surrey, Stanley S., ed. Federal income taxation: cases and materials. Vol. 1. Foundation Press, 2014

Answer D:

There could be some circumstances where a person is given lump sum payment and

the amount may be held as assessable income. Representing clarification in “paragraph 118-

37 (1), (b), ITAA 1997” taxpayers are directed to omit the personal injury compensation

suffered on account of accidental or mistaken or illness payment from their assessable

revenue because it does not amount to income14.

In the same way the receipt of $10,000 as the damages for personal injuries suffered

in car accident is a tax exempt amount under “paragraph 118-37 (1), (b), ITAA 1997”.

Therefore, no tax is to be paid on such receipts.

Answer E:

There could be some situations when a person may be anticipating to derive income

on the upcoming or the future time period based on present entitlement of deriving income.

Such kind of anticipation is considered to remote too provide any form of nexus with the

current income year15. Shares for $5 has been purchased by the taxpayer on 30th June. The

value of shares increased to trend at $7.50. It can be stated no income is derived because the

shares are not sold and the future anticipated income is considered to be too remote to offer

any form of nexus with the current income year.

14 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

15 Surrey, Stanley S., ed. Federal income taxation: cases and materials. Vol. 1. Foundation Press, 2014

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.