Taxation Law 2: Fringe Benefits Tax and Income Tax Analysis

VerifiedAdded on 2020/05/16

|12

|2130

|63

Homework Assignment

AI Summary

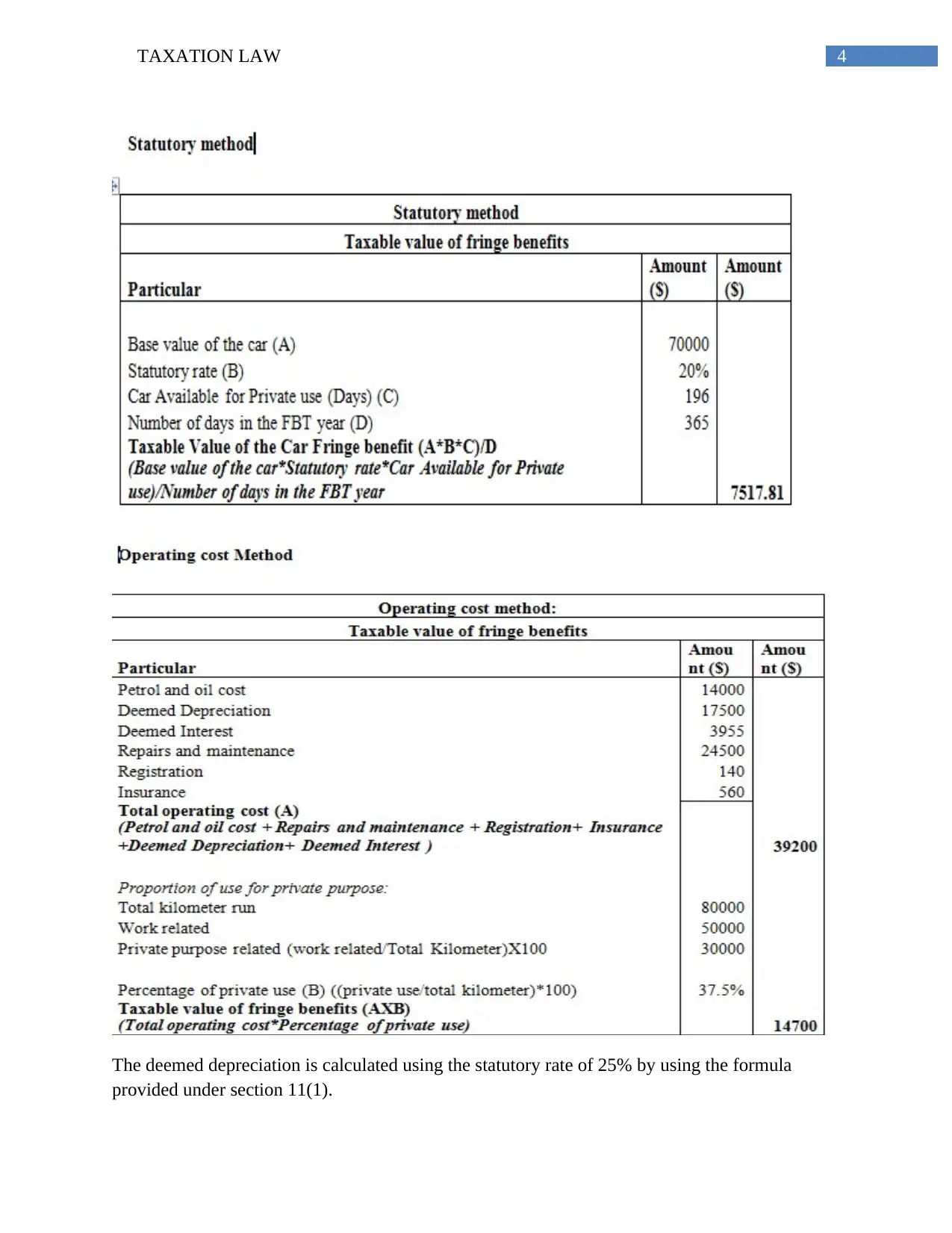

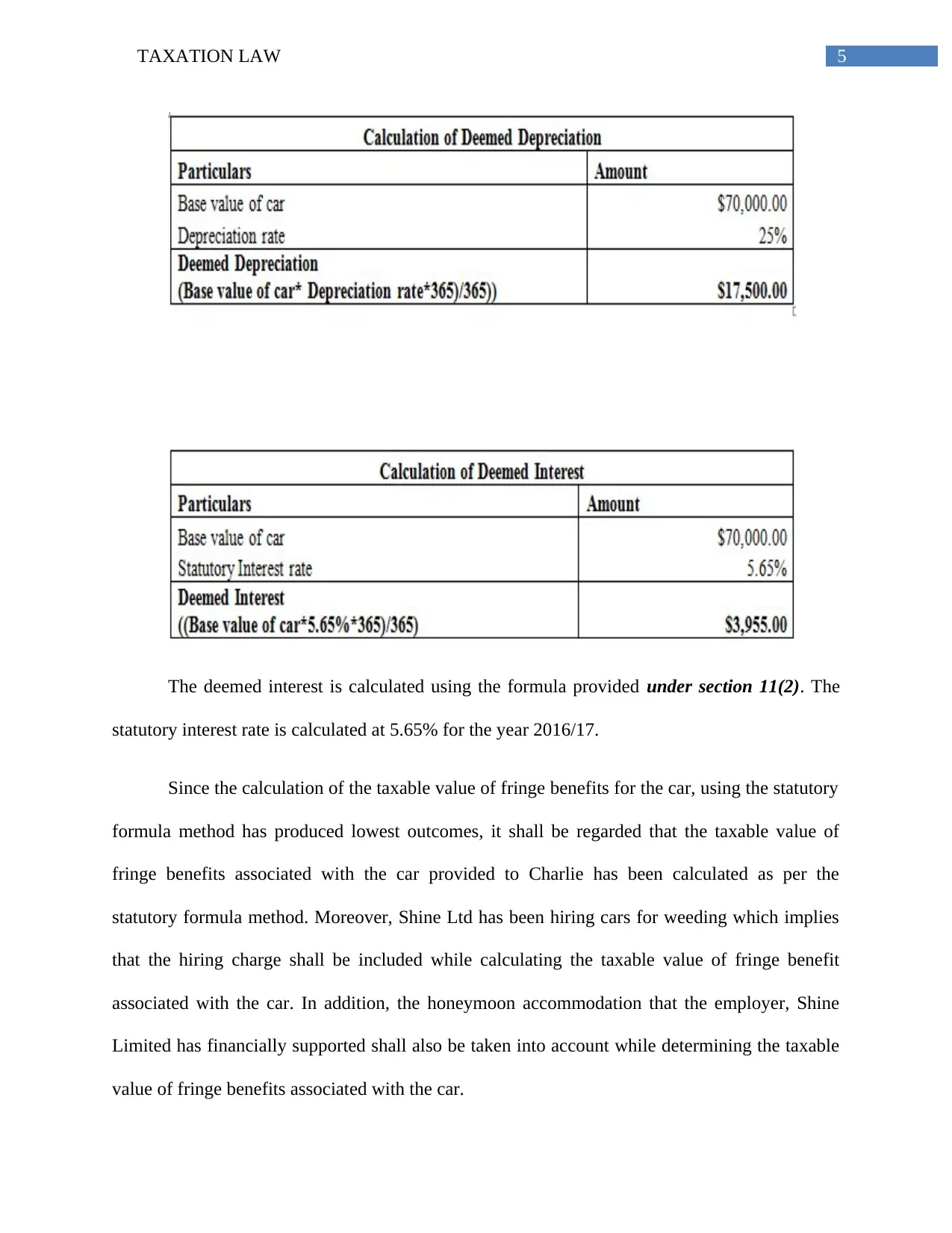

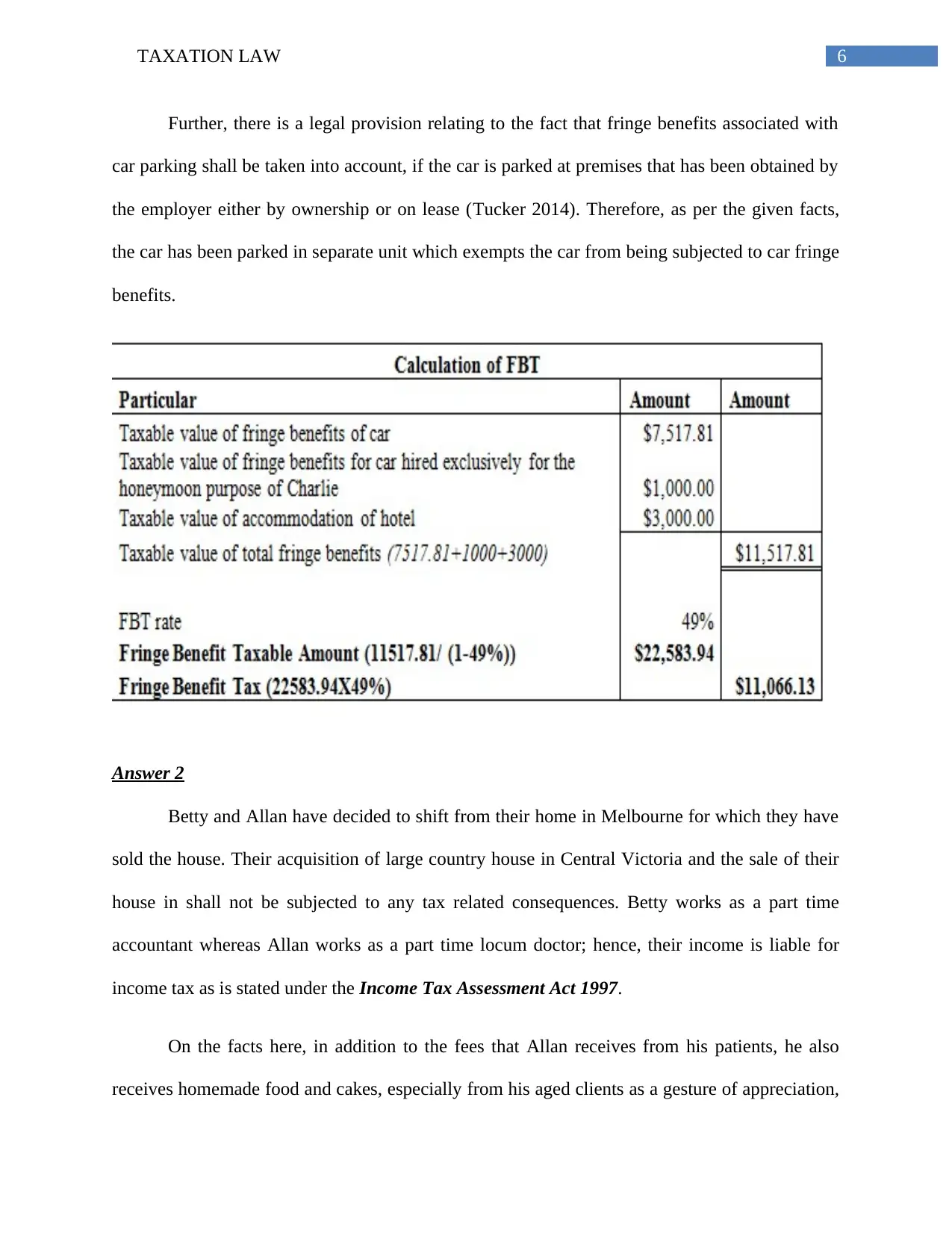

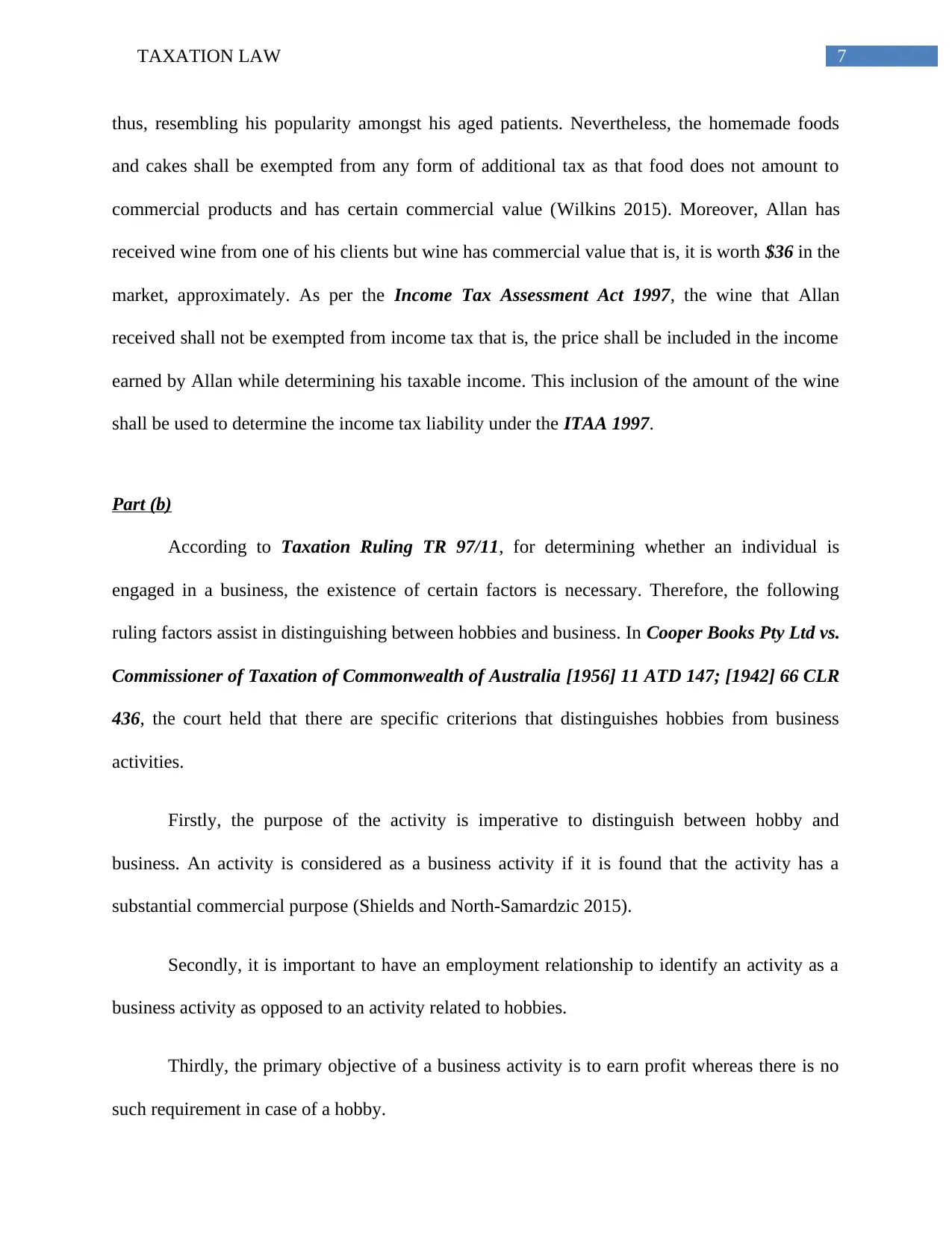

This assignment solution addresses various aspects of Australian taxation law, specifically focusing on Fringe Benefits Tax (FBT) and Income Tax. The solution begins by defining fringe benefits and their tax implications, particularly concerning car fringe benefits, detailing the statutory formula method and the operating cost method for calculating taxable values. The case facts involve an employer providing a car to an employee and the associated tax liabilities. The assignment then examines income tax implications for individuals, including the tax treatment of non-monetary benefits such as homemade food and wine. It further explores the criteria distinguishing business activities from hobbies, referencing relevant court cases and taxation rulings. The solution concludes by analyzing the tax implications of a barter system, emphasizing its treatment under the Income Tax Assessment Act 1997 and the Goods and Services Tax (GST) legislation, ensuring such transactions are treated equally to cash and credit transactions. The assignment demonstrates an understanding of relevant legislation and provides practical application of tax principles.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.