Taxation Law 13 - University Assignment: Residency, Income and Tax

VerifiedAdded on 2022/11/17

|15

|2812

|236

Homework Assignment

AI Summary

This document presents a comprehensive analysis of Australian taxation law, addressing key aspects such as residency, income, and deductions. The assignment examines the application of the Income Tax Assessment Act (ITAA) 1936 and ITAA 1997 to determine resident status using various tests including the resides test, domicile test, 183-day test, and Commonwealth Superannuation Fund test. It further explores the classification of income sources, differentiating between business and hobby income, and the tax implications of each. The assignment provides case studies to illustrate the application of tax laws, including the taxability of personal service income, business receipts, gifts, and lottery winnings. It also addresses permissible deductions for business expenses, such as contractor fees, office rent, and employee salaries, while clarifying non-deductible expenses such as private travel. The document concludes with a determination of the total tax owed and the application of carried-forward losses.

Running Head: TAXATION LAW

TAXATION LAW

Name of the Student

Name of the University

Author Note

TAXATION LAW

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................8

Issues:.....................................................................................................................................8

Rule:.......................................................................................................................................9

Application:............................................................................................................................9

Conclusion:............................................................................................................................9

Case Study Three.......................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:..........................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................8

Issues:.....................................................................................................................................8

Rule:.......................................................................................................................................9

Application:............................................................................................................................9

Conclusion:............................................................................................................................9

Case Study Three.......................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:..........................................................................................................................10

2TAXATION LAW

Conclusion:..........................................................................................................................12

References:...............................................................................................................................13

Conclusion:..........................................................................................................................12

References:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Part A:

Issues:

Conferring to the definition of “sec6 (1), ITAA 1936” will Rachel be viewed as an

Australian occupant for the relevant income year.

Rule:

The general sense of the expression “resides” as stated by the tax commissioner in the

“TR 98/17” are the people who has come to Australia as workers, migrants, teachers with

pre-determined work agreements (Woellner et al., 2016). This is stated in the in the

description of dweller in the “subsection 6 (1), ITAA 1936”.

According to “sec 6 (1), ITAA 1997” an Australian occupant is a person who is

residing in Australia with a permanent residence in Australia. The individual will be treated

as an Australian resident unless the officer is not complacent about the taxpayer having a

perpetual house anywhere outside (Barkoczy 2016) Australia and having no meaning of

leaving Australia. There are four alternative test as stated in the definition of “sec 6 (1),

ITAA 1997”. These tests are as follows-

a. The Resides Test

b. The Domicile Test

c. The 183-Day Test

d. The Commonwealth Superannuation Fund Test

The Resides Test:

Here the word “reside” means to live on a enduring basis or for a significant period of

time. Relevant considerations are required for this test such as-

Answer to question 1:

Part A:

Issues:

Conferring to the definition of “sec6 (1), ITAA 1936” will Rachel be viewed as an

Australian occupant for the relevant income year.

Rule:

The general sense of the expression “resides” as stated by the tax commissioner in the

“TR 98/17” are the people who has come to Australia as workers, migrants, teachers with

pre-determined work agreements (Woellner et al., 2016). This is stated in the in the

description of dweller in the “subsection 6 (1), ITAA 1936”.

According to “sec 6 (1), ITAA 1997” an Australian occupant is a person who is

residing in Australia with a permanent residence in Australia. The individual will be treated

as an Australian resident unless the officer is not complacent about the taxpayer having a

perpetual house anywhere outside (Barkoczy 2016) Australia and having no meaning of

leaving Australia. There are four alternative test as stated in the definition of “sec 6 (1),

ITAA 1997”. These tests are as follows-

a. The Resides Test

b. The Domicile Test

c. The 183-Day Test

d. The Commonwealth Superannuation Fund Test

The Resides Test:

Here the word “reside” means to live on a enduring basis or for a significant period of

time. Relevant considerations are required for this test such as-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. Intention of existence in Australia

b. Family, employment or business relationship

c. Maintenance or location of assets

d. Communal and living preparation.

Every factor should be given importance. Likewise, the taxpayer in “Iyengar v FCT

(2011)” who was an Australian resident and took up a two years’ overseas employment. But

managed to maintain his personal relationships and home in Australia (Jones 2018).

Domicile Test:

An individual, who has its home in Australia will be called an Australian occupant

even if it resides in overseas. A person is no more be called a resident of Australia if it can

satisfy the ATO about choosing another country as the permanent home of its own. Several

relevant factors like relationship durability of a person having with Australia is considered

important. The law court in “Applegate v FCT (1979)” stated that Applegate besides

maintaining its domicile has also established a permanent house somewhere outside Australia

(Norbury 2019). The intention of the person for living permanently or temporarily is also an

important factor to be considered.

The 183-Day test:

The 183-Day test identifies the existence of Australian either on a constant basis or

for 183 or more days in breaks.

Superannuation Fund Test:

The Superannuation test is applicable for those who has a membership of a particular

commonwealth super fund.

Sources of Income:

a. Intention of existence in Australia

b. Family, employment or business relationship

c. Maintenance or location of assets

d. Communal and living preparation.

Every factor should be given importance. Likewise, the taxpayer in “Iyengar v FCT

(2011)” who was an Australian resident and took up a two years’ overseas employment. But

managed to maintain his personal relationships and home in Australia (Jones 2018).

Domicile Test:

An individual, who has its home in Australia will be called an Australian occupant

even if it resides in overseas. A person is no more be called a resident of Australia if it can

satisfy the ATO about choosing another country as the permanent home of its own. Several

relevant factors like relationship durability of a person having with Australia is considered

important. The law court in “Applegate v FCT (1979)” stated that Applegate besides

maintaining its domicile has also established a permanent house somewhere outside Australia

(Norbury 2019). The intention of the person for living permanently or temporarily is also an

important factor to be considered.

The 183-Day test:

The 183-Day test identifies the existence of Australian either on a constant basis or

for 183 or more days in breaks.

Superannuation Fund Test:

The Superannuation test is applicable for those who has a membership of a particular

commonwealth super fund.

Sources of Income:

5TAXATION LAW

The sources of income are ascertained on the basis of determination of material facts

(Burman et al., 2016). The liability of tax imposition originates when the services are carried

forward according to the federal court stated in “FCT v French (1957)”.

Application:

The available evidences show that Racheal stayed in Australia for 12 months as the

service of agreement required her to stay till 1st December in Australia. The four relevant test

is applied for Racheal’s case according to “sec 6 (1), ITAA 1936”.

Resides Test:

Racheal is an Australian dweller under “reside” test. Since Racheal is present in

Australia for substantial time. Referring the tax ruling of “TR 98/17” Racheal visited

Australia with a pre-arranged contract with her company in which she is employed (Keyzer,

Goff and Fisher 2017). Referring “Iyengar v FCT (2011)” Racheal is an Australian dweller

as she is living in Australian for 12 months. Other factors such as maintenance of home in

Australia contributes to her physical presence.

Domicile Test:

Racheal does not has a enduring home in Australia. Referring to “FCT v Applegate

(1979)” Racheal permanent home is in UK and she cannot be held resident under Domicile

Test.

The 183-Day Test:

Notwithstanding that Racheal is a citizen of Australia under “Resides Test”, she is an

Australian dweller under 183-days since she is existent in Australia for 12 months during the

year. On satisfying the 183-day test Racheal is Australian dweller inside the classification of

“sec 6 (1), ITAA 1936”.

The sources of income are ascertained on the basis of determination of material facts

(Burman et al., 2016). The liability of tax imposition originates when the services are carried

forward according to the federal court stated in “FCT v French (1957)”.

Application:

The available evidences show that Racheal stayed in Australia for 12 months as the

service of agreement required her to stay till 1st December in Australia. The four relevant test

is applied for Racheal’s case according to “sec 6 (1), ITAA 1936”.

Resides Test:

Racheal is an Australian dweller under “reside” test. Since Racheal is present in

Australia for substantial time. Referring the tax ruling of “TR 98/17” Racheal visited

Australia with a pre-arranged contract with her company in which she is employed (Keyzer,

Goff and Fisher 2017). Referring “Iyengar v FCT (2011)” Racheal is an Australian dweller

as she is living in Australian for 12 months. Other factors such as maintenance of home in

Australia contributes to her physical presence.

Domicile Test:

Racheal does not has a enduring home in Australia. Referring to “FCT v Applegate

(1979)” Racheal permanent home is in UK and she cannot be held resident under Domicile

Test.

The 183-Day Test:

Notwithstanding that Racheal is a citizen of Australia under “Resides Test”, she is an

Australian dweller under 183-days since she is existent in Australia for 12 months during the

year. On satisfying the 183-day test Racheal is Australian dweller inside the classification of

“sec 6 (1), ITAA 1936”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

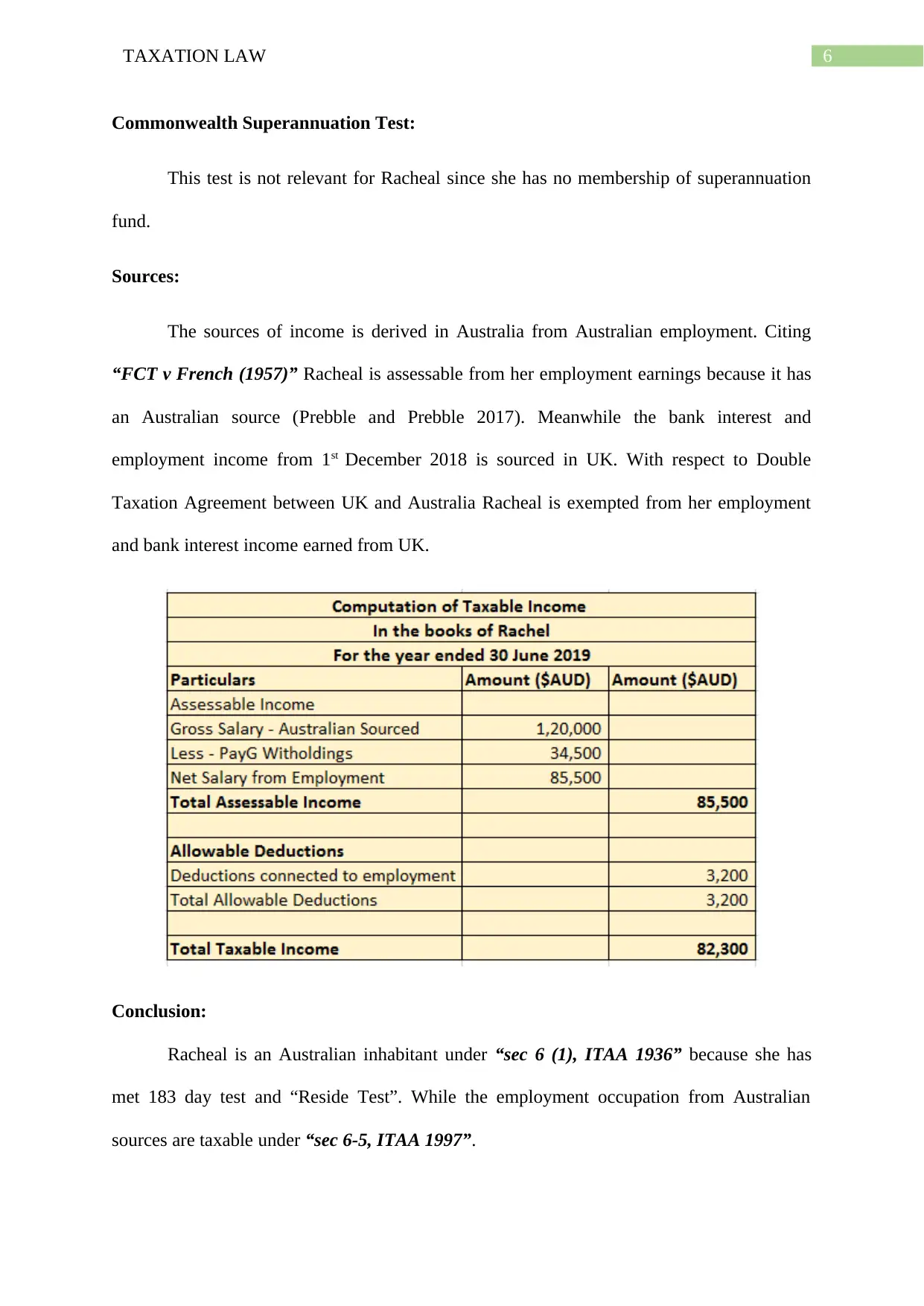

Commonwealth Superannuation Test:

This test is not relevant for Racheal since she has no membership of superannuation

fund.

Sources:

The sources of income is derived in Australia from Australian employment. Citing

“FCT v French (1957)” Racheal is assessable from her employment earnings because it has

an Australian source (Prebble and Prebble 2017). Meanwhile the bank interest and

employment income from 1st December 2018 is sourced in UK. With respect to Double

Taxation Agreement between UK and Australia Racheal is exempted from her employment

and bank interest income earned from UK.

Conclusion:

Racheal is an Australian inhabitant under “sec 6 (1), ITAA 1936” because she has

met 183 day test and “Reside Test”. While the employment occupation from Australian

sources are taxable under “sec 6-5, ITAA 1997”.

Commonwealth Superannuation Test:

This test is not relevant for Racheal since she has no membership of superannuation

fund.

Sources:

The sources of income is derived in Australia from Australian employment. Citing

“FCT v French (1957)” Racheal is assessable from her employment earnings because it has

an Australian source (Prebble and Prebble 2017). Meanwhile the bank interest and

employment income from 1st December 2018 is sourced in UK. With respect to Double

Taxation Agreement between UK and Australia Racheal is exempted from her employment

and bank interest income earned from UK.

Conclusion:

Racheal is an Australian inhabitant under “sec 6 (1), ITAA 1936” because she has

met 183 day test and “Reside Test”. While the employment occupation from Australian

sources are taxable under “sec 6-5, ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Part B:

Issues:

Whether or not John will be viewed Australian dweller under “subsection 6 (1),

ITAA 1936”.

Rule:

Resides Test:

Reside test implies to live in Australia for considerably or permanently. The “resides

test” includes a person’s behavior when they are present in Australia. It takes into

consideration the intention of coming to Australia and place of fixed home in Australia

(Sadiq 2019). The judgment in “Dempsey v FC of T (2014)” considered taxpayer was

employed in Saudi Arabia and was held as not a dweller of Australia. This is because the

taxpayer has the intention of living outside Australia.

Domicile Test:

Domicile implies the permanent home of the taxpayer. The Federal Court in

“Harding v FCT (2019)” considered taxpayer as non-resident because he had permanent

home in Bahrain (Butler 2019).

The 183-Day test:

The 183-Day test classifies the presence of an Australian citizen either on a incessant

base or for 183 or more days in interruptions.

Superannuation Fund Test:

The Superannuation test is valid for those who has an association of a particular

commonwealth super fund.

Answer to Part B:

Issues:

Whether or not John will be viewed Australian dweller under “subsection 6 (1),

ITAA 1936”.

Rule:

Resides Test:

Reside test implies to live in Australia for considerably or permanently. The “resides

test” includes a person’s behavior when they are present in Australia. It takes into

consideration the intention of coming to Australia and place of fixed home in Australia

(Sadiq 2019). The judgment in “Dempsey v FC of T (2014)” considered taxpayer was

employed in Saudi Arabia and was held as not a dweller of Australia. This is because the

taxpayer has the intention of living outside Australia.

Domicile Test:

Domicile implies the permanent home of the taxpayer. The Federal Court in

“Harding v FCT (2019)” considered taxpayer as non-resident because he had permanent

home in Bahrain (Butler 2019).

The 183-Day test:

The 183-Day test classifies the presence of an Australian citizen either on a incessant

base or for 183 or more days in interruptions.

Superannuation Fund Test:

The Superannuation test is valid for those who has an association of a particular

commonwealth super fund.

8TAXATION LAW

Application:

The relevant test is implemented to understand the resident status of John.

Resides Test:

Under this test John is not Australian resident. This is because he is out of Australia

from a very long time and has also taken all his belongings to Brunei. Referring to “Dempsey

v FCT (2014)” John has expressed his intention to live in Brunei (Morgan, Mortimer and

Pinto 2018). John has successfully passed the “resides test”.

Domicile Test:

After going to Brunei John has demonstrated that he choice of home is in Brunei and

has also renewed his Brunie apartment lease for another 12 months. Referring to “Harding v

FCT (2019)” John is not an Australian under this test (Murray et al. 2018).

183-Day Test:

John was not present in Australia for both 2017/18 and 2018/19. Hence, this test is not

relevant.

Commonwealth Superannuation Test:

This does not applies to John.

Conclusion:

The test conducted above states that John has a place of abode in Brunei and he

should be considered foreign inhabitant under “sec 995-1 (1), ITAA 1997”.

Application:

The relevant test is implemented to understand the resident status of John.

Resides Test:

Under this test John is not Australian resident. This is because he is out of Australia

from a very long time and has also taken all his belongings to Brunei. Referring to “Dempsey

v FCT (2014)” John has expressed his intention to live in Brunei (Morgan, Mortimer and

Pinto 2018). John has successfully passed the “resides test”.

Domicile Test:

After going to Brunei John has demonstrated that he choice of home is in Brunei and

has also renewed his Brunie apartment lease for another 12 months. Referring to “Harding v

FCT (2019)” John is not an Australian under this test (Murray et al. 2018).

183-Day Test:

John was not present in Australia for both 2017/18 and 2018/19. Hence, this test is not

relevant.

Commonwealth Superannuation Test:

This does not applies to John.

Conclusion:

The test conducted above states that John has a place of abode in Brunei and he

should be considered foreign inhabitant under “sec 995-1 (1), ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Case Study 2: Part A:

Issues:

Is the painting receipts amounts to business proceeds or hobby under “section 995-1,

ITAA 1997”?

Rule:

Under “sec 6-5, ITAA 1997”, gains from business amounts to ordinary earnings while

gains from non-commercial undertakings such as hobby is not a taxable income (Morgan and

Castelyn 2018). Important factors such as presence of profit earning intention is important

factor in classifying the receipts of hobby as income. In “Stone v FCT (2005)” lack of profit

deriving intent cannot prohibit an activity from being treated as business. The degree of

capital and regularity of activity or any commercial approach undertaken must be considered.

Application:

Nadine to relieve her work stress does paintings. On being advice by one her friend

she decides to display her paintings in market for sale and also earned $4,500 as sales

receipts. The receipts from Nadine’s painting is not an income. Referring to “Stone v FCT

(2005)” her activities is only for relieving stress and only for hobby purpose (Cavenagh et al.

2018). Nadine also has no such intent of making profit nor does her activity involved any

regularity. No commercial approach was taken by her so her activities are classified as hobby.

Conclusion:

The proceeds from sale of painting is classified as hobby and the sum of $4,500 is not

a taxable income.

Case Study 2: Part A:

Issues:

Is the painting receipts amounts to business proceeds or hobby under “section 995-1,

ITAA 1997”?

Rule:

Under “sec 6-5, ITAA 1997”, gains from business amounts to ordinary earnings while

gains from non-commercial undertakings such as hobby is not a taxable income (Morgan and

Castelyn 2018). Important factors such as presence of profit earning intention is important

factor in classifying the receipts of hobby as income. In “Stone v FCT (2005)” lack of profit

deriving intent cannot prohibit an activity from being treated as business. The degree of

capital and regularity of activity or any commercial approach undertaken must be considered.

Application:

Nadine to relieve her work stress does paintings. On being advice by one her friend

she decides to display her paintings in market for sale and also earned $4,500 as sales

receipts. The receipts from Nadine’s painting is not an income. Referring to “Stone v FCT

(2005)” her activities is only for relieving stress and only for hobby purpose (Cavenagh et al.

2018). Nadine also has no such intent of making profit nor does her activity involved any

regularity. No commercial approach was taken by her so her activities are classified as hobby.

Conclusion:

The proceeds from sale of painting is classified as hobby and the sum of $4,500 is not

a taxable income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Case Study Three

Issues:

Is the money earned from personal services and business receipts are taxable as ordinary

earnings under “sec 6-5, ITAA 1997”.

Rule:

Income derived from own efforts under “sec 6, ITAA 1936” are considered taxable as

ordinary earnings. In “Dean v FCT (1997)” salary received from service was a chargeable

pays under “sec 6-5, ITAA 1997”. While gains that do hold income nature are not held for

tax. The Federal Court in “Hayes v FCT (1956)” stated that gift received as shares by former

boss was not a taxable income (Main 2019). Receipts of interest is taxable under “section 15-

35”. While windfall gains does not attracts tax liability. In “Moore v Griffiths (1972)” mere

prize earnings was not a chargeable earnings.

Deduction for expenses is allowed in “section 8-1, ITAA 1997” to taxpayers when it

is occurred in creating an calculable income. This includes outgoings occurred in the ordinary

business course (Morgan and Castelyn 2018). Whereas taxpayer are deprived of deduction

under “negative limbs” of “sec 8-1(2)” for outgoings that are capital or private expenses.

Small business with revenues of less than $10 million or less is permitted to instantly

write off the assets purchased for $20,000 or less. Entertainment expenses by way of meal or

food is permissible as tax deduction under “sec 32-10 (1), ITAA 1997”. Travel from home

and office is a private expenditures and not permitted for deduction under “sec 8-1, ITAA

1997”. In “Lunney v FCT (1958)” deduction was disallowed to taxpayer for travelling

amongst home and office.

Case Study Three

Issues:

Is the money earned from personal services and business receipts are taxable as ordinary

earnings under “sec 6-5, ITAA 1997”.

Rule:

Income derived from own efforts under “sec 6, ITAA 1936” are considered taxable as

ordinary earnings. In “Dean v FCT (1997)” salary received from service was a chargeable

pays under “sec 6-5, ITAA 1997”. While gains that do hold income nature are not held for

tax. The Federal Court in “Hayes v FCT (1956)” stated that gift received as shares by former

boss was not a taxable income (Main 2019). Receipts of interest is taxable under “section 15-

35”. While windfall gains does not attracts tax liability. In “Moore v Griffiths (1972)” mere

prize earnings was not a chargeable earnings.

Deduction for expenses is allowed in “section 8-1, ITAA 1997” to taxpayers when it

is occurred in creating an calculable income. This includes outgoings occurred in the ordinary

business course (Morgan and Castelyn 2018). Whereas taxpayer are deprived of deduction

under “negative limbs” of “sec 8-1(2)” for outgoings that are capital or private expenses.

Small business with revenues of less than $10 million or less is permitted to instantly

write off the assets purchased for $20,000 or less. Entertainment expenses by way of meal or

food is permissible as tax deduction under “sec 32-10 (1), ITAA 1997”. Travel from home

and office is a private expenditures and not permitted for deduction under “sec 8-1, ITAA

1997”. In “Lunney v FCT (1958)” deduction was disallowed to taxpayer for travelling

amongst home and office.

11TAXATION LAW

Application:

The receipt of $450,000 from accounting business is chargeable as normal business

proceeds under “sec 6-5, ITAA 1997”. Sam reports receipts of wedding gift amounting to

$10,000. Citing “Hayes v FCT (1956)” the wedding gift amount is exempted from tax since

it is a personal gift. Incentives for advertisement by Sam from publishing company is

assessable business receipts under “sec 6-5, ITAA 1997”.

The part-time employment wages received by Sam amounts to personal exertion

income and taxable under as normal receipts under “sec 6-5, ITAA 1997”. While the bank

interest will be chargeable income for Sam under “section 15-35” (Keyzer, Goff and Fisher

2017). Citing “Moore v Griffiths (1972)” winnings from lottery of $15,000 is a non-taxable

windfall gain.

Business expenses of S contractor, office rent and salary to employee is permissible

business deduction under “sec 8-1, ITAA 1997” because it was occurred in ordinary business

course for making income. The photocopier bought by Sam is allowed for immediate write-

off since its cost base is less than $20,000. The meal expenses on client is deductible under

“sec 32-10 (1), ITAA 1997”.

No deduction for travel expense is permitted to Sam under “sec 8-1, ITAA 1997”.

Citing “Lunney v FCT (1958)” Sam cannot claim general deduction for private travel

expense. The carried forward loss of $12,000 is permitted for offset from exempted income

and hence it should be subsequently carried forward to next year.

Application:

The receipt of $450,000 from accounting business is chargeable as normal business

proceeds under “sec 6-5, ITAA 1997”. Sam reports receipts of wedding gift amounting to

$10,000. Citing “Hayes v FCT (1956)” the wedding gift amount is exempted from tax since

it is a personal gift. Incentives for advertisement by Sam from publishing company is

assessable business receipts under “sec 6-5, ITAA 1997”.

The part-time employment wages received by Sam amounts to personal exertion

income and taxable under as normal receipts under “sec 6-5, ITAA 1997”. While the bank

interest will be chargeable income for Sam under “section 15-35” (Keyzer, Goff and Fisher

2017). Citing “Moore v Griffiths (1972)” winnings from lottery of $15,000 is a non-taxable

windfall gain.

Business expenses of S contractor, office rent and salary to employee is permissible

business deduction under “sec 8-1, ITAA 1997” because it was occurred in ordinary business

course for making income. The photocopier bought by Sam is allowed for immediate write-

off since its cost base is less than $20,000. The meal expenses on client is deductible under

“sec 32-10 (1), ITAA 1997”.

No deduction for travel expense is permitted to Sam under “sec 8-1, ITAA 1997”.

Citing “Lunney v FCT (1958)” Sam cannot claim general deduction for private travel

expense. The carried forward loss of $12,000 is permitted for offset from exempted income

and hence it should be subsequently carried forward to next year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.