HA3042: Taxation Law Assignment on Fringe Benefits and Capital Gains

VerifiedAdded on 2022/11/26

|11

|2565

|126

Homework Assignment

AI Summary

This assignment analyzes two key areas of Australian taxation law: Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). The FBT section focuses on calculating the fringe benefit arising from a company car, comparing the statutory formula method and the operating cost method, considering employee contributions, depreciation, and imputed interest. The CGT section assesses capital gains and losses from the sale of various assets, including a house, a painting, a yacht, and shares. The analysis applies the Income Tax Assessment Act 1997, considering cost base, capital proceeds, and relevant exemptions and discounts, such as the main residence exemption and the 50% CGT discount. The assignment demonstrates an understanding of CGT events, cost base calculations, and the treatment of personal use assets and capital losses.

Running head: TAXATION LAW

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Answer 1:

The present case study involves the issue of analyzing the Fringe Benefit (FB)

consequences of the Car as per operating cost method as well as statutory formula method1.

The Fringe Benefit Tax is dealt in the Fringe Benefits Tax Assessment Act 1986 in

Australia2. FBT is defined as any type of benefit related to an employment and granted by the

employer or associate to an employee or associate in a year at any time out of a bond of mutual

relationship. This is given in section 136(1) of FBTA. Such benefit can comprise any interest,

right, things of value and even things of personal use. The FBT is given in a year. The tax year

usually runs from 1st of April of a particular year to March 31st of the year next. The type 1 class

of benefit forms the fringe benefits over which GST is applicable. For a Financial Year 2019 to

2019, the FBT’s gross rate is 2.0802. The Fringe Tax Benefit for the same financial year is 47

percent.

Sec. 7 is related to FB of cars. It occurs when car is gifted as a benefit to an employee by

an employer to use it privately. There lies two ways for calculating Car Fringe Benefit. One of

the ways is known as statutory formula (SFM) method given in sec. 9(1) in FBTAA. Another is

called the Operating Cost Method given in sec. 10(2) of FBTAA.

In SFM, formula used is simple and can be represented as (0.2 * Car Base Value * day’s

number of the financial year in which CFB is allowed/ total taxable tax)- Recipient’s payment)

The formula, as per Operating Cost Method, can be represented as OC*(100%-B)-RC

1 Hemmings, Philip, and Annamaria Tuske. "Improving Taxes and Transfers in Australia." (2015).

2 The Fringe Benefits Tax Assessment Act 1986.

TAXATION LAW

Answer 1:

The present case study involves the issue of analyzing the Fringe Benefit (FB)

consequences of the Car as per operating cost method as well as statutory formula method1.

The Fringe Benefit Tax is dealt in the Fringe Benefits Tax Assessment Act 1986 in

Australia2. FBT is defined as any type of benefit related to an employment and granted by the

employer or associate to an employee or associate in a year at any time out of a bond of mutual

relationship. This is given in section 136(1) of FBTA. Such benefit can comprise any interest,

right, things of value and even things of personal use. The FBT is given in a year. The tax year

usually runs from 1st of April of a particular year to March 31st of the year next. The type 1 class

of benefit forms the fringe benefits over which GST is applicable. For a Financial Year 2019 to

2019, the FBT’s gross rate is 2.0802. The Fringe Tax Benefit for the same financial year is 47

percent.

Sec. 7 is related to FB of cars. It occurs when car is gifted as a benefit to an employee by

an employer to use it privately. There lies two ways for calculating Car Fringe Benefit. One of

the ways is known as statutory formula (SFM) method given in sec. 9(1) in FBTAA. Another is

called the Operating Cost Method given in sec. 10(2) of FBTAA.

In SFM, formula used is simple and can be represented as (0.2 * Car Base Value * day’s

number of the financial year in which CFB is allowed/ total taxable tax)- Recipient’s payment)

The formula, as per Operating Cost Method, can be represented as OC*(100%-B)-RC

1 Hemmings, Philip, and Annamaria Tuske. "Improving Taxes and Transfers in Australia." (2015).

2 The Fringe Benefits Tax Assessment Act 1986.

2

TAXATION LAW

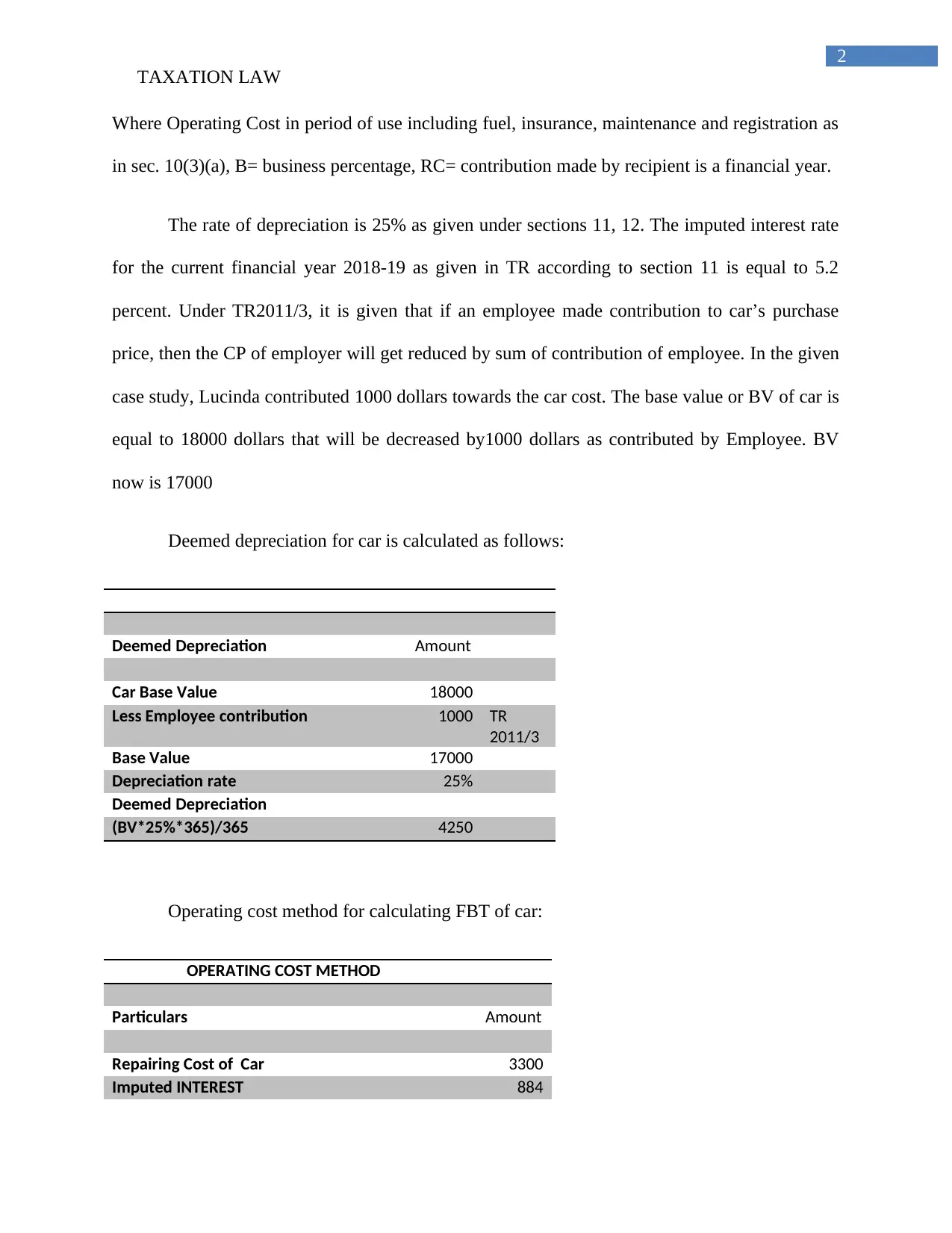

Where Operating Cost in period of use including fuel, insurance, maintenance and registration as

in sec. 10(3)(a), B= business percentage, RC= contribution made by recipient is a financial year.

The rate of depreciation is 25% as given under sections 11, 12. The imputed interest rate

for the current financial year 2018-19 as given in TR according to section 11 is equal to 5.2

percent. Under TR2011/3, it is given that if an employee made contribution to car’s purchase

price, then the CP of employer will get reduced by sum of contribution of employee. In the given

case study, Lucinda contributed 1000 dollars towards the car cost. The base value or BV of car is

equal to 18000 dollars that will be decreased by1000 dollars as contributed by Employee. BV

now is 17000

Deemed depreciation for car is calculated as follows:

Deemed Depreciation Amount

Car Base Value 18000

Less Employee contribution 1000 TR

2011/3

Base Value 17000

Depreciation rate 25%

Deemed Depreciation

(BV*25%*365)/365 4250

Operating cost method for calculating FBT of car:

OPERATING COST METHOD

Particulars Amount

Repairing Cost of Car 3300

Imputed INTEREST 884

TAXATION LAW

Where Operating Cost in period of use including fuel, insurance, maintenance and registration as

in sec. 10(3)(a), B= business percentage, RC= contribution made by recipient is a financial year.

The rate of depreciation is 25% as given under sections 11, 12. The imputed interest rate

for the current financial year 2018-19 as given in TR according to section 11 is equal to 5.2

percent. Under TR2011/3, it is given that if an employee made contribution to car’s purchase

price, then the CP of employer will get reduced by sum of contribution of employee. In the given

case study, Lucinda contributed 1000 dollars towards the car cost. The base value or BV of car is

equal to 18000 dollars that will be decreased by1000 dollars as contributed by Employee. BV

now is 17000

Deemed depreciation for car is calculated as follows:

Deemed Depreciation Amount

Car Base Value 18000

Less Employee contribution 1000 TR

2011/3

Base Value 17000

Depreciation rate 25%

Deemed Depreciation

(BV*25%*365)/365 4250

Operating cost method for calculating FBT of car:

OPERATING COST METHOD

Particulars Amount

Repairing Cost of Car 3300

Imputed INTEREST 884

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

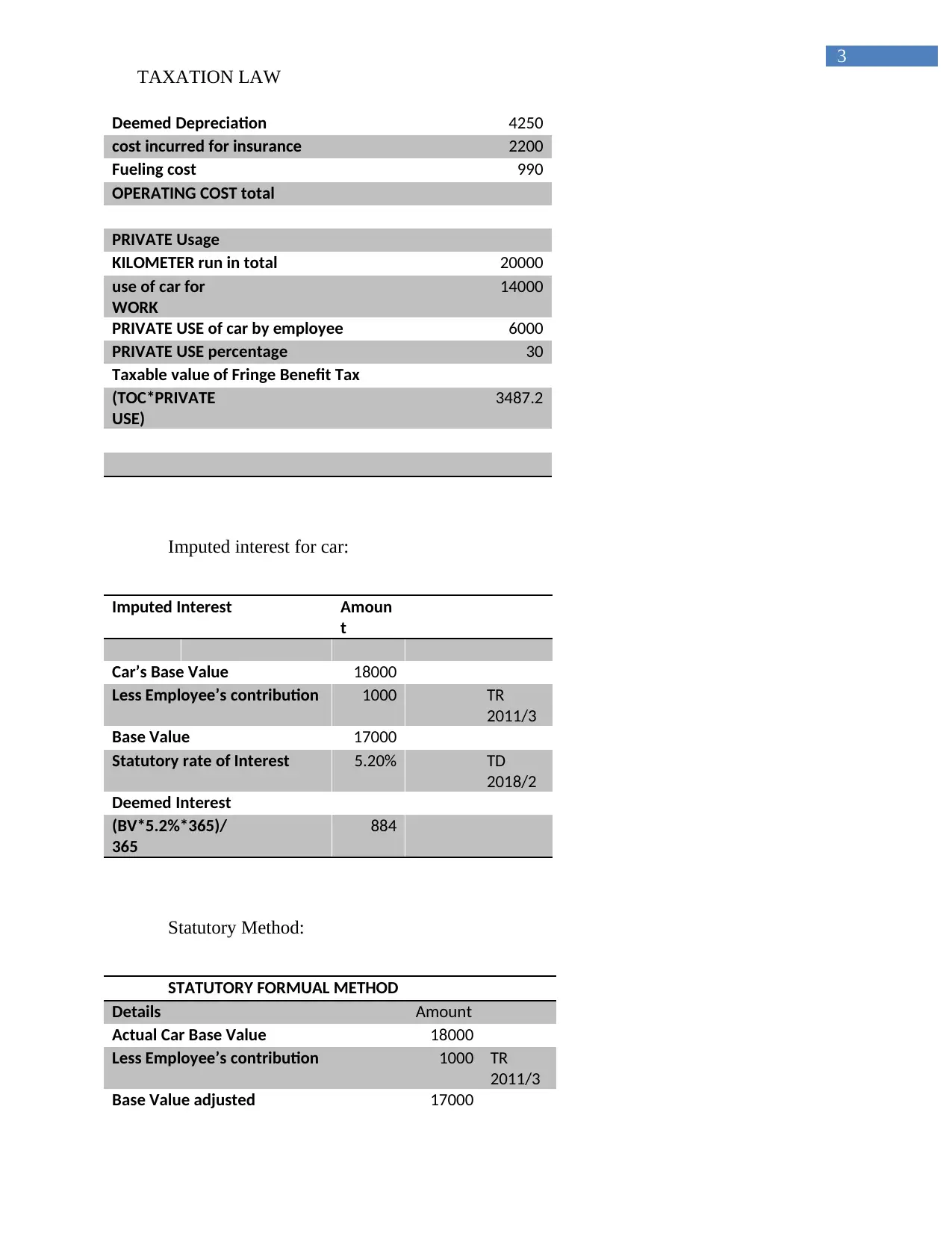

Deemed Depreciation 4250

cost incurred for insurance 2200

Fueling cost 990

OPERATING COST total

PRIVATE Usage

KILOMETER run in total 20000

use of car for

WORK

14000

PRIVATE USE of car by employee 6000

PRIVATE USE percentage 30

Taxable value of Fringe Benefit Tax

(TOC*PRIVATE

USE)

3487.2

Imputed interest for car:

Imputed Interest Amoun

t

Car’s Base Value 18000

Less Employee’s contribution 1000 TR

2011/3

Base Value 17000

Statutory rate of Interest 5.20% TD

2018/2

Deemed Interest

(BV*5.2%*365)/

365

884

Statutory Method:

STATUTORY FORMUAL METHOD

Details Amount

Actual Car Base Value 18000

Less Employee’s contribution 1000 TR

2011/3

Base Value adjusted 17000

TAXATION LAW

Deemed Depreciation 4250

cost incurred for insurance 2200

Fueling cost 990

OPERATING COST total

PRIVATE Usage

KILOMETER run in total 20000

use of car for

WORK

14000

PRIVATE USE of car by employee 6000

PRIVATE USE percentage 30

Taxable value of Fringe Benefit Tax

(TOC*PRIVATE

USE)

3487.2

Imputed interest for car:

Imputed Interest Amoun

t

Car’s Base Value 18000

Less Employee’s contribution 1000 TR

2011/3

Base Value 17000

Statutory rate of Interest 5.20% TD

2018/2

Deemed Interest

(BV*5.2%*365)/

365

884

Statutory Method:

STATUTORY FORMUAL METHOD

Details Amount

Actual Car Base Value 18000

Less Employee’s contribution 1000 TR

2011/3

Base Value adjusted 17000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

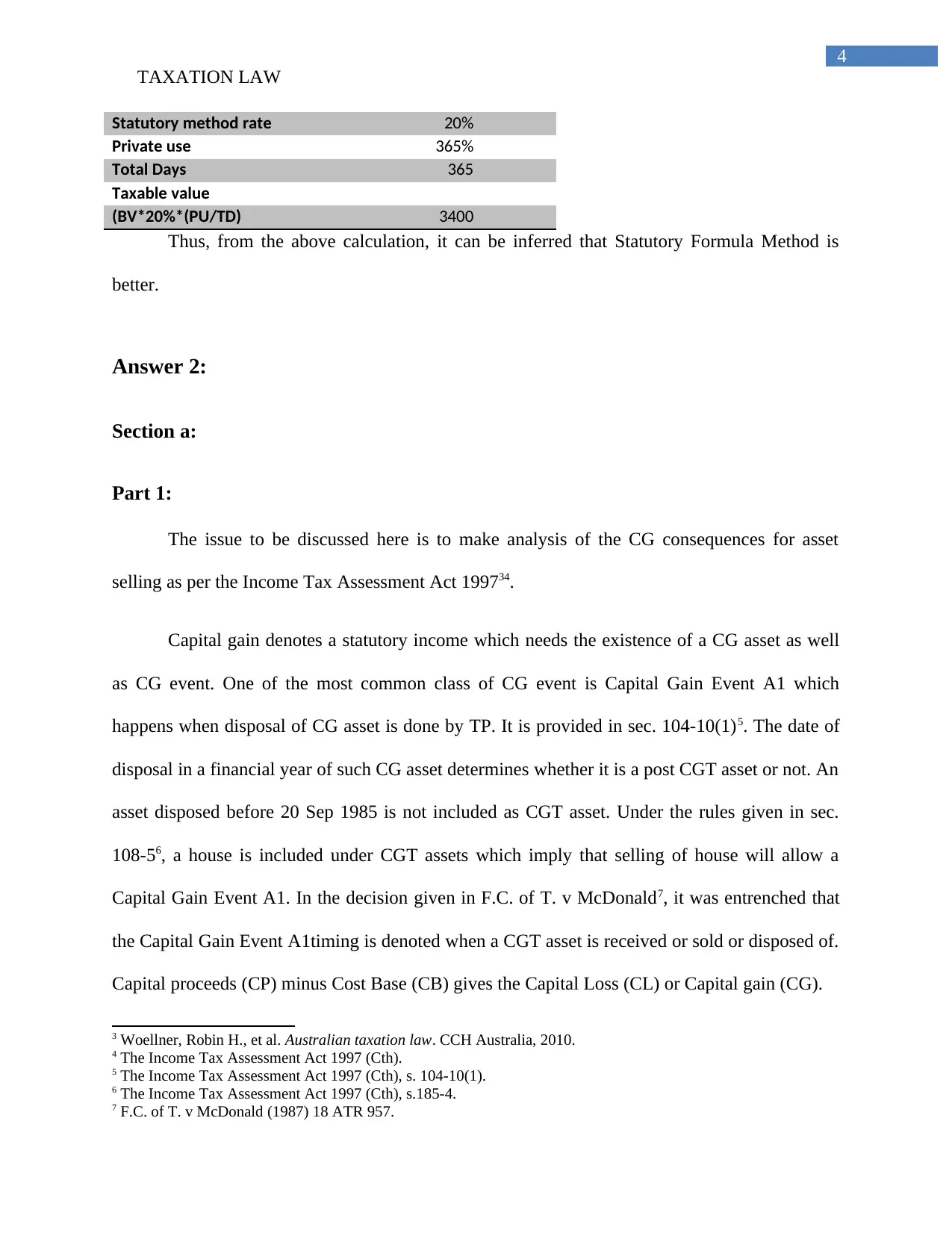

Statutory method rate 20%

Private use 365%

Total Days 365

Taxable value

(BV*20%*(PU/TD) 3400

Thus, from the above calculation, it can be inferred that Statutory Formula Method is

better.

Answer 2:

Section a:

Part 1:

The issue to be discussed here is to make analysis of the CG consequences for asset

selling as per the Income Tax Assessment Act 199734.

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1)5. The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

108-56, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald7, it was entrenched that

the Capital Gain Event A1timing is denoted when a CGT asset is received or sold or disposed of.

Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or Capital gain (CG).

3 Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2010.

4 The Income Tax Assessment Act 1997 (Cth).

5 The Income Tax Assessment Act 1997 (Cth), s. 104-10(1).

6 The Income Tax Assessment Act 1997 (Cth), s.185-4.

7 F.C. of T. v McDonald (1987) 18 ATR 957.

TAXATION LAW

Statutory method rate 20%

Private use 365%

Total Days 365

Taxable value

(BV*20%*(PU/TD) 3400

Thus, from the above calculation, it can be inferred that Statutory Formula Method is

better.

Answer 2:

Section a:

Part 1:

The issue to be discussed here is to make analysis of the CG consequences for asset

selling as per the Income Tax Assessment Act 199734.

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1)5. The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

108-56, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald7, it was entrenched that

the Capital Gain Event A1timing is denoted when a CGT asset is received or sold or disposed of.

Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or Capital gain (CG).

3 Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2010.

4 The Income Tax Assessment Act 1997 (Cth).

5 The Income Tax Assessment Act 1997 (Cth), s. 104-10(1).

6 The Income Tax Assessment Act 1997 (Cth), s.185-4.

7 F.C. of T. v McDonald (1987) 18 ATR 957.

5

TAXATION LAW

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.208. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. Hence, Element 1 of CB of the house equals to 70000 dollars as per subsec.2 of

110-25. Sum of 15000$ granted to real estate agent forms the element 2 of CB as per sub sec. 3

of 110-25. Thus CB= 85000$. The date of formation of contract appears to be 29th of June’ 19.

Thus, CP is the amount to be received and equals to 865000 dollars. Net capital gain of Ray is

780000 dollars. He is eligible for claiming 50 percent discount as per Division 115. However,

some of the conditions are to be satisfied for this which are individual persons, selling of asset

after 21st of September’ 99 and asset must be held for one year. all these are provided under s

115-10, 115-15 and 115-25. Total CG= 390000 dollars. But as per the facts of the case, Ray

resided in the house for about thirty years; hence it is his residence. So, Capital gain by sale of

house is exempted as per sec. 118-110. So, he is not needed to pay CGT in this year. Since the

events of contract being cancelled and the deposit being retained occurs in the next financial

year, hence they are excluded.

Part 2:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

8 The Income Tax Assessment Act 1997 (Cth), s. 116.20.

TAXATION LAW

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.208. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. Hence, Element 1 of CB of the house equals to 70000 dollars as per subsec.2 of

110-25. Sum of 15000$ granted to real estate agent forms the element 2 of CB as per sub sec. 3

of 110-25. Thus CB= 85000$. The date of formation of contract appears to be 29th of June’ 19.

Thus, CP is the amount to be received and equals to 865000 dollars. Net capital gain of Ray is

780000 dollars. He is eligible for claiming 50 percent discount as per Division 115. However,

some of the conditions are to be satisfied for this which are individual persons, selling of asset

after 21st of September’ 99 and asset must be held for one year. all these are provided under s

115-10, 115-15 and 115-25. Total CG= 390000 dollars. But as per the facts of the case, Ray

resided in the house for about thirty years; hence it is his residence. So, Capital gain by sale of

house is exempted as per sec. 118-110. So, he is not needed to pay CGT in this year. Since the

events of contract being cancelled and the deposit being retained occurs in the next financial

year, hence they are excluded.

Part 2:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

8 The Income Tax Assessment Act 1997 (Cth), s. 116.20.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It indicates CB’s first element for the painting by Preston is equal to 15000 dollars

according to sec. 110-25 (2). Painting being received before 20.09.1985 forms a CGT asset as it

was not bought before 11.55 pm of 19.09.1985. The CP= 125000 dollars which is incurred by

sale. Here CG= 125000-15000= 110000 dollars. However, some of the conditions are to be

satisfied for this which are individual persons, selling of asset after 21st of September’ 99 and

asset must be held for one year. All these are provided under s 115-10, 115-15 and 115-25.

Hence, CGT=55000 dollars as all criteria are met by Ray.

Part 3:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

TAXATION LAW

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It indicates CB’s first element for the painting by Preston is equal to 15000 dollars

according to sec. 110-25 (2). Painting being received before 20.09.1985 forms a CGT asset as it

was not bought before 11.55 pm of 19.09.1985. The CP= 125000 dollars which is incurred by

sale. Here CG= 125000-15000= 110000 dollars. However, some of the conditions are to be

satisfied for this which are individual persons, selling of asset after 21st of September’ 99 and

asset must be held for one year. All these are provided under s 115-10, 115-15 and 115-25.

Hence, CGT=55000 dollars as all criteria are met by Ray.

Part 3:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It means element 1 of CB of the yacht is equal to 110000 dollars as per sec. 110-

25(2). CP= 60000 dollars. There is a CL of 50000 dollars. As per sec. 108-20(2), loss of capital

on personal use asset is not taken into account. So, loss must be ignored. CB here is to be

denoted as the Reduced cost base (RCB)

Part 4:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

TAXATION LAW

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It means element 1 of CB of the yacht is equal to 110000 dollars as per sec. 110-

25(2). CP= 60000 dollars. There is a CL of 50000 dollars. As per sec. 108-20(2), loss of capital

on personal use asset is not taken into account. So, loss must be ignored. CB here is to be

denoted as the Reduced cost base (RCB)

Part 4:

Capital gain denotes a statutory income which needs the existence of a CG asset as well

as CG event. One of the most common class of CG event is Capital Gain Event A1 which

happens when disposal of CG asset is done by TP. It is provided in sec. 104-10(1). The date of

disposal in a financial year of such CG asset determines whether it is a post CGT asset or not. An

asset disposed before 20 Sep 1985 is not included as CGT asset. Under the rules given in sec.

108-5, a house is included under CGT assets which imply that selling of house will allow a

Capital Gain Event A1. In the decision given in F.C. of T. v McDonald (1987) 18 ATR 957, it

was entrenched that the Capital Gain Event A1timing is denoted when a CGT asset is received or

8

TAXATION LAW

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It means E1 of CB for shares= 75000 dollars according to sub section 2 of 110-25.

Interest over loan will not be considered here though it forms a not deductable expense as Ray

has a CL. RCB is not including Element 3 of sec. 110-25 (4). Element 3 is the interest. Stamp

duty of 250 dollars is the Element 2. CP here = 80000 dollars. It will be reduced by brokerage

fee of 750 dollars as per sec. 116-30. So, total Capital gain = 75250-79250 = -4000, hence CL. In

addition to this, CL from last year will reduce CG by 10000 dollars.

Ray’s net Capital gain or Capital loss for FY 2018-19:

House=0

Painting=55000

Yacht= 50000 (not considered)

Shares= -4000

Loss of last year= 10000

Total CG = 49000

TAXATION LAW

sold or disposed of. Capital proceeds (CP) minus Cost Base (CB) gives the Capital Loss (CL) or

Capital gain (CG).

That is, CP-CB=CG or CL.

CP is the sum of money incurred by selling an asset under sec. 116.20. CP also includes

any amount that can be received in future. Ideally, CB comprises of five elements. This shows

price money received by TP for an asset is mentioned under sec. 110-25(1). The cost price is the

first element. It means E1 of CB for shares= 75000 dollars according to sub section 2 of 110-25.

Interest over loan will not be considered here though it forms a not deductable expense as Ray

has a CL. RCB is not including Element 3 of sec. 110-25 (4). Element 3 is the interest. Stamp

duty of 250 dollars is the Element 2. CP here = 80000 dollars. It will be reduced by brokerage

fee of 750 dollars as per sec. 116-30. So, total Capital gain = 75250-79250 = -4000, hence CL. In

addition to this, CL from last year will reduce CG by 10000 dollars.

Ray’s net Capital gain or Capital loss for FY 2018-19:

House=0

Painting=55000

Yacht= 50000 (not considered)

Shares= -4000

Loss of last year= 10000

Total CG = 49000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Section b:

In account of the net CG for FY is 2019-19, Ray is to pay IT as it forms a statutory

income. The gain must be assessed in the Ray’s income.

Section c:

In account of the net CL for FY is 2019-19, Ray is eligible to offset the amount in next

FY of 2019-2020 as done for shares. But collectables can offset other collectables. Loss on

personal asset can’t be offset.

TAXATION LAW

Section b:

In account of the net CG for FY is 2019-19, Ray is to pay IT as it forms a statutory

income. The gain must be assessed in the Ray’s income.

Section c:

In account of the net CL for FY is 2019-19, Ray is eligible to offset the amount in next

FY of 2019-2020 as done for shares. But collectables can offset other collectables. Loss on

personal asset can’t be offset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

References:

F.C. of T. v McDonald (1987) 18 ATR 957; 87 ATC 4541

Hemmings, Philip, and Annamaria Tuske. "Improving Taxes and Transfers in Australia." (2015).

The Fringe Benefits Tax Assessment Act 1986

The Income Tax Assessment Act 1997 (Cth)

Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2010

TAXATION LAW

References:

F.C. of T. v McDonald (1987) 18 ATR 957; 87 ATC 4541

Hemmings, Philip, and Annamaria Tuske. "Improving Taxes and Transfers in Australia." (2015).

The Fringe Benefits Tax Assessment Act 1986

The Income Tax Assessment Act 1997 (Cth)

Woellner, Robin H., et al. Australian taxation law. CCH Australia, 2010

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.