Taxation Law: Taxation of Compensation Receipts and CGT Implications

VerifiedAdded on 2022/12/23

|19

|4957

|12

Report

AI Summary

This report analyzes the taxation implications of compensation receipts and capital gains tax (CGT) for two clients, Sophie and Kate, and addresses the tax treatment of a property sale. The report examines various compensation receipts, including lump-sum damages for loss of reputation and income, reimbursement of legal fees, payments for pain and suffering, ongoing medical costs, and interest. It applies relevant sections of the ITAA 1997 and related rulings to determine whether these receipts are taxable as ordinary income or subject to CGT. Furthermore, the report investigates the CGT consequences of selling a pre-CGT asset that was the main residence of a deceased taxpayer, considering the beneficiaries' circumstances. The analysis considers the main residence exemption and other relevant provisions of the ITAA 1997 to determine the tax liability in each scenario. The report provides a detailed examination of the legal issues, laws, and their application to the given facts, offering a comprehensive understanding of the taxation principles involved.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................4

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................11

Conclusion:..........................................................................................................................13

References:...............................................................................................................................15

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................4

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................11

Conclusion:..........................................................................................................................13

References:...............................................................................................................................15

2TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Introduction:

Issues:

1.1. The main issue to the question is whether the lump sum amount as damages,

compensation relating to the loss of income and reimbursement relating to legal fees

received by Sophie and Kate for damages will be treated as the taxable earnings under the

legislative provision of “sec 6-5, ITAA 1997”.

1.2. Is the capital gains arising from the damages payment is not regarded as taxable

under the “sec 118-37, ITAA 1997”?

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

As denoted under the “Taxation Ruling of TR 95/35” it is largely related with

providing guidelines regarding the tax liability of income earned from the compensation

receipts (Woellner et al., 2016). This rule is usually applied on those individual taxpayers that

gets any money as compensation. The ruling is useful in outlining the CGT outcomes that is

associated to the receipt of compensation payments and ascertain whether the amount

received should be taken into consideration as the taxable receipts for the recipient under

“Part IIIA of the ITAA 1936”.

Where a taxpayer receives any compensation which is completely associated to the

disposal of underlying asset or any part of the underlying asset of the individual taxpayer then

the compensation that is received amounts to a consideration received for the sale of asset

Answer to question 1:

Introduction:

Issues:

1.1. The main issue to the question is whether the lump sum amount as damages,

compensation relating to the loss of income and reimbursement relating to legal fees

received by Sophie and Kate for damages will be treated as the taxable earnings under the

legislative provision of “sec 6-5, ITAA 1997”.

1.2. Is the capital gains arising from the damages payment is not regarded as taxable

under the “sec 118-37, ITAA 1997”?

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

As denoted under the “Taxation Ruling of TR 95/35” it is largely related with

providing guidelines regarding the tax liability of income earned from the compensation

receipts (Woellner et al., 2016). This rule is usually applied on those individual taxpayers that

gets any money as compensation. The ruling is useful in outlining the CGT outcomes that is

associated to the receipt of compensation payments and ascertain whether the amount

received should be taken into consideration as the taxable receipts for the recipient under

“Part IIIA of the ITAA 1936”.

Where a taxpayer receives any compensation which is completely associated to the

disposal of underlying asset or any part of the underlying asset of the individual taxpayer then

the compensation that is received amounts to a consideration received for the sale of asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(Coleman, 2015). The law court in the case of “FC of T v Spedley Securities Ltd (1988)”

stated that where any amount received as compensation for damage of business goodwill then

the amount will be considered as capital receipt.

Application:

As understood from the case facts of Sophie, she sued Fracpro for providing her

faulty calibration of laser machine. She received compensation from the Fracpro regarding

the loss of her income and reputation. The amount of $100,000 that is received by Sophie

should be viewed as the damage for the potential loss of business reputation. Apart from this

she also received a reimbursement of the legal fees that amounted to $7,000. Citing the

judgement made in “FCT v Spedley Securities Ltd (1988)” the sum of $100,000 that is

received by Sophie will be considered as the compensation for damage to business goodwill

and reputation (Braithwaite, 2017). The amount will be considered as capital receipt and non-

taxable as ordinary income under “sec 6-5, ITAA 1997”.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

A compensation receipts generally carries the character which is aimed at substituting

for something. When a taxpayer receives any compensation amount for the loss of capital

asset then in such circumstances the receipt of such compensation amount relating to loss of

capital asset will be considered as capital receipt and will not be treated as ordinary income.

Similarly, under the “paragraph 118-37 (1)(a) of the ITAA 1997” capital gains are to be

disregarded when it is obtained as a result of “CGT event C2” (Kewley, 2014). Under this

provision, any amount that is received by the taxpayer in regard to any injuries that is

suffered while conducting any occupation should be simply disregarded.

(Coleman, 2015). The law court in the case of “FC of T v Spedley Securities Ltd (1988)”

stated that where any amount received as compensation for damage of business goodwill then

the amount will be considered as capital receipt.

Application:

As understood from the case facts of Sophie, she sued Fracpro for providing her

faulty calibration of laser machine. She received compensation from the Fracpro regarding

the loss of her income and reputation. The amount of $100,000 that is received by Sophie

should be viewed as the damage for the potential loss of business reputation. Apart from this

she also received a reimbursement of the legal fees that amounted to $7,000. Citing the

judgement made in “FCT v Spedley Securities Ltd (1988)” the sum of $100,000 that is

received by Sophie will be considered as the compensation for damage to business goodwill

and reputation (Braithwaite, 2017). The amount will be considered as capital receipt and non-

taxable as ordinary income under “sec 6-5, ITAA 1997”.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

A compensation receipts generally carries the character which is aimed at substituting

for something. When a taxpayer receives any compensation amount for the loss of capital

asset then in such circumstances the receipt of such compensation amount relating to loss of

capital asset will be considered as capital receipt and will not be treated as ordinary income.

Similarly, under the “paragraph 118-37 (1)(a) of the ITAA 1997” capital gains are to be

disregarded when it is obtained as a result of “CGT event C2” (Kewley, 2014). Under this

provision, any amount that is received by the taxpayer in regard to any injuries that is

suffered while conducting any occupation should be simply disregarded.

5TAXATION LAW

It mainly comprises of the right of seeking compensation for the asset relating to CGT

purpose by taking into account for consideration the definition of asset. One of the

noteworthy case that is related to this issue is the “Happles v FCT (1991)” that considered

whether the right to work will be treated as the asset inside the sense of “part IIIA of the

paragraph 118-37(1)(a), ITAA 1997” (Barkoczy, 2016).

Application:

Sophie in the current instances received a sum of $20,000 as the compensation for the

loss of income. The sum of lump sum payment which is received as the compensation for the

loss of income will be treated as the capital receipt and it will not be held as the ordinary

earnings. Referring to the court’s judgement made in “Happles v FCT (1991)” the

compensation received by Sophie is associated to the loss of capital asset (Keyzer et al.,

2017). The lump sum amount that is received by Sophie has resulted in the capital gain and

under the “paragraph 118-37(1) (a), ITAA 1997” Sophie is required to simply disregard the

capital gains that is obtained from the “CGT event C2”. This is because the amount received

by Sophie is mainly to recompense the damage caused as injury to her business.

2.3: Reimbursement of Legal Fees:

Laws:

As explained under the “section 118-37 (2)” capital gains or loss should be simply

ignored when a person makes a receipt of payment or the property in the form of

reimbursement for the expenses occurred (Sadiq, 2019). When a taxpayer receives any

amount as the reimbursement of the legal expenditure it do not lead to any capital gains

because it is viewed as the capital asset.

It mainly comprises of the right of seeking compensation for the asset relating to CGT

purpose by taking into account for consideration the definition of asset. One of the

noteworthy case that is related to this issue is the “Happles v FCT (1991)” that considered

whether the right to work will be treated as the asset inside the sense of “part IIIA of the

paragraph 118-37(1)(a), ITAA 1997” (Barkoczy, 2016).

Application:

Sophie in the current instances received a sum of $20,000 as the compensation for the

loss of income. The sum of lump sum payment which is received as the compensation for the

loss of income will be treated as the capital receipt and it will not be held as the ordinary

earnings. Referring to the court’s judgement made in “Happles v FCT (1991)” the

compensation received by Sophie is associated to the loss of capital asset (Keyzer et al.,

2017). The lump sum amount that is received by Sophie has resulted in the capital gain and

under the “paragraph 118-37(1) (a), ITAA 1997” Sophie is required to simply disregard the

capital gains that is obtained from the “CGT event C2”. This is because the amount received

by Sophie is mainly to recompense the damage caused as injury to her business.

2.3: Reimbursement of Legal Fees:

Laws:

As explained under the “section 118-37 (2)” capital gains or loss should be simply

ignored when a person makes a receipt of payment or the property in the form of

reimbursement for the expenses occurred (Sadiq, 2019). When a taxpayer receives any

amount as the reimbursement of the legal expenditure it do not lead to any capital gains

because it is viewed as the capital asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

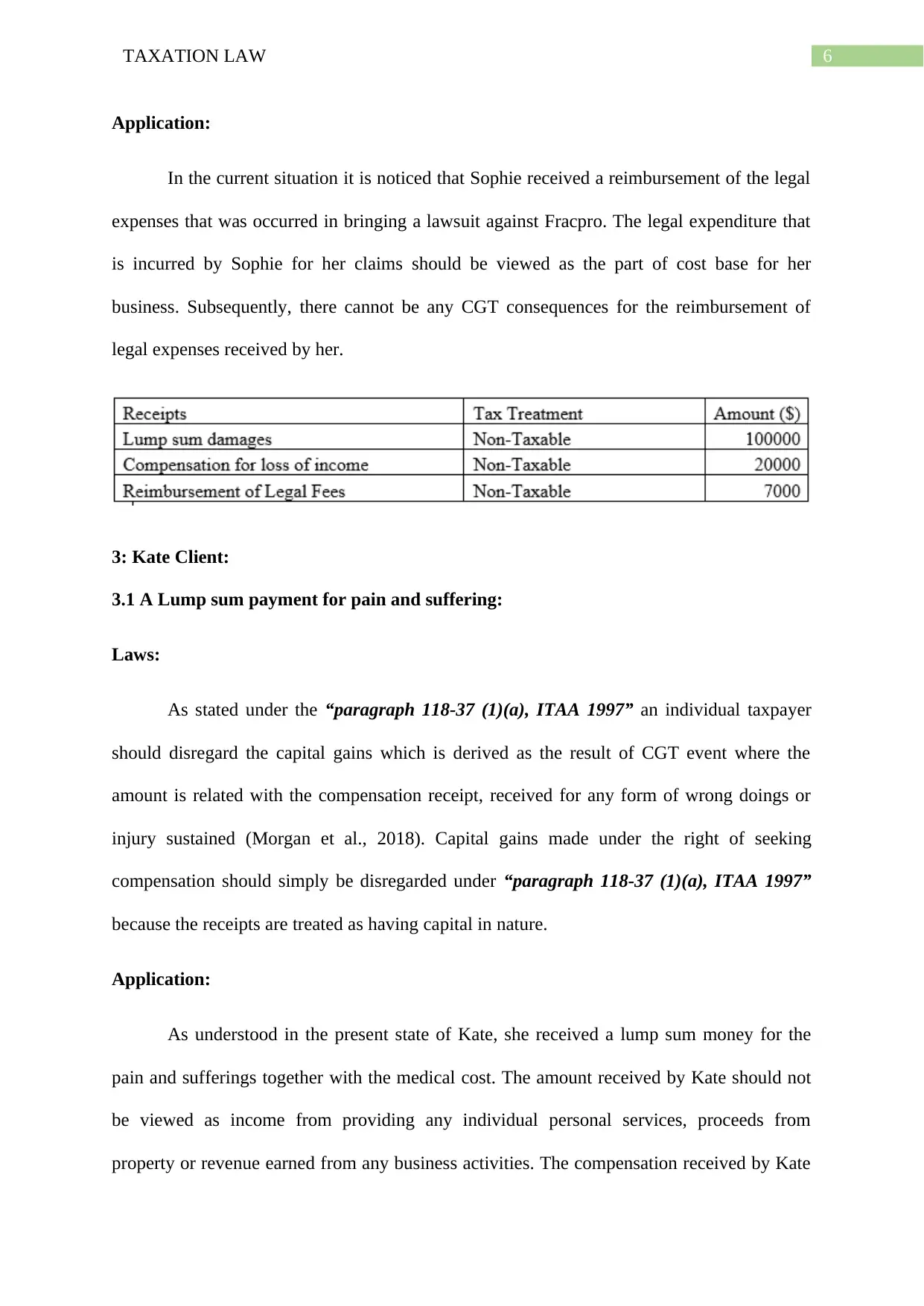

Application:

In the current situation it is noticed that Sophie received a reimbursement of the legal

expenses that was occurred in bringing a lawsuit against Fracpro. The legal expenditure that

is incurred by Sophie for her claims should be viewed as the part of cost base for her

business. Subsequently, there cannot be any CGT consequences for the reimbursement of

legal expenses received by her.

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

As stated under the “paragraph 118-37 (1)(a), ITAA 1997” an individual taxpayer

should disregard the capital gains which is derived as the result of CGT event where the

amount is related with the compensation receipt, received for any form of wrong doings or

injury sustained (Morgan et al., 2018). Capital gains made under the right of seeking

compensation should simply be disregarded under “paragraph 118-37 (1)(a), ITAA 1997”

because the receipts are treated as having capital in nature.

Application:

As understood in the present state of Kate, she received a lump sum money for the

pain and sufferings together with the medical cost. The amount received by Kate should not

be viewed as income from providing any individual personal services, proceeds from

property or revenue earned from any business activities. The compensation received by Kate

Application:

In the current situation it is noticed that Sophie received a reimbursement of the legal

expenses that was occurred in bringing a lawsuit against Fracpro. The legal expenditure that

is incurred by Sophie for her claims should be viewed as the part of cost base for her

business. Subsequently, there cannot be any CGT consequences for the reimbursement of

legal expenses received by her.

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

As stated under the “paragraph 118-37 (1)(a), ITAA 1997” an individual taxpayer

should disregard the capital gains which is derived as the result of CGT event where the

amount is related with the compensation receipt, received for any form of wrong doings or

injury sustained (Morgan et al., 2018). Capital gains made under the right of seeking

compensation should simply be disregarded under “paragraph 118-37 (1)(a), ITAA 1997”

because the receipts are treated as having capital in nature.

Application:

As understood in the present state of Kate, she received a lump sum money for the

pain and sufferings together with the medical cost. The amount received by Kate should not

be viewed as income from providing any individual personal services, proceeds from

property or revenue earned from any business activities. The compensation received by Kate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

was not earned as the receipt of any performance of any services. Rather, the compensation

receipt amounted to a one-off payment which was received by Kate and do not comprise of

any element of repetition.

Despite the fact that the payment was expected and relied by Kate, the expected sum arose as

the outcome of pain and suffering from the alleged injuries and general damages instead of

any kind of relation to personal services rendered.

The compensation received by Kate for pain and suffering amounts to settlement for

damages. The sum of $120,000 will be treated as capital originating from the “CGT event

C2” based on the right of seeking compensation (Morgan & Castelyn, 2018). The capital

gains made as the outcome of CGT event by Kate is disregarded under “sec 118-37(1)(b),

ITAA 1997”.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

Where a taxpayer receives any lump sum then it may be held as capital gains. The net

amount of capital gains is included in the assessable income of the taxpayer under “section

102-5, ITAA 1997” except when any exemption is allowed to the taxpayer. Under the

“Division 118, ITAA 1997” an exemption is allowed to the taxpayer when they receive

compensation for any form of wrong or injuries suffered in regard to their occupation or

personal by the taxpayer (Murray et al., 2018). For example, compensation received by the

taxpayer for any kind of discrimination or harassment at the workplace then it is simply

disregarded under “section 118-37 (1) (a), ITAA 1997.” Furthermore, a taxpayer is also

allowed to obtain exemption under “sec 118-37 (1) (b), ITAA 1997” when they receive

compensation for any form of wrong, illness or the injuries suffered by the taxpayer

personally or their relatives.

was not earned as the receipt of any performance of any services. Rather, the compensation

receipt amounted to a one-off payment which was received by Kate and do not comprise of

any element of repetition.

Despite the fact that the payment was expected and relied by Kate, the expected sum arose as

the outcome of pain and suffering from the alleged injuries and general damages instead of

any kind of relation to personal services rendered.

The compensation received by Kate for pain and suffering amounts to settlement for

damages. The sum of $120,000 will be treated as capital originating from the “CGT event

C2” based on the right of seeking compensation (Morgan & Castelyn, 2018). The capital

gains made as the outcome of CGT event by Kate is disregarded under “sec 118-37(1)(b),

ITAA 1997”.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

Where a taxpayer receives any lump sum then it may be held as capital gains. The net

amount of capital gains is included in the assessable income of the taxpayer under “section

102-5, ITAA 1997” except when any exemption is allowed to the taxpayer. Under the

“Division 118, ITAA 1997” an exemption is allowed to the taxpayer when they receive

compensation for any form of wrong or injuries suffered in regard to their occupation or

personal by the taxpayer (Murray et al., 2018). For example, compensation received by the

taxpayer for any kind of discrimination or harassment at the workplace then it is simply

disregarded under “section 118-37 (1) (a), ITAA 1997.” Furthermore, a taxpayer is also

allowed to obtain exemption under “sec 118-37 (1) (b), ITAA 1997” when they receive

compensation for any form of wrong, illness or the injuries suffered by the taxpayer

personally or their relatives.

8TAXATION LAW

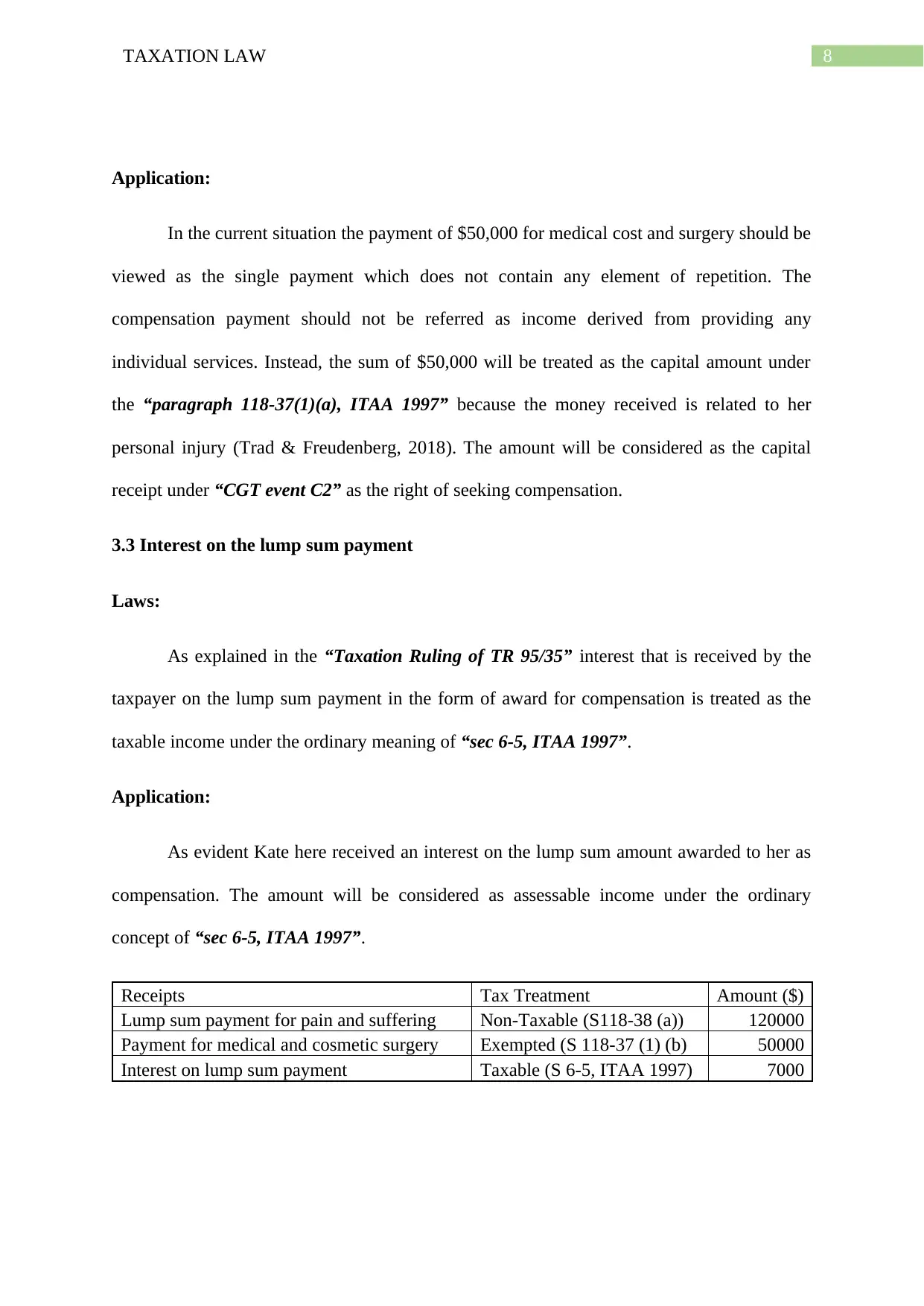

Application:

In the current situation the payment of $50,000 for medical cost and surgery should be

viewed as the single payment which does not contain any element of repetition. The

compensation payment should not be referred as income derived from providing any

individual services. Instead, the sum of $50,000 will be treated as the capital amount under

the “paragraph 118-37(1)(a), ITAA 1997” because the money received is related to her

personal injury (Trad & Freudenberg, 2018). The amount will be considered as the capital

receipt under “CGT event C2” as the right of seeking compensation.

3.3 Interest on the lump sum payment

Laws:

As explained in the “Taxation Ruling of TR 95/35” interest that is received by the

taxpayer on the lump sum payment in the form of award for compensation is treated as the

taxable income under the ordinary meaning of “sec 6-5, ITAA 1997”.

Application:

As evident Kate here received an interest on the lump sum amount awarded to her as

compensation. The amount will be considered as assessable income under the ordinary

concept of “sec 6-5, ITAA 1997”.

Receipts Tax Treatment Amount ($)

Lump sum payment for pain and suffering Non-Taxable (S118-38 (a)) 120000

Payment for medical and cosmetic surgery Exempted (S 118-37 (1) (b) 50000

Interest on lump sum payment Taxable (S 6-5, ITAA 1997) 7000

Application:

In the current situation the payment of $50,000 for medical cost and surgery should be

viewed as the single payment which does not contain any element of repetition. The

compensation payment should not be referred as income derived from providing any

individual services. Instead, the sum of $50,000 will be treated as the capital amount under

the “paragraph 118-37(1)(a), ITAA 1997” because the money received is related to her

personal injury (Trad & Freudenberg, 2018). The amount will be considered as the capital

receipt under “CGT event C2” as the right of seeking compensation.

3.3 Interest on the lump sum payment

Laws:

As explained in the “Taxation Ruling of TR 95/35” interest that is received by the

taxpayer on the lump sum payment in the form of award for compensation is treated as the

taxable income under the ordinary meaning of “sec 6-5, ITAA 1997”.

Application:

As evident Kate here received an interest on the lump sum amount awarded to her as

compensation. The amount will be considered as assessable income under the ordinary

concept of “sec 6-5, ITAA 1997”.

Receipts Tax Treatment Amount ($)

Lump sum payment for pain and suffering Non-Taxable (S118-38 (a)) 120000

Payment for medical and cosmetic surgery Exempted (S 118-37 (1) (b) 50000

Interest on lump sum payment Taxable (S 6-5, ITAA 1997) 7000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion:

The lump sum amount received by Kate and Sophie as compensation is mainly for the

personal injury and damages suffered in her business. The amount will be considered as

capital receipt and it will be exempt “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The central issue to the problem is associated with the determination of the capital gains

tax consequences to Joe and Amy, the taxpayers, regarding the sale of the property provided

that the;

1.1. The property was the pre-CGT asset of deceased

1.2. Before the death, the property was regarded as the main residence of the deceased

1.3. The taxpayer here acquired the property as the beneficiary under the deceased estate

1.4. The taxpayer lived in that property commencing from the day of death till the day

when the property was sold.

Laws:

As it has been explained in the “sec 118-110, ITAA 1997” the main residence of the

taxpayer is usually considered tax exempt from the provision of capital gains tax. Main

residence is better known as the dwelling along with the plus 2 hectares of land which

surrounds the dwelling (Main, 2019). Partial main residence exemption is available to the

taxpayer that subdivides or sells the land of their main residence or if the property has been

used by the taxpayer for generating taxable earnings. Where any capital gains or capital loss

Conclusion:

The lump sum amount received by Kate and Sophie as compensation is mainly for the

personal injury and damages suffered in her business. The amount will be considered as

capital receipt and it will be exempt “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The central issue to the problem is associated with the determination of the capital gains

tax consequences to Joe and Amy, the taxpayers, regarding the sale of the property provided

that the;

1.1. The property was the pre-CGT asset of deceased

1.2. Before the death, the property was regarded as the main residence of the deceased

1.3. The taxpayer here acquired the property as the beneficiary under the deceased estate

1.4. The taxpayer lived in that property commencing from the day of death till the day

when the property was sold.

Laws:

As it has been explained in the “sec 118-110, ITAA 1997” the main residence of the

taxpayer is usually considered tax exempt from the provision of capital gains tax. Main

residence is better known as the dwelling along with the plus 2 hectares of land which

surrounds the dwelling (Main, 2019). Partial main residence exemption is available to the

taxpayer that subdivides or sells the land of their main residence or if the property has been

used by the taxpayer for generating taxable earnings. Where any capital gains or capital loss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

arises from the dwelling that is the main place of residence for the taxpayer, then it is

exempted from tax given that;

a. The taxpayer is an individual

b. The house was the main residence of the taxpayer for the whole period of ownership

c. The ownership of the main residence was not given or passed to the taxpayer as the

beneficiary of deceased estate.

As stated in the “Division 128, ITAA 1997” it is largely related with CGT

consequences when the taxpayer dies (Payne, 2018). Denoting the explanation in “sec 128-

10” when the taxpayer dies, then their death should be regarded as the sale of asset by

deceased. Subsequently, no CGT event takes in this regard. Importantly “sec 128-10, ITAA

1997” is concerned with the CGT and consequences of death (Pert et al., 2018). The general

rule of the “sec 128-10” explains that when the taxpayer passes away, a CGT event that is

associated to the CGT asset is simply disregarded under this provision. When the taxpayer

passes away, the beneficiary or their legal heirs is deemed to have obtain the ownership of the

CGT asset starting from the day when the taxpayer died.

Additionally, when it is noticed that the a pre-CGT asset of the deceased is inherited

by a beneficiary, then in such situation the new beneficiary is assumed to have acquired the

asset based on the current market value on the day of death. While “sec 128-15, ITAA 1997”

provides explanation regarding the inheritance of the post-CGT assets (Liu, 2018). As per the

“sec 128-15, ITAA 1997” when it is noticed that the asset forms the part of post-CGT asset

of the deceased, the beneficiary is assumed to have acquired the asset on the day of death of

deceased based on the present case base.

While “sec 118-195” provides explanation regarding the inherited main residence

(Lieuallen & Shurtz, 2018). Under this provision, when it is noticed that the asses forms the

arises from the dwelling that is the main place of residence for the taxpayer, then it is

exempted from tax given that;

a. The taxpayer is an individual

b. The house was the main residence of the taxpayer for the whole period of ownership

c. The ownership of the main residence was not given or passed to the taxpayer as the

beneficiary of deceased estate.

As stated in the “Division 128, ITAA 1997” it is largely related with CGT

consequences when the taxpayer dies (Payne, 2018). Denoting the explanation in “sec 128-

10” when the taxpayer dies, then their death should be regarded as the sale of asset by

deceased. Subsequently, no CGT event takes in this regard. Importantly “sec 128-10, ITAA

1997” is concerned with the CGT and consequences of death (Pert et al., 2018). The general

rule of the “sec 128-10” explains that when the taxpayer passes away, a CGT event that is

associated to the CGT asset is simply disregarded under this provision. When the taxpayer

passes away, the beneficiary or their legal heirs is deemed to have obtain the ownership of the

CGT asset starting from the day when the taxpayer died.

Additionally, when it is noticed that the a pre-CGT asset of the deceased is inherited

by a beneficiary, then in such situation the new beneficiary is assumed to have acquired the

asset based on the current market value on the day of death. While “sec 128-15, ITAA 1997”

provides explanation regarding the inheritance of the post-CGT assets (Liu, 2018). As per the

“sec 128-15, ITAA 1997” when it is noticed that the asset forms the part of post-CGT asset

of the deceased, the beneficiary is assumed to have acquired the asset on the day of death of

deceased based on the present case base.

While “sec 118-195” provides explanation regarding the inherited main residence

(Lieuallen & Shurtz, 2018). Under this provision, when it is noticed that the asses forms the

11TAXATION LAW

main residence of the deceased and it not used for generating assessable income such as

renting out or performing any business activities, the cost base to the beneficiary represents

the market value on the day of demise (Trad & Freudenberg, 2018). Furthermore, where the

asset is regarded as the main residence of the decease and not used for producing assessable

income, the beneficiary in this can inherit the exemption on main residence when some

specific conditions listed under “sec 118-195, ITAA 1997” are met.

As explained in the “sec 118-195, ITAA 1997”, a taxpayer is permitted to ignore any

kind of capital gains or loss that they make from the sale of dwelling that is passed to them as

the trustee or the beneficiary of the deceased estate on meeting some specific criteria (Minas

et al., 2018). In the meantime, “sec 118-195, ITAA 1997” provides the permission to the

taxpayer, as a legal heir, to ignore any form of capital gains or loss in respect of the previous

residence of the deceased person if any one of the below listed criteria is satisfied;

(1). The taxpayer has sold their interest of ownership in the asset inside the time span

of two years following the demise of the deceased or inside the longer time span as

permitted by the taxation commissioner (Siebert, 2019); or

(2). The taxpayer has not sold their ownership interest inside the timespan of two

years, the house was, from the day of the demise until the ownership of the taxpayer

ended; the main house was;

(a). The spouse of the deceased was alive during the time of the demise

(b). an individual that had the right of occupying the dwelling under the will of

the deceased or as the beneficiary of the estate.

The sale of the CGT assets results in the CGT event A1 under “sec 104-10, ITAA

1997”. An asset is usually described as the pre-CGT asset if the asset has been acquired by

the taxpayer before 20th September 1985 (Krever & Sadiq, 2019). Any asset that are acquired

main residence of the deceased and it not used for generating assessable income such as

renting out or performing any business activities, the cost base to the beneficiary represents

the market value on the day of demise (Trad & Freudenberg, 2018). Furthermore, where the

asset is regarded as the main residence of the decease and not used for producing assessable

income, the beneficiary in this can inherit the exemption on main residence when some

specific conditions listed under “sec 118-195, ITAA 1997” are met.

As explained in the “sec 118-195, ITAA 1997”, a taxpayer is permitted to ignore any

kind of capital gains or loss that they make from the sale of dwelling that is passed to them as

the trustee or the beneficiary of the deceased estate on meeting some specific criteria (Minas

et al., 2018). In the meantime, “sec 118-195, ITAA 1997” provides the permission to the

taxpayer, as a legal heir, to ignore any form of capital gains or loss in respect of the previous

residence of the deceased person if any one of the below listed criteria is satisfied;

(1). The taxpayer has sold their interest of ownership in the asset inside the time span

of two years following the demise of the deceased or inside the longer time span as

permitted by the taxation commissioner (Siebert, 2019); or

(2). The taxpayer has not sold their ownership interest inside the timespan of two

years, the house was, from the day of the demise until the ownership of the taxpayer

ended; the main house was;

(a). The spouse of the deceased was alive during the time of the demise

(b). an individual that had the right of occupying the dwelling under the will of

the deceased or as the beneficiary of the estate.

The sale of the CGT assets results in the CGT event A1 under “sec 104-10, ITAA

1997”. An asset is usually described as the pre-CGT asset if the asset has been acquired by

the taxpayer before 20th September 1985 (Krever & Sadiq, 2019). Any asset that are acquired

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.