Taxation Law Theory, Practice & Law Assignment - HI6028

VerifiedAdded on 2022/08/21

|11

|2484

|38

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing key aspects of the Australian income tax system. The assignment solution delves into the taxability of various income sources, including salaries, wages, tips, gifts, and fringe benefits, referencing the Income Tax Act 1936 and 1997. It examines the concept of assessable income and provides guidance on the tax treatment of different scenarios. Furthermore, the solution explores capital gains tax (CGT), outlining its calculation, exemptions, and implications for assets such as houses, cars, businesses, furniture, and paintings. The solution applies taxation principles to real-life problems, interpreting relevant taxation legislation and case law to provide a clear and practical understanding of taxation concepts. The assignment covers the assessment of income, capital gains tax, and the application of relevant tax laws to specific scenarios, offering insights into how taxation principles are applied in practice.

Running Head: TAXATION LAW

Taxation Law

Name of the Students:

Name of the University:

Author Note:

Taxation Law

Name of the Students:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to question 1..............................................................................................3

Answer to question 2..............................................................................................6

Reference list........................................................................................................10

TAXATION LAW

Table of Contents

Answer to question 1..............................................................................................3

Answer to question 2..............................................................................................6

Reference list........................................................................................................10

2

TAXATION LAW

Answer to question 1

Law: According to the Income Tax Act 1936 and Income Tax Act 1997 income from

salary and wages are always taxable which includes salary, wages, any allowances,

commission, bonuses, income from part time or full time work, parental leave pay and

any other related income received under the course of employment. Gross assessable

income for the purpose of tax of an employee includes all cash remunerations from the

employer. Residential individual is are subjected to the Australian tax for the income

arise from all source. Salaries and wages of an Australian resident working in the

overseas for a period of more than 90 days then they are also eligible for exemption

from the income tax. While the foreign resident are taxable for the salary and wages

income which is earned in Australia (Bentley 2019).

Employment income is the money which is received by an individual by his or her

employer which can be paid in hand, bank transfer, cheque payment or nay other

method. Regardless of the money received for the purpose of one or more job, full time

or part time job all income is related to be included in the tax return of the individual.

There are some allowances related to the employment which is generally

provided by the employer. It includes allowances like car, travel, clothing, safety,

working condition and others. It also includes tips, attendance fees, consultation fees or

any benefit received for the service provided. While if the individual receives travel

allowances and meal allowances under any industrial law then it does not forms the part

of the tax return (Carter and Breunig 2019).

TAXATION LAW

Answer to question 1

Law: According to the Income Tax Act 1936 and Income Tax Act 1997 income from

salary and wages are always taxable which includes salary, wages, any allowances,

commission, bonuses, income from part time or full time work, parental leave pay and

any other related income received under the course of employment. Gross assessable

income for the purpose of tax of an employee includes all cash remunerations from the

employer. Residential individual is are subjected to the Australian tax for the income

arise from all source. Salaries and wages of an Australian resident working in the

overseas for a period of more than 90 days then they are also eligible for exemption

from the income tax. While the foreign resident are taxable for the salary and wages

income which is earned in Australia (Bentley 2019).

Employment income is the money which is received by an individual by his or her

employer which can be paid in hand, bank transfer, cheque payment or nay other

method. Regardless of the money received for the purpose of one or more job, full time

or part time job all income is related to be included in the tax return of the individual.

There are some allowances related to the employment which is generally

provided by the employer. It includes allowances like car, travel, clothing, safety,

working condition and others. It also includes tips, attendance fees, consultation fees or

any benefit received for the service provided. While if the individual receives travel

allowances and meal allowances under any industrial law then it does not forms the part

of the tax return (Carter and Breunig 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

Lump sum payment received which is either received during leaving a job or the

amount arrear from the previous year is assessable in the current income year and

forms the part of the income tax return. Fringe benefit is also considered as the income

in employment.

According to the Income Tax act 1997 under section 6(e) of Australia is that the

tips received by an employee directly from the customer need to be shown in the tax

return of the individual and it is the forming part of the income. While if any expenses

made by the employer towards the employee which is considered as the reward for

work then it does not need to be disclosed in the tax return as it does not forms the part

of assessable income of the individual (Cassidy 2017).

Gifts received from the customer are deductible if it is a voluntary transferred and

it have a monetary value. Gift can include money or property. For claiming deduction an

individual need to keep a proper record of the gifts received with the receipts. For

claiming deduction the monetary value of the gift must be more than $2. Gift from any

family member for any personnel reason and which is not related to any income

producing activities does not forms the part of the assessable income. While if any

interest is received on that money from the Australian bank then it need to be shown in

the tax return.

Issues: Emmi is an accounts student who studies in Holmes Institution while working as

a part time in a restaurant. During the assessment year Emmi has received some

income which consist of tips from customer and salary from the restaurant. She also got

an expensive perfume as gift from a regular customer during the Christmas which late

on she gave that to her mother. Next as she was working in a restaurant, for the

TAXATION LAW

Lump sum payment received which is either received during leaving a job or the

amount arrear from the previous year is assessable in the current income year and

forms the part of the income tax return. Fringe benefit is also considered as the income

in employment.

According to the Income Tax act 1997 under section 6(e) of Australia is that the

tips received by an employee directly from the customer need to be shown in the tax

return of the individual and it is the forming part of the income. While if any expenses

made by the employer towards the employee which is considered as the reward for

work then it does not need to be disclosed in the tax return as it does not forms the part

of assessable income of the individual (Cassidy 2017).

Gifts received from the customer are deductible if it is a voluntary transferred and

it have a monetary value. Gift can include money or property. For claiming deduction an

individual need to keep a proper record of the gifts received with the receipts. For

claiming deduction the monetary value of the gift must be more than $2. Gift from any

family member for any personnel reason and which is not related to any income

producing activities does not forms the part of the assessable income. While if any

interest is received on that money from the Australian bank then it need to be shown in

the tax return.

Issues: Emmi is an accounts student who studies in Holmes Institution while working as

a part time in a restaurant. During the assessment year Emmi has received some

income which consist of tips from customer and salary from the restaurant. She also got

an expensive perfume as gift from a regular customer during the Christmas which late

on she gave that to her mother. Next as she was working in a restaurant, for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

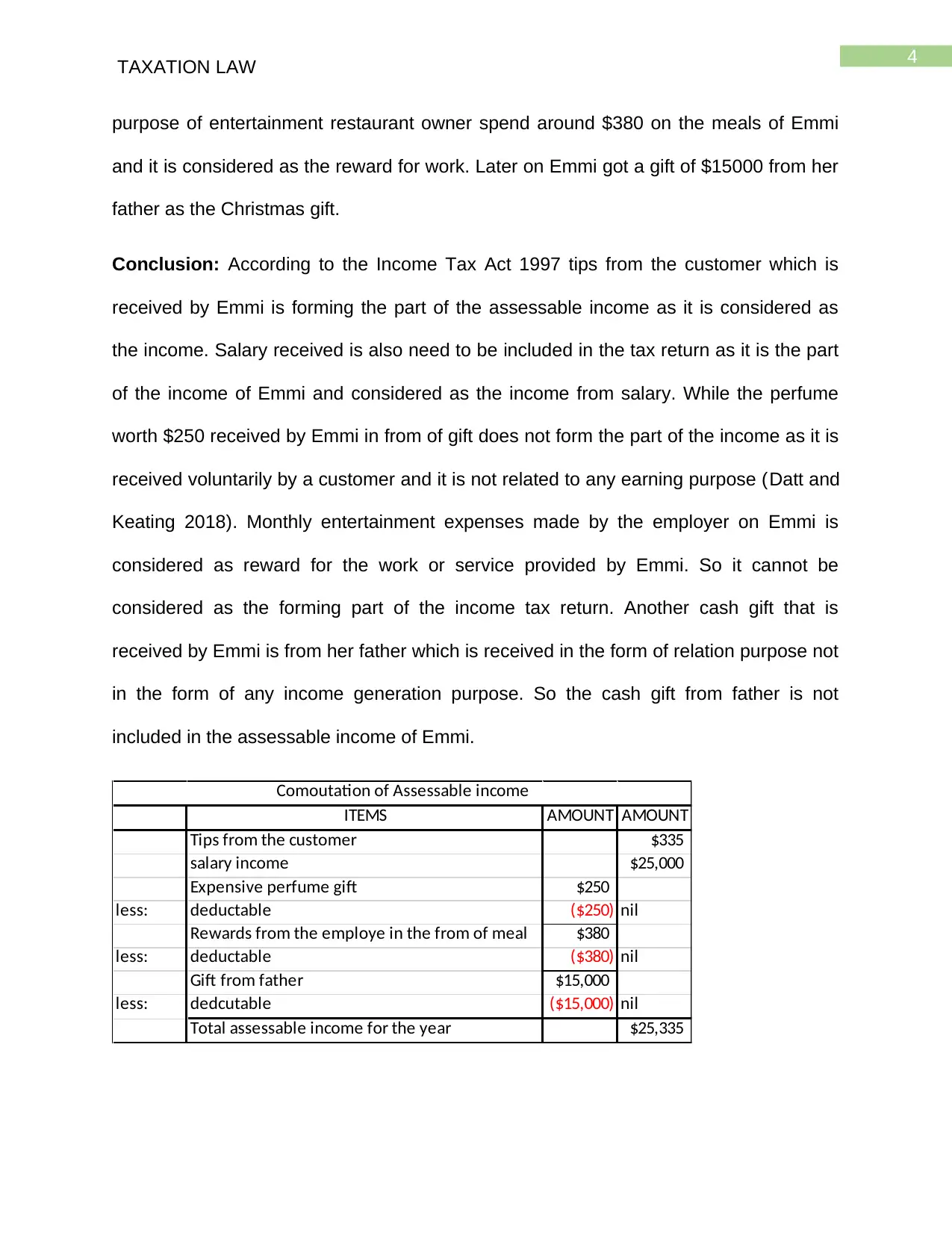

purpose of entertainment restaurant owner spend around $380 on the meals of Emmi

and it is considered as the reward for work. Later on Emmi got a gift of $15000 from her

father as the Christmas gift.

Conclusion: According to the Income Tax Act 1997 tips from the customer which is

received by Emmi is forming the part of the assessable income as it is considered as

the income. Salary received is also need to be included in the tax return as it is the part

of the income of Emmi and considered as the income from salary. While the perfume

worth $250 received by Emmi in from of gift does not form the part of the income as it is

received voluntarily by a customer and it is not related to any earning purpose (Datt and

Keating 2018). Monthly entertainment expenses made by the employer on Emmi is

considered as reward for the work or service provided by Emmi. So it cannot be

considered as the forming part of the income tax return. Another cash gift that is

received by Emmi is from her father which is received in the form of relation purpose not

in the form of any income generation purpose. So the cash gift from father is not

included in the assessable income of Emmi.

ITEMS AMOUNT AMOUNT

Tips from the customer $335

salary income $25,000

Expensive perfume gift $250

less: deductable ($250) nil

Rewards from the employe in the from of meal $380

less: deductable ($380) nil

Gift from father $15,000

less: dedcutable ($15,000) nil

Total assessable income for the year $25,335

Comoutation of Assessable income

TAXATION LAW

purpose of entertainment restaurant owner spend around $380 on the meals of Emmi

and it is considered as the reward for work. Later on Emmi got a gift of $15000 from her

father as the Christmas gift.

Conclusion: According to the Income Tax Act 1997 tips from the customer which is

received by Emmi is forming the part of the assessable income as it is considered as

the income. Salary received is also need to be included in the tax return as it is the part

of the income of Emmi and considered as the income from salary. While the perfume

worth $250 received by Emmi in from of gift does not form the part of the income as it is

received voluntarily by a customer and it is not related to any earning purpose (Datt and

Keating 2018). Monthly entertainment expenses made by the employer on Emmi is

considered as reward for the work or service provided by Emmi. So it cannot be

considered as the forming part of the income tax return. Another cash gift that is

received by Emmi is from her father which is received in the form of relation purpose not

in the form of any income generation purpose. So the cash gift from father is not

included in the assessable income of Emmi.

ITEMS AMOUNT AMOUNT

Tips from the customer $335

salary income $25,000

Expensive perfume gift $250

less: deductable ($250) nil

Rewards from the employe in the from of meal $380

less: deductable ($380) nil

Gift from father $15,000

less: dedcutable ($15,000) nil

Total assessable income for the year $25,335

Comoutation of Assessable income

5

TAXATION LAW

Answer to question 2

Law: According to the Income Tax Act 1997 under section 104-5, Capital gain tax

calculation generally rise when the capital asset is sold or disposed of for more values

than it was purchased. Capital asset consist of mutual funds, stocks, fixed assets, real

estate, crypto currency and many others. Capital gain tax arises when an individual

earns profit from the sale of the capital asset and if the individual incurs loss then the

capital loos need to be adjusted against the capital gain. Both the capital gain and loss

need to be added to the assessable income and must be filled in the return. Capital loss

cannot be claimed against any other income but can be used to reduce the value of the

capital gain. Capital gain tax is the part of the income tax calculation it is not a different

part of taxation (Davis, G., Akroyd, Pearl and Sainsbury 2019).

Capital gain or loss usually happens when the individual enters into the contract

of disposal of asset. So if the individual sign a contract to sell in previous year but made

the settlement next year than the capital gain or loss arises from it need to be settled in

the previous year tax return. If the individual is an Australian resident than CGT is

applicable in all the assets of the individual all over the world.

Two most important point for acquiring the capital gain tax is by acquiring the

assets or becoming the owner and keeping the record of every transaction which is

related to the assets. If an asset is jointly owned than it is necessary to determine the

share of each partner (Evans 2019).

TAXATION LAW

Answer to question 2

Law: According to the Income Tax Act 1997 under section 104-5, Capital gain tax

calculation generally rise when the capital asset is sold or disposed of for more values

than it was purchased. Capital asset consist of mutual funds, stocks, fixed assets, real

estate, crypto currency and many others. Capital gain tax arises when an individual

earns profit from the sale of the capital asset and if the individual incurs loss then the

capital loos need to be adjusted against the capital gain. Both the capital gain and loss

need to be added to the assessable income and must be filled in the return. Capital loss

cannot be claimed against any other income but can be used to reduce the value of the

capital gain. Capital gain tax is the part of the income tax calculation it is not a different

part of taxation (Davis, G., Akroyd, Pearl and Sainsbury 2019).

Capital gain or loss usually happens when the individual enters into the contract

of disposal of asset. So if the individual sign a contract to sell in previous year but made

the settlement next year than the capital gain or loss arises from it need to be settled in

the previous year tax return. If the individual is an Australian resident than CGT is

applicable in all the assets of the individual all over the world.

Two most important point for acquiring the capital gain tax is by acquiring the

assets or becoming the owner and keeping the record of every transaction which is

related to the assets. If an asset is jointly owned than it is necessary to determine the

share of each partner (Evans 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

There are few rule which provides exemption in the capital gain tax which is applied to

both owned asset and partial asset or tangible or intangible assets. So few exemption

rules are as follows:

Assets which are acquired before 20 September 1985, it is the date before the

application of capital gain tax.

Depreciable assets which is solely used for the taxable purpose which includes

equipment’s, machinery and many others (Freundenberg and Minas 2018).

The house or home which the taxpayer uses as his or her main residence.

Personnel assets which is acquired for the price up to $ 10000. It includes

furniture, equipment’s and many other items.

Collectable acquired up to the value of $500 which includes art, jewelry,

sculpture and other related items.

Cars and other vehicle whose carrying capacity is less than one ton or nine

passenger.

Selling of life insurance policy before maturity is considered as the ordinary

income.

Winning or losses from gambling

An individual or a taxpayer need to keep the record of all the asset for the purpose of

calculating the capital gain tax. Keeping the records of purchase price and selling price

is the most important data for determining the capital gain and loss (Hasseldine and

Fatemi 2018). Purchase price of the capital asset includes all the cost which is paid for

acquiring the assets. So it is necessary to identify the purchase price. There are three

methods to calculate the capital gain which are as follows:

TAXATION LAW

There are few rule which provides exemption in the capital gain tax which is applied to

both owned asset and partial asset or tangible or intangible assets. So few exemption

rules are as follows:

Assets which are acquired before 20 September 1985, it is the date before the

application of capital gain tax.

Depreciable assets which is solely used for the taxable purpose which includes

equipment’s, machinery and many others (Freundenberg and Minas 2018).

The house or home which the taxpayer uses as his or her main residence.

Personnel assets which is acquired for the price up to $ 10000. It includes

furniture, equipment’s and many other items.

Collectable acquired up to the value of $500 which includes art, jewelry,

sculpture and other related items.

Cars and other vehicle whose carrying capacity is less than one ton or nine

passenger.

Selling of life insurance policy before maturity is considered as the ordinary

income.

Winning or losses from gambling

An individual or a taxpayer need to keep the record of all the asset for the purpose of

calculating the capital gain tax. Keeping the records of purchase price and selling price

is the most important data for determining the capital gain and loss (Hasseldine and

Fatemi 2018). Purchase price of the capital asset includes all the cost which is paid for

acquiring the assets. So it is necessary to identify the purchase price. There are three

methods to calculate the capital gain which are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

1. Discounting method – It is the method which is applicable when the taxpayer

owns the asset for more than 12 month. Capital gain is calculated by reducing

the entire cost from the sales amount then reducing the amount by 50 %. This

methods is applicable only for the individual and for those who does not follows

indexation methods. Companies cannot apply this method as they have to pay

capital gain tax at a fixed rate of 30 percent of the capital gain (Jones 2016).

2. Indexation methods – This method is applicable when the asset is owned for

more than 12 month and the asset is acquired before 21 September 1999. It

helps in increasing the cost base of the asset as the price index method is used.

Under this method capital gain is calculated by deducting the index cost from the

sale value. This method is applicable to both company as well individuals.

3. Others method – This method is applicable when the asset is owned less than 12

month. It is the simplest method than other two methods as it is calculated by

deducting the cost from the sale price.

Issues: In this case Liu is an Australian resident who has decided to sell of all her

Australian assets and business after the retirement and get back to China. In Australia

she has house which was purchased in 1981, car which was purchased in 2011, she

also has a small business of photograph studio, some personal furniture and some

paintings. After selling this all Liu has to pay the capital gain tax to the Australian

government as all the asset belongs to the Australian asset.

TAXATION LAW

1. Discounting method – It is the method which is applicable when the taxpayer

owns the asset for more than 12 month. Capital gain is calculated by reducing

the entire cost from the sales amount then reducing the amount by 50 %. This

methods is applicable only for the individual and for those who does not follows

indexation methods. Companies cannot apply this method as they have to pay

capital gain tax at a fixed rate of 30 percent of the capital gain (Jones 2016).

2. Indexation methods – This method is applicable when the asset is owned for

more than 12 month and the asset is acquired before 21 September 1999. It

helps in increasing the cost base of the asset as the price index method is used.

Under this method capital gain is calculated by deducting the index cost from the

sale value. This method is applicable to both company as well individuals.

3. Others method – This method is applicable when the asset is owned less than 12

month. It is the simplest method than other two methods as it is calculated by

deducting the cost from the sale price.

Issues: In this case Liu is an Australian resident who has decided to sell of all her

Australian assets and business after the retirement and get back to China. In Australia

she has house which was purchased in 1981, car which was purchased in 2011, she

also has a small business of photograph studio, some personal furniture and some

paintings. After selling this all Liu has to pay the capital gain tax to the Australian

government as all the asset belongs to the Australian asset.

8

TAXATION LAW

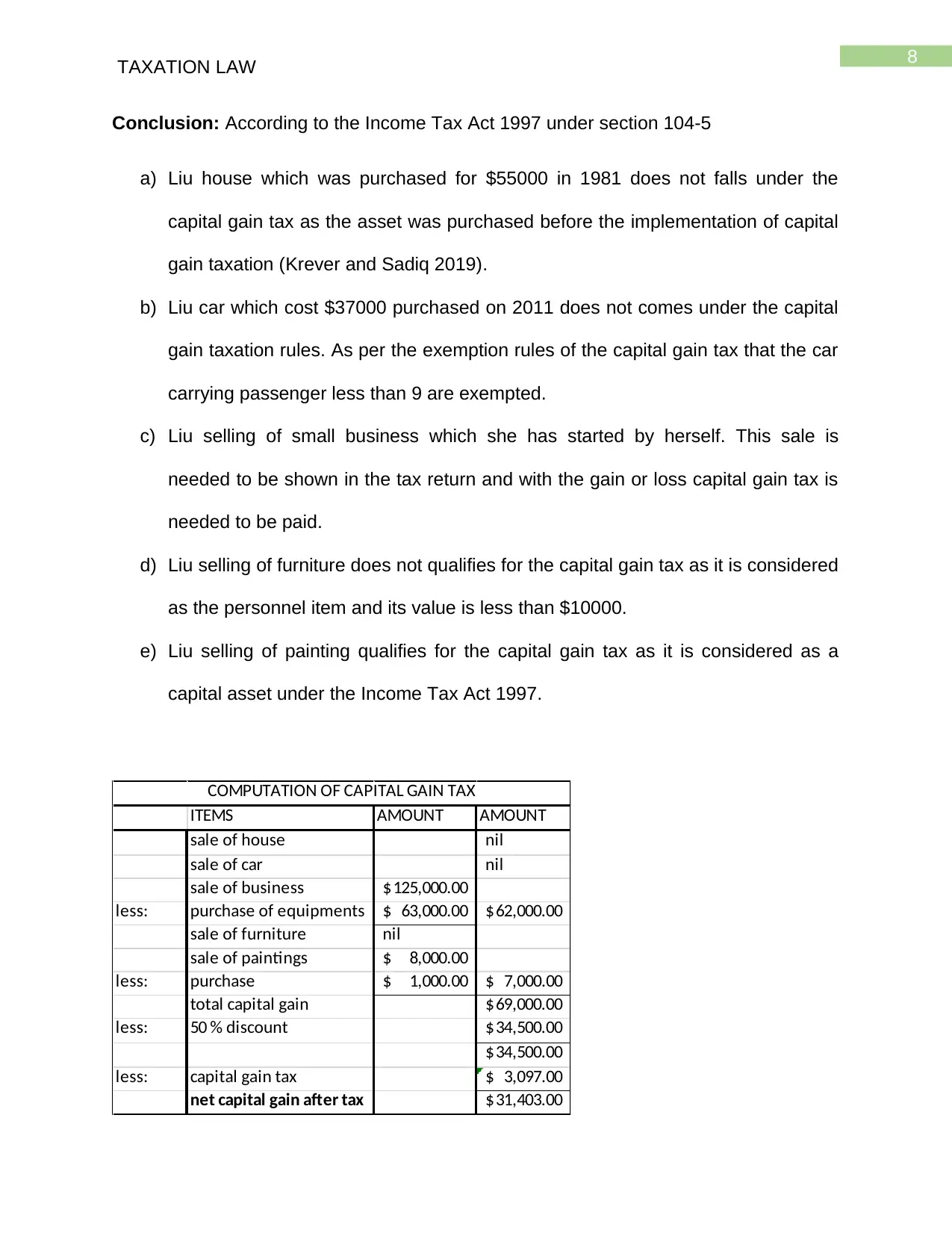

Conclusion: According to the Income Tax Act 1997 under section 104-5

a) Liu house which was purchased for $55000 in 1981 does not falls under the

capital gain tax as the asset was purchased before the implementation of capital

gain taxation (Krever and Sadiq 2019).

b) Liu car which cost $37000 purchased on 2011 does not comes under the capital

gain taxation rules. As per the exemption rules of the capital gain tax that the car

carrying passenger less than 9 are exempted.

c) Liu selling of small business which she has started by herself. This sale is

needed to be shown in the tax return and with the gain or loss capital gain tax is

needed to be paid.

d) Liu selling of furniture does not qualifies for the capital gain tax as it is considered

as the personnel item and its value is less than $10000.

e) Liu selling of painting qualifies for the capital gain tax as it is considered as a

capital asset under the Income Tax Act 1997.

ITEMS AMOUNT AMOUNT

sale of house nil

sale of car nil

sale of business 125,000.00$

less: purchase of equipments 63,000.00$ 62,000.00$

sale of furniture nil

sale of paintings 8,000.00$

less: purchase 1,000.00$ 7,000.00$

total capital gain 69,000.00$

less: 50 % discount 34,500.00$

34,500.00$

less: capital gain tax 3,097.00$

net capital gain after tax 31,403.00$

COMPUTATION OF CAPITAL GAIN TAX

TAXATION LAW

Conclusion: According to the Income Tax Act 1997 under section 104-5

a) Liu house which was purchased for $55000 in 1981 does not falls under the

capital gain tax as the asset was purchased before the implementation of capital

gain taxation (Krever and Sadiq 2019).

b) Liu car which cost $37000 purchased on 2011 does not comes under the capital

gain taxation rules. As per the exemption rules of the capital gain tax that the car

carrying passenger less than 9 are exempted.

c) Liu selling of small business which she has started by herself. This sale is

needed to be shown in the tax return and with the gain or loss capital gain tax is

needed to be paid.

d) Liu selling of furniture does not qualifies for the capital gain tax as it is considered

as the personnel item and its value is less than $10000.

e) Liu selling of painting qualifies for the capital gain tax as it is considered as a

capital asset under the Income Tax Act 1997.

ITEMS AMOUNT AMOUNT

sale of house nil

sale of car nil

sale of business 125,000.00$

less: purchase of equipments 63,000.00$ 62,000.00$

sale of furniture nil

sale of paintings 8,000.00$

less: purchase 1,000.00$ 7,000.00$

total capital gain 69,000.00$

less: 50 % discount 34,500.00$

34,500.00$

less: capital gain tax 3,097.00$

net capital gain after tax 31,403.00$

COMPUTATION OF CAPITAL GAIN TAX

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Reference list

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Carter, A. and Breunig, R., 2019. Do Earned Income Tax Credits for Older Workers

Prolong Labour Market Participation and Boost Earned Income? Evidence from

Australia's Mature Age Worker Tax Offset. Economic Record, 95(309), pp.200-226.

Cassidy, J., 2017, January. A GST with GRRRRRR: Legislative responses to GST tax

avoidance in Australia and New Zealand. In Australasian Tax Teachers Association

Conference 2017.

Datt, K.H. and Keating, M., 2018, April. The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Davis, G., Akroyd, P., Pearl, D. and Sainsbury, T., 2019. Recent personal income tax

progressivity trends in Australia (No. 2019-05). Treasury Working Paper.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Freundenberg, B. and Minas, J., 2018. Reforming Australia's 50 per cent capital gains

tax discount incrementally. eJTR, 16, p.317.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy:

the blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

TAXATION LAW

Reference list

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Carter, A. and Breunig, R., 2019. Do Earned Income Tax Credits for Older Workers

Prolong Labour Market Participation and Boost Earned Income? Evidence from

Australia's Mature Age Worker Tax Offset. Economic Record, 95(309), pp.200-226.

Cassidy, J., 2017, January. A GST with GRRRRRR: Legislative responses to GST tax

avoidance in Australia and New Zealand. In Australasian Tax Teachers Association

Conference 2017.

Datt, K.H. and Keating, M., 2018, April. The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Davis, G., Akroyd, P., Pearl, D. and Sainsbury, T., 2019. Recent personal income tax

progressivity trends in Australia (No. 2019-05). Treasury Working Paper.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Freundenberg, B. and Minas, J., 2018. Reforming Australia's 50 per cent capital gains

tax discount incrementally. eJTR, 16, p.317.

Hasseldine, J. and Fatemi, D., 2018. Tax practitioner judgements and client advocacy:

the blurred boundary between capital gains vs. ordinary income. eJTR, 16, p.303.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in

Australia, 51(2), p.67.

Krever, R. and Sadiq, K., 2019. Non-residents and capital gains tax in

Australia. Canadian Tax Journal/Revue fiscale canadienne, 67(1).

Martin, F. and Todd, T.M., 2018, August. The income tax exemption of charities and the

tax deductibility of charitable donations: the United States and Australia compared.

In Australian Tax Forum (Vol. 33, No. 4, p. 667). Tax Institute.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No.

4).

TEO, E., Barros, C. and Hinchliffe, S.A., 2016. Clash of the Deeming Provisions: Pre-

Capital Gains Tax Concessions, Tax Consolidation and Policy in the Federal Court.

Tucker, J., 2019. Tax files: The meaning of'sufficient influence'under income tax

assessment acts. Bulletin (Law Society of South Australia), 41(6), p.38.

TAXATION LAW

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in

Australia, 51(2), p.67.

Krever, R. and Sadiq, K., 2019. Non-residents and capital gains tax in

Australia. Canadian Tax Journal/Revue fiscale canadienne, 67(1).

Martin, F. and Todd, T.M., 2018, August. The income tax exemption of charities and the

tax deductibility of charitable donations: the United States and Australia compared.

In Australian Tax Forum (Vol. 33, No. 4, p. 667). Tax Institute.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No.

4).

TEO, E., Barros, C. and Hinchliffe, S.A., 2016. Clash of the Deeming Provisions: Pre-

Capital Gains Tax Concessions, Tax Consolidation and Policy in the Federal Court.

Tucker, J., 2019. Tax files: The meaning of'sufficient influence'under income tax

assessment acts. Bulletin (Law Society of South Australia), 41(6), p.38.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.