HI6028 Taxation Law Assignment: Input Tax Credit and CGT Analysis

VerifiedAdded on 2022/11/09

|12

|2481

|479

Homework Assignment

AI Summary

This assignment solution addresses two key questions related to Australian taxation law. The first question focuses on the concept of input tax credit, examining the circumstances under which a business, specifically City Sky Co, can claim it for the creditable acquisition of land. It analyzes the relevant legislation, including GSTR 2008/1 and Division 11, and applies them to the scenario, considering factors like creditable purpose and assessable supplies. The second question delves into capital gains tax (CGT), detailing the calculation of capital gains and losses for Emma from the sale of various assets, including land, shares in Rio Tinto, stamps, and a grand piano. The solution outlines the cost base elements, pre- and post-CGT assets, collectables, and personal use assets, providing a comprehensive analysis of the tax implications for each asset sale, referencing relevant sections of the ITAA 1997.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The question is concerned with the issues of claim regarding the input tax credit

arising from making the creditable acquisition.

Laws:

The “GSTR 2008/1” says that when a taxpayer aspires to claim the input tax credit

they should in such situation make the creditable acquisition. For making a creditable

acquisition or importation the taxpayer in such situation needs to make the creditable

acquisition or import either exclusively or partially for the creditable purpose (Bidin et al.

2014). The “GSTR 2008/1” provides the explanation regarding the factor which provides the

guidance in ascertaining whether the purchase made by a company is for the creditable

purpose. The ruling addresses that

A. Whether the entity has made the acquisition at the time of conducting the enterprise or

whether the purchase made is personal or domestic in nature.

B. The ruling also addresses that whether the acquisition that is made by the entity, is

linked with the construction of taxable supplies which would be input taxed.

The taxpayers must denote that the common entitlement arises regarding the input tax

credit originates when the entity makes the creditable acquisition. “Division 11” is usually

associated with the creditable purchase (Mawuli, 2014). As stated under “sec 11-5”, a

business makes the creditable acquisition if they purchase anything that is totally or

somewhat for the creditable purpose and the supply of a particular item for the entity is

viewed as the assessable supply and the business is registered for GST.

Answer to question 1:

Issues:

The question is concerned with the issues of claim regarding the input tax credit

arising from making the creditable acquisition.

Laws:

The “GSTR 2008/1” says that when a taxpayer aspires to claim the input tax credit

they should in such situation make the creditable acquisition. For making a creditable

acquisition or importation the taxpayer in such situation needs to make the creditable

acquisition or import either exclusively or partially for the creditable purpose (Bidin et al.

2014). The “GSTR 2008/1” provides the explanation regarding the factor which provides the

guidance in ascertaining whether the purchase made by a company is for the creditable

purpose. The ruling addresses that

A. Whether the entity has made the acquisition at the time of conducting the enterprise or

whether the purchase made is personal or domestic in nature.

B. The ruling also addresses that whether the acquisition that is made by the entity, is

linked with the construction of taxable supplies which would be input taxed.

The taxpayers must denote that the common entitlement arises regarding the input tax

credit originates when the entity makes the creditable acquisition. “Division 11” is usually

associated with the creditable purchase (Mawuli, 2014). As stated under “sec 11-5”, a

business makes the creditable acquisition if they purchase anything that is totally or

somewhat for the creditable purpose and the supply of a particular item for the entity is

viewed as the assessable supply and the business is registered for GST.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

“Sec 11-15” further provides the explanation regarding the creditable purpose

(Rimmer, Smith and Wende 2014). Under “sec 11-15” a company that purchases things for

the creditable purpose up to the amount that they acquire the item while performing the

business activities.

The judgement handed in “HP Mercantile Pty Ltd v Commissioner of Taxation

(2005)” stated that a taxpayer would be permitted to get the input tax credit when it turns

essential that the credit is given to make sure that the output tax owed by taxpayer is not

levied on the sum which at present contains the tax outstanding at some earlier stage under

the profitable cycle (Schneider, F., Raczkowski and Mróz 2015). A taxpayer is only allowed

to get the input tax credit up to the degree that the purchaser and the supply to it satisfies the

conditions that the acquirer makes the acquisition during the ordinary course of carrying the

company and hence they are not a customer. The input tax credit is usually aimed at

offsetting the GST that is contained within the purchase that is paid for the purchase given the

purchase is exclusively for the company’s usage.

When it is noticed a supplier has made a taxable supply then they will be considered

accountable for GST on those supplies. The supplier will be considered permitted to get the

input tax credit for the acquisition that is made associated to the supplies (Braithwaite 2017).

Under “sec 11-5”, a company that is registered under the GST will be given the permission

of claiming the input tax credit for the creditable purchase that they make. “Subsection 11-15

(1)” says that a company usually acquire things while carrying on the enterprise. A clear

connection must be existent between the thing that is acquired by the company and the

enterprise being carried on.

Application:

“Sec 11-15” further provides the explanation regarding the creditable purpose

(Rimmer, Smith and Wende 2014). Under “sec 11-15” a company that purchases things for

the creditable purpose up to the amount that they acquire the item while performing the

business activities.

The judgement handed in “HP Mercantile Pty Ltd v Commissioner of Taxation

(2005)” stated that a taxpayer would be permitted to get the input tax credit when it turns

essential that the credit is given to make sure that the output tax owed by taxpayer is not

levied on the sum which at present contains the tax outstanding at some earlier stage under

the profitable cycle (Schneider, F., Raczkowski and Mróz 2015). A taxpayer is only allowed

to get the input tax credit up to the degree that the purchaser and the supply to it satisfies the

conditions that the acquirer makes the acquisition during the ordinary course of carrying the

company and hence they are not a customer. The input tax credit is usually aimed at

offsetting the GST that is contained within the purchase that is paid for the purchase given the

purchase is exclusively for the company’s usage.

When it is noticed a supplier has made a taxable supply then they will be considered

accountable for GST on those supplies. The supplier will be considered permitted to get the

input tax credit for the acquisition that is made associated to the supplies (Braithwaite 2017).

Under “sec 11-5”, a company that is registered under the GST will be given the permission

of claiming the input tax credit for the creditable purchase that they make. “Subsection 11-15

(1)” says that a company usually acquire things while carrying on the enterprise. A clear

connection must be existent between the thing that is acquired by the company and the

enterprise being carried on.

Application:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The business here City Sky Co is carrying on the business of property investment and

development. The company has recently bought a vacant land in Brisbane where he intends

to construct 15 apartments for sell. City Sky Co is registered for GST. With regard to the

GSTR 2008/1 the purchase of vacant land should be regarded as the creditable acquisition.

The creditable acquisition of land is made by City Sky Co solely for the creditable purpose.

Important factors such as the acquisition of land was made by City Sky Co while carrying on

the enterprise activities and it is associated to making the supplies which will be input taxed.

With respect to the “division 11”, the creditable acquisition that is made by the City

Sky Co will be permitted to input tax credits under “sec 11-5” (Garg et al. 2018). The land

was acquired by City Sky Co exclusively for the creditable purpose and the supply of land to

City Sky Co is an assessable supply. The company here is liable to provide the consideration

for supply and it is also registered under the GST Act 1999 (Burman et al. 2016). With regard

to “sec 11-15”, City Sky Co purchased the land for the creditable purpose only up to the

degree that the land was bought at the time of conducting the business activities.

By referring to the factual decision that was given in “HP Mercantile Pty Ltd v

Commissioner of Taxation (2005)” City Sky Co will be permitted to the input tax credit

since the credit that is permitted was to assure that the out tax owed by the company is not

levied on the sum which by now includes the tax owed under the commercial cycle. Denoting

subsection 11-15 (1) the land was acquired by the City Sky Co while carrying on its

enterprise activities and clearly there is a relation between the land acquired and carrying of

the enterprise activity.

Conclusion:

The study says that an input tax credit is permitted for claim by the City Sky Co for

the creditable acquisition of land made in the ordinary business course.

The business here City Sky Co is carrying on the business of property investment and

development. The company has recently bought a vacant land in Brisbane where he intends

to construct 15 apartments for sell. City Sky Co is registered for GST. With regard to the

GSTR 2008/1 the purchase of vacant land should be regarded as the creditable acquisition.

The creditable acquisition of land is made by City Sky Co solely for the creditable purpose.

Important factors such as the acquisition of land was made by City Sky Co while carrying on

the enterprise activities and it is associated to making the supplies which will be input taxed.

With respect to the “division 11”, the creditable acquisition that is made by the City

Sky Co will be permitted to input tax credits under “sec 11-5” (Garg et al. 2018). The land

was acquired by City Sky Co exclusively for the creditable purpose and the supply of land to

City Sky Co is an assessable supply. The company here is liable to provide the consideration

for supply and it is also registered under the GST Act 1999 (Burman et al. 2016). With regard

to “sec 11-15”, City Sky Co purchased the land for the creditable purpose only up to the

degree that the land was bought at the time of conducting the business activities.

By referring to the factual decision that was given in “HP Mercantile Pty Ltd v

Commissioner of Taxation (2005)” City Sky Co will be permitted to the input tax credit

since the credit that is permitted was to assure that the out tax owed by the company is not

levied on the sum which by now includes the tax owed under the commercial cycle. Denoting

subsection 11-15 (1) the land was acquired by the City Sky Co while carrying on its

enterprise activities and clearly there is a relation between the land acquired and carrying of

the enterprise activity.

Conclusion:

The study says that an input tax credit is permitted for claim by the City Sky Co for

the creditable acquisition of land made in the ordinary business course.

5TAXATION LAW

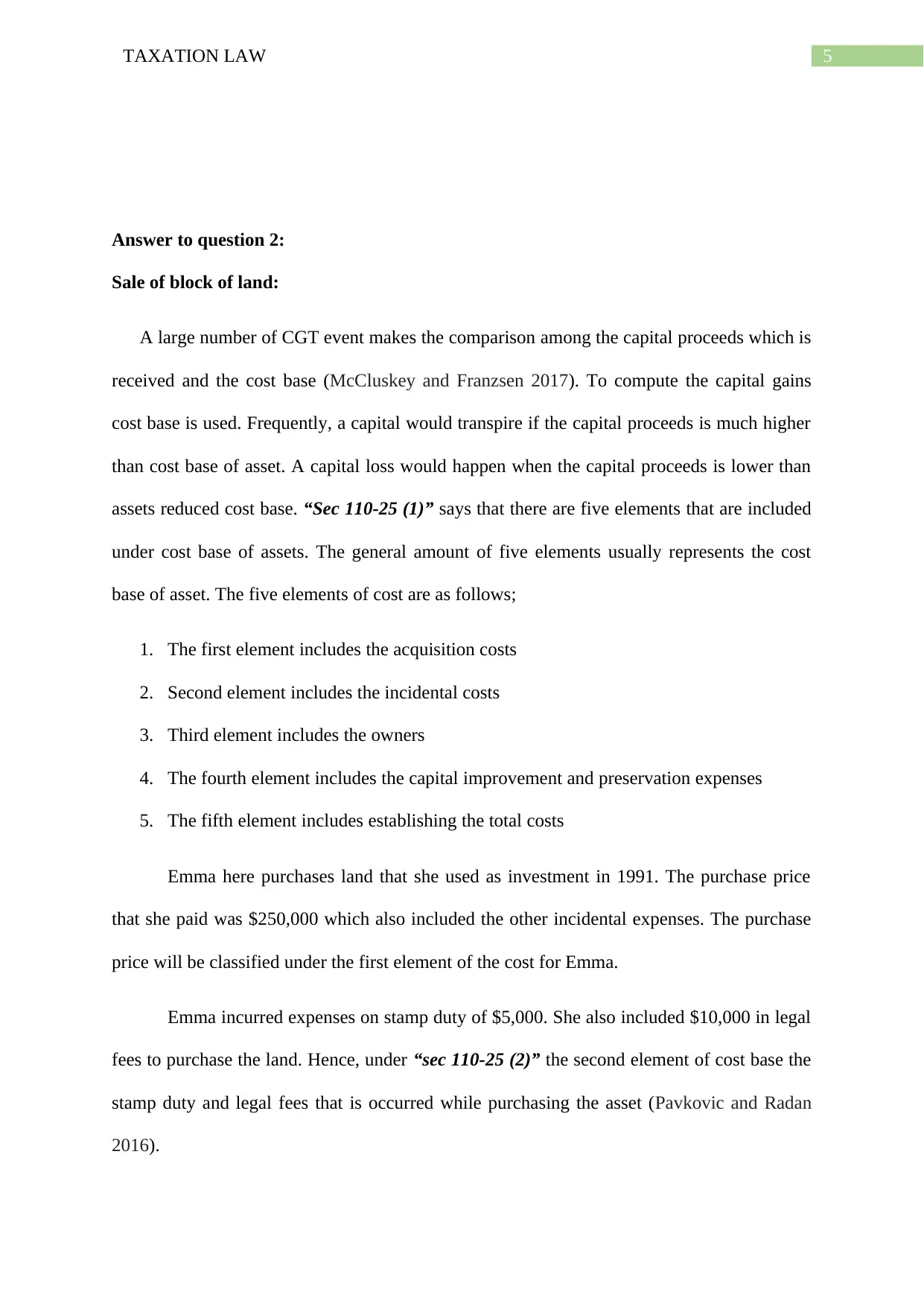

Answer to question 2:

Sale of block of land:

A large number of CGT event makes the comparison among the capital proceeds which is

received and the cost base (McCluskey and Franzsen 2017). To compute the capital gains

cost base is used. Frequently, a capital would transpire if the capital proceeds is much higher

than cost base of asset. A capital loss would happen when the capital proceeds is lower than

assets reduced cost base. “Sec 110-25 (1)” says that there are five elements that are included

under cost base of assets. The general amount of five elements usually represents the cost

base of asset. The five elements of cost are as follows;

1. The first element includes the acquisition costs

2. Second element includes the incidental costs

3. Third element includes the owners

4. The fourth element includes the capital improvement and preservation expenses

5. The fifth element includes establishing the total costs

Emma here purchases land that she used as investment in 1991. The purchase price

that she paid was $250,000 which also included the other incidental expenses. The purchase

price will be classified under the first element of the cost for Emma.

Emma incurred expenses on stamp duty of $5,000. She also included $10,000 in legal

fees to purchase the land. Hence, under “sec 110-25 (2)” the second element of cost base the

stamp duty and legal fees that is occurred while purchasing the asset (Pavkovic and Radan

2016).

Answer to question 2:

Sale of block of land:

A large number of CGT event makes the comparison among the capital proceeds which is

received and the cost base (McCluskey and Franzsen 2017). To compute the capital gains

cost base is used. Frequently, a capital would transpire if the capital proceeds is much higher

than cost base of asset. A capital loss would happen when the capital proceeds is lower than

assets reduced cost base. “Sec 110-25 (1)” says that there are five elements that are included

under cost base of assets. The general amount of five elements usually represents the cost

base of asset. The five elements of cost are as follows;

1. The first element includes the acquisition costs

2. Second element includes the incidental costs

3. Third element includes the owners

4. The fourth element includes the capital improvement and preservation expenses

5. The fifth element includes establishing the total costs

Emma here purchases land that she used as investment in 1991. The purchase price

that she paid was $250,000 which also included the other incidental expenses. The purchase

price will be classified under the first element of the cost for Emma.

Emma incurred expenses on stamp duty of $5,000. She also included $10,000 in legal

fees to purchase the land. Hence, under “sec 110-25 (2)” the second element of cost base the

stamp duty and legal fees that is occurred while purchasing the asset (Pavkovic and Radan

2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

She also paid a loan interest of $32,000 as a means to fund the purchase land. During

the year expenses were incurred on council rates, wages and insurance which totalled around

$22,000. These cost will be included into the third element cost base as the cost of ownership

of the asset.

During the year in January 2005 a dispute happened with the neighbour and incurred a

legal expense of $5000 to resolve the dispute. These expenses will be considered as the

capital expenditure cost that is occurred in preserving as well defending the title in the asset.

Under the “sec 110-25 (6) of the ITAA 1997” these cost will be counted in her cost base

under the fifth element (Miller and Oats 2016).

Prior to putting the placing, the property on sale a sum of $27,500 was incurred for

removing the pine trees on the land. The sum of $27,500 will be contained within the cost

base of fourth element under “sec 110-25 (5), ITAA 1997”. The overall capital gains of

Emma from the sale of land is included below;

She also paid a loan interest of $32,000 as a means to fund the purchase land. During

the year expenses were incurred on council rates, wages and insurance which totalled around

$22,000. These cost will be included into the third element cost base as the cost of ownership

of the asset.

During the year in January 2005 a dispute happened with the neighbour and incurred a

legal expense of $5000 to resolve the dispute. These expenses will be considered as the

capital expenditure cost that is occurred in preserving as well defending the title in the asset.

Under the “sec 110-25 (6) of the ITAA 1997” these cost will be counted in her cost base

under the fifth element (Miller and Oats 2016).

Prior to putting the placing, the property on sale a sum of $27,500 was incurred for

removing the pine trees on the land. The sum of $27,500 will be contained within the cost

base of fourth element under “sec 110-25 (5), ITAA 1997”. The overall capital gains of

Emma from the sale of land is included below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

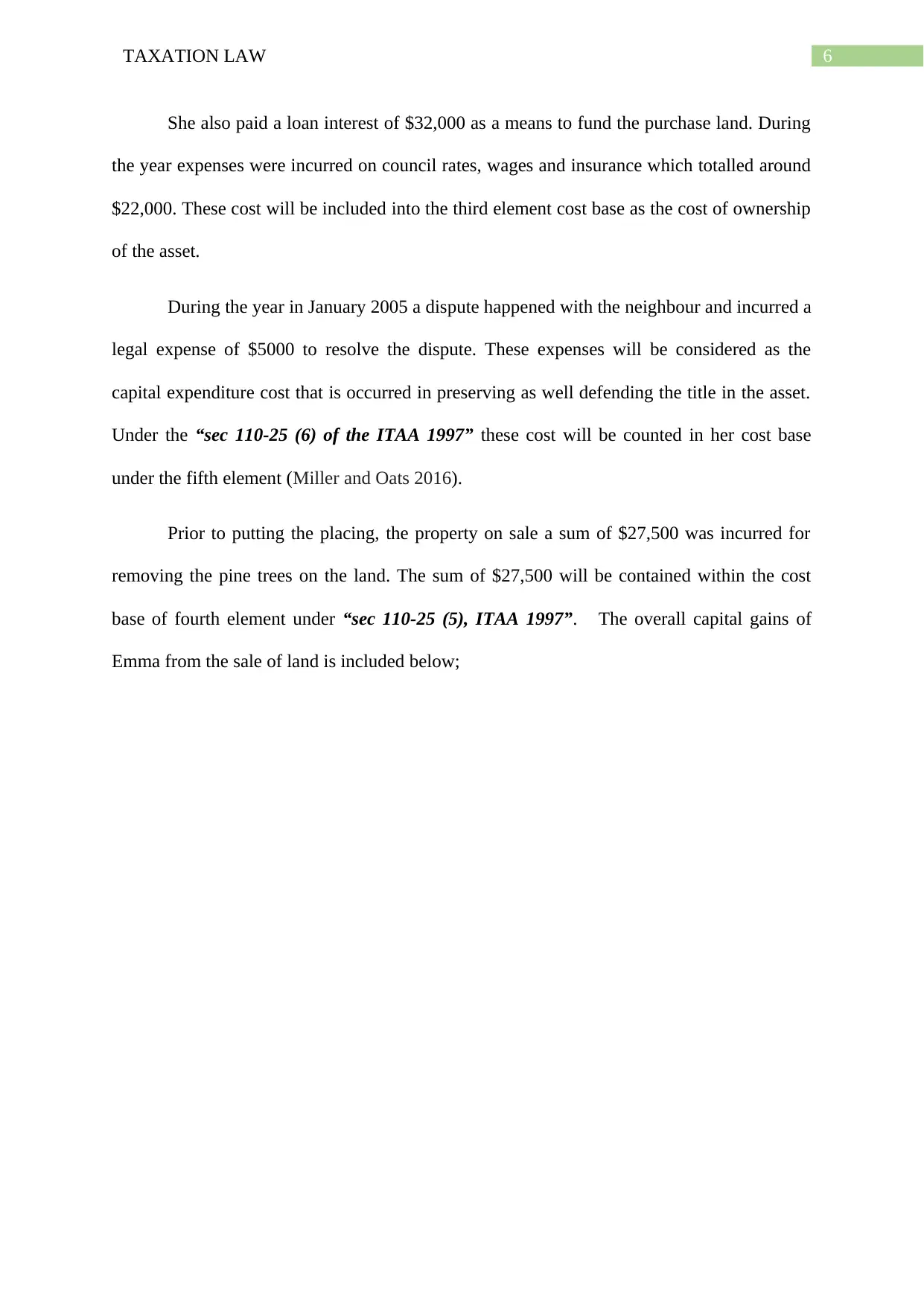

Sale of Shares in Rio Tinto:

“Sec 100-25 (1), ITAA 1997” says that assets which is purchased on or following the

20/9/1985 will be seen as post-CGT assets (Fleurbaey and Maniquet 2018). While assets

which is purchased before 20/9/1985 will be seen as the pre-CGT asset and the capital gains

that are made is exempted. While “sec 108-5 (1)” says that CGT asset are any form of

property or the lawful or equitable rights. It comprises of any form of tangible and intangible

assets. Emma sold shares in Rio Tinto for $50.85 per share while these shares were actually

purchased by paying $3.5 per share in 1982. The sale of Rio Tinto shares has led to “CGT

event A1”. As the shares were purchased before 20/9/1985 hence it is a pre-CGT asset. The

capital gains which is made is exempted from tax for Emma.

Sale of Shares in Rio Tinto:

“Sec 100-25 (1), ITAA 1997” says that assets which is purchased on or following the

20/9/1985 will be seen as post-CGT assets (Fleurbaey and Maniquet 2018). While assets

which is purchased before 20/9/1985 will be seen as the pre-CGT asset and the capital gains

that are made is exempted. While “sec 108-5 (1)” says that CGT asset are any form of

property or the lawful or equitable rights. It comprises of any form of tangible and intangible

assets. Emma sold shares in Rio Tinto for $50.85 per share while these shares were actually

purchased by paying $3.5 per share in 1982. The sale of Rio Tinto shares has led to “CGT

event A1”. As the shares were purchased before 20/9/1985 hence it is a pre-CGT asset. The

capital gains which is made is exempted from tax for Emma.

8TAXATION LAW

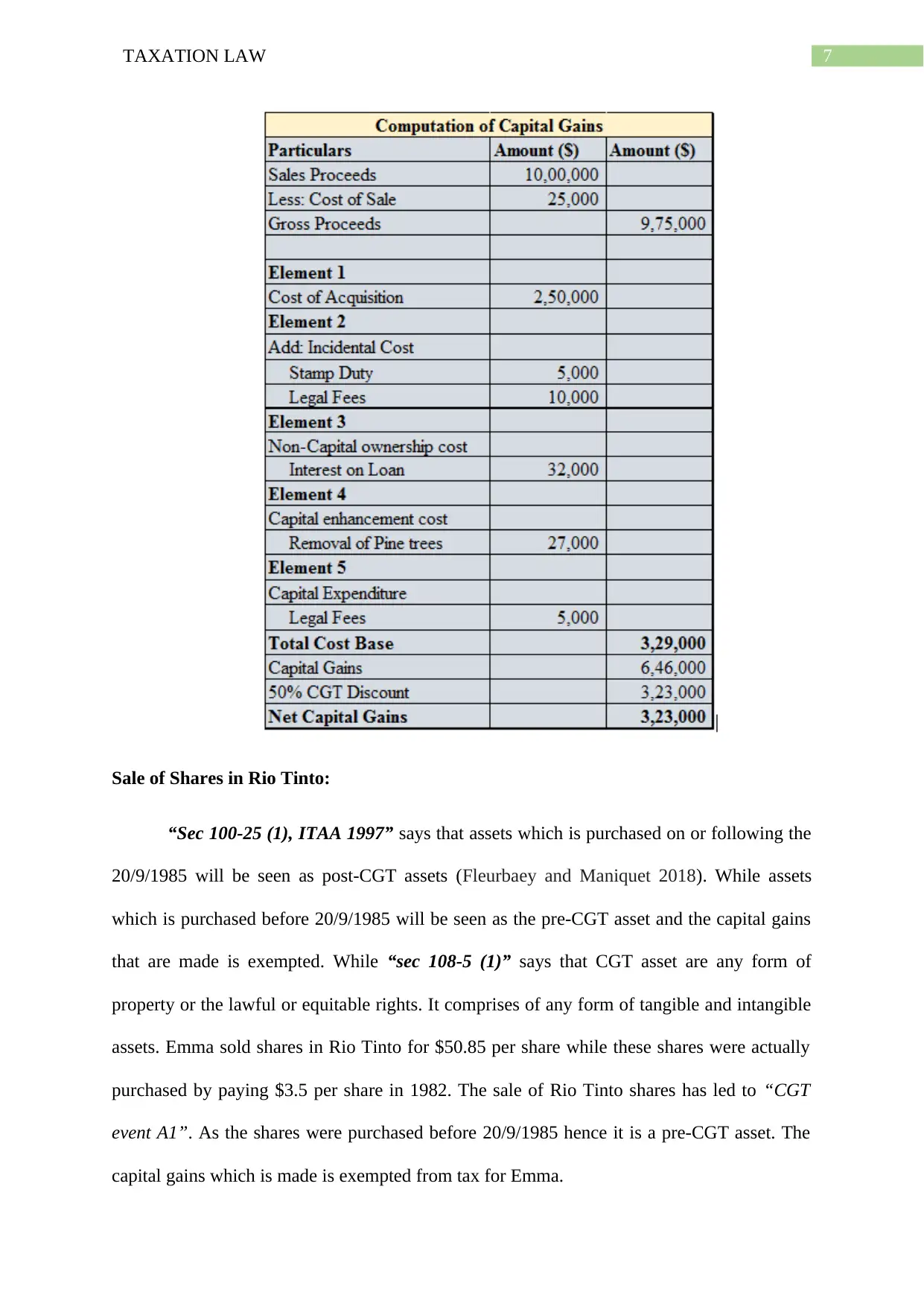

Sale of stamp:

Collectable under “s 108-10, ITA Act 1997” denotes items of assets which is held by

a person for their own satisfaction and usage (Sikka 2017). Some examples of collectables

are Antiques, paintings, jewellery, rare stamps, coins etc. An important aspect regarding

collectable is that when a capital loss happens they are required to quarantined and it is only

permitted for offset against capital gains made from other collectables. Similarly, Emma sells

a collection of stamps in auction for $50,000 and also incurred a cost of sale of $5,000 as

auction fees. The stamp was initially purchased for $60,000. On selling the stamp a “CGT

Event A1” happened under “s 104-10 (1), ITA Act 1997”. The stamps are characterized as

collectable under “s 108-10, ITA Act 1997” (Basu 2016). Therefore, a capital loss has

occurred in this situation. Emma should carry forward the capital loss to next year because

she did not have capital gains in the present year from collectables.

Sale of stamp:

Collectable under “s 108-10, ITA Act 1997” denotes items of assets which is held by

a person for their own satisfaction and usage (Sikka 2017). Some examples of collectables

are Antiques, paintings, jewellery, rare stamps, coins etc. An important aspect regarding

collectable is that when a capital loss happens they are required to quarantined and it is only

permitted for offset against capital gains made from other collectables. Similarly, Emma sells

a collection of stamps in auction for $50,000 and also incurred a cost of sale of $5,000 as

auction fees. The stamp was initially purchased for $60,000. On selling the stamp a “CGT

Event A1” happened under “s 104-10 (1), ITA Act 1997”. The stamps are characterized as

collectable under “s 108-10, ITA Act 1997” (Basu 2016). Therefore, a capital loss has

occurred in this situation. Emma should carry forward the capital loss to next year because

she did not have capital gains in the present year from collectables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

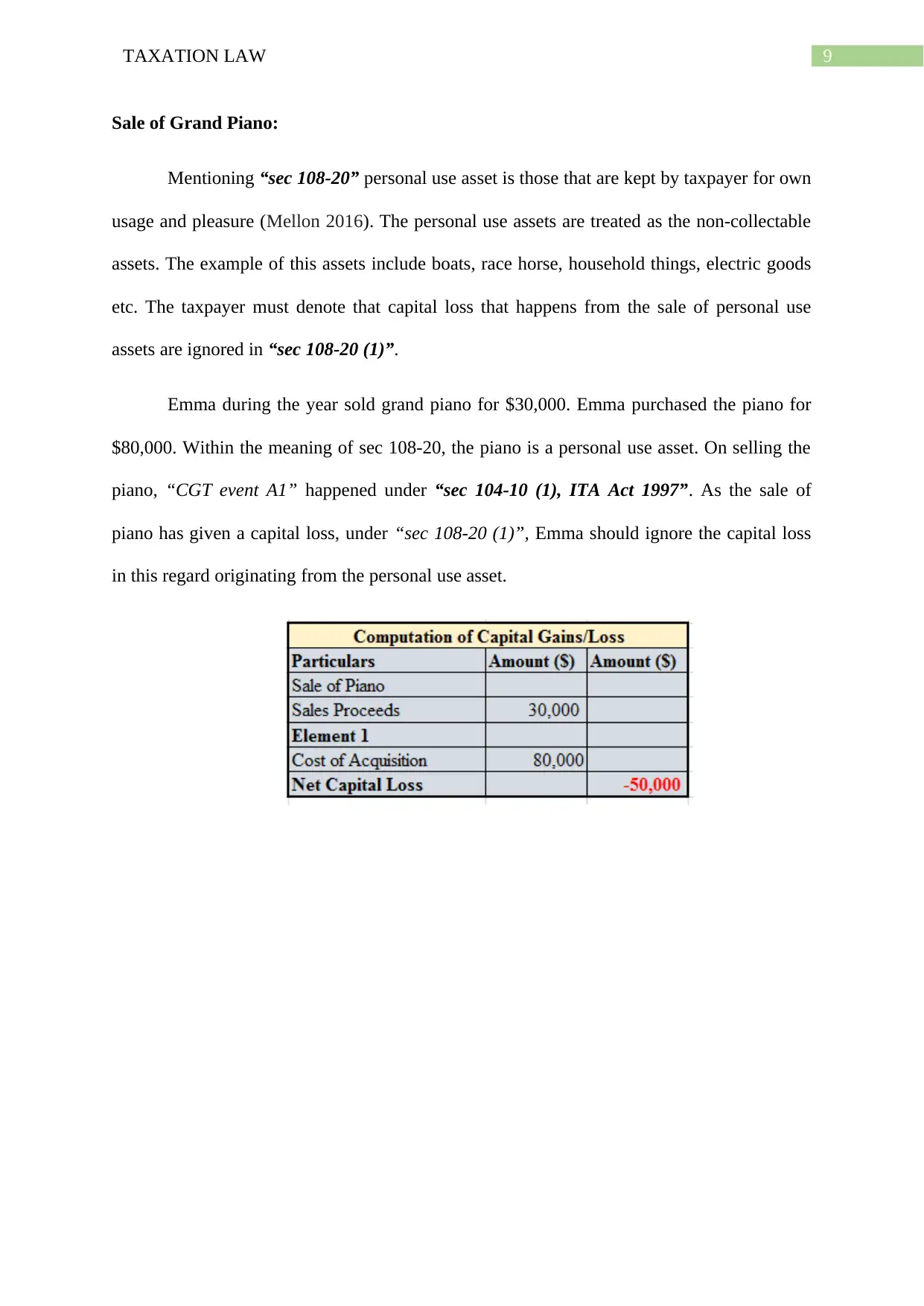

Sale of Grand Piano:

Mentioning “sec 108-20” personal use asset is those that are kept by taxpayer for own

usage and pleasure (Mellon 2016). The personal use assets are treated as the non-collectable

assets. The example of this assets include boats, race horse, household things, electric goods

etc. The taxpayer must denote that capital loss that happens from the sale of personal use

assets are ignored in “sec 108-20 (1)”.

Emma during the year sold grand piano for $30,000. Emma purchased the piano for

$80,000. Within the meaning of sec 108-20, the piano is a personal use asset. On selling the

piano, “CGT event A1” happened under “sec 104-10 (1), ITA Act 1997”. As the sale of

piano has given a capital loss, under “sec 108-20 (1)”, Emma should ignore the capital loss

in this regard originating from the personal use asset.

Sale of Grand Piano:

Mentioning “sec 108-20” personal use asset is those that are kept by taxpayer for own

usage and pleasure (Mellon 2016). The personal use assets are treated as the non-collectable

assets. The example of this assets include boats, race horse, household things, electric goods

etc. The taxpayer must denote that capital loss that happens from the sale of personal use

assets are ignored in “sec 108-20 (1)”.

Emma during the year sold grand piano for $30,000. Emma purchased the piano for

$80,000. Within the meaning of sec 108-20, the piano is a personal use asset. On selling the

piano, “CGT event A1” happened under “sec 104-10 (1), ITA Act 1997”. As the sale of

piano has given a capital loss, under “sec 108-20 (1)”, Emma should ignore the capital loss

in this regard originating from the personal use asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bidin, Z., Mohd Shamsudin, F. and Othman, Z., 2014. Using theory of reasoned action to

explain taxpayer intention to comply with goods and services tax. International Journal of

Business and Social Science.

Rimmer, X., Smith, J. and Wende, S., 2014. The incidence of company tax in

Australia. Economic Round-up, (1), p.33.

Schneider, F., Raczkowski, K. and Mróz, B., 2015. Shadow economy and tax evasion in the

EU. Journal of Money Laundering Control, 18(1), pp.34-51.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Garg, K., Chawla, M., Chawla, C. and Taneja, S., 2018. Impact of goods and services tax on

business. International Journal of Education and Management Studies, 8(2), pp.312-314.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Pavkovic, A. and Radan, P., 2016. Creating new states: theory and practice of secession.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

References:

Bidin, Z., Mohd Shamsudin, F. and Othman, Z., 2014. Using theory of reasoned action to

explain taxpayer intention to comply with goods and services tax. International Journal of

Business and Social Science.

Rimmer, X., Smith, J. and Wende, S., 2014. The incidence of company tax in

Australia. Economic Round-up, (1), p.33.

Schneider, F., Raczkowski, K. and Mróz, B., 2015. Shadow economy and tax evasion in the

EU. Journal of Money Laundering Control, 18(1), pp.34-51.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Garg, K., Chawla, M., Chawla, C. and Taneja, S., 2018. Impact of goods and services tax on

business. International Journal of Education and Management Studies, 8(2), pp.312-314.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Pavkovic, A. and Radan, P., 2016. Creating new states: theory and practice of secession.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

11TAXATION LAW

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mawuli, A., 2014, May. Goods and services tax: An appraisal. In Paper presented at the

PNG Taxation Research and Review Symposium (Vol. 29, p. 30).

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mawuli, A., 2014, May. Goods and services tax: An appraisal. In Paper presented at the

PNG Taxation Research and Review Symposium (Vol. 29, p. 30).

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.