Taxation Law: Income Tax and CGT Assignment - HI6028

VerifiedAdded on 2022/08/31

|12

|2860

|16

Homework Assignment

AI Summary

This Taxation Law assignment solution addresses two main questions. The first question examines the assessability of various income sources, including tips, employment income, gifts, and fringe benefits, under the Income Tax Assessment Act 1997 (ITAA 1997). It analyzes relevant case law, such as Calvert v Wainwright (1947) and Scott v CT (1935), to determine the tax treatment of different receipts. The second question focuses on Capital Gains Tax (CGT), exploring concepts like pre-CGT assets, personal use assets, small business concessions, and collectables. It applies CGT rules to specific scenarios, including the sale of a house, a car, business goodwill, furniture, and paintings. The solution references key sections of the ITAA 1997 and relevant tax rulings to provide a comprehensive analysis of each issue.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer to C:..........................................................................................................................7

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Will Emmi be held assessable for numerous receipt from her employment inside the

ordinary denotation of “sec 6-5 ITAA 1997”?

Rule:

According to the “sec 6-5 (1) ITAA 1997” it takes into the account the ordinary

earnings for tax purpose. Noting “sec 6-5 ITAA 1997” an individual taxpayer taxable

earnings involves the pay that is earned in agreement with the ordinary concepts. A “nexus”

with the receipt originating from the personal service of taxpayer amounts to ordinary income

(Miller & Oats, 2016). Unexpected or voluntary payments given to a taxpayer as the part of

service amounts to an ordinary earnings. As noted in “Calvert v Wainwright (1947)” the

receipt of tips by the taxi driver represents the occurrence of work and chargeable as ordinary

earnings.

The income producing actions of the taxpayer usually involves the income personal

exertion in the form of services, employment, one off services etc. Usually majority of the

earnings earned by a taxpayer is regarded as ordinary pay (Barkoczy, 2016). The law court in

“Scott v CT (1935)” the word income should not be treated as the word of art and requires

the use of necessary values to treat the earnings as income.

Gift received by taxpayer relating to private qualities is not an ordinary earnings.

While gift arising out of taxpayer’s capability to work or from the employment agreement is

regarded as ordinary income (Gashenko et al., 2019). As noted in “Hayes v FCT (1956)” the

receipt of shares in a company by an accountant from his previous boss or business owner

cannot be regarded as ordinary income and hence non-assessable for recipient.

Answer to question 1:

Issues:

Will Emmi be held assessable for numerous receipt from her employment inside the

ordinary denotation of “sec 6-5 ITAA 1997”?

Rule:

According to the “sec 6-5 (1) ITAA 1997” it takes into the account the ordinary

earnings for tax purpose. Noting “sec 6-5 ITAA 1997” an individual taxpayer taxable

earnings involves the pay that is earned in agreement with the ordinary concepts. A “nexus”

with the receipt originating from the personal service of taxpayer amounts to ordinary income

(Miller & Oats, 2016). Unexpected or voluntary payments given to a taxpayer as the part of

service amounts to an ordinary earnings. As noted in “Calvert v Wainwright (1947)” the

receipt of tips by the taxi driver represents the occurrence of work and chargeable as ordinary

earnings.

The income producing actions of the taxpayer usually involves the income personal

exertion in the form of services, employment, one off services etc. Usually majority of the

earnings earned by a taxpayer is regarded as ordinary pay (Barkoczy, 2016). The law court in

“Scott v CT (1935)” the word income should not be treated as the word of art and requires

the use of necessary values to treat the earnings as income.

Gift received by taxpayer relating to private qualities is not an ordinary earnings.

While gift arising out of taxpayer’s capability to work or from the employment agreement is

regarded as ordinary income (Gashenko et al., 2019). As noted in “Hayes v FCT (1956)” the

receipt of shares in a company by an accountant from his previous boss or business owner

cannot be regarded as ordinary income and hence non-assessable for recipient.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

According to the reconciliation rule given in “sec 6-25 (2)”, if an amount represents

both the aspects of statutory earnings and ordinary earnings then in such a situation the rules

concerning to the statutory earnings prevails excepting when there are any contrary intentions

is given. Alternatively, if the employer provides any fringe benefit to the worker, then the

benefit would be treated as non-assessable pay for the employee under “sec 23L ITAA 1936”

and the employer in such circumstances will be held liable for FBT based on the value of

benefit given (Woellner et al., 2016). As held in “Essenboourne Pty Ltd v FCT (2002)” held

that a fringe benefit will only happen when the benefit is directly related to a particular

employee.

There are also certain types of receipts apart from the ordinary income or capital

which usually arise. Gifts and lottery winnings are not considered taxable earnings since the

requirements associated to assessment provision is not met. Purely personal gifts are not

treated as chargeable pay (Blakelock & King, 2017). As noted in “Scott v FCT (1966)”

receipt of 10,000 pounds gift from a client’s wife out of husband estate is not regarded as

income. The gift was simply unsolicited.

Application:

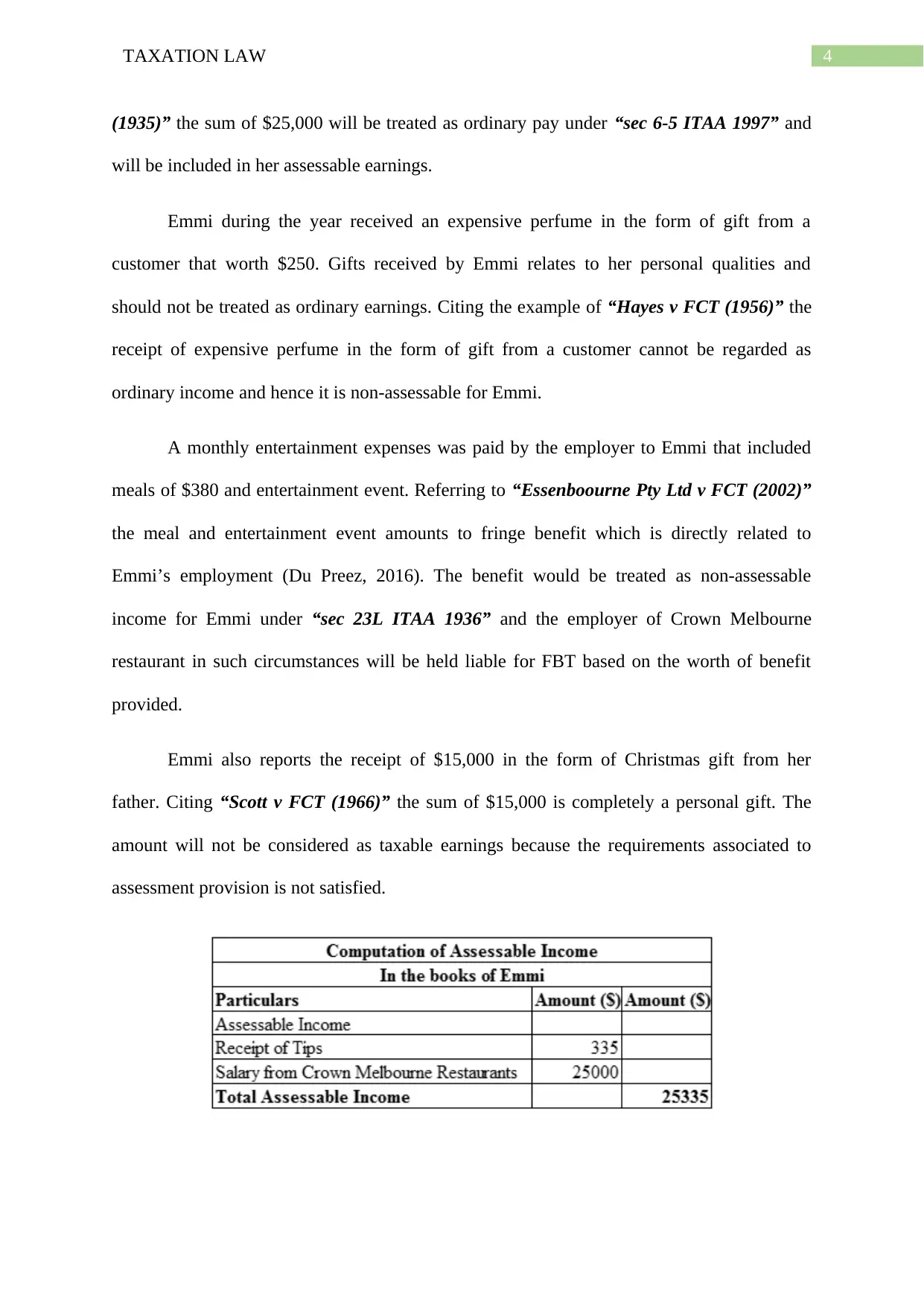

Emmi reports a receipt of tips from customer amounting to $335 from her part-time

work in restaurant. The receipt holds “nexus” from Emmi’s personal service and amounts to

ordinary pay under “sec 6-5 ITAA 1997”. Citing “Calvert v Wainwright (1947)” the receipt

of tips by the Emmi represents the event of occupation and will be assessable as ordinary

earnings (Taylor et al., 2017).

She further reports the receipt of $25,000 from her employment in Crown Melbourne

restaurants. The receipt is an income personal exertion. Bring up the case of “Scott v CT

According to the reconciliation rule given in “sec 6-25 (2)”, if an amount represents

both the aspects of statutory earnings and ordinary earnings then in such a situation the rules

concerning to the statutory earnings prevails excepting when there are any contrary intentions

is given. Alternatively, if the employer provides any fringe benefit to the worker, then the

benefit would be treated as non-assessable pay for the employee under “sec 23L ITAA 1936”

and the employer in such circumstances will be held liable for FBT based on the value of

benefit given (Woellner et al., 2016). As held in “Essenboourne Pty Ltd v FCT (2002)” held

that a fringe benefit will only happen when the benefit is directly related to a particular

employee.

There are also certain types of receipts apart from the ordinary income or capital

which usually arise. Gifts and lottery winnings are not considered taxable earnings since the

requirements associated to assessment provision is not met. Purely personal gifts are not

treated as chargeable pay (Blakelock & King, 2017). As noted in “Scott v FCT (1966)”

receipt of 10,000 pounds gift from a client’s wife out of husband estate is not regarded as

income. The gift was simply unsolicited.

Application:

Emmi reports a receipt of tips from customer amounting to $335 from her part-time

work in restaurant. The receipt holds “nexus” from Emmi’s personal service and amounts to

ordinary pay under “sec 6-5 ITAA 1997”. Citing “Calvert v Wainwright (1947)” the receipt

of tips by the Emmi represents the event of occupation and will be assessable as ordinary

earnings (Taylor et al., 2017).

She further reports the receipt of $25,000 from her employment in Crown Melbourne

restaurants. The receipt is an income personal exertion. Bring up the case of “Scott v CT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(1935)” the sum of $25,000 will be treated as ordinary pay under “sec 6-5 ITAA 1997” and

will be included in her assessable earnings.

Emmi during the year received an expensive perfume in the form of gift from a

customer that worth $250. Gifts received by Emmi relates to her personal qualities and

should not be treated as ordinary earnings. Citing the example of “Hayes v FCT (1956)” the

receipt of expensive perfume in the form of gift from a customer cannot be regarded as

ordinary income and hence it is non-assessable for Emmi.

A monthly entertainment expenses was paid by the employer to Emmi that included

meals of $380 and entertainment event. Referring to “Essenboourne Pty Ltd v FCT (2002)”

the meal and entertainment event amounts to fringe benefit which is directly related to

Emmi’s employment (Du Preez, 2016). The benefit would be treated as non-assessable

income for Emmi under “sec 23L ITAA 1936” and the employer of Crown Melbourne

restaurant in such circumstances will be held liable for FBT based on the worth of benefit

provided.

Emmi also reports the receipt of $15,000 in the form of Christmas gift from her

father. Citing “Scott v FCT (1966)” the sum of $15,000 is completely a personal gift. The

amount will not be considered as taxable earnings because the requirements associated to

assessment provision is not satisfied.

(1935)” the sum of $25,000 will be treated as ordinary pay under “sec 6-5 ITAA 1997” and

will be included in her assessable earnings.

Emmi during the year received an expensive perfume in the form of gift from a

customer that worth $250. Gifts received by Emmi relates to her personal qualities and

should not be treated as ordinary earnings. Citing the example of “Hayes v FCT (1956)” the

receipt of expensive perfume in the form of gift from a customer cannot be regarded as

ordinary income and hence it is non-assessable for Emmi.

A monthly entertainment expenses was paid by the employer to Emmi that included

meals of $380 and entertainment event. Referring to “Essenboourne Pty Ltd v FCT (2002)”

the meal and entertainment event amounts to fringe benefit which is directly related to

Emmi’s employment (Du Preez, 2016). The benefit would be treated as non-assessable

income for Emmi under “sec 23L ITAA 1936” and the employer of Crown Melbourne

restaurant in such circumstances will be held liable for FBT based on the worth of benefit

provided.

Emmi also reports the receipt of $15,000 in the form of Christmas gift from her

father. Citing “Scott v FCT (1966)” the sum of $15,000 is completely a personal gift. The

amount will not be considered as taxable earnings because the requirements associated to

assessment provision is not satisfied.

5TAXATION LAW

Conclusion:

Conclusively, it should be noted that that tips and employment pay that that is

received by Emmi will be included in her taxable income in agreement with the ordinary

conception of “sec 6-5 ITAA 1997”. This is because the receipts hold adequate relation with

the income generating activities of Emmi. While the expensive perfume received by Emmi

from a customer during Christmas time is a mere gift and non-convertible into money. While

the entertainment event and meals provided to Emmi is a non-taxable fringe benefit and the

Christmas gift of $15,000 received by Emmi is purely a personal gift and hence non-taxable.

Conclusion:

Conclusively, it should be noted that that tips and employment pay that that is

received by Emmi will be included in her taxable income in agreement with the ordinary

conception of “sec 6-5 ITAA 1997”. This is because the receipts hold adequate relation with

the income generating activities of Emmi. While the expensive perfume received by Emmi

from a customer during Christmas time is a mere gift and non-convertible into money. While

the entertainment event and meals provided to Emmi is a non-taxable fringe benefit and the

Christmas gift of $15,000 received by Emmi is purely a personal gift and hence non-taxable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Answer A:

CGT is commonly relevant on the assets that is bought or dealings that takes place on

or following the 20 sept 1985. Consequently, the terms “pre-CGT” and “post-CGT” which is

very commonly used to state assets purchased or events that takes place before or succeeding

the aforementioned date (McCluskey & Franzsen, (2017). The legislation of capital gains tax

is applied on the assets that is purchased on or following the 20 sept 1985 date. While any

asset that is purchased before this date is exempted from CGT regime.

Liu an Australian resident is returning back to China and sells all her assets. During

the year Liu sold the house for $630,000 which she purchased in 1981 by paying an

acquisition cost of $55,000. The house here will be classified as “Pre-CGT asset” because it

was purchased by Liu in 1981 which is before the CGT introduction date of 20th September

1985. The capital gains that is made by Liu from sale of her main residence will be simply

exempted from tax.

Answer B:

CGT assets under “section 108-5 ITAA 1997” denotes assets which are subjected to

CGT. It includes any sort or belongings or lawful or equitable rights which cannot be

classified as property. A CGT event is usually applicable on the assets which is purchased

following the 19-9-1985. Under “sec 104-10 ITAA 1997” a “CGT event A1” involves the

disposal of CGT asset (O’Connell, 2017). As given under “sec 108-20 (2) ITAA 1997” a

personal use asset involves the non-collectable assets or those assets which a taxpayer keeps

for their private usage and enjoyment. The examples of this assets includes, boats, motor cars,

furniture, household items and electrical goods. As per “sec 108-20 (1) ITAA 1997” capital

loss that happens from the sale of PUA’s are simply disregarded.

Answer to question 2:

Answer A:

CGT is commonly relevant on the assets that is bought or dealings that takes place on

or following the 20 sept 1985. Consequently, the terms “pre-CGT” and “post-CGT” which is

very commonly used to state assets purchased or events that takes place before or succeeding

the aforementioned date (McCluskey & Franzsen, (2017). The legislation of capital gains tax

is applied on the assets that is purchased on or following the 20 sept 1985 date. While any

asset that is purchased before this date is exempted from CGT regime.

Liu an Australian resident is returning back to China and sells all her assets. During

the year Liu sold the house for $630,000 which she purchased in 1981 by paying an

acquisition cost of $55,000. The house here will be classified as “Pre-CGT asset” because it

was purchased by Liu in 1981 which is before the CGT introduction date of 20th September

1985. The capital gains that is made by Liu from sale of her main residence will be simply

exempted from tax.

Answer B:

CGT assets under “section 108-5 ITAA 1997” denotes assets which are subjected to

CGT. It includes any sort or belongings or lawful or equitable rights which cannot be

classified as property. A CGT event is usually applicable on the assets which is purchased

following the 19-9-1985. Under “sec 104-10 ITAA 1997” a “CGT event A1” involves the

disposal of CGT asset (O’Connell, 2017). As given under “sec 108-20 (2) ITAA 1997” a

personal use asset involves the non-collectable assets or those assets which a taxpayer keeps

for their private usage and enjoyment. The examples of this assets includes, boats, motor cars,

furniture, household items and electrical goods. As per “sec 108-20 (1) ITAA 1997” capital

loss that happens from the sale of PUA’s are simply disregarded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Liu reported the sale of car during the year for $8,000. The car was purchased by Liu

in 2011 for an acquisition cost of $37,000. The car owned by Liu must be characterized as

personal use asset in “sec 108-20 (2) ITAA 1997”. The sale of car has given rise to “CGT

event A1” under “sec 104-10 ITAA 1997” (Jones, 2016). When the car was sold for $8,000 a

capital loss was suffered. As a result, under “sec 108-20 (1) ITAA 1997” capital loss

happening from the sale of car are simply disregarded.

Answer to C:

As per the “Taxation Ruling of TR 1999/16”, in respect of Goodwill a “CGT event

C1” happens when the business is enduringly ended (McCluskey & Franzsen, 2017). When

the business is permanently ceased from operation, whether out of voluntary or involuntary

act, the ruling defines that a loss or destruction of business goodwill takes place.

Concessions are awarded to small business under the “division 152”. The basic

conditions to get the access of concessions is;

a. An entity will be treated as small business when their aggregate turnover in the

present or previous year is less than $2 million with net value of the assets is not

greater than $6 million (Freebairn, 2016).

b. The CGT asset is ought to be the active asset.

On meeting the above criteria, the small business is provided with four types of

concession. These are

a. “15-year Exemption” when the asset is owned for at least 15 years and the age of tax

payer is 55 years or more (Bentley, 2019).

b. “50% reduction” in capital gain following the application of general 50% discount.

c. “Retirement concession” lets a taxpayer to disregard the capital gain derived from

CGT asset of small business up to a limit of $500,000.

Liu reported the sale of car during the year for $8,000. The car was purchased by Liu

in 2011 for an acquisition cost of $37,000. The car owned by Liu must be characterized as

personal use asset in “sec 108-20 (2) ITAA 1997”. The sale of car has given rise to “CGT

event A1” under “sec 104-10 ITAA 1997” (Jones, 2016). When the car was sold for $8,000 a

capital loss was suffered. As a result, under “sec 108-20 (1) ITAA 1997” capital loss

happening from the sale of car are simply disregarded.

Answer to C:

As per the “Taxation Ruling of TR 1999/16”, in respect of Goodwill a “CGT event

C1” happens when the business is enduringly ended (McCluskey & Franzsen, 2017). When

the business is permanently ceased from operation, whether out of voluntary or involuntary

act, the ruling defines that a loss or destruction of business goodwill takes place.

Concessions are awarded to small business under the “division 152”. The basic

conditions to get the access of concessions is;

a. An entity will be treated as small business when their aggregate turnover in the

present or previous year is less than $2 million with net value of the assets is not

greater than $6 million (Freebairn, 2016).

b. The CGT asset is ought to be the active asset.

On meeting the above criteria, the small business is provided with four types of

concession. These are

a. “15-year Exemption” when the asset is owned for at least 15 years and the age of tax

payer is 55 years or more (Bentley, 2019).

b. “50% reduction” in capital gain following the application of general 50% discount.

c. “Retirement concession” lets a taxpayer to disregard the capital gain derived from

CGT asset of small business up to a limit of $500,000.

8TAXATION LAW

d. “Roll-over relief” allows the deferral of capital gains when a taxpayer purchases a

replacement asset.

As obvious, Liu owned a small business enterprise which she sells for $125,000. She

fetched $53,000 for all her photography equipment and $50,000 for goodwill. With respect to

“Division 152” a small business concession can be accessed by Liu because the value of her

net asset is not more than $6 million (Mishra & Anwar 2017). As Liu is retiring from her

business, she can claim retirement concession where the capital proceeds from the sale of her

business can be used to fund her retirement. While for her business goodwill, Liu can obtain a

15-year exemption from the CGT asset because she meets the criteria of 55 years older or

more.

Answer to D:

The special rules say that capital gains from personal use asset is to ignored if the cost

base of asset is lower than $10,000 under “sec 118-10 ITAA 1997”. Liu during the year

reports the sale of furniture for a sum of $2,000. The furniture was actually bought by Liu for

an acquisition cost of $4,800. The furniture must be categorized as personal use asset under

“sec 108-20 (2) ITAA 1997” (Miller & Oats, 2016). As evident the sale of furniture has

given rise to “CGT event A1” under “sec 104-10 ITAA 1997”. The sale of furniture has

resulted in capital gains and under “sec 118-10 ITAA 1997” the capital gains from furniture

should be ignored by Liu because it cost is less than $10,000.

Answer to E:

As explained within the “sec 108-10 (2) ITAA 1997” a collectable involves items that

is held by an individual for their private usage (Barkoczy, 2016). The examples of the

collectables consist of antiques, works of art, jewellery, paintings, sculptures, stamps or coins

etc. The taxpayer should denote that under “sec 118-10 (1) and (2)” capital gains from

d. “Roll-over relief” allows the deferral of capital gains when a taxpayer purchases a

replacement asset.

As obvious, Liu owned a small business enterprise which she sells for $125,000. She

fetched $53,000 for all her photography equipment and $50,000 for goodwill. With respect to

“Division 152” a small business concession can be accessed by Liu because the value of her

net asset is not more than $6 million (Mishra & Anwar 2017). As Liu is retiring from her

business, she can claim retirement concession where the capital proceeds from the sale of her

business can be used to fund her retirement. While for her business goodwill, Liu can obtain a

15-year exemption from the CGT asset because she meets the criteria of 55 years older or

more.

Answer to D:

The special rules say that capital gains from personal use asset is to ignored if the cost

base of asset is lower than $10,000 under “sec 118-10 ITAA 1997”. Liu during the year

reports the sale of furniture for a sum of $2,000. The furniture was actually bought by Liu for

an acquisition cost of $4,800. The furniture must be categorized as personal use asset under

“sec 108-20 (2) ITAA 1997” (Miller & Oats, 2016). As evident the sale of furniture has

given rise to “CGT event A1” under “sec 104-10 ITAA 1997”. The sale of furniture has

resulted in capital gains and under “sec 118-10 ITAA 1997” the capital gains from furniture

should be ignored by Liu because it cost is less than $10,000.

Answer to E:

As explained within the “sec 108-10 (2) ITAA 1997” a collectable involves items that

is held by an individual for their private usage (Barkoczy, 2016). The examples of the

collectables consist of antiques, works of art, jewellery, paintings, sculptures, stamps or coins

etc. The taxpayer should denote that under “sec 118-10 (1) and (2)” capital gains from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

collectables needs to be ignored when the assets is purchased for lower than $500 (Gashenko

et al., 2019). While the capital gains that is earned from the sale of collectables is included

into the assessable proceeds of the taxpayer under “section 102-5 ITAA 1997”.

As noticed Liu sold a painting for $28,000. She purchased the paintings from a second

hand shop and none of the painting were purchased for $500. The paintings will be classified

has collectable under “sec 108-10 (2) ITAA 1997” since Liu bought the painting for private

use purpose (Morgan & Castelyn, 2018). The sale of painting has resulted capital gains

however the cost base of each painting is not more than $500 therefore, the capital gains

made from selling the second hand painting should be ignored by Liu.

Apart from this Liu also sold one painting that she had directly purchased from an

artist for $1,000. The painting was sold for $8,000 and Liu derived capital gains from it. As

the painting’s cost base is greater than $500 the capital gains made from it will be contained

within in Liu’s assessable income under “section 102-5 ITAA 1997”.

collectables needs to be ignored when the assets is purchased for lower than $500 (Gashenko

et al., 2019). While the capital gains that is earned from the sale of collectables is included

into the assessable proceeds of the taxpayer under “section 102-5 ITAA 1997”.

As noticed Liu sold a painting for $28,000. She purchased the paintings from a second

hand shop and none of the painting were purchased for $500. The paintings will be classified

has collectable under “sec 108-10 (2) ITAA 1997” since Liu bought the painting for private

use purpose (Morgan & Castelyn, 2018). The sale of painting has resulted capital gains

however the cost base of each painting is not more than $500 therefore, the capital gains

made from selling the second hand painting should be ignored by Liu.

Apart from this Liu also sold one painting that she had directly purchased from an

artist for $1,000. The painting was sold for $8,000 and Liu derived capital gains from it. As

the painting’s cost base is greater than $500 the capital gains made from it will be contained

within in Liu’s assessable income under “section 102-5 ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S., (2016). Foundations of taxation law 2016. OUP Catalogue.

Bentley, D., (2019). Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Blakelock, S. & King, P., (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Du Preez, H., (2016). A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Freebairn, J., (2016). Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Gashenko, I.V., Zima, Y.S. & Davidyan, A.V., (2019). Principles and Methods of Taxation.

In Optimization of the Taxation System: Preconditions, Tendencies and

Perspectives (pp. 33-39). Springer, Cham.

Jones, D., (2016). Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

McCluskey, W.J. & Franzsen, R.C., (2017). Land value taxation: An applied analysis.

Routledge.

Miller, A. & Oats, L., (2016). Principles of international taxation. Bloomsbury Publishing.

Mishra, A.V. & Anwar, S., (2017). Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

Morgan, A. & Castelyn, D., (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

O’Connell, A., (2017). Australia. In Capital Gains Taxation. Edward Elgar Publishing.

References:

Barkoczy, S., (2016). Foundations of taxation law 2016. OUP Catalogue.

Bentley, D., (2019). Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Blakelock, S. & King, P., (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Du Preez, H., (2016). A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Freebairn, J., (2016). Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Gashenko, I.V., Zima, Y.S. & Davidyan, A.V., (2019). Principles and Methods of Taxation.

In Optimization of the Taxation System: Preconditions, Tendencies and

Perspectives (pp. 33-39). Springer, Cham.

Jones, D., (2016). Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

McCluskey, W.J. & Franzsen, R.C., (2017). Land value taxation: An applied analysis.

Routledge.

Miller, A. & Oats, L., (2016). Principles of international taxation. Bloomsbury Publishing.

Mishra, A.V. & Anwar, S., (2017). Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

Morgan, A. & Castelyn, D., (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

O’Connell, A., (2017). Australia. In Capital Gains Taxation. Edward Elgar Publishing.

11TAXATION LAW

Taylor, J., Walpole, M., Burton, M., Ciro, T. & Murray, I., (2017). Understanding Taxation

Law 2018. LexisNexis Butterworths.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. & Pinto, D., (2016). Australian Taxation

Law 2016. OUP Catalogue.

Taylor, J., Walpole, M., Burton, M., Ciro, T. & Murray, I., (2017). Understanding Taxation

Law 2018. LexisNexis Butterworths.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. & Pinto, D., (2016). Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.