TAXATION LAW Assignment: Capital Gains, Fringe Benefits, Tax Evasion

VerifiedAdded on 2020/03/28

|12

|2581

|50

Homework Assignment

AI Summary

This taxation law assignment provides an in-depth analysis of various tax-related issues. The first question focuses on capital gains tax, examining the classification of assets (collectables, personal use, and ordinary business assets) and the implications for calculating gains and losses, including set-off and carry-forward rules. The second question addresses fringe benefit tax, specifically concerning a bank providing a loan to an executive at a lower-than-market interest rate, calculating the taxable fringe benefit and considering scenarios such as income-producing activities and loan repayment. The third question explores the allocation of profit or loss from a jointly owned house property, determining whether the allocation follows the ownership ratio or a formal agreement between the owners. The fourth question distinguishes between tax evasion and tax avoidance. The final question addresses the taxation of receipts from the sale of felled timber, considering whether such receipts are subject to income tax based on the nature of the activity and applicable legal principles. The assignment utilizes relevant tax legislation, rulings, and case law to support its conclusions.

Running head: TAXATION LAW

Taxation Theory, Practice & Law

Taxation Theory, Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Question 4..................................................................................................................................7

Question 5..................................................................................................................................8

Reference..................................................................................................................................10

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................4

Question 3..................................................................................................................................6

Question 4..................................................................................................................................7

Question 5..................................................................................................................................8

Reference..................................................................................................................................10

2TAXATION LAW

Question 1

Issue in Question

Eric sold few assets acquired by him over the last 12 months period. The

determination of capital gains in relation to these assets is the issue to be addressed in this

question. Different provisions of capital gains tax apply in relation to different category of

assets. Further, the set off of capital gains losses and carry forward of the losses is also

different depending upon the type of capital asset. Thus, the issue of set off capital losses and

carry forward of the losses on the assets sold by Eric is also involved in the given case.

Applicable Law

Various provisions of income tax assessment act 1997 and new business tax system

(capital gains tax) 1999 are applicable in the given case. The income tax assessment act 1997

contains basic provisions related to inclusions and exclusions to and from the taxable income.

The provisions of new business tax system (capital gains tax) 1999 contains specific

guidelines on the computation of capital gains tax (CCH Australia Limited, 2011).

Analysis of Case

In the given case, assets held by Eric fall into three types of categories such as

collectables, personal use, and ordinary business asset. The assets namely painting, antique

chair and antique vase are collectables while the asset such as home sound system is personal

use. The shares in a listed company are ordinary business assets. As per the provisions of

section 100-25 (1), the personal use assets below the value of $10,000 are exempt from

capital gains tax. Further, the collectables are also exempt up to the value of $500 (ATO.

2017). Further, the losses on the personal use assets and collectables are only allowed to be

set off against the capital gains under the respective categories. This implies that the losses on

Question 1

Issue in Question

Eric sold few assets acquired by him over the last 12 months period. The

determination of capital gains in relation to these assets is the issue to be addressed in this

question. Different provisions of capital gains tax apply in relation to different category of

assets. Further, the set off of capital gains losses and carry forward of the losses is also

different depending upon the type of capital asset. Thus, the issue of set off capital losses and

carry forward of the losses on the assets sold by Eric is also involved in the given case.

Applicable Law

Various provisions of income tax assessment act 1997 and new business tax system

(capital gains tax) 1999 are applicable in the given case. The income tax assessment act 1997

contains basic provisions related to inclusions and exclusions to and from the taxable income.

The provisions of new business tax system (capital gains tax) 1999 contains specific

guidelines on the computation of capital gains tax (CCH Australia Limited, 2011).

Analysis of Case

In the given case, assets held by Eric fall into three types of categories such as

collectables, personal use, and ordinary business asset. The assets namely painting, antique

chair and antique vase are collectables while the asset such as home sound system is personal

use. The shares in a listed company are ordinary business assets. As per the provisions of

section 100-25 (1), the personal use assets below the value of $10,000 are exempt from

capital gains tax. Further, the collectables are also exempt up to the value of $500 (ATO.

2017). Further, the losses on the personal use assets and collectables are only allowed to be

set off against the capital gains under the respective categories. This implies that the losses on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

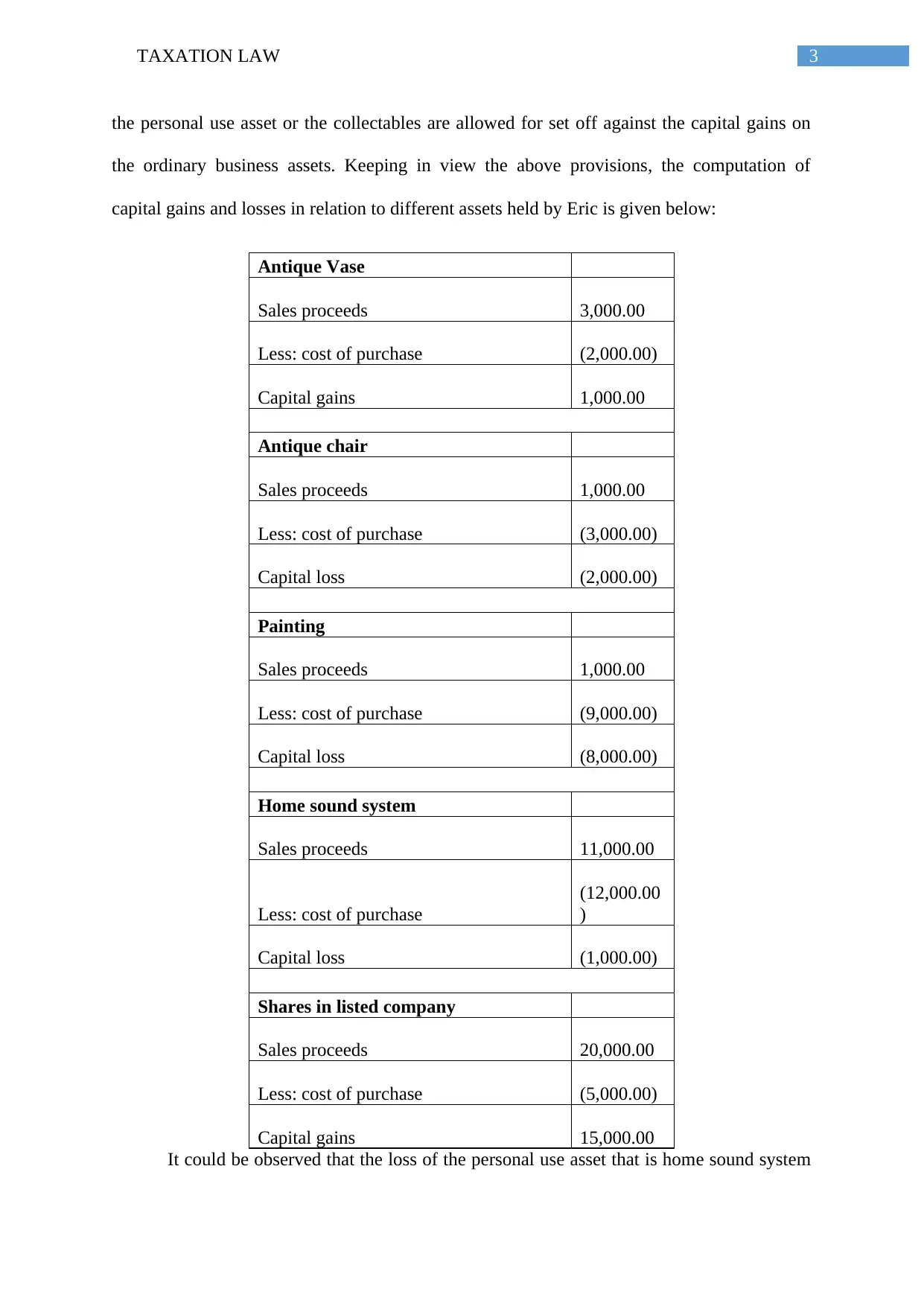

the personal use asset or the collectables are allowed for set off against the capital gains on

the ordinary business assets. Keeping in view the above provisions, the computation of

capital gains and losses in relation to different assets held by Eric is given below:

Antique Vase

Sales proceeds 3,000.00

Less: cost of purchase (2,000.00)

Capital gains 1,000.00

Antique chair

Sales proceeds 1,000.00

Less: cost of purchase (3,000.00)

Capital loss (2,000.00)

Painting

Sales proceeds 1,000.00

Less: cost of purchase (9,000.00)

Capital loss (8,000.00)

Home sound system

Sales proceeds 11,000.00

Less: cost of purchase

(12,000.00

)

Capital loss (1,000.00)

Shares in listed company

Sales proceeds 20,000.00

Less: cost of purchase (5,000.00)

Capital gains 15,000.00

It could be observed that the loss of the personal use asset that is home sound system

the personal use asset or the collectables are allowed for set off against the capital gains on

the ordinary business assets. Keeping in view the above provisions, the computation of

capital gains and losses in relation to different assets held by Eric is given below:

Antique Vase

Sales proceeds 3,000.00

Less: cost of purchase (2,000.00)

Capital gains 1,000.00

Antique chair

Sales proceeds 1,000.00

Less: cost of purchase (3,000.00)

Capital loss (2,000.00)

Painting

Sales proceeds 1,000.00

Less: cost of purchase (9,000.00)

Capital loss (8,000.00)

Home sound system

Sales proceeds 11,000.00

Less: cost of purchase

(12,000.00

)

Capital loss (1,000.00)

Shares in listed company

Sales proceeds 20,000.00

Less: cost of purchase (5,000.00)

Capital gains 15,000.00

It could be observed that the loss of the personal use asset that is home sound system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

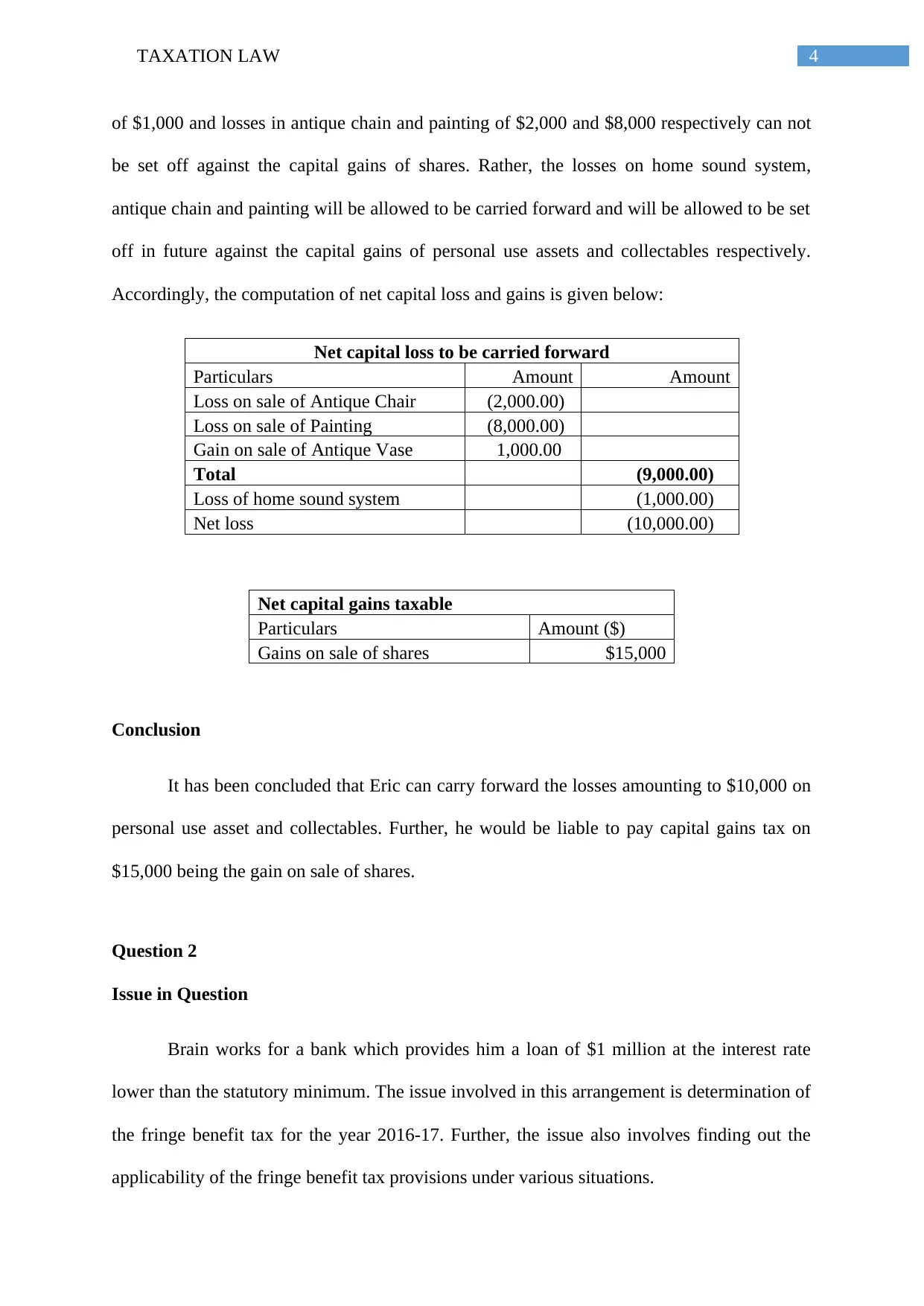

of $1,000 and losses in antique chain and painting of $2,000 and $8,000 respectively can not

be set off against the capital gains of shares. Rather, the losses on home sound system,

antique chain and painting will be allowed to be carried forward and will be allowed to be set

off in future against the capital gains of personal use assets and collectables respectively.

Accordingly, the computation of net capital loss and gains is given below:

Net capital loss to be carried forward

Particulars Amount Amount

Loss on sale of Antique Chair (2,000.00)

Loss on sale of Painting (8,000.00)

Gain on sale of Antique Vase 1,000.00

Total (9,000.00)

Loss of home sound system (1,000.00)

Net loss (10,000.00)

Net capital gains taxable

Particulars Amount ($)

Gains on sale of shares $15,000

Conclusion

It has been concluded that Eric can carry forward the losses amounting to $10,000 on

personal use asset and collectables. Further, he would be liable to pay capital gains tax on

$15,000 being the gain on sale of shares.

Question 2

Issue in Question

Brain works for a bank which provides him a loan of $1 million at the interest rate

lower than the statutory minimum. The issue involved in this arrangement is determination of

the fringe benefit tax for the year 2016-17. Further, the issue also involves finding out the

applicability of the fringe benefit tax provisions under various situations.

of $1,000 and losses in antique chain and painting of $2,000 and $8,000 respectively can not

be set off against the capital gains of shares. Rather, the losses on home sound system,

antique chain and painting will be allowed to be carried forward and will be allowed to be set

off in future against the capital gains of personal use assets and collectables respectively.

Accordingly, the computation of net capital loss and gains is given below:

Net capital loss to be carried forward

Particulars Amount Amount

Loss on sale of Antique Chair (2,000.00)

Loss on sale of Painting (8,000.00)

Gain on sale of Antique Vase 1,000.00

Total (9,000.00)

Loss of home sound system (1,000.00)

Net loss (10,000.00)

Net capital gains taxable

Particulars Amount ($)

Gains on sale of shares $15,000

Conclusion

It has been concluded that Eric can carry forward the losses amounting to $10,000 on

personal use asset and collectables. Further, he would be liable to pay capital gains tax on

$15,000 being the gain on sale of shares.

Question 2

Issue in Question

Brain works for a bank which provides him a loan of $1 million at the interest rate

lower than the statutory minimum. The issue involved in this arrangement is determination of

the fringe benefit tax for the year 2016-17. Further, the issue also involves finding out the

applicability of the fringe benefit tax provisions under various situations.

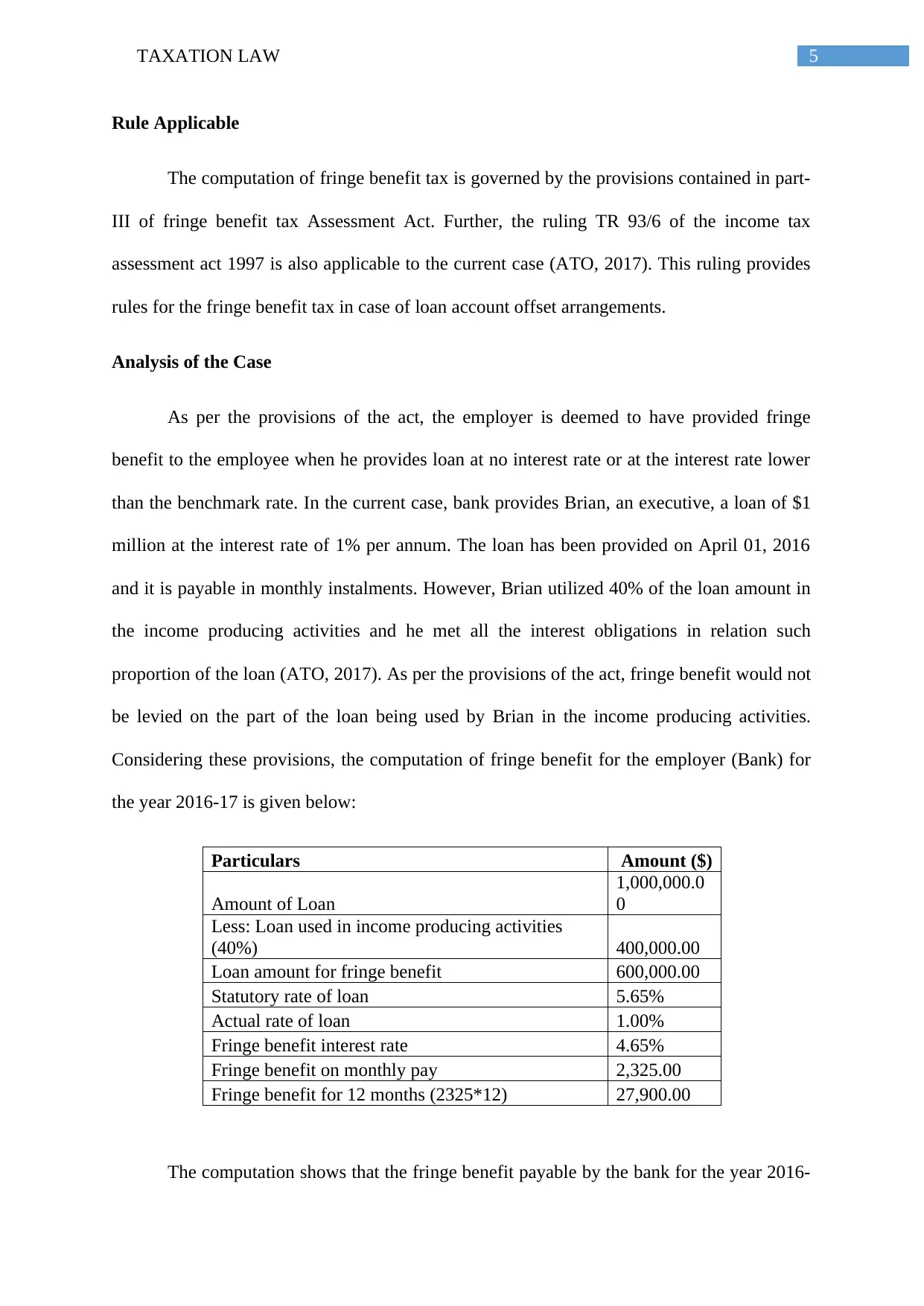

5TAXATION LAW

Rule Applicable

The computation of fringe benefit tax is governed by the provisions contained in part-

III of fringe benefit tax Assessment Act. Further, the ruling TR 93/6 of the income tax

assessment act 1997 is also applicable to the current case (ATO, 2017). This ruling provides

rules for the fringe benefit tax in case of loan account offset arrangements.

Analysis of the Case

As per the provisions of the act, the employer is deemed to have provided fringe

benefit to the employee when he provides loan at no interest rate or at the interest rate lower

than the benchmark rate. In the current case, bank provides Brian, an executive, a loan of $1

million at the interest rate of 1% per annum. The loan has been provided on April 01, 2016

and it is payable in monthly instalments. However, Brian utilized 40% of the loan amount in

the income producing activities and he met all the interest obligations in relation such

proportion of the loan (ATO, 2017). As per the provisions of the act, fringe benefit would not

be levied on the part of the loan being used by Brian in the income producing activities.

Considering these provisions, the computation of fringe benefit for the employer (Bank) for

the year 2016-17 is given below:

Particulars Amount ($)

Amount of Loan

1,000,000.0

0

Less: Loan used in income producing activities

(40%) 400,000.00

Loan amount for fringe benefit 600,000.00

Statutory rate of loan 5.65%

Actual rate of loan 1.00%

Fringe benefit interest rate 4.65%

Fringe benefit on monthly pay 2,325.00

Fringe benefit for 12 months (2325*12) 27,900.00

The computation shows that the fringe benefit payable by the bank for the year 2016-

Rule Applicable

The computation of fringe benefit tax is governed by the provisions contained in part-

III of fringe benefit tax Assessment Act. Further, the ruling TR 93/6 of the income tax

assessment act 1997 is also applicable to the current case (ATO, 2017). This ruling provides

rules for the fringe benefit tax in case of loan account offset arrangements.

Analysis of the Case

As per the provisions of the act, the employer is deemed to have provided fringe

benefit to the employee when he provides loan at no interest rate or at the interest rate lower

than the benchmark rate. In the current case, bank provides Brian, an executive, a loan of $1

million at the interest rate of 1% per annum. The loan has been provided on April 01, 2016

and it is payable in monthly instalments. However, Brian utilized 40% of the loan amount in

the income producing activities and he met all the interest obligations in relation such

proportion of the loan (ATO, 2017). As per the provisions of the act, fringe benefit would not

be levied on the part of the loan being used by Brian in the income producing activities.

Considering these provisions, the computation of fringe benefit for the employer (Bank) for

the year 2016-17 is given below:

Particulars Amount ($)

Amount of Loan

1,000,000.0

0

Less: Loan used in income producing activities

(40%) 400,000.00

Loan amount for fringe benefit 600,000.00

Statutory rate of loan 5.65%

Actual rate of loan 1.00%

Fringe benefit interest rate 4.65%

Fringe benefit on monthly pay 2,325.00

Fringe benefit for 12 months (2325*12) 27,900.00

The computation shows that the fringe benefit payable by the bank for the year 2016-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

17 would be $27,900. If Brian (employee) pays the loan at the end of the loan period instead

of paying monthly instalments, the fringe benefit tax would be applicable at the time of

repayment of loan. Therefore, in that situation, the fringe benefit tax would be nil for the year

2016-17 (ATO, 2017).

Further, if the bank (employer) releases Brian (employee) from the re-payment of

interest on loan, the provisions of debt waiver would apply. In that case if the bank satisfies

the tax authorities that the loan was waived for genuine reasons, the fringe benefit tax would

not apply. However, the bank is not able to so satisfy the tax authorities, the fringe benefit tax

would apply in the year in which the loan waiver is given (ATO, 2017).

Conclusion

It could be concluded that the bank (employer) would be liable to pay fringe benefit

tax of a sum of $27,900 in the year 2016-17.

Question 3

Issue in Question

The issue in question is that whether the profit or loss of house property jointly owned

by two or more persons are to be allocated between or among them in the ratio of ownership

or in the ratio agreed between or among them. It is to be determined that whether the terms of

formal agreement between the two persons jointly owning a property would prevail for

taxation purposes.

Rules Applicable

The taxation ruling of TR 93/32 provides rules for distribution of the profit or loss

between the co-owners of the house property. Further, the principles enunciated in the case of

F.C. of T. v McDonald are also applicable to situation given in the current case (ATO, 2017).

17 would be $27,900. If Brian (employee) pays the loan at the end of the loan period instead

of paying monthly instalments, the fringe benefit tax would be applicable at the time of

repayment of loan. Therefore, in that situation, the fringe benefit tax would be nil for the year

2016-17 (ATO, 2017).

Further, if the bank (employer) releases Brian (employee) from the re-payment of

interest on loan, the provisions of debt waiver would apply. In that case if the bank satisfies

the tax authorities that the loan was waived for genuine reasons, the fringe benefit tax would

not apply. However, the bank is not able to so satisfy the tax authorities, the fringe benefit tax

would apply in the year in which the loan waiver is given (ATO, 2017).

Conclusion

It could be concluded that the bank (employer) would be liable to pay fringe benefit

tax of a sum of $27,900 in the year 2016-17.

Question 3

Issue in Question

The issue in question is that whether the profit or loss of house property jointly owned

by two or more persons are to be allocated between or among them in the ratio of ownership

or in the ratio agreed between or among them. It is to be determined that whether the terms of

formal agreement between the two persons jointly owning a property would prevail for

taxation purposes.

Rules Applicable

The taxation ruling of TR 93/32 provides rules for distribution of the profit or loss

between the co-owners of the house property. Further, the principles enunciated in the case of

F.C. of T. v McDonald are also applicable to situation given in the current case (ATO, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

As per the ruling, the agreement between the co-owners in relation to distribution of the profit

and losses of the property could be establish partnership between them. The partnership

between them will be deemed only when they carry on a business or trade. Further, the

principles enunciated in the case of F.C. of T. v McDonald state that mere receipt of rent from

the property is not sufficient to establish a partnership between the co-owners (ATO, 2017).

Analysis of the Case

Jack and Jill, who are husband and wife, purchased a house property by borrowing the

amount from the bank. They agreed through a formal agreement on the terms of allocation of

profit and loss from the house property between them. As per the terms Jack was entitled to

90% of the profits and remaining 10% goes to Jill. In the case of loss, the agreement provided

that Jack would be liable for the entire loss. Referring to the provisions of TR 93/32, this

agreement between Jack and Jill does not establish partnership between them. In order to

establish partnership, they should carry on a business joint owned by them. Thus, in the

absence of partnership agreement, the income of the house property would be assessed in

their individual capacity (ATO, 2017).

Therefore, the profit or loss of the house property would be divided between them in

the ratio of their ownership rather than in the ratio as agreed through formal agreement.

Assuming that Jack and Jill own the property equally, the loss of $10,000 would be shared by

them equally.

Conclusion

The conclusion is that Jack and Jill will share the loss of $10,000 in equal proportions.

Question 4

There is a clear difference between the term tax evasion and tax avoidance. The

As per the ruling, the agreement between the co-owners in relation to distribution of the profit

and losses of the property could be establish partnership between them. The partnership

between them will be deemed only when they carry on a business or trade. Further, the

principles enunciated in the case of F.C. of T. v McDonald state that mere receipt of rent from

the property is not sufficient to establish a partnership between the co-owners (ATO, 2017).

Analysis of the Case

Jack and Jill, who are husband and wife, purchased a house property by borrowing the

amount from the bank. They agreed through a formal agreement on the terms of allocation of

profit and loss from the house property between them. As per the terms Jack was entitled to

90% of the profits and remaining 10% goes to Jill. In the case of loss, the agreement provided

that Jack would be liable for the entire loss. Referring to the provisions of TR 93/32, this

agreement between Jack and Jill does not establish partnership between them. In order to

establish partnership, they should carry on a business joint owned by them. Thus, in the

absence of partnership agreement, the income of the house property would be assessed in

their individual capacity (ATO, 2017).

Therefore, the profit or loss of the house property would be divided between them in

the ratio of their ownership rather than in the ratio as agreed through formal agreement.

Assuming that Jack and Jill own the property equally, the loss of $10,000 would be shared by

them equally.

Conclusion

The conclusion is that Jack and Jill will share the loss of $10,000 in equal proportions.

Question 4

There is a clear difference between the term tax evasion and tax avoidance. The

8TAXATION LAW

earlier is illegal and unethical while the later is legally permitted though it may not be ethical

in certain circumstances. The evasion is the act of reducing the income by breaching the legal

provisions while tax avoidance implies reduction in income through legal means and without

the beach of any provision of the law. The discussion in the case of IRC v Duke of

Westminster [1936] AC 1 was undertaken around these two terms (Twining & Miers, 2010).

The principle laid down in this case was that the tax payer is legally permitted to

reduce his income. The tax payer can plan his taxes and use the benefits provided under the

income tax laws. However, contravention of the provisions is not permitted and if the tax

payer contravenes the provisions, the same would be termed as tax evasion (Twining &

Miers, 2010).

Question 5

Issue in Question

The determination of status for taxation purposes of the sale receipts of felled timber

is the issue in current question. The taxpayer received cash against the sale of felled timber,

which raises an issue that whether this sale would attract income tax or not.

Rules Applicable

Subsection 6 (1) of the Income Tax Assessment Act 1936 contains provisions that

guide the determination of the nature of receipts (Austlii.edu, 2017). Thus, resorting to the

provisions of this section, it could be clarified that whether the receipts against the sale of

felled timber would be liable for tax or not. Further, the principles stated as enunciated in the

case of McCauley v. The Federal Commissioner of Taxation, are also applicable in the given

case.

Analysis of the Case

earlier is illegal and unethical while the later is legally permitted though it may not be ethical

in certain circumstances. The evasion is the act of reducing the income by breaching the legal

provisions while tax avoidance implies reduction in income through legal means and without

the beach of any provision of the law. The discussion in the case of IRC v Duke of

Westminster [1936] AC 1 was undertaken around these two terms (Twining & Miers, 2010).

The principle laid down in this case was that the tax payer is legally permitted to

reduce his income. The tax payer can plan his taxes and use the benefits provided under the

income tax laws. However, contravention of the provisions is not permitted and if the tax

payer contravenes the provisions, the same would be termed as tax evasion (Twining &

Miers, 2010).

Question 5

Issue in Question

The determination of status for taxation purposes of the sale receipts of felled timber

is the issue in current question. The taxpayer received cash against the sale of felled timber,

which raises an issue that whether this sale would attract income tax or not.

Rules Applicable

Subsection 6 (1) of the Income Tax Assessment Act 1936 contains provisions that

guide the determination of the nature of receipts (Austlii.edu, 2017). Thus, resorting to the

provisions of this section, it could be clarified that whether the receipts against the sale of

felled timber would be liable for tax or not. Further, the principles stated as enunciated in the

case of McCauley v. The Federal Commissioner of Taxation, are also applicable in the given

case.

Analysis of the Case

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

In this case, Bill intends to sale the felled timber on the piece of land owned by him.

In the connection of this sale, he has been offered a pay of $1,000 per 100 meters of timber.

Further, there is an alternative to receive $50,000 in the lump sum from a logging company.

Under this alternative, Bill would be selling a right to remove the felled trees to the logging

company. Bill intends to use the piece of land for the purposes of gazing sheep after it is

being cleared by removing the felled trees. The question arises in front of the taxation

authorities as to how the receipts in the hands of Bill would be taxed.

The provisions of subsection 6 (1) states that the forestry operations covers the

production of the primary produces. Further, removing the felling trees is covered under the

production of primary produces which implies that the activity of removing the felling trees

would be covered under the forestry operations (ATO, 2017). Thus, if Bill is causing removal

of the felled trees, it could be deemed that he is engaged in the business activities and

carrying on the business activities attracts taxation. This means that Bill would be liable to

pay taxes on the receipts of the cash against the sale of felled trees. If Bill receives a lump

sum payment against the sale of right, the same would be taxable as royalty payment (ATO,

2017).

Conclusion

In the conclusion, it could be said that the receipts in the hands of Bill against the sale

of felled trees would liable to tax either the receipts are in lump sum or otherwise.

In this case, Bill intends to sale the felled timber on the piece of land owned by him.

In the connection of this sale, he has been offered a pay of $1,000 per 100 meters of timber.

Further, there is an alternative to receive $50,000 in the lump sum from a logging company.

Under this alternative, Bill would be selling a right to remove the felled trees to the logging

company. Bill intends to use the piece of land for the purposes of gazing sheep after it is

being cleared by removing the felled trees. The question arises in front of the taxation

authorities as to how the receipts in the hands of Bill would be taxed.

The provisions of subsection 6 (1) states that the forestry operations covers the

production of the primary produces. Further, removing the felling trees is covered under the

production of primary produces which implies that the activity of removing the felling trees

would be covered under the forestry operations (ATO, 2017). Thus, if Bill is causing removal

of the felled trees, it could be deemed that he is engaged in the business activities and

carrying on the business activities attracts taxation. This means that Bill would be liable to

pay taxes on the receipts of the cash against the sale of felled trees. If Bill receives a lump

sum payment against the sale of right, the same would be taxable as royalty payment (ATO,

2017).

Conclusion

In the conclusion, it could be said that the receipts in the hands of Bill against the sale

of felled trees would liable to tax either the receipts are in lump sum or otherwise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference

ATO. 2017. CGT assets and exemptions. Retrieved September 21, 2017, from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

ATO. 2017. Division 100- A guide to capital gains and losses. Retrieved September 21,

2017, from https://www.ato.gov.au/law/view/document?docid=PAC/19970038/100-

25

ATO. 2017. Fringe benefit tax: A guide for employers. Retrieved September 21, 2017, from

http://law.ato.gov.au/atolaw/view.htm?docid=SAV/FBTGEMP/00009&PiT=9999123

1235958

ATO. 2017. Income tax and fringe benefit tax: loan account setoff. Retrieved September 21,

2017, from http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR936/NAT/ATO

ATO. 2017. Loan Fringe Benefit. Retrieved September 21, 2017, from

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/Types-of-fringe-benefits/

Loan-fringe-benefits/

ATO. 2017. Taxation Ruling: TR 93/32. Retrieved September 21, 2017, from

https://www.ato.gov.au/law/view/document?docid=TXR/TR9332/NAT/ATO/00001

Austlii.edu. 2017. Income Tax Assessment Act 1936 - SECT 6 Interpretation. Retrieved

September 21, 2017, from

http://www6.austlii.edu.au/cgibin/viewdoc/au/legis/cth/consol_act/itaa1936240/

s6.html

CCH Australia Limited. 2011. Australian Income Tax Legislation 2011: Income Tax

Assessment Act 1997 (sections 1-1 - 717-710). CCH Australia Limited.

Reference

ATO. 2017. CGT assets and exemptions. Retrieved September 21, 2017, from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

ATO. 2017. Division 100- A guide to capital gains and losses. Retrieved September 21,

2017, from https://www.ato.gov.au/law/view/document?docid=PAC/19970038/100-

25

ATO. 2017. Fringe benefit tax: A guide for employers. Retrieved September 21, 2017, from

http://law.ato.gov.au/atolaw/view.htm?docid=SAV/FBTGEMP/00009&PiT=9999123

1235958

ATO. 2017. Income tax and fringe benefit tax: loan account setoff. Retrieved September 21,

2017, from http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR936/NAT/ATO

ATO. 2017. Loan Fringe Benefit. Retrieved September 21, 2017, from

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/Types-of-fringe-benefits/

Loan-fringe-benefits/

ATO. 2017. Taxation Ruling: TR 93/32. Retrieved September 21, 2017, from

https://www.ato.gov.au/law/view/document?docid=TXR/TR9332/NAT/ATO/00001

Austlii.edu. 2017. Income Tax Assessment Act 1936 - SECT 6 Interpretation. Retrieved

September 21, 2017, from

http://www6.austlii.edu.au/cgibin/viewdoc/au/legis/cth/consol_act/itaa1936240/

s6.html

CCH Australia Limited. 2011. Australian Income Tax Legislation 2011: Income Tax

Assessment Act 1997 (sections 1-1 - 717-710). CCH Australia Limited.

11TAXATION LAW

Twining, W. & Miers, D. 2010. How to Do Things with Rules. Cambridge University Press.

Twining, W. & Miers, D. 2010. How to Do Things with Rules. Cambridge University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.