LAW5230 Taxation Law Assignment: Analyzing CGT and Residency, 2019

VerifiedAdded on 2022/09/01

|20

|5135

|17

Homework Assignment

AI Summary

This assignment solution addresses two key parts of taxation law. Part A examines the residency status of an individual with a working holiday visa in Australia, analyzing whether her income is assessable and taxable, referencing relevant sections of the ITAA 1936 and ITAA 1997, and applying case law such as Gregory v FC of T and Nathan v FCT. The solution determines the tax implications of various income sources including salary, prize winnings, and interest. Part B delves into the small business CGT concessions, tracing their evolution from the 1999 Federal Treasurer's announcement and subsequent legislative changes. It explores the eligibility criteria, the four CGT concessions available, and the evolution of the 'simplified tax system' (STS), including the increase in revenue thresholds and the 'pick and choose' approach to concessions. The analysis compares Australian CGT provisions with those in the UK, evaluating the principles of equity, simplicity, and efficiency within the tax regime.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................4

Requirement (I):.....................................................................................................................5

Requirement (II):....................................................................................................................5

References:.................................................................................................................................6

Part B: Small Business CGT Concession...................................................................................7

References:...............................................................................................................................17

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................4

Requirement (I):.....................................................................................................................5

Requirement (II):....................................................................................................................5

References:.................................................................................................................................6

Part B: Small Business CGT Concession...................................................................................7

References:...............................................................................................................................17

2TAXATION LAW

Part A:

Issues:

Whether Catherine who has arrived in Australia with a 12 month working holiday

visa will be considered as Australian resident under “section 6 (1) ITAA 1936” or a

foreign occupant under “section 6-5 (3) ITAA 1997”?

Will the salary earned by Catherine would be included in her assessable returns and

taxable within the ordinary concept of “section 6-5, ITAA 1997”?

Laws:

“Section 6 (1) ITAA 1997”

“Section 6-5 (2) ITAA 1997”

“Section 6-5 (3) ITAA 1997”

Gregory v FC of T (1937)

Nathan v FCT (1918)

Moore v Griffiths (1972)

FCT v Spotless Services (1995)

Application:

Catherine will not be considered as Australian resident even though he stayed in

Australia for 12 months. In other words, Catherine is a foreign resident under “section 6-5

(3) ITAA 1997”. Citing “Gregory v FC of T (1937)” even though Catherine stayed in

Australia for 12 months, her behaviour demonstrated that he was a visitor1. Her main

objective was to have a working holiday in Australia and fund the same with the help of

casual employment and intermittent work2. While Catherine stayed in Brisbane she did not

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6 (2018): 296.

Part A:

Issues:

Whether Catherine who has arrived in Australia with a 12 month working holiday

visa will be considered as Australian resident under “section 6 (1) ITAA 1936” or a

foreign occupant under “section 6-5 (3) ITAA 1997”?

Will the salary earned by Catherine would be included in her assessable returns and

taxable within the ordinary concept of “section 6-5, ITAA 1997”?

Laws:

“Section 6 (1) ITAA 1997”

“Section 6-5 (2) ITAA 1997”

“Section 6-5 (3) ITAA 1997”

Gregory v FC of T (1937)

Nathan v FCT (1918)

Moore v Griffiths (1972)

FCT v Spotless Services (1995)

Application:

Catherine will not be considered as Australian resident even though he stayed in

Australia for 12 months. In other words, Catherine is a foreign resident under “section 6-5

(3) ITAA 1997”. Citing “Gregory v FC of T (1937)” even though Catherine stayed in

Australia for 12 months, her behaviour demonstrated that he was a visitor1. Her main

objective was to have a working holiday in Australia and fund the same with the help of

casual employment and intermittent work2. While Catherine stayed in Brisbane she did not

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6 (2018): 296.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

treated any habitation as if it were her “home” or as separate from any other place where

somebody may stay while they are on working holiday. Referring to the description made by

the ATO it should be noted that majority of the people that come to Australia for a working

holiday or visit are not treated as Australian dweller inside the ordinary sense of the “section

6 (1) ITAA 1997”3.

The main reason for treating Catherine as a non-resident because her visit is very

much consistent with her visa requirements and she does not have any intention of staying in

Australia however only has the intention of having a holiday while simultaneously working

for a short time period. Unlike majority of the people, Catherine holds the working and

holiday visas which is consistent with her requirements of visa and does not has the purpose

of residing in Australia, but only has the intention of having a holiday in Australia and work

for some time before coming back to home once she has finished travelling.

Unlike majority of the individuals, her behaviour while existent in Australia is not

constant with this purpose and hence not consistent with being an Australian dweller.

Catherine will not be considered as an Australian occupant inside the conventional concept of

“section 6 (1) ITAA 1997” simply because she rents a shared house with other working

holiday makers or stayed in another place for the extended time period4. As the working

holiday maker, the first $37,000 of Catherine income will be levied tax at a rate of 15% and

the balance is taxed at the ordinary rates.

Apart from the residency status of Catherine, the sources of income are primarily

relevant for the Non-residents. Referring to “Nathan v FCT (1918)” determining the original

3 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

treated any habitation as if it were her “home” or as separate from any other place where

somebody may stay while they are on working holiday. Referring to the description made by

the ATO it should be noted that majority of the people that come to Australia for a working

holiday or visit are not treated as Australian dweller inside the ordinary sense of the “section

6 (1) ITAA 1997”3.

The main reason for treating Catherine as a non-resident because her visit is very

much consistent with her visa requirements and she does not have any intention of staying in

Australia however only has the intention of having a holiday while simultaneously working

for a short time period. Unlike majority of the people, Catherine holds the working and

holiday visas which is consistent with her requirements of visa and does not has the purpose

of residing in Australia, but only has the intention of having a holiday in Australia and work

for some time before coming back to home once she has finished travelling.

Unlike majority of the individuals, her behaviour while existent in Australia is not

constant with this purpose and hence not consistent with being an Australian dweller.

Catherine will not be considered as an Australian occupant inside the conventional concept of

“section 6 (1) ITAA 1997” simply because she rents a shared house with other working

holiday makers or stayed in another place for the extended time period4. As the working

holiday maker, the first $37,000 of Catherine income will be levied tax at a rate of 15% and

the balance is taxed at the ordinary rates.

Apart from the residency status of Catherine, the sources of income are primarily

relevant for the Non-residents. Referring to “Nathan v FCT (1918)” determining the original

3 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

source of earnings is regarded as the real, hard subject of fact5. Apportionment is considered

appropriate where the income is earned from the multiple sources. The salary from

employment in Wales earned by Catherine does not has the Australian sources and hence it is

not included in her taxable returns. While the salary paid to her for her work in café, hotel

and cattle station will be included in her assessable income since it has the Australian

sources.

Later Catherine also reports prize winnings of $250. Citing “Moore v Griffiths

(1972)”, the amount of $250 is a mere prize winnings and hence it is not taxable. While she

also reports an interest income of $50 received from Australian bank account6. Citing “FCT

v Spotless Services (1995)” the interest received from Australian bank account has an

Australian sources and will be subjected to tax in Australia for Catherine.

Catherine further reports the sale of excessive clothing, sleeping bags and other

personal items on the eBay in the month of June before leaving Australia7. As Catherine is

not carrying on the business of online selling the amount of $350 and hence it will not be

contained within in her taxable income for tax purpose.

Conclusion:

Conclusively, it can be stated that Catherine will be treated as non-resident inside the

“section 6-5 (3) ITAA 1997”. She will be held taxable on her salary pay and interest returns

that is earned from Australian sources. While the salary from Wales is not from Australian

sources and hence will not be considered taxable.

5 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax

Tchrs. Ass'n 13 (2018): 307.

6 Taylor, John, et al. Understanding Taxation Law 2018. LexisNexis Butterworths, 2017.

7 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018.

Oxford University Press, 2018.

source of earnings is regarded as the real, hard subject of fact5. Apportionment is considered

appropriate where the income is earned from the multiple sources. The salary from

employment in Wales earned by Catherine does not has the Australian sources and hence it is

not included in her taxable returns. While the salary paid to her for her work in café, hotel

and cattle station will be included in her assessable income since it has the Australian

sources.

Later Catherine also reports prize winnings of $250. Citing “Moore v Griffiths

(1972)”, the amount of $250 is a mere prize winnings and hence it is not taxable. While she

also reports an interest income of $50 received from Australian bank account6. Citing “FCT

v Spotless Services (1995)” the interest received from Australian bank account has an

Australian sources and will be subjected to tax in Australia for Catherine.

Catherine further reports the sale of excessive clothing, sleeping bags and other

personal items on the eBay in the month of June before leaving Australia7. As Catherine is

not carrying on the business of online selling the amount of $350 and hence it will not be

contained within in her taxable income for tax purpose.

Conclusion:

Conclusively, it can be stated that Catherine will be treated as non-resident inside the

“section 6-5 (3) ITAA 1997”. She will be held taxable on her salary pay and interest returns

that is earned from Australian sources. While the salary from Wales is not from Australian

sources and hence will not be considered taxable.

5 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax

Tchrs. Ass'n 13 (2018): 307.

6 Taylor, John, et al. Understanding Taxation Law 2018. LexisNexis Butterworths, 2017.

7 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018.

Oxford University Press, 2018.

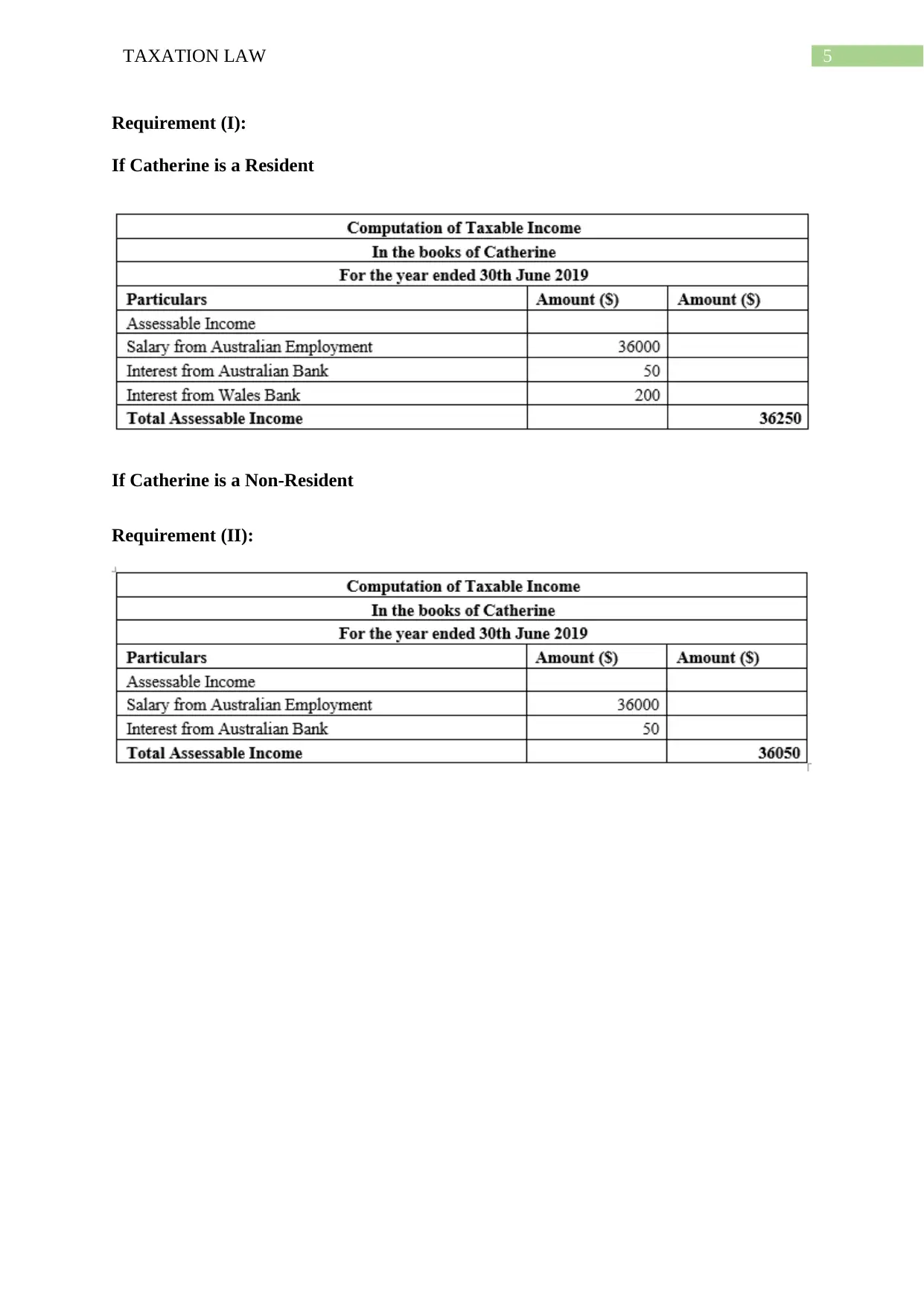

5TAXATION LAW

Requirement (I):

If Catherine is a Resident

If Catherine is a Non-Resident

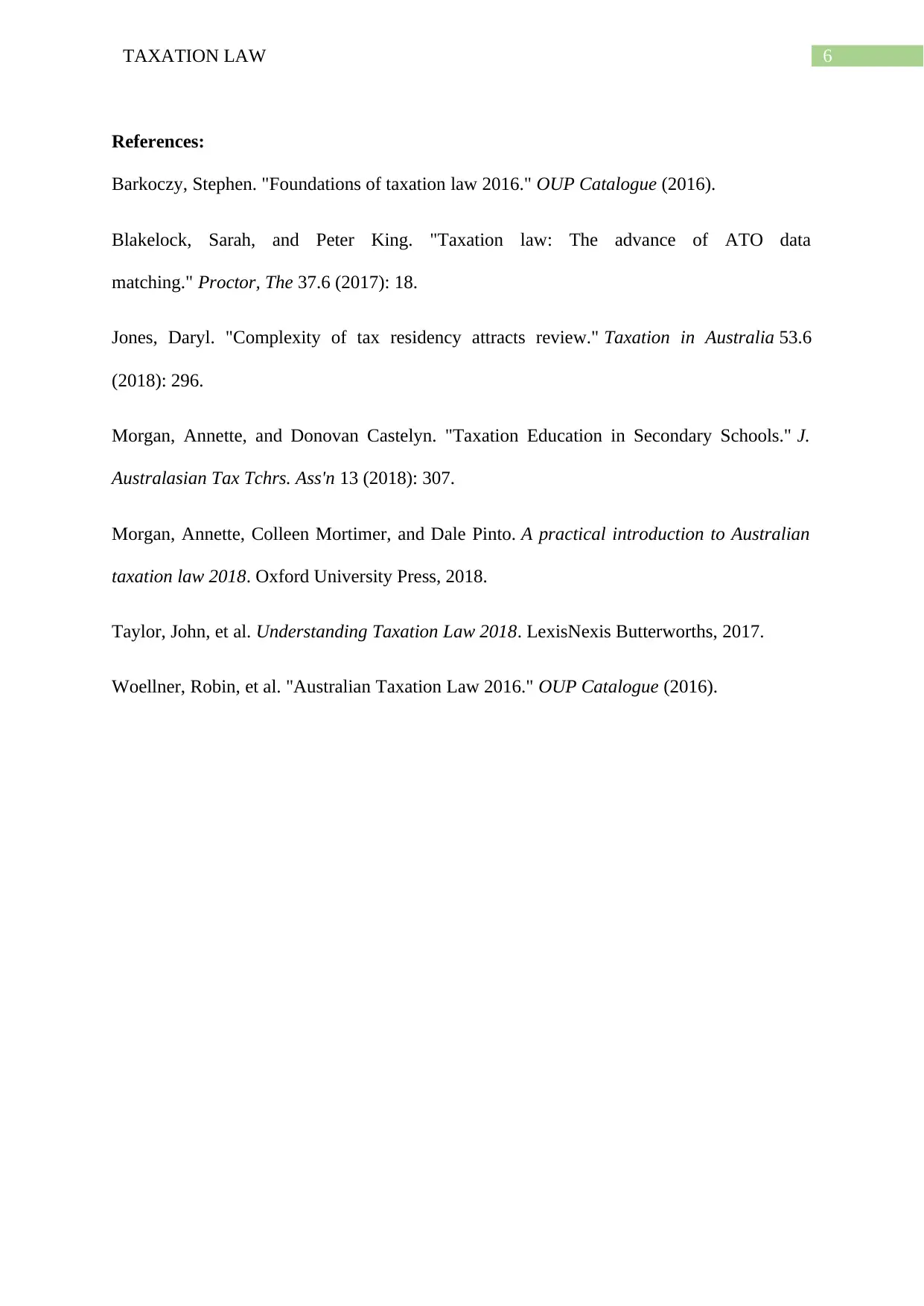

Requirement (II):

Requirement (I):

If Catherine is a Resident

If Catherine is a Non-Resident

Requirement (II):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6

(2018): 296.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Taylor, John, et al. Understanding Taxation Law 2018. LexisNexis Butterworths, 2017.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Jones, Daryl. "Complexity of tax residency attracts review." Taxation in Australia 53.6

(2018): 296.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Taylor, John, et al. Understanding Taxation Law 2018. LexisNexis Butterworths, 2017.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Part B: Small Business CGT Concession

Introduction:

The small business capital gains tax (CGT) concessions was announced on 21st

September 1999 by the Federal Treasurer. The requirements are based on milestone of

“Review of Business Taxation”. The main intention of federal government was to eliminate

the weaknesses to effective asset administration, improving capital movement, reducing the

complication and cost of compliance and making the CGT regime of Australia comparative

internationally (Sadiq and Marsden 2014). The “Division 152” comprised of four different

concessions for small business. To qualify for four CGT concession, the small business is

obligatory needed to satisfy the stringent tests. It is very much likely that the small business

would obtain noteworthy amount of concessional treatment given they are able to meet the

basic criteria.

Observation by several tax practitioners and academics have indicated that CGT

concession for small business is very complex. Concerns have been expressed that the

provisions have not been successful in attaining the desired purposes. This comprises of

critical assessment of “Division 152” against the traditional principles of good tax system.

The essay also includes comparative assessment of Australian and UK legislative provision

concerning the CGT concession for small business (Tapiolas 2017). The comparisons are

with the objective of highlighting the strength and weakness in the particular legislature to

better highlight the objectives of efficiency, simplicity and equity. The essay would examine

the CGT concession for small business comprised inside ITAA 1997. The enormous amount

of contribution that is made by the segment to the economy of Australia is the main

encouraging factor for this essay.

Part B: Small Business CGT Concession

Introduction:

The small business capital gains tax (CGT) concessions was announced on 21st

September 1999 by the Federal Treasurer. The requirements are based on milestone of

“Review of Business Taxation”. The main intention of federal government was to eliminate

the weaknesses to effective asset administration, improving capital movement, reducing the

complication and cost of compliance and making the CGT regime of Australia comparative

internationally (Sadiq and Marsden 2014). The “Division 152” comprised of four different

concessions for small business. To qualify for four CGT concession, the small business is

obligatory needed to satisfy the stringent tests. It is very much likely that the small business

would obtain noteworthy amount of concessional treatment given they are able to meet the

basic criteria.

Observation by several tax practitioners and academics have indicated that CGT

concession for small business is very complex. Concerns have been expressed that the

provisions have not been successful in attaining the desired purposes. This comprises of

critical assessment of “Division 152” against the traditional principles of good tax system.

The essay also includes comparative assessment of Australian and UK legislative provision

concerning the CGT concession for small business (Tapiolas 2017). The comparisons are

with the objective of highlighting the strength and weakness in the particular legislature to

better highlight the objectives of efficiency, simplicity and equity. The essay would examine

the CGT concession for small business comprised inside ITAA 1997. The enormous amount

of contribution that is made by the segment to the economy of Australia is the main

encouraging factor for this essay.

8TAXATION LAW

Discussion:

Australia was regarded as the last OECD nations to levy the wide-ranging tax on

capital gains upon the institution of “Part IIIA under sec 160A to 160ZZU of the ITAA

1936” applicable from 20th September 1985 (Evans et al. 2014). The chief purpose of

publicizing the capital gains was to eliminate the one-sided benefit which was existent when

a taxpayer earned a tax free capital gain in comparison to those taxpayers that derived income

which were held for taxation. In view of that, CGT is applied when the asset is disposed that

is purchased on or following 20th September 1985. Assets which is purchased earlier that date

is usually exempted from CGT and treated as pre-CGT assets. The CGT rule do not levy any

kind of distinct tax on capital gains.

As stated under “sec 6-5 and 6-10 ITAA 1997”, a taxpayer is commonly considered

taxable on all the ordinary earnings and statutory earnings which is earned in relevant income

year (Pizzacalla 2014). Any form of net capital gains is treated as statutory earnings and taxes

are levied on the taxpayer on the basis of marginal tax rate. Majority of the OECD nations

have the CGT rules in place, the tax system of Australia like those of US and New Zealand

has the origins from UK.

Before analysing the use of small business CGT concessions, it is important to

concisely sketch the CGT system together with the applicable “superannuation

concessionary regime” that possibly correspondences with the present CGT system. For a

taxpayer to be considered qualified for small business CGT concessions, it is important that a

taxpayer should meet the basic conditions that is given in “section 152-10” (Kenny 2014).

This includes that a CGT event should arise in respect of the CGT asset to a “small business

entity” or the partners in the partnership which amounts to small business entity or when the

Discussion:

Australia was regarded as the last OECD nations to levy the wide-ranging tax on

capital gains upon the institution of “Part IIIA under sec 160A to 160ZZU of the ITAA

1936” applicable from 20th September 1985 (Evans et al. 2014). The chief purpose of

publicizing the capital gains was to eliminate the one-sided benefit which was existent when

a taxpayer earned a tax free capital gain in comparison to those taxpayers that derived income

which were held for taxation. In view of that, CGT is applied when the asset is disposed that

is purchased on or following 20th September 1985. Assets which is purchased earlier that date

is usually exempted from CGT and treated as pre-CGT assets. The CGT rule do not levy any

kind of distinct tax on capital gains.

As stated under “sec 6-5 and 6-10 ITAA 1997”, a taxpayer is commonly considered

taxable on all the ordinary earnings and statutory earnings which is earned in relevant income

year (Pizzacalla 2014). Any form of net capital gains is treated as statutory earnings and taxes

are levied on the taxpayer on the basis of marginal tax rate. Majority of the OECD nations

have the CGT rules in place, the tax system of Australia like those of US and New Zealand

has the origins from UK.

Before analysing the use of small business CGT concessions, it is important to

concisely sketch the CGT system together with the applicable “superannuation

concessionary regime” that possibly correspondences with the present CGT system. For a

taxpayer to be considered qualified for small business CGT concessions, it is important that a

taxpayer should meet the basic conditions that is given in “section 152-10” (Kenny 2014).

This includes that a CGT event should arise in respect of the CGT asset to a “small business

entity” or the partners in the partnership which amounts to small business entity or when the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

taxpayer satisfies the maximum net asset value. The taxpayer should denote that the asset

should satisfy the active asset test (Norbury 2016). When a CGT asset amounts to share in

corporation or interest in the trust then there should be a CGT concession stakeholders in the

company or trust should have the contribution ratio in small business of at least 90%. On

meeting the basic eligibility criteria, a small business will be considered qualified for any one

or more of the above given CGT concession for small business.

The early purpose of “simplified tax system” (STS) provision was to enable the

qualified small business with a new policy so that they can deal with their tax. While

presenting the STS scheme in 2001, the aim of issuing the amendments was to lower the

income tax compliance burden of 95% on businesses (Toth 2014). The new STS packaged

enabled the small business with the choice of jointly adopting the package of four tax

treatments that included basic rules of depreciation, cash accounting for income tax purpose,

simplifying the rules of trading stock and the capability of claiming the immediate deduction

relating to tax for the pre-paid expenditure.

As stated previously, the added concessions relating to small business comprised of

CGT relief and GST for accounting on cash basis. Regardless of the taxpayers were provided

with CGT relief before 1999, the current regime was presented through the “New Business

Tax System” that came into effect from 1st September 1999 (Geljic, Koustas and Burke 2016).

The primary objective of introducing the amendments in 1999 was to offer the taxpayers of

small business with the straightforwardness and lowering the compliance cost by simply

rationalising and standardizing the criteria for eligibility of CGT concession for small

business. Even though the main operative provision stated under “section 328” continued to

be the same, certain significant amendments were made.

taxpayer satisfies the maximum net asset value. The taxpayer should denote that the asset

should satisfy the active asset test (Norbury 2016). When a CGT asset amounts to share in

corporation or interest in the trust then there should be a CGT concession stakeholders in the

company or trust should have the contribution ratio in small business of at least 90%. On

meeting the basic eligibility criteria, a small business will be considered qualified for any one

or more of the above given CGT concession for small business.

The early purpose of “simplified tax system” (STS) provision was to enable the

qualified small business with a new policy so that they can deal with their tax. While

presenting the STS scheme in 2001, the aim of issuing the amendments was to lower the

income tax compliance burden of 95% on businesses (Toth 2014). The new STS packaged

enabled the small business with the choice of jointly adopting the package of four tax

treatments that included basic rules of depreciation, cash accounting for income tax purpose,

simplifying the rules of trading stock and the capability of claiming the immediate deduction

relating to tax for the pre-paid expenditure.

As stated previously, the added concessions relating to small business comprised of

CGT relief and GST for accounting on cash basis. Regardless of the taxpayers were provided

with CGT relief before 1999, the current regime was presented through the “New Business

Tax System” that came into effect from 1st September 1999 (Geljic, Koustas and Burke 2016).

The primary objective of introducing the amendments in 1999 was to offer the taxpayers of

small business with the straightforwardness and lowering the compliance cost by simply

rationalising and standardizing the criteria for eligibility of CGT concession for small

business. Even though the main operative provision stated under “section 328” continued to

be the same, certain significant amendments were made.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

In detail, under the eligibility test the yearly revenue threshold was increased from $1

million to $2 million, this allowed majority of the small business to gain the benefit of

concession. Another notable changes which was made under revised SBE framework

included that the small business was now permitted to “pick and choose” which individual

concession relating to tax they would prefer to accept, instead of simply being forced to adopt

the complete package of concession (Bembrick 2017). The CGT concession for small

business comprised of substantive business concessions over the last decade with the ultimate

objective of increasing the simplicity for eligible small business.

The customary tax procedure scheme necessitates the tax regime to meet certain

number of different and usually a contradictory criterion for assessing the “good policy”.

Equity, convenience, certainty and economy is commonly referred as traditional benchmarks

(Travers 2014). There are large number of different government and regulatory bodies which

usually accepts this criterion in certain form at the time of applying the new provision of

taxation regime as well as assessing the entire tax regime. Of late, Australia has undertaken

the principles of equity, sustainability, simplicity and efficiency. On introducing the

“simplified tax system” in 2001, the main objective was to enhance the transparency and

simplicity so that the compliance of small business is reduced. The CGT concessionary

packages were considered consistent with this objective.

Opposing to the statement of federal government, the literature critically evaluating

the CGT concession for small business have argued that they fail to satisfy the criterion of

“good tax policy”. The claims are mostly related to the possibility of increased complication

and cost of compliance within the system (Gaal 2016). For example, taking into account the

first claim relating to increased easiness, it is suggested that the choice of arriving into the

concessionary regime ultimately increases the intricacy by requiring a detailed personalized

evaluation, in this manner it further adds layers to an already difficult system. This type of

In detail, under the eligibility test the yearly revenue threshold was increased from $1

million to $2 million, this allowed majority of the small business to gain the benefit of

concession. Another notable changes which was made under revised SBE framework

included that the small business was now permitted to “pick and choose” which individual

concession relating to tax they would prefer to accept, instead of simply being forced to adopt

the complete package of concession (Bembrick 2017). The CGT concession for small

business comprised of substantive business concessions over the last decade with the ultimate

objective of increasing the simplicity for eligible small business.

The customary tax procedure scheme necessitates the tax regime to meet certain

number of different and usually a contradictory criterion for assessing the “good policy”.

Equity, convenience, certainty and economy is commonly referred as traditional benchmarks

(Travers 2014). There are large number of different government and regulatory bodies which

usually accepts this criterion in certain form at the time of applying the new provision of

taxation regime as well as assessing the entire tax regime. Of late, Australia has undertaken

the principles of equity, sustainability, simplicity and efficiency. On introducing the

“simplified tax system” in 2001, the main objective was to enhance the transparency and

simplicity so that the compliance of small business is reduced. The CGT concessionary

packages were considered consistent with this objective.

Opposing to the statement of federal government, the literature critically evaluating

the CGT concession for small business have argued that they fail to satisfy the criterion of

“good tax policy”. The claims are mostly related to the possibility of increased complication

and cost of compliance within the system (Gaal 2016). For example, taking into account the

first claim relating to increased easiness, it is suggested that the choice of arriving into the

concessionary regime ultimately increases the intricacy by requiring a detailed personalized

evaluation, in this manner it further adds layers to an already difficult system. This type of

11TAXATION LAW

taxation is time taking and expensive as well, based on whether any specialized advice was

sought. The mystifying explanation relating to the criterion, demonstrated the need for ATO

interpretation in successive taxation rulings further compounded the issue.

The lowered cost of compliance is the second claimed benefits under the

concessionary regime of CGT has also attracted further scrutiny. The institution of simplified

tax regime during 2001 was viewed as deliberate act of federal government to address the

rising amount of tax compliance cost burden that was faced by the small companies and offer

them with some relief. In an attempt to sell the “simplified tax system”, the federal treasurer

in a press release endorsed the “STS” because of benefits relating to compliance cost.

Nevertheless, in spite of the frequent claims that the application of STS may lessen the cost

of compliance that is faced by the small business, the writings which was soon released

following the publication established otherwise. An argument stated by Festa (2018) noticed

that small business has noticed that “STS” contained the similar cost of compliance or even

more than the present system.

There are some scholars that have assessed the perceptions of taxpayers regarding the

CGT concessions. Taking into the account the above given issue of tax increasing cost of tax

compliance. It is fact that all the businesses are faced with cost in conforming with several

laws relating to taxation and principles. Empirical lessons conducted by Bembrick (2019)

have revealed that the cost of tax compliance is very relapsing in nature, which means that

the small business have to bear an uneven share of tax compliance cost in comparison to the

larger businesses. There are other researchers such as Hicks and Tran (2014) have discovered

that the differences in cost of compliance amongst the Australian small, medium and large

businesses was very much noteworthy with large businesses having negative cost of

compliance following the accounting for tax offsets. While medium businesses had the

taxation is time taking and expensive as well, based on whether any specialized advice was

sought. The mystifying explanation relating to the criterion, demonstrated the need for ATO

interpretation in successive taxation rulings further compounded the issue.

The lowered cost of compliance is the second claimed benefits under the

concessionary regime of CGT has also attracted further scrutiny. The institution of simplified

tax regime during 2001 was viewed as deliberate act of federal government to address the

rising amount of tax compliance cost burden that was faced by the small companies and offer

them with some relief. In an attempt to sell the “simplified tax system”, the federal treasurer

in a press release endorsed the “STS” because of benefits relating to compliance cost.

Nevertheless, in spite of the frequent claims that the application of STS may lessen the cost

of compliance that is faced by the small business, the writings which was soon released

following the publication established otherwise. An argument stated by Festa (2018) noticed

that small business has noticed that “STS” contained the similar cost of compliance or even

more than the present system.

There are some scholars that have assessed the perceptions of taxpayers regarding the

CGT concessions. Taking into the account the above given issue of tax increasing cost of tax

compliance. It is fact that all the businesses are faced with cost in conforming with several

laws relating to taxation and principles. Empirical lessons conducted by Bembrick (2019)

have revealed that the cost of tax compliance is very relapsing in nature, which means that

the small business have to bear an uneven share of tax compliance cost in comparison to the

larger businesses. There are other researchers such as Hicks and Tran (2014) have discovered

that the differences in cost of compliance amongst the Australian small, medium and large

businesses was very much noteworthy with large businesses having negative cost of

compliance following the accounting for tax offsets. While medium businesses had the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.