Taxation Law of Australia Individual Assignment LAWS20060 Term 1 2019

VerifiedAdded on 2023/01/04

|19

|4522

|87

Homework Assignment

AI Summary

This assignment solution addresses key concepts in Australian taxation law, covering various aspects such as depreciation, tax offsets, and income tax rates. It delves into specific sections of the Income Tax Assessment Act 1997 (ITAA 1997) and relevant tax rulings, providing explanations and examples. The document explores topics like collectibles, CGT events, and the calculation of income tax, with references to case law such as FC of T v Day and Amalgamated Zinc Ltd v FCT. The assignment also examines general deductions, including those for expenses incurred in earning assessable income, and specific scenarios involving child care expenses and theft losses. Furthermore, it analyses CGT events related to leases and land options, and presents a capital gains tax calculation for share transactions. The solution provides a comprehensive overview of taxation principles and their practical application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer of Question 1:...............................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answers G:.............................................................................................................................4

Answer H:..............................................................................................................................5

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to A:..........................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................8

Answer E:...............................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:..........................................................................................................................9

Answer to C:........................................................................................................................10

Table of Contents

Answer of Question 1:...............................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answers G:.............................................................................................................................4

Answer H:..............................................................................................................................5

Answer to I:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to A:..........................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................8

Answer E:...............................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to A:..........................................................................................................................9

Answer to B:..........................................................................................................................9

Answer to C:........................................................................................................................10

2TAXATION LAW

Answer D:............................................................................................................................11

Answer to question 4:...............................................................................................................11

Answer A:............................................................................................................................11

Answer B:.............................................................................................................................12

Answer C:.............................................................................................................................12

Answer D:............................................................................................................................13

Answer E:.............................................................................................................................13

Answer to Question 5:..............................................................................................................13

References:...............................................................................................................................16

Answer D:............................................................................................................................11

Answer to question 4:...............................................................................................................11

Answer A:............................................................................................................................11

Answer B:.............................................................................................................................12

Answer C:.............................................................................................................................12

Answer D:............................................................................................................................13

Answer E:.............................................................................................................................13

Answer to Question 5:..............................................................................................................13

References:...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer of Question 1:

Answer A:

Denoting the explanation made in the “Taxation Ruling of TR 2018/4”, explanation

regarding the methodology used in computing or determining the useful life of the asset for

depreciation purpose has been explained in “section 40-100, ITAA 1997”1.

Answer B:

Under the “Division 13 of the ITAA 1997” a noteworthy explanation has been made

where the taxpayer can gain the access regarding the detailed tax offset.

Answer C:

For the Australian resident that is having the highest income tax bracket a specific rate

of tax is applied on them which is given below;

Taxable Earnings Tax (AUD$)

$180,001 or more $54,097 + 45c for each $1 above $180,000

Answer D:

Under the “section 108-10 (2), ITAA 1997” collectible means those assets that are

kept mostly for their own private use2. The special rules that is applicable on the collectibles

1 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

2 Jones, Daryl. "Tax and accounting income-Worlds apart?." Taxation in Australia 52.1

(2017): 14.

Answer of Question 1:

Answer A:

Denoting the explanation made in the “Taxation Ruling of TR 2018/4”, explanation

regarding the methodology used in computing or determining the useful life of the asset for

depreciation purpose has been explained in “section 40-100, ITAA 1997”1.

Answer B:

Under the “Division 13 of the ITAA 1997” a noteworthy explanation has been made

where the taxpayer can gain the access regarding the detailed tax offset.

Answer C:

For the Australian resident that is having the highest income tax bracket a specific rate

of tax is applied on them which is given below;

Taxable Earnings Tax (AUD$)

$180,001 or more $54,097 + 45c for each $1 above $180,000

Answer D:

Under the “section 108-10 (2), ITAA 1997” collectible means those assets that are

kept mostly for their own private use2. The special rules that is applicable on the collectibles

1 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

2 Jones, Daryl. "Tax and accounting income-Worlds apart?." Taxation in Australia 52.1

(2017): 14.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

includes that under “section 118-10(1) of the ITAA 1997” capital loss or gains is ignored

under first element if the cost base of collectible is less than $500.

Answer E:

CGT event B1 is dealing with the use and enjoyment prior to the passing of title. Under

“section 104-15, ITAA 1997”, CGT event B1 happen3s;

a. When the taxpayer forms a contract with another entity where the right of using and

enjoying the CGT asset that is owned to taxpayers is passed to another entity; and

b. Title of the asset may pass to another entity prior to the termination of the agreement.

Answer F:

As per the “section 4-10(3) of the ITAA 1997” it lay down the method of calculating

the amount of tax a person must pay. The formula for calculating the income tax is given

below;

Income tax = (Taxable Income x Rate) – Tax offsets

Answers G:

The decision that was given in “FC of T v Day 2008 ATC 20-064” states that the

taxpayer was the public servant that has applied for the deduction relating to the legal

outgoings under “section 8-1, ITAA 1997” that was occurred because of the several charges

that were levied by his employer4. The charges were related to the disciplinary cases. The

3 Jones, Daryl. "Mid market focus: Income or capital?: Taxpayer draws a blank." Taxation in

Australia 51.7 (2017): 357.

4 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia53.2 (2018): 80.

includes that under “section 118-10(1) of the ITAA 1997” capital loss or gains is ignored

under first element if the cost base of collectible is less than $500.

Answer E:

CGT event B1 is dealing with the use and enjoyment prior to the passing of title. Under

“section 104-15, ITAA 1997”, CGT event B1 happen3s;

a. When the taxpayer forms a contract with another entity where the right of using and

enjoying the CGT asset that is owned to taxpayers is passed to another entity; and

b. Title of the asset may pass to another entity prior to the termination of the agreement.

Answer F:

As per the “section 4-10(3) of the ITAA 1997” it lay down the method of calculating

the amount of tax a person must pay. The formula for calculating the income tax is given

below;

Income tax = (Taxable Income x Rate) – Tax offsets

Answers G:

The decision that was given in “FC of T v Day 2008 ATC 20-064” states that the

taxpayer was the public servant that has applied for the deduction relating to the legal

outgoings under “section 8-1, ITAA 1997” that was occurred because of the several charges

that were levied by his employer4. The charges were related to the disciplinary cases. The

3 Jones, Daryl. "Mid market focus: Income or capital?: Taxpayer draws a blank." Taxation in

Australia 51.7 (2017): 357.

4 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia53.2 (2018): 80.

5TAXATION LAW

commissioner held that the cases that were brought against the taxpayer were because of his

own concerns and as a result the legal outgoings were not allowed for deductions under

“section 8-1, ITAA 1997” because the taxpayer was dismissed from his employment and the

expenses were as the outcome of his own consequences.

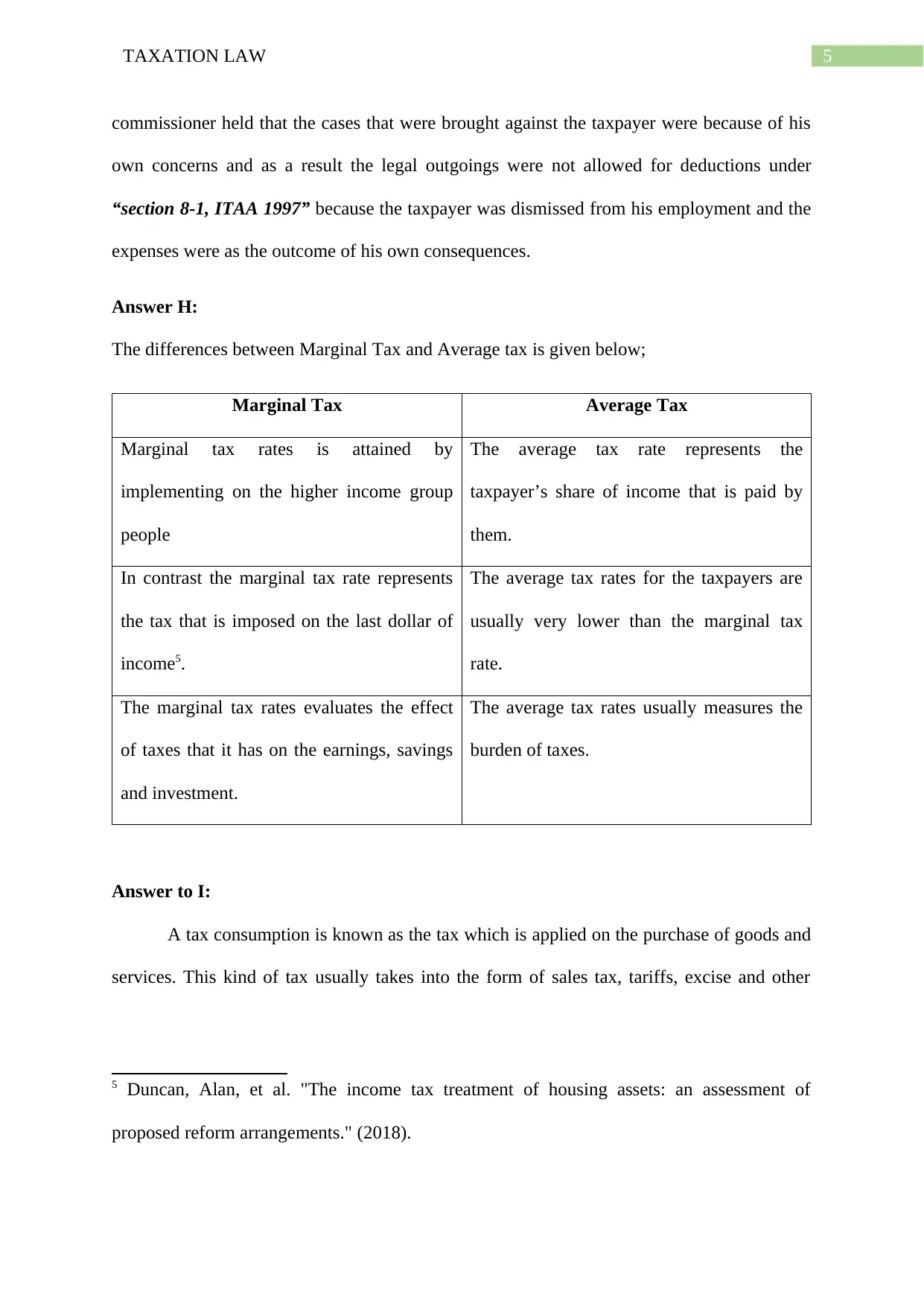

Answer H:

The differences between Marginal Tax and Average tax is given below;

Marginal Tax Average Tax

Marginal tax rates is attained by

implementing on the higher income group

people

The average tax rate represents the

taxpayer’s share of income that is paid by

them.

In contrast the marginal tax rate represents

the tax that is imposed on the last dollar of

income5.

The average tax rates for the taxpayers are

usually very lower than the marginal tax

rate.

The marginal tax rates evaluates the effect

of taxes that it has on the earnings, savings

and investment.

The average tax rates usually measures the

burden of taxes.

Answer to I:

A tax consumption is known as the tax which is applied on the purchase of goods and

services. This kind of tax usually takes into the form of sales tax, tariffs, excise and other

5 Duncan, Alan, et al. "The income tax treatment of housing assets: an assessment of

proposed reform arrangements." (2018).

commissioner held that the cases that were brought against the taxpayer were because of his

own concerns and as a result the legal outgoings were not allowed for deductions under

“section 8-1, ITAA 1997” because the taxpayer was dismissed from his employment and the

expenses were as the outcome of his own consequences.

Answer H:

The differences between Marginal Tax and Average tax is given below;

Marginal Tax Average Tax

Marginal tax rates is attained by

implementing on the higher income group

people

The average tax rate represents the

taxpayer’s share of income that is paid by

them.

In contrast the marginal tax rate represents

the tax that is imposed on the last dollar of

income5.

The average tax rates for the taxpayers are

usually very lower than the marginal tax

rate.

The marginal tax rates evaluates the effect

of taxes that it has on the earnings, savings

and investment.

The average tax rates usually measures the

burden of taxes.

Answer to I:

A tax consumption is known as the tax which is applied on the purchase of goods and

services. This kind of tax usually takes into the form of sales tax, tariffs, excise and other

5 Duncan, Alan, et al. "The income tax treatment of housing assets: an assessment of

proposed reform arrangements." (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

types of consumption taxes that is imposed on the goods and service6. The examples of

consumption taxes include the excise duties, value added tax and taxes that are levied on the

gross business receipts.

Answer to question 2:

Answer to A:

Under the “section 8-1, ITAA 1997” a taxpayer is permitted to deduction from their

taxable earnings a loss or expenses till the extent that is occurred in producing assessable

income. In “Amalgamated Zinc Ltd v FCT (1935)” taxpayers were allowed deduction for

expenses occurred in the course of gaining or producing taxable income.

Brett here borrowed from bank to pay the wages for his employees. Mentioning

“Amalgamated Zinc Ltd v FCT (1935)” the interest on loan that is occurred on the borrowed

funds by Brett is occurred in the course of producing assessable earnings. Therefore, the

interest on loan is allowable deductions under “section 8-1, ITAA 1997”.

Answer B:

An expenditure or loss that are occurred for dual purpose then the expenses should be

apportioned up to the extent that meets it meets the positive limbs of “section 8-1, ITAA

1997”. The Federal Court in “Ronpibon Tin NL v FC of T (1949)” held that expenses must

be apportioned up to the deductible portion that has dual purpose7.

6 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

7 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New

Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

types of consumption taxes that is imposed on the goods and service6. The examples of

consumption taxes include the excise duties, value added tax and taxes that are levied on the

gross business receipts.

Answer to question 2:

Answer to A:

Under the “section 8-1, ITAA 1997” a taxpayer is permitted to deduction from their

taxable earnings a loss or expenses till the extent that is occurred in producing assessable

income. In “Amalgamated Zinc Ltd v FCT (1935)” taxpayers were allowed deduction for

expenses occurred in the course of gaining or producing taxable income.

Brett here borrowed from bank to pay the wages for his employees. Mentioning

“Amalgamated Zinc Ltd v FCT (1935)” the interest on loan that is occurred on the borrowed

funds by Brett is occurred in the course of producing assessable earnings. Therefore, the

interest on loan is allowable deductions under “section 8-1, ITAA 1997”.

Answer B:

An expenditure or loss that are occurred for dual purpose then the expenses should be

apportioned up to the extent that meets it meets the positive limbs of “section 8-1, ITAA

1997”. The Federal Court in “Ronpibon Tin NL v FC of T (1949)” held that expenses must

be apportioned up to the deductible portion that has dual purpose7.

6 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

7 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New

Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Noticeably, Julie occurred mobile phone expenses for dual purpose which involved

both private and work purpose. Citing “Ronpibon Tin NL v FC of T (1949)” Julie can

deduction up to 60% of mobile phone bill because the expenses satisfies the positive limb of

“section 8-1, ITAA 1997”.

Answer C:

No general deduction is allowed under the “section 8-1, ITAA 1997” for the child

care expenses. In “Lodge v FCT (1972)” the taxpayer here reported the child care expenses

which was not allowed for general deduction because it does not puts the taxpayer in the

position of earning taxable income8.

Sally during the year paid a sum of $1,200 for babysitting purpose. Mentioning

decision made in “Lodge v FCT (1972)” the babysitter expenses is a private expenses and

not relevant to Sally’s income producing activities. Therefore no deduction is allowed under

“section 8-1, ITAA 1997”.

Answer D:

The rule of general deduction is also applicable both on the losses and outgoings. The

court in “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)”, allowed to taxpayer to

claim deduction for the theft of money while going to bank because the loss represents

depletion to financial position of taxpayer9.

8 Kudrna, George. "Australia’s Retirement Income Policy: Means Testing and Taxation of

Pensions." CESifo DICE Report 14.1 (2016): 3-9.

9 Yuan, Helena. "Mid market focus: The sharing economy and taxation." Taxation in

Australia 51.6 (2016): 293.

Noticeably, Julie occurred mobile phone expenses for dual purpose which involved

both private and work purpose. Citing “Ronpibon Tin NL v FC of T (1949)” Julie can

deduction up to 60% of mobile phone bill because the expenses satisfies the positive limb of

“section 8-1, ITAA 1997”.

Answer C:

No general deduction is allowed under the “section 8-1, ITAA 1997” for the child

care expenses. In “Lodge v FCT (1972)” the taxpayer here reported the child care expenses

which was not allowed for general deduction because it does not puts the taxpayer in the

position of earning taxable income8.

Sally during the year paid a sum of $1,200 for babysitting purpose. Mentioning

decision made in “Lodge v FCT (1972)” the babysitter expenses is a private expenses and

not relevant to Sally’s income producing activities. Therefore no deduction is allowed under

“section 8-1, ITAA 1997”.

Answer D:

The rule of general deduction is also applicable both on the losses and outgoings. The

court in “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)”, allowed to taxpayer to

claim deduction for the theft of money while going to bank because the loss represents

depletion to financial position of taxpayer9.

8 Kudrna, George. "Australia’s Retirement Income Policy: Means Testing and Taxation of

Pensions." CESifo DICE Report 14.1 (2016): 3-9.

9 Yuan, Helena. "Mid market focus: The sharing economy and taxation." Taxation in

Australia 51.6 (2016): 293.

8TAXATION LAW

Similarly, the theft of goods from Jerry’s business amounting to $20,000 is allowed

for deduction under “section 8-1, ITAA 1997” because the loss represents depletion to

financial position of Jerry’s business.

Answer E:

Expenses that is related to the production of taxable earnings in the future period

where nexus is not established is not allowed for deduction. As held in “Maddalena v FCT

(1971)” traveling expenses occurred in obtaining a new employment is not allowed for

deduction under “section 8-1, ITAA 1997” because the expenses were very much

preliminary to the income producing activities10.

As evident in the current situation of taxpayer where the expenses were reported for

contesting the local government election of $5000 and $2000 on big election party is non-

deductible under “section 8-1, ITAA 1997”. Mentioning the decision of “Maddalena v FCT

(1971)” the expenses were very much preliminary to the income producing activities11.

10 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

11 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

Similarly, the theft of goods from Jerry’s business amounting to $20,000 is allowed

for deduction under “section 8-1, ITAA 1997” because the loss represents depletion to

financial position of Jerry’s business.

Answer E:

Expenses that is related to the production of taxable earnings in the future period

where nexus is not established is not allowed for deduction. As held in “Maddalena v FCT

(1971)” traveling expenses occurred in obtaining a new employment is not allowed for

deduction under “section 8-1, ITAA 1997” because the expenses were very much

preliminary to the income producing activities10.

As evident in the current situation of taxpayer where the expenses were reported for

contesting the local government election of $5000 and $2000 on big election party is non-

deductible under “section 8-1, ITAA 1997”. Mentioning the decision of “Maddalena v FCT

(1971)” the expenses were very much preliminary to the income producing activities11.

10 Lee, Joanne. "The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test." J. Austl. Tax'n 20 (2018): 1.

11 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to question 3:

Answer to A:

According to the Australian Taxation Office a taxpayer is only allowed to choose

CGT event F2 when a person provides any grant or extension of the long term lease. It is

applicable to the owner of land when they grant any sub-lease12.

Andy here is the owner of underlying land grants a lease to Brian for five years at

$5,000 premium rate. The granting of lease to Brian results in CGT event F2. However, Andy

will not be able to obtain 50% CGT upon making the CGT event.

Answer to B:

As stated by the ATO a CGT event B1 happens when the land is bought by the new

owner13. On the original basis, the use of land only happens when the ownership of land is

passed to new owner and from the day the holder of land is allowed to profits and rents. In

the current case, in the exchange of $40,000 the option of purchasing the land was provided

to Farm Ltd by John. For John this gives rise to CGT event B1. Consequently, John is

allowed to apply the 50% CGT discount on the above deal.

Answer to C:

According to the ATO basic exemption on capital gains or loss is provided to

taxpayer for sale of main residence. However under “section 118-10 (1), ITAA 1997” the

main dwelling should be the main residence of taxpayer all through their ownership period

12 Pinto, Dale, and Michelle Evans. "Returning income taxation revenue to the states: back to

the future." (2018).

13 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies

in Australia." Austl. Tax F. 30 (2015): 569.

Answer to question 3:

Answer to A:

According to the Australian Taxation Office a taxpayer is only allowed to choose

CGT event F2 when a person provides any grant or extension of the long term lease. It is

applicable to the owner of land when they grant any sub-lease12.

Andy here is the owner of underlying land grants a lease to Brian for five years at

$5,000 premium rate. The granting of lease to Brian results in CGT event F2. However, Andy

will not be able to obtain 50% CGT upon making the CGT event.

Answer to B:

As stated by the ATO a CGT event B1 happens when the land is bought by the new

owner13. On the original basis, the use of land only happens when the ownership of land is

passed to new owner and from the day the holder of land is allowed to profits and rents. In

the current case, in the exchange of $40,000 the option of purchasing the land was provided

to Farm Ltd by John. For John this gives rise to CGT event B1. Consequently, John is

allowed to apply the 50% CGT discount on the above deal.

Answer to C:

According to the ATO basic exemption on capital gains or loss is provided to

taxpayer for sale of main residence. However under “section 118-10 (1), ITAA 1997” the

main dwelling should be the main residence of taxpayer all through their ownership period

12 Pinto, Dale, and Michelle Evans. "Returning income taxation revenue to the states: back to

the future." (2018).

13 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies

in Australia." Austl. Tax F. 30 (2015): 569.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

and not used for producing income14. In case the property is used to produce income then

only partial exemption is provided on the main residence.

A residential property was bought by Jamie and Olivia. Soon after purchase it was

rented out for two years from 2006 to 2008. However the property was used for residential

purpose from 2008 to 2018 until it was finally sold at a net capital gain of $300,000. Hence,

Jamie and Olivia will only be allowed to claim partial exemption from capital gains made

thereon. Additionally, the property has met the twelve month ownership rule therefore a 50%

CGT discount can be obtained from the capital gains made.

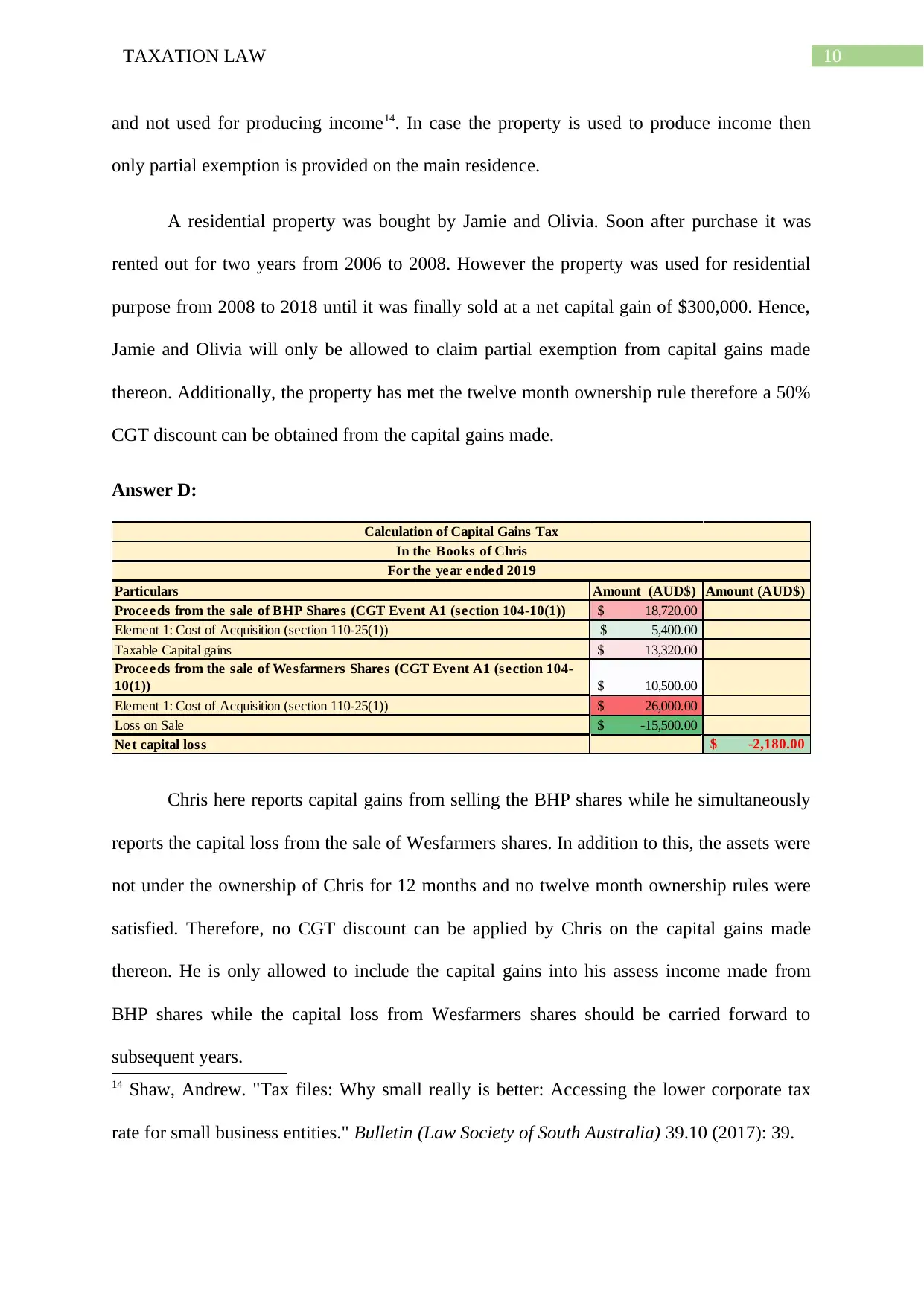

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris here reports capital gains from selling the BHP shares while he simultaneously

reports the capital loss from the sale of Wesfarmers shares. In addition to this, the assets were

not under the ownership of Chris for 12 months and no twelve month ownership rules were

satisfied. Therefore, no CGT discount can be applied by Chris on the capital gains made

thereon. He is only allowed to include the capital gains into his assess income made from

BHP shares while the capital loss from Wesfarmers shares should be carried forward to

subsequent years.

14 Shaw, Andrew. "Tax files: Why small really is better: Accessing the lower corporate tax

rate for small business entities." Bulletin (Law Society of South Australia) 39.10 (2017): 39.

and not used for producing income14. In case the property is used to produce income then

only partial exemption is provided on the main residence.

A residential property was bought by Jamie and Olivia. Soon after purchase it was

rented out for two years from 2006 to 2008. However the property was used for residential

purpose from 2008 to 2018 until it was finally sold at a net capital gain of $300,000. Hence,

Jamie and Olivia will only be allowed to claim partial exemption from capital gains made

thereon. Additionally, the property has met the twelve month ownership rule therefore a 50%

CGT discount can be obtained from the capital gains made.

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris here reports capital gains from selling the BHP shares while he simultaneously

reports the capital loss from the sale of Wesfarmers shares. In addition to this, the assets were

not under the ownership of Chris for 12 months and no twelve month ownership rules were

satisfied. Therefore, no CGT discount can be applied by Chris on the capital gains made

thereon. He is only allowed to include the capital gains into his assess income made from

BHP shares while the capital loss from Wesfarmers shares should be carried forward to

subsequent years.

14 Shaw, Andrew. "Tax files: Why small really is better: Accessing the lower corporate tax

rate for small business entities." Bulletin (Law Society of South Australia) 39.10 (2017): 39.

11TAXATION LAW

Answer to question 4:

Answer A:

It is noteworthy to denote that the prizes and coincidental winnings is not income in

accordance with ordinary concept given the windfall income is earned by luck. However, In

“Kelly v FCT (1985)” the prize winnings was considered taxable because it was related with

taxpayer use of skill15.

The taxpayer here receives a sum of $2,000 as winnings from the best TV

advertisements. Therefore, referring to “Kelly v FCT (1985)” the prize winnings was

considered taxable income in accordance with ordinary concept of “section 6-5, ITAA 1997”

because it was related with taxpayer income earning activity.

Answer B:

As explained in the “section 6-1, ITAA 1936” income from private exertion

comprises of the allowances, salaries, wages, gratuities etc. that is received by an individual

taxpayer in the course of employment by working as the employee16.

In this case, the sum of $500 is received by the employee from the employer which is

associated to the outlay occurred for travelling to Sydney for work purpose. While the

employee only got the ticket at $120 and rest amount he was allowed to keep with himself.

Hence, the left-over amount is considered as income which is taxable under “section 6-5,

ITAA 1997”.

15 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

16 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

Answer to question 4:

Answer A:

It is noteworthy to denote that the prizes and coincidental winnings is not income in

accordance with ordinary concept given the windfall income is earned by luck. However, In

“Kelly v FCT (1985)” the prize winnings was considered taxable because it was related with

taxpayer use of skill15.

The taxpayer here receives a sum of $2,000 as winnings from the best TV

advertisements. Therefore, referring to “Kelly v FCT (1985)” the prize winnings was

considered taxable income in accordance with ordinary concept of “section 6-5, ITAA 1997”

because it was related with taxpayer income earning activity.

Answer B:

As explained in the “section 6-1, ITAA 1936” income from private exertion

comprises of the allowances, salaries, wages, gratuities etc. that is received by an individual

taxpayer in the course of employment by working as the employee16.

In this case, the sum of $500 is received by the employee from the employer which is

associated to the outlay occurred for travelling to Sydney for work purpose. While the

employee only got the ticket at $120 and rest amount he was allowed to keep with himself.

Hence, the left-over amount is considered as income which is taxable under “section 6-5,

ITAA 1997”.

15 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

16 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.