HA3042 Taxation Law Assignment: FBT and CGT Issues and Solutions

VerifiedAdded on 2022/11/24

|10

|2071

|436

Homework Assignment

AI Summary

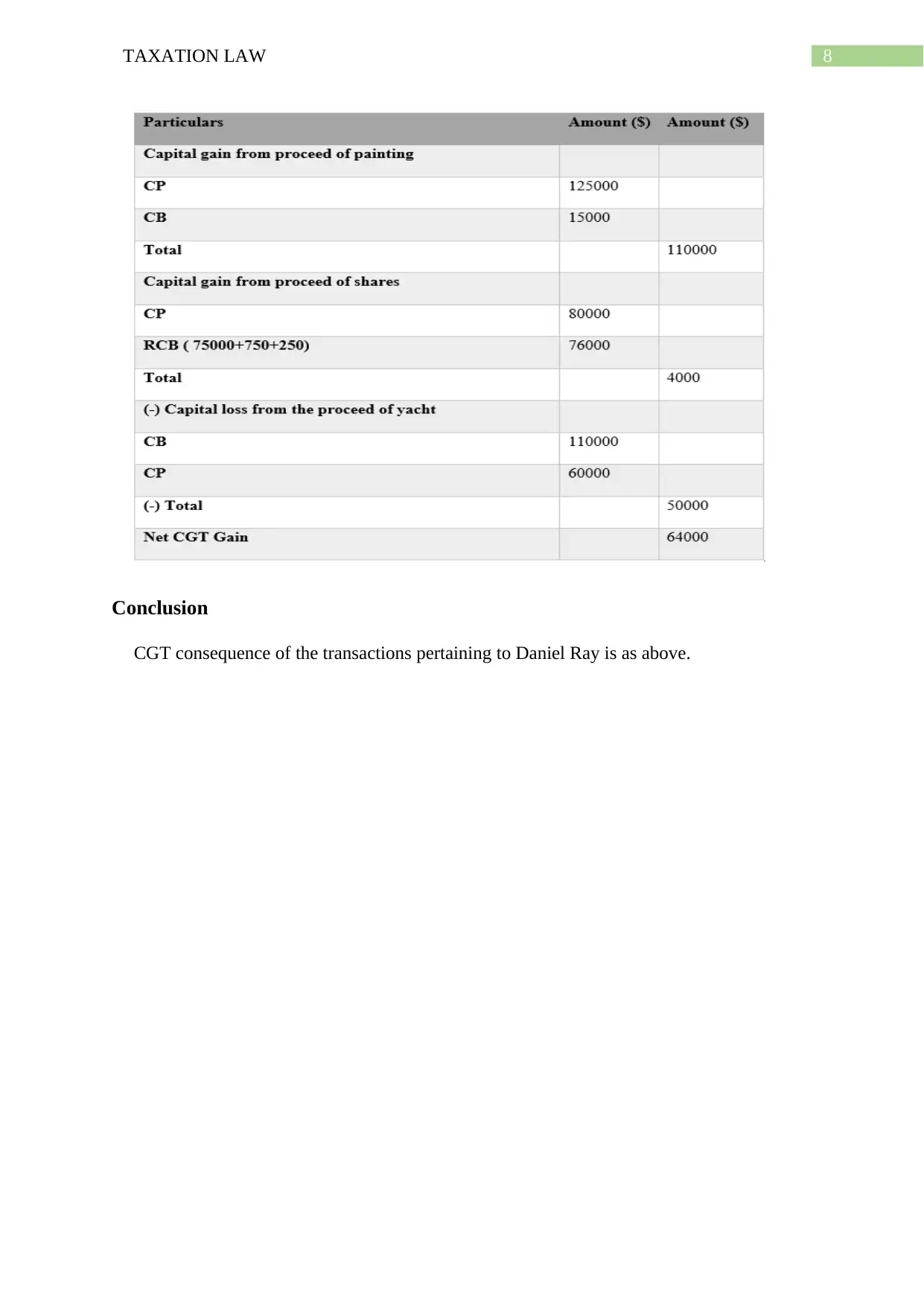

This assignment solution addresses two key areas of Australian taxation law: Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). The first part focuses on FBT, specifically the computation of FBT liability for Spiceco Pty Ltd, analyzing different FBT computation methods (statutory and operating cost methods) and recommending the most appropriate method based on minimizing tax liability. The second part delves into CGT, calculating the net capital gain or loss for Daniel Ray, considering various CGT events, including the sale of a main residence, collectibles, shares, and the implications of loans and interest expenses. The solution applies relevant sections of the FBTAA 1986 and ITAA 1997, demonstrating an understanding of tax law concepts and principles, and providing detailed calculations and analysis to support the conclusions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.