HI3042 Taxation Law T2 2017 Assignment: Deductions & Credits

VerifiedAdded on 2020/02/24

|14

|1682

|53

Homework Assignment

AI Summary

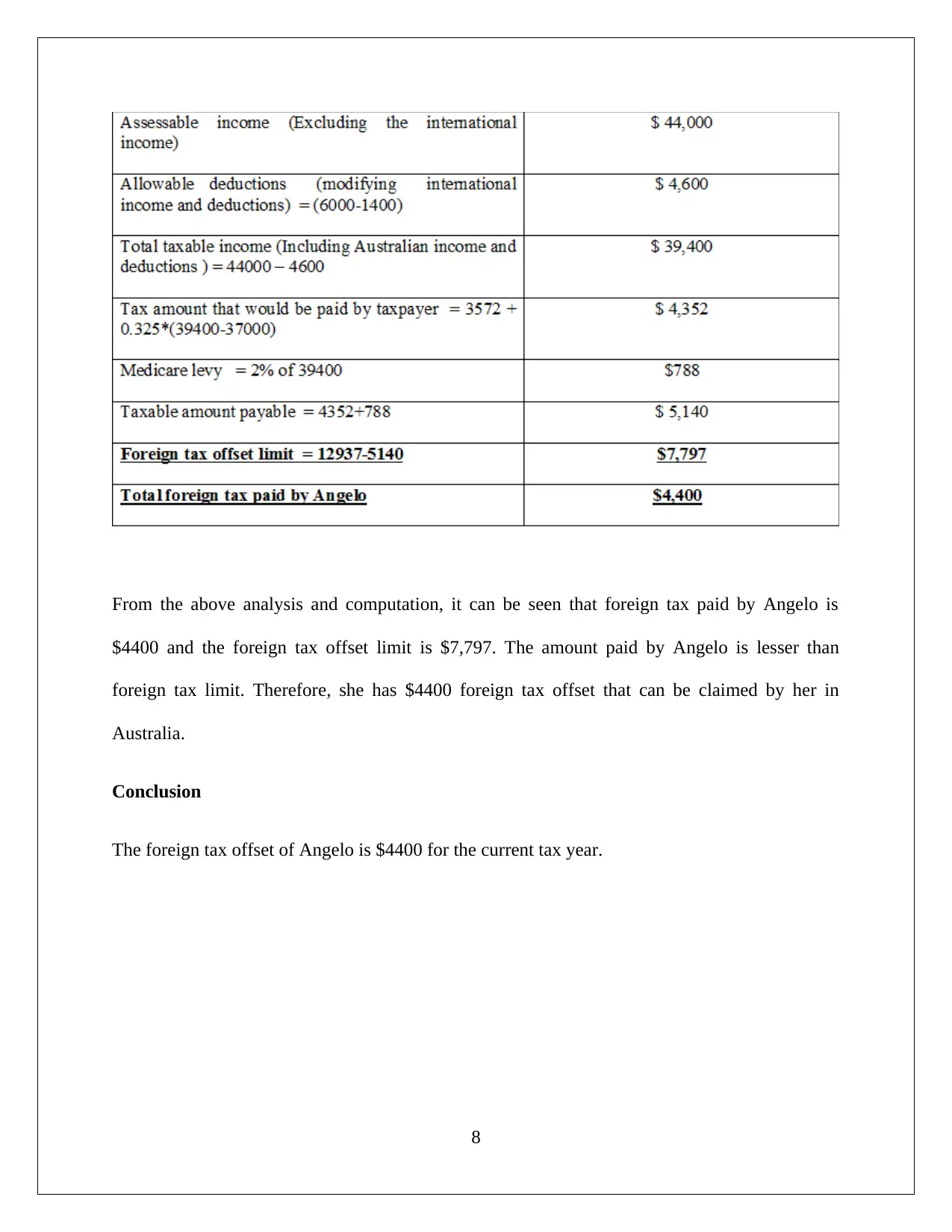

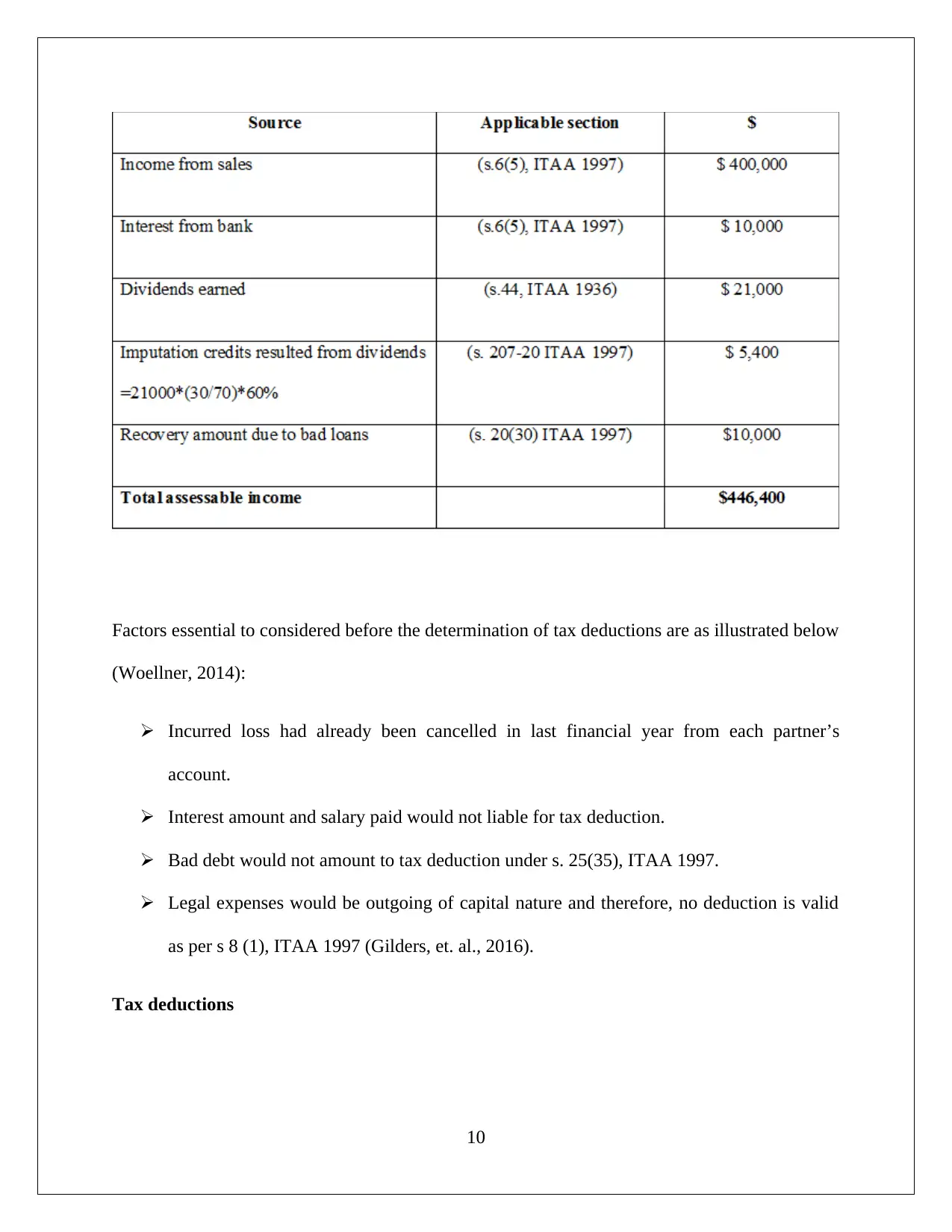

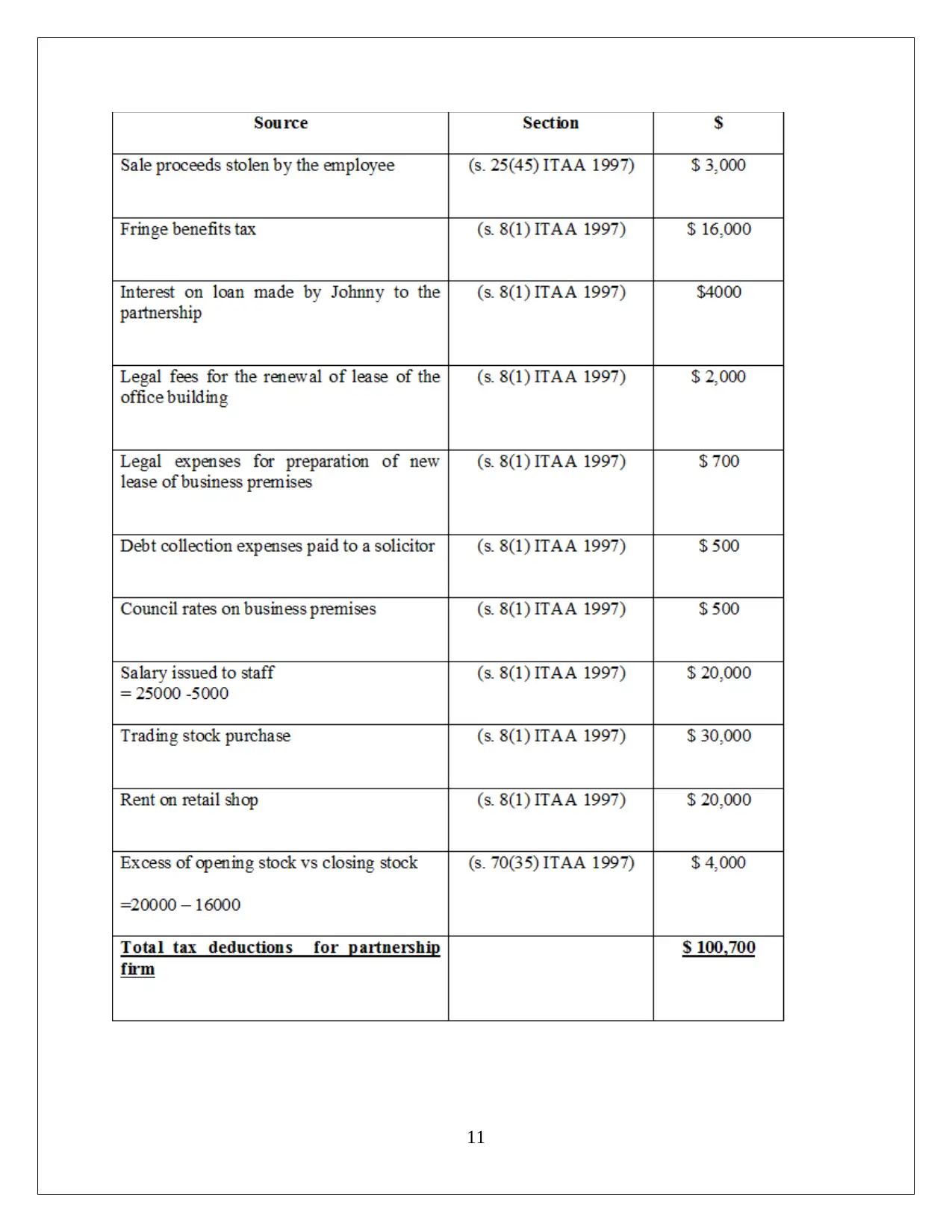

This document provides a comprehensive solution to a taxation law assignment (HI3042) from T2 2017, covering key aspects of Australian taxation. The solution addresses four key questions. Question 1 examines the deductibility of various business expenses under s 8-1 of the Income Tax Assessment Act 1997, including costs of moving machinery, asset revaluation, and legal expenses. Question 2 determines the input tax credit claimable by a bank based on advertising expenditure and GST. Question 3 calculates the foreign tax offset for a taxpayer, Angelo, considering foreign tax paid and offset limits. Finally, Question 4 calculates the net income of a partnership firm, Johnny and Leon, considering assessable income and allowable deductions. The solution provides detailed explanations, calculations, and references to relevant tax laws and case precedents.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.