Taxation Law Assignment: Analysis of Deductions and Taxation

VerifiedAdded on 2020/05/11

|6

|425

|105

Homework Assignment

AI Summary

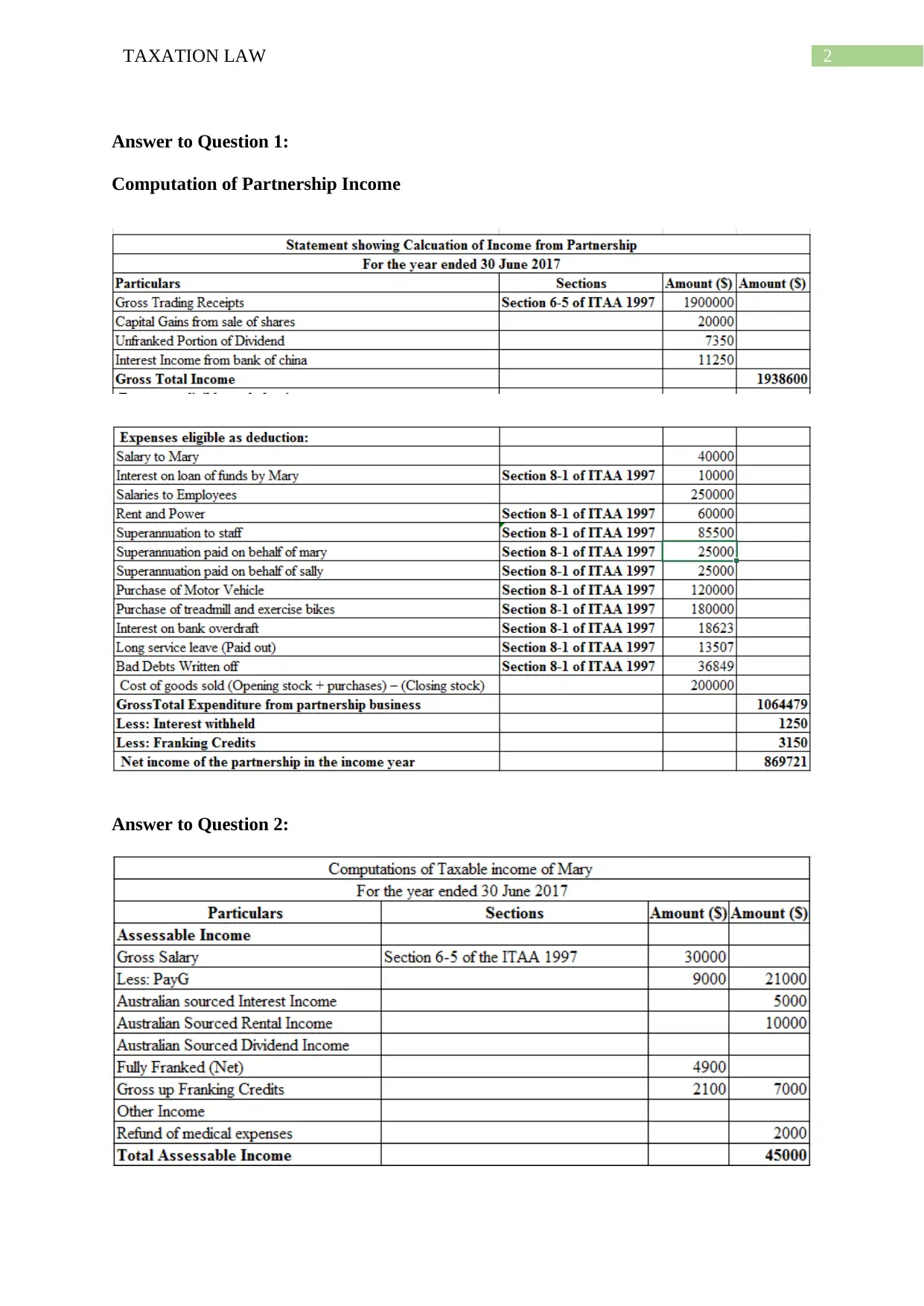

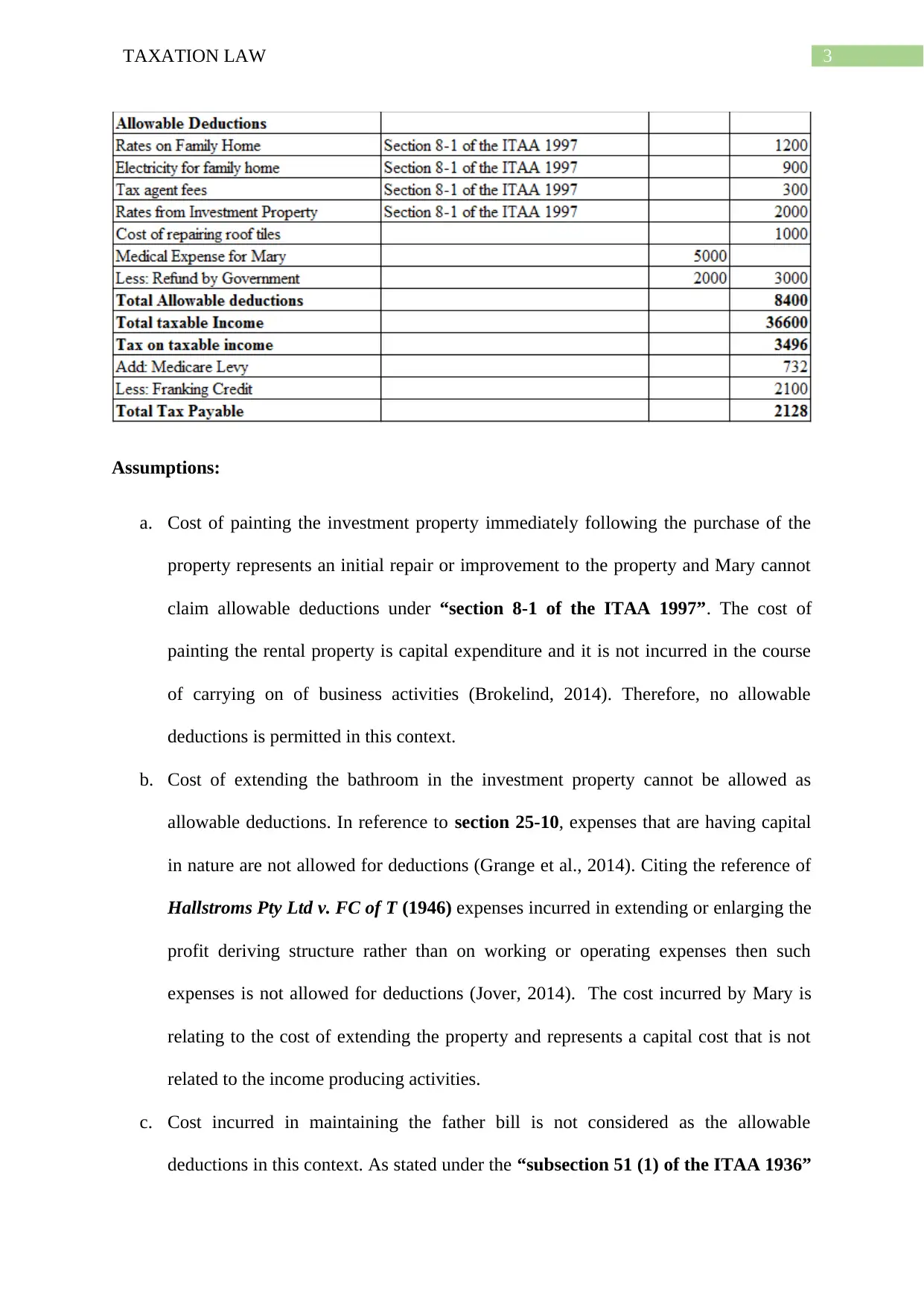

This assignment analyzes a taxation law problem focusing on allowable deductions related to an investment property. The solution addresses the deductibility of various expenses, including the cost of painting, extending a bathroom, and other costs incurred. The assignment references relevant sections of the ITAA 1997 and ITAA 1936, providing a legal basis for the deductions. The solution also cites legal precedents such as Hallstroms Pty Ltd. v. FC of T. The assignment covers the computation of partnership income and details about costs of maintaining the father bill. The assignment uses the provided references and case laws to justify the deductions or non-deductibility of expenses, offering a comprehensive understanding of taxation principles. The assignment is a valuable resource for students studying taxation law.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.