HA3042 Taxation Law Assignment: Fringe Benefits Tax and CGT Analysis

VerifiedAdded on 2022/11/24

|9

|2279

|418

Homework Assignment

AI Summary

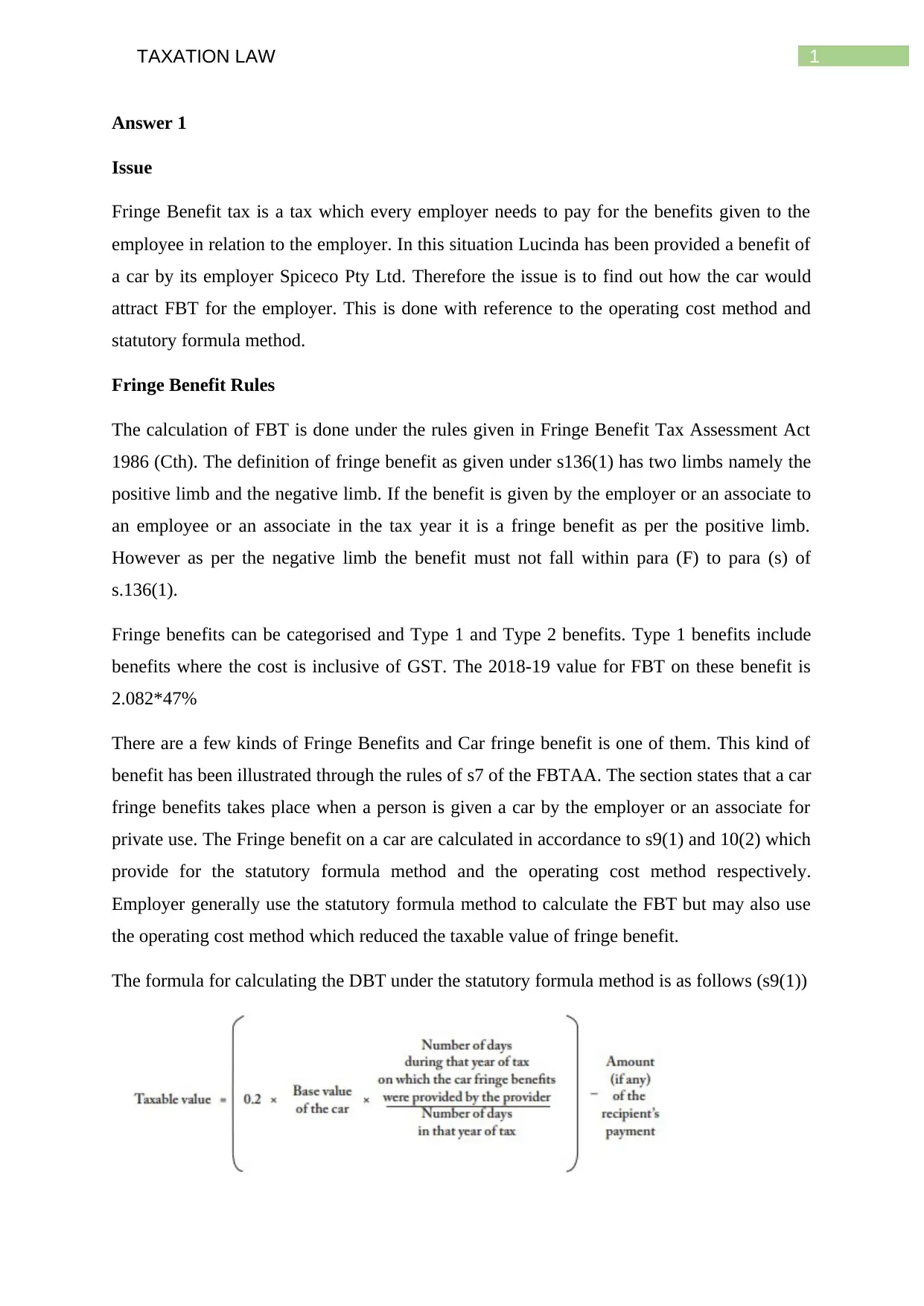

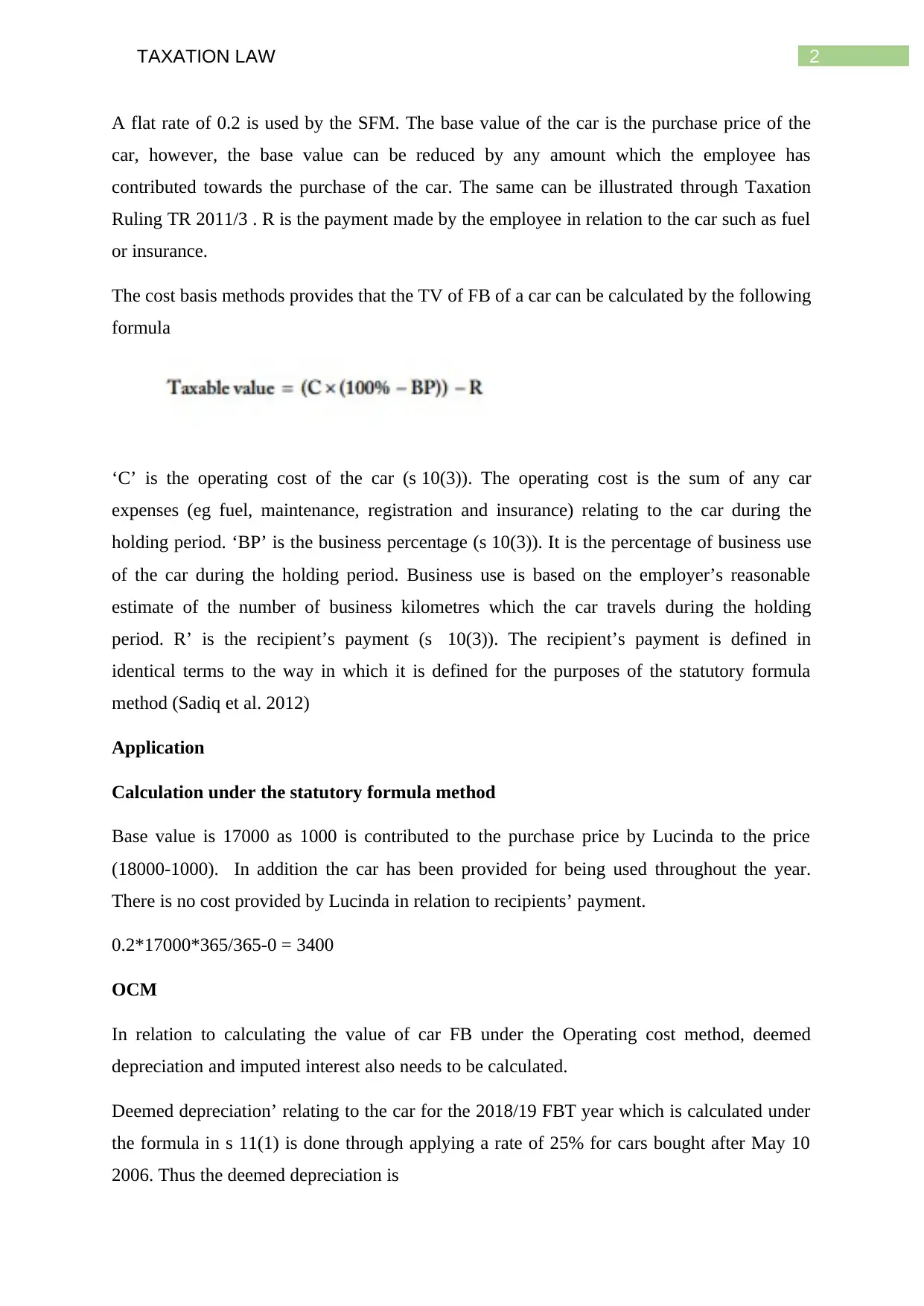

This document presents a detailed solution to a Taxation Law assignment, addressing two key areas: Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). The FBT section analyzes a car fringe benefit, calculating the taxable value using both the statutory formula method and the operating cost method, comparing the outcomes to determine the most advantageous approach. The CGT section provides an in-depth analysis of various capital gains events, including the sale of a house, an artistic painting, a luxury yacht, and shares in a mining company. It calculates capital gains or losses for each asset, considering relevant cost bases, capital proceeds, and the impact of primary place of residence exemptions. The document also addresses the treatment of capital losses and their potential to offset capital gains in the current and future tax years, concluding with the integration of capital gains into assessable income and the application of tax slabs.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.