Taxation Law Assignment: Tax Implications and Advice for Harpreet Kaur

VerifiedAdded on 2022/11/26

|9

|1312

|211

Homework Assignment

AI Summary

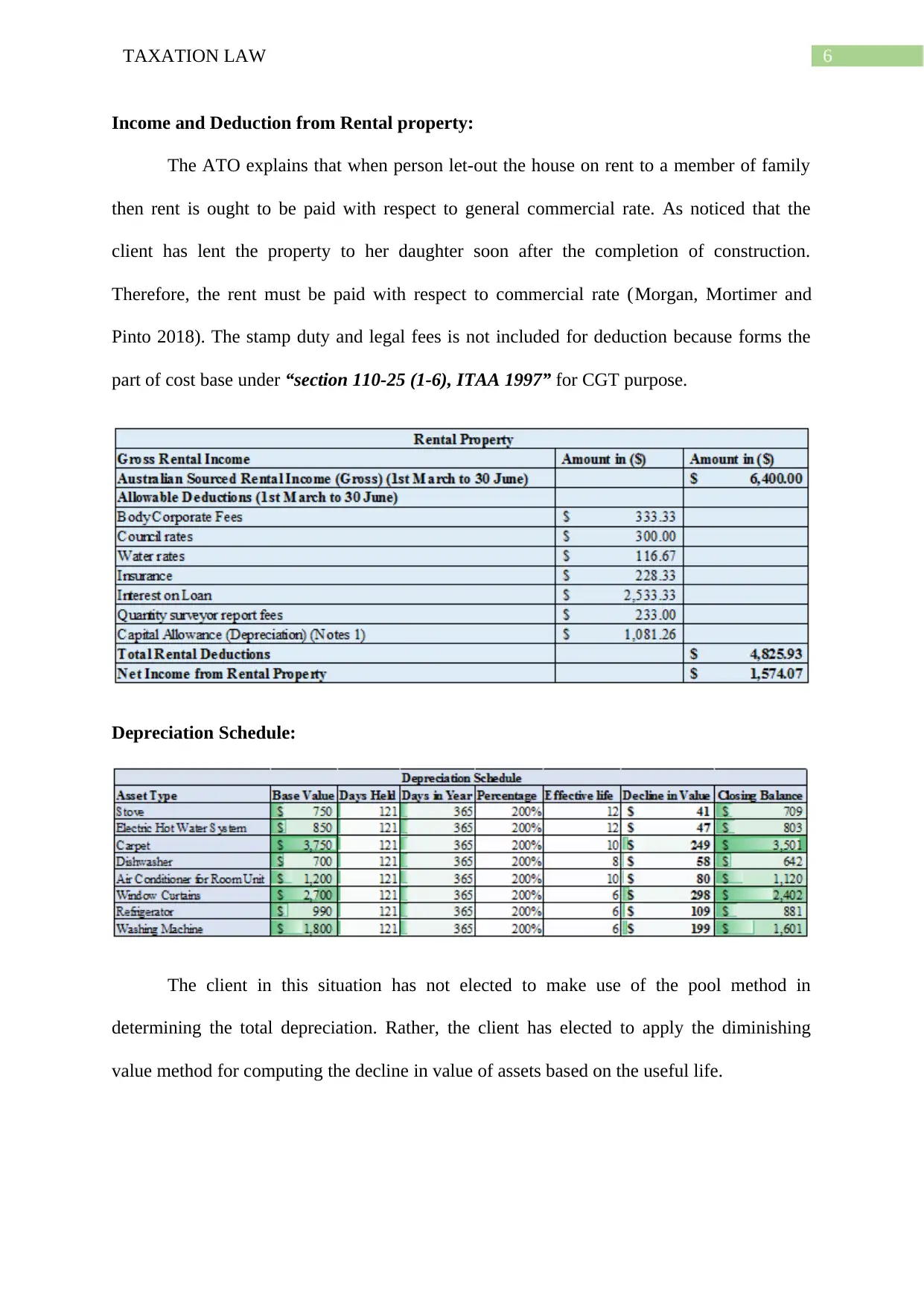

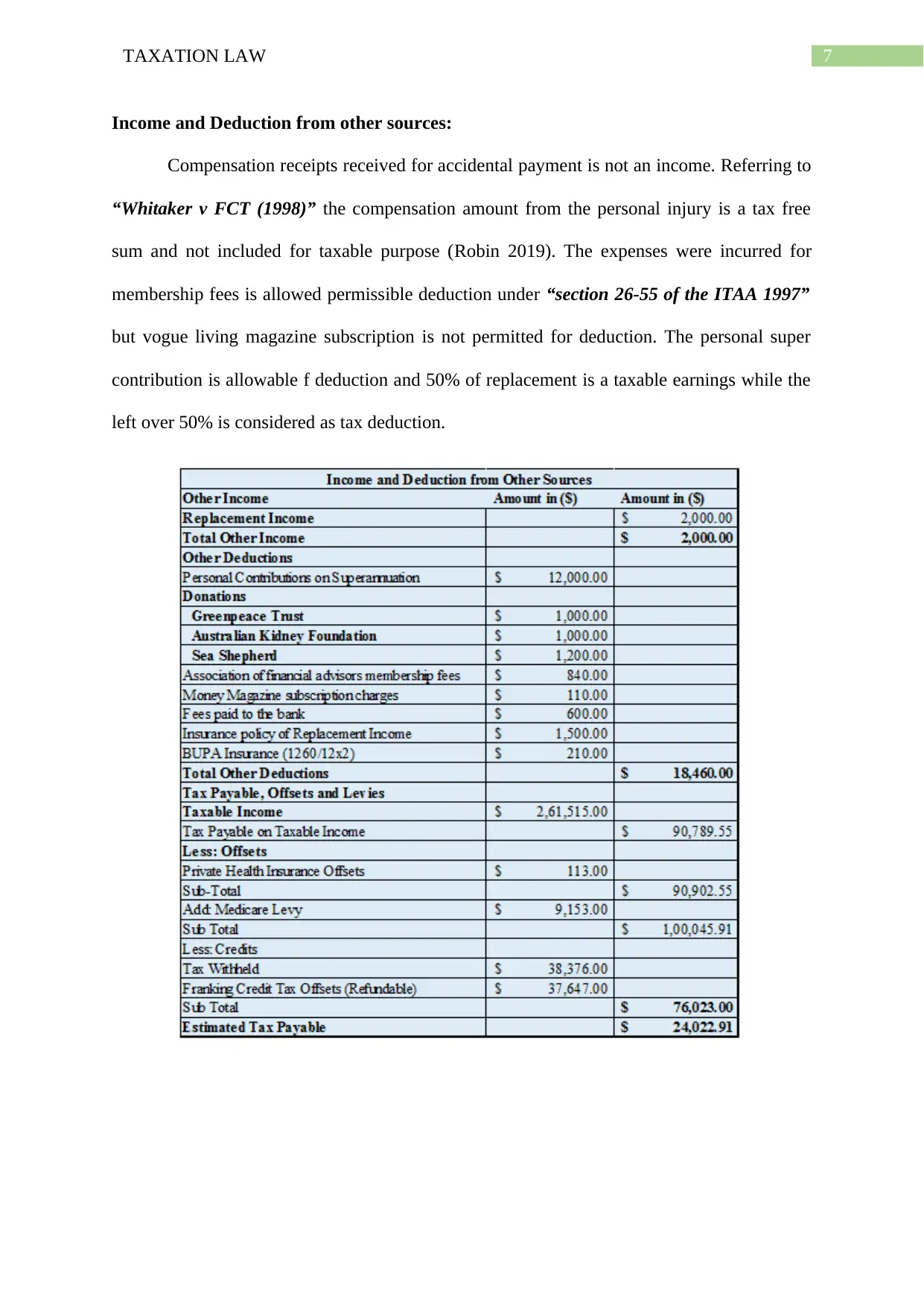

This assignment solution addresses a taxation law case study for an individual, Harpreet Kaur, focusing on her income and tax liabilities for the income year. The solution includes a letter of advice from Pitchers Tax Partners, outlining the scope of the advice and summarizing key tax implications. The analysis covers various income sources such as salary, dividends, and capital gains from the sale of inherited shares (BHP and MYR). It also addresses deductions related to work expenses, car expenses, and rental property income and expenses. The assignment provides a detailed breakdown of each income and deduction category, including references to relevant sections of the ITAA 1997 and ITAA 1936. The solution also includes a depreciation schedule and discusses the tax treatment of compensation receipts and membership fees. The advice provided aims to help Harpreet Kaur understand her tax position and manage her expenses effectively, with recommendations for offsetting capital losses against gains and ensuring commercial rates are applied for rental property transactions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.