Taxation Law Assignment: University Taxation Law Principles and Cases

VerifiedAdded on 2020/04/07

|13

|2133

|46

Homework Assignment

AI Summary

This taxation law assignment presents five case studies concerning various aspects of Australian taxation law. The first case analyzes the calculation of capital gains and losses, referencing "Section 108-20 of the ITAA 1997" and "Section 108-10 of ITAA 1997." The second case focuses on Fringe Benefits Tax (FBT) and relevant rulings like "Taxation Ruling of TR 93/6." The third case examines the allocation of losses from a jointly owned rental property, citing "Taxation rulings of TR 93/32" and "F.C. of T. v McDonald (1987)." The fourth case discusses tax avoidance, referencing "IRC v Duke of Westminster [1936] AC 1" and the "WT Ramsay v. IRC principle." The final case study explores the assessment of income from the sale of timber, referencing "subsection 6 (1) of the Income Tax Assessment Act 1936." The assignment includes calculations, references, and appendices to support the analysis.

1

Running head:TAXATION LAW

Taxation Law

Student Name

University Name

Running head:TAXATION LAW

Taxation Law

Student Name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Running head:TAXATION LAW

Table of Contents

Question 1: Answer- Case Study of Eric.........................................................................................4

Regulations to the case....................................................................................................................4

Application to the case.....................................................................................................................5

Questions 2 Answer: Case Study of Brian......................................................................................5

Issue.................................................................................................................................................5

Regulations to the case....................................................................................................................5

Application to the case.....................................................................................................................5

Question 3: Case study of Jack and Jill...........................................................................................7

Issue.................................................................................................................................................7

Regulations to the case....................................................................................................................7

Application to the case.....................................................................................................................7

Question 4: “IRC v Duke of Westminster [1936] AC 1”.................................................................8

Question 5: Case study of Bill.........................................................................................................8

Regulations to the case....................................................................................................................9

Application to the case.....................................................................................................................9

References and Bibliography.........................................................................................................10

Appendices....................................................................................................................................12

Calculations for Question 2...........................................................................................................13

Running head:TAXATION LAW

Table of Contents

Question 1: Answer- Case Study of Eric.........................................................................................4

Regulations to the case....................................................................................................................4

Application to the case.....................................................................................................................5

Questions 2 Answer: Case Study of Brian......................................................................................5

Issue.................................................................................................................................................5

Regulations to the case....................................................................................................................5

Application to the case.....................................................................................................................5

Question 3: Case study of Jack and Jill...........................................................................................7

Issue.................................................................................................................................................7

Regulations to the case....................................................................................................................7

Application to the case.....................................................................................................................7

Question 4: “IRC v Duke of Westminster [1936] AC 1”.................................................................8

Question 5: Case study of Bill.........................................................................................................8

Regulations to the case....................................................................................................................9

Application to the case.....................................................................................................................9

References and Bibliography.........................................................................................................10

Appendices....................................................................................................................................12

Calculations for Question 2...........................................................................................................13

3

Running head:TAXATION LAW

Running head:TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Running head:TAXATION LAW

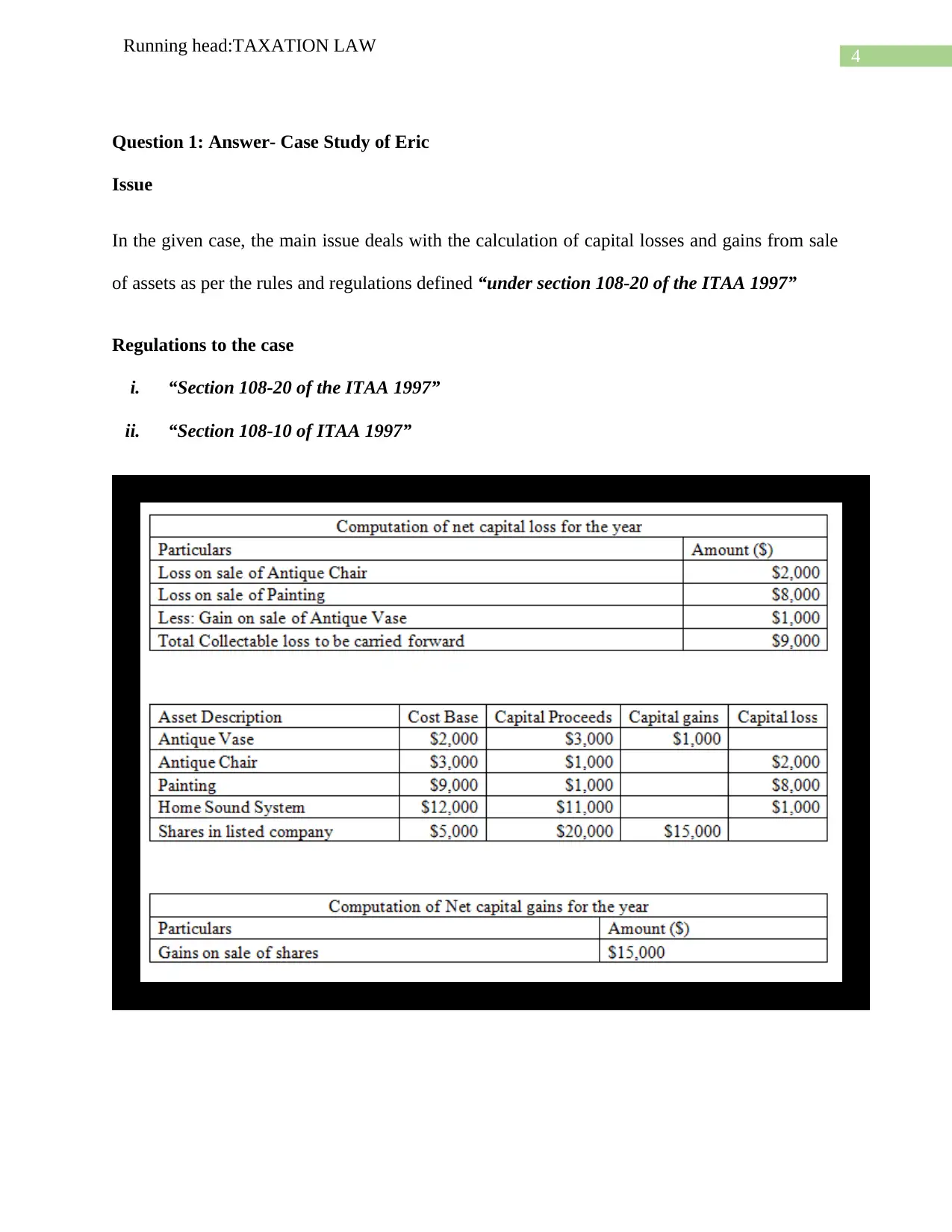

Question 1: Answer- Case Study of Eric

Issue

In the given case, the main issue deals with the calculation of capital losses and gains from sale

of assets as per the rules and regulations defined “under section 108-20 of the ITAA 1997”

Regulations to the case

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Running head:TAXATION LAW

Question 1: Answer- Case Study of Eric

Issue

In the given case, the main issue deals with the calculation of capital losses and gains from sale

of assets as per the rules and regulations defined “under section 108-20 of the ITAA 1997”

Regulations to the case

i. “Section 108-20 of the ITAA 1997”

ii. “Section 108-10 of ITAA 1997”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Running head:TAXATION LAW

Application to the case

The given analysis has been done as per Australian Taxation rules and regulations. In accordance

to “section 108-20 of the ITAA 1997”, loss of $1,000 for the home sound system cannot be

considered as set off, because losses cannot be considered on disposal of any kind of personal

assets for any considered parties (Fry 2017). In the given case, Eric obtained a considerable

amount of profit $15000 from the sale of ordinary assets. This offset can be considered as per

“Section 108-10 of ITAA 1997”.

Conclusion

From the above analysis, it can be concluded that Eric has gained profit from the sale of ordinary

assets, therefore, he cannot offset the loss from the given collectables. This is also inevitable

from the analysis and calculation as shown in the following table.

Questions 2 Answer: Case Study of Brian

Issue

The main issue highlighted in this case us with regards ascertainment of FBT as per ““Taxation

Ruling of TR 93/6”.

Regulations to the case

“Taxation Ruling of TR 93/6”

Application to the case

The application of the given case can be evaluated with the help of computation of FBT

Running head:TAXATION LAW

Application to the case

The given analysis has been done as per Australian Taxation rules and regulations. In accordance

to “section 108-20 of the ITAA 1997”, loss of $1,000 for the home sound system cannot be

considered as set off, because losses cannot be considered on disposal of any kind of personal

assets for any considered parties (Fry 2017). In the given case, Eric obtained a considerable

amount of profit $15000 from the sale of ordinary assets. This offset can be considered as per

“Section 108-10 of ITAA 1997”.

Conclusion

From the above analysis, it can be concluded that Eric has gained profit from the sale of ordinary

assets, therefore, he cannot offset the loss from the given collectables. This is also inevitable

from the analysis and calculation as shown in the following table.

Questions 2 Answer: Case Study of Brian

Issue

The main issue highlighted in this case us with regards ascertainment of FBT as per ““Taxation

Ruling of TR 93/6”.

Regulations to the case

“Taxation Ruling of TR 93/6”

Application to the case

The application of the given case can be evaluated with the help of computation of FBT

6

Running head:TAXATION LAW

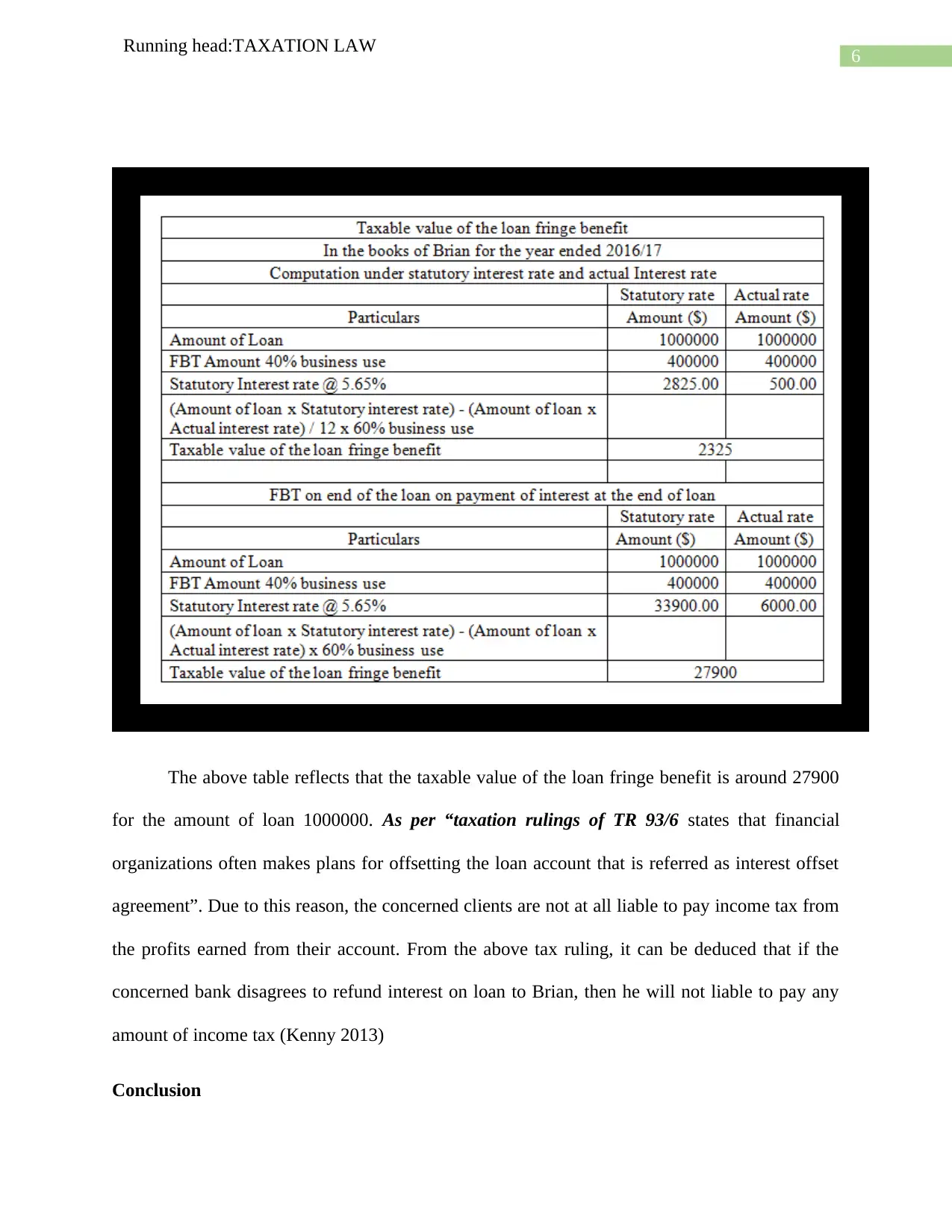

The above table reflects that the taxable value of the loan fringe benefit is around 27900

for the amount of loan 1000000. As per “taxation rulings of TR 93/6 states that financial

organizations often makes plans for offsetting the loan account that is referred as interest offset

agreement”. Due to this reason, the concerned clients are not at all liable to pay income tax from

the profits earned from their account. From the above tax ruling, it can be deduced that if the

concerned bank disagrees to refund interest on loan to Brian, then he will not liable to pay any

amount of income tax (Kenny 2013)

Conclusion

Running head:TAXATION LAW

The above table reflects that the taxable value of the loan fringe benefit is around 27900

for the amount of loan 1000000. As per “taxation rulings of TR 93/6 states that financial

organizations often makes plans for offsetting the loan account that is referred as interest offset

agreement”. Due to this reason, the concerned clients are not at all liable to pay income tax from

the profits earned from their account. From the above tax ruling, it can be deduced that if the

concerned bank disagrees to refund interest on loan to Brian, then he will not liable to pay any

amount of income tax (Kenny 2013)

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Running head:TAXATION LAW

It can be concluded that Brian will not liable to pay any kind of income tax if the bank do not

refund his interest on loan.

Question 3: Case study of Jack and Jill

Issue

The given case deals with the issue regarding allocation of loss amount derived from the rental

property which is under joint ownership of Jack and Jill.

Regulations to the case

“Taxation rulings of TR 93/32”

“F.C. of T. v McDonald (1987)”

Application to the case

As per the “Taxation rulings of TR 93/32”, co-ownership in any kind of rental property

can be considered as an ordinary partnership. This is also for the purpose of paying appropriate

income tax (Saad 2014). This is applicable for any kind of individual parties. In the given case

study, Jack and Jill has a rental property, under their co-ownership which is also mainly for

taxable purposes and cannot be considered as partnership under general law. However, since

they are co-owners for the given property, then they are bound to share the profit and losses

which are arisen from their given rental property.

With reference to the case, “F.C. of T. v McDonald (1987)”, the tax payer and his wife

jointly owned two state units. The rate of percentage of profit and losses was pre-determined by

Running head:TAXATION LAW

It can be concluded that Brian will not liable to pay any kind of income tax if the bank do not

refund his interest on loan.

Question 3: Case study of Jack and Jill

Issue

The given case deals with the issue regarding allocation of loss amount derived from the rental

property which is under joint ownership of Jack and Jill.

Regulations to the case

“Taxation rulings of TR 93/32”

“F.C. of T. v McDonald (1987)”

Application to the case

As per the “Taxation rulings of TR 93/32”, co-ownership in any kind of rental property

can be considered as an ordinary partnership. This is also for the purpose of paying appropriate

income tax (Saad 2014). This is applicable for any kind of individual parties. In the given case

study, Jack and Jill has a rental property, under their co-ownership which is also mainly for

taxable purposes and cannot be considered as partnership under general law. However, since

they are co-owners for the given property, then they are bound to share the profit and losses

which are arisen from their given rental property.

With reference to the case, “F.C. of T. v McDonald (1987)”, the tax payer and his wife

jointly owned two state units. The rate of percentage of profit and losses was pre-determined by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Running head:TAXATION LAW

both the parties. Similarly, in this case, since it is not pre-determined, therefore, the losses will be

divided equally.

Conclusion

It can be concluded that the losses between Jack and Jill will be divided equally and joint

ownership business do not account for partnership business.

Question 4: “IRC v Duke of Westminster [1936] AC 1”

The given case “IRC v Duke of Westminster [1936] AC 1” is considered as one of the

prime examples of occurrence of tax avoidance. This case depicts one principle that each tax

payer is allowed to order all his/her affairs. However, this ruling cannot be considered that useful

in case of complex tax structures under the law.

“WT Ramsay v. IRC principle” can be considered as more restrictive in comparison to

the previous case discuss above. This principle reflects that if an individual is successful in the

given result, then he is not bound to pay any increased amount of tax and it also allows

individuals as well as corporates to restructure all their agreements in order to meet their

respective objectives of lowering down the taxable amount.

Question 5: Case study of Bill

Issue

The given case study deals with the “assessment of income from the sale of felled timber is

deduced under subsection 6 (1) of the Income Tax Assessment Act 1936”

Running head:TAXATION LAW

both the parties. Similarly, in this case, since it is not pre-determined, therefore, the losses will be

divided equally.

Conclusion

It can be concluded that the losses between Jack and Jill will be divided equally and joint

ownership business do not account for partnership business.

Question 4: “IRC v Duke of Westminster [1936] AC 1”

The given case “IRC v Duke of Westminster [1936] AC 1” is considered as one of the

prime examples of occurrence of tax avoidance. This case depicts one principle that each tax

payer is allowed to order all his/her affairs. However, this ruling cannot be considered that useful

in case of complex tax structures under the law.

“WT Ramsay v. IRC principle” can be considered as more restrictive in comparison to

the previous case discuss above. This principle reflects that if an individual is successful in the

given result, then he is not bound to pay any increased amount of tax and it also allows

individuals as well as corporates to restructure all their agreements in order to meet their

respective objectives of lowering down the taxable amount.

Question 5: Case study of Bill

Issue

The given case study deals with the “assessment of income from the sale of felled timber is

deduced under subsection 6 (1) of the Income Tax Assessment Act 1936”

9

Running head:TAXATION LAW

Regulations to the case “Subsection 6 (1) of the Income Tax Assessment Act 1936” “McCauley v. The Federal Commissioner of Taxation”

Application to the case

In the given case study, Bill is the owner of a piece of land which consists of seven pine

trees. He primarily aimed for grazing of sheep and wanted to clear it. He finds a lodging

company who is willing to pay him $100 for every 100 meters of land. As per “taxation ruling

related to 95/6” gives a proper view regarding the tax consequences for income generated from

the activities of primary production. The ruling states that there is a limit to the receipts derived

from the sale of timber (James 2016). In the given case, Bill is the owner of land, but he did not

plant trees in the given land. However, the whole amount that constitutes from the sale of timber

is his assessable income. Therefore, it can be inferred that the considered trees are taken as

assessable income of the tax payers “under subsection 6 (1) of the Income Tax Assessment Act

1936”. On the contrary, if Bill pays an amount of $50,000, then the receipts can be considered as

Royalties, as per section 26 (f). The total amount earned by Bill as royalty is his assessable

income.

Conclusion

From the above analysis, it can be inferred that income from cutting timber from trees

can be considered as taxable income for Bill as per “subsection 6 (1) of the ITAA 1997”.

Running head:TAXATION LAW

Regulations to the case “Subsection 6 (1) of the Income Tax Assessment Act 1936” “McCauley v. The Federal Commissioner of Taxation”

Application to the case

In the given case study, Bill is the owner of a piece of land which consists of seven pine

trees. He primarily aimed for grazing of sheep and wanted to clear it. He finds a lodging

company who is willing to pay him $100 for every 100 meters of land. As per “taxation ruling

related to 95/6” gives a proper view regarding the tax consequences for income generated from

the activities of primary production. The ruling states that there is a limit to the receipts derived

from the sale of timber (James 2016). In the given case, Bill is the owner of land, but he did not

plant trees in the given land. However, the whole amount that constitutes from the sale of timber

is his assessable income. Therefore, it can be inferred that the considered trees are taken as

assessable income of the tax payers “under subsection 6 (1) of the Income Tax Assessment Act

1936”. On the contrary, if Bill pays an amount of $50,000, then the receipts can be considered as

Royalties, as per section 26 (f). The total amount earned by Bill as royalty is his assessable

income.

Conclusion

From the above analysis, it can be inferred that income from cutting timber from trees

can be considered as taxable income for Bill as per “subsection 6 (1) of the ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Running head:TAXATION LAW

References and Bibliography

Brennan, G., 2016. The church on tax reform?. St Mark's Review, (235), p.1.

Campbell, S., 2015. A mater of trusts: CGT issues when creating and dealing with

UPEs. Taxation in Australia, 50(6), p.332.

Choi, S.K., 2016. The Determinants and Trends in Public-Private Wage and Fringe Benefit

Differential.

Daley, J. and Wood, D., 2015. Fiscal challenges for Australia. Grattan Institute.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office. The APPEA Journal, 57(1), pp.49-63.

Gabbay, D.M. and Smets, P. eds., 2013. Quantified Representation of Uncertainty and

Imprecision (Vol. 1). Springer Science & Business Media.

Hogg, C. and Bush, A., 2012. Genotyping in primary ciliary dyskinesia: ready for prime time, or

a fringe benefit?. Thorax, 67(5), pp.377-378.

Hussein, A., 2015. The use of triangulation in social sciences research: Can qualitative and

quantitative methods be combined?. Journal of Comparative Social Work, 4(1).

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), pp.345-362.

Jorgensen, R., 2017. Division 7A structuring: The contortionist revisited. Tax Specialist, 20(3),

p.118.

Running head:TAXATION LAW

References and Bibliography

Brennan, G., 2016. The church on tax reform?. St Mark's Review, (235), p.1.

Campbell, S., 2015. A mater of trusts: CGT issues when creating and dealing with

UPEs. Taxation in Australia, 50(6), p.332.

Choi, S.K., 2016. The Determinants and Trends in Public-Private Wage and Fringe Benefit

Differential.

Daley, J. and Wood, D., 2015. Fiscal challenges for Australia. Grattan Institute.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office. The APPEA Journal, 57(1), pp.49-63.

Gabbay, D.M. and Smets, P. eds., 2013. Quantified Representation of Uncertainty and

Imprecision (Vol. 1). Springer Science & Business Media.

Hogg, C. and Bush, A., 2012. Genotyping in primary ciliary dyskinesia: ready for prime time, or

a fringe benefit?. Thorax, 67(5), pp.377-378.

Hussein, A., 2015. The use of triangulation in social sciences research: Can qualitative and

quantitative methods be combined?. Journal of Comparative Social Work, 4(1).

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), pp.345-362.

Jorgensen, R., 2017. Division 7A structuring: The contortionist revisited. Tax Specialist, 20(3),

p.118.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Running head:TAXATION LAW

Karlsson, S. and Kullingsjö, L.H., 2013, November. GPS measurement of Swedish car

movements for assessment of possible electrification. InElectric Vehicle Symposium and

Exhibition (EVS27), 2013 World (pp. 1-14). IEEE.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Lin, C.Y.Y., Edvinsson, L., Chen, J. and Beding, T., 2013. National intellectual capital and the

financial crisis in Australia, Canada, Japan, New Zealand, and the United States. Springer

Science & Business Media.

Milton, 2013. The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Nguyen, P. and Rahman, N., 2015. Which governance characteristics affect the incidence of

divestitures in Australia?. Australian Journal of Management, 40(2), pp.351-374.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

Running head:TAXATION LAW

Karlsson, S. and Kullingsjö, L.H., 2013, November. GPS measurement of Swedish car

movements for assessment of possible electrification. InElectric Vehicle Symposium and

Exhibition (EVS27), 2013 World (pp. 1-14). IEEE.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Lin, C.Y.Y., Edvinsson, L., Chen, J. and Beding, T., 2013. National intellectual capital and the

financial crisis in Australia, Canada, Japan, New Zealand, and the United States. Springer

Science & Business Media.

Milton, 2013. The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Nguyen, P. and Rahman, N., 2015. Which governance characteristics affect the incidence of

divestitures in Australia?. Australian Journal of Management, 40(2), pp.351-374.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

12

Running head:TAXATION LAW

Appendices

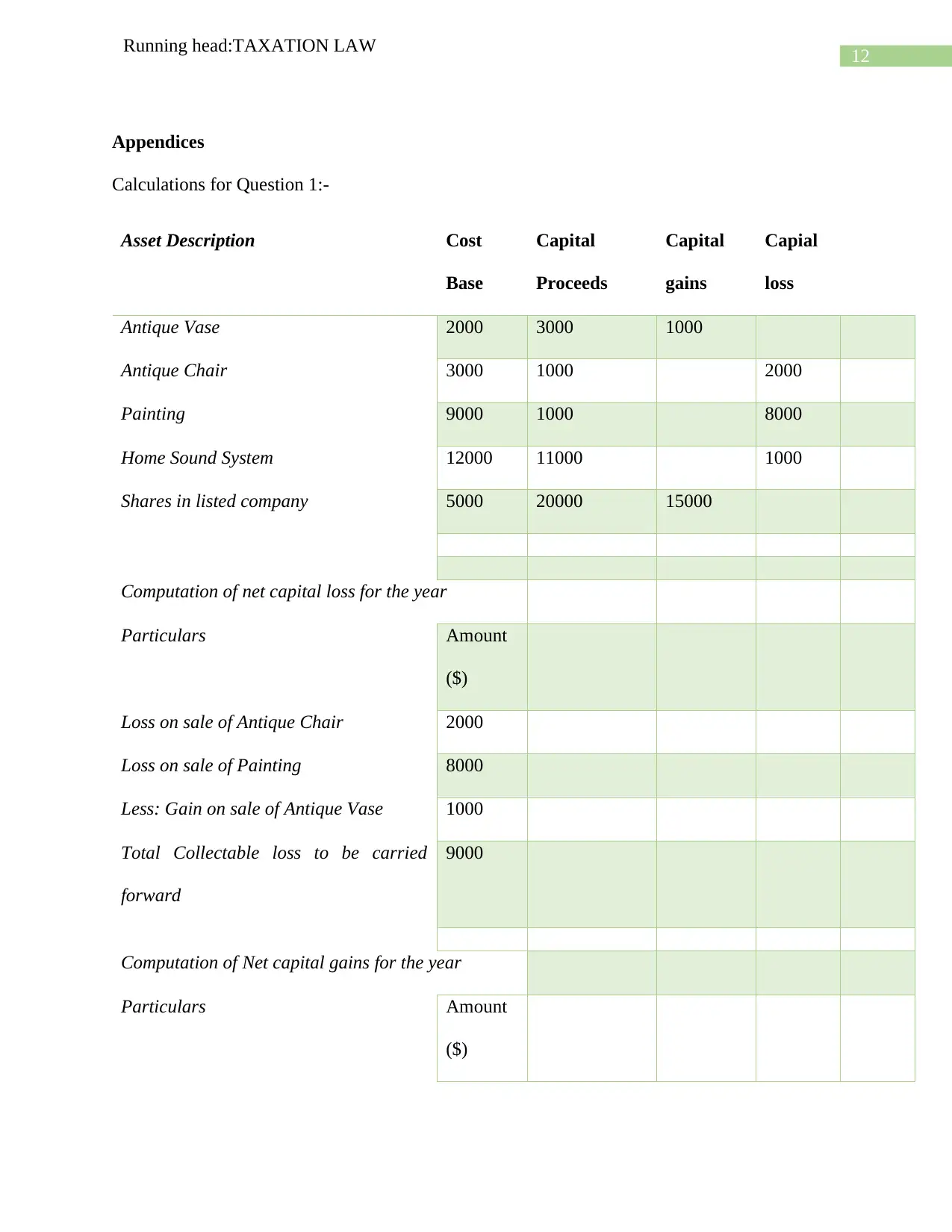

Calculations for Question 1:-

Asset Description Cost

Base

Capital

Proceeds

Capital

gains

Capial

loss

Antique Vase 2000 3000 1000

Antique Chair 3000 1000 2000

Painting 9000 1000 8000

Home Sound System 12000 11000 1000

Shares in listed company 5000 20000 15000

Computation of net capital loss for the year

Particulars Amount

($)

Loss on sale of Antique Chair 2000

Loss on sale of Painting 8000

Less: Gain on sale of Antique Vase 1000

Total Collectable loss to be carried

forward

9000

Computation of Net capital gains for the year

Particulars Amount

($)

Running head:TAXATION LAW

Appendices

Calculations for Question 1:-

Asset Description Cost

Base

Capital

Proceeds

Capital

gains

Capial

loss

Antique Vase 2000 3000 1000

Antique Chair 3000 1000 2000

Painting 9000 1000 8000

Home Sound System 12000 11000 1000

Shares in listed company 5000 20000 15000

Computation of net capital loss for the year

Particulars Amount

($)

Loss on sale of Antique Chair 2000

Loss on sale of Painting 8000

Less: Gain on sale of Antique Vase 1000

Total Collectable loss to be carried

forward

9000

Computation of Net capital gains for the year

Particulars Amount

($)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.