Taxation Law Assignment: Fringe Benefits, Income Tax, and Barter

VerifiedAdded on 2020/05/16

|9

|1574

|58

Homework Assignment

AI Summary

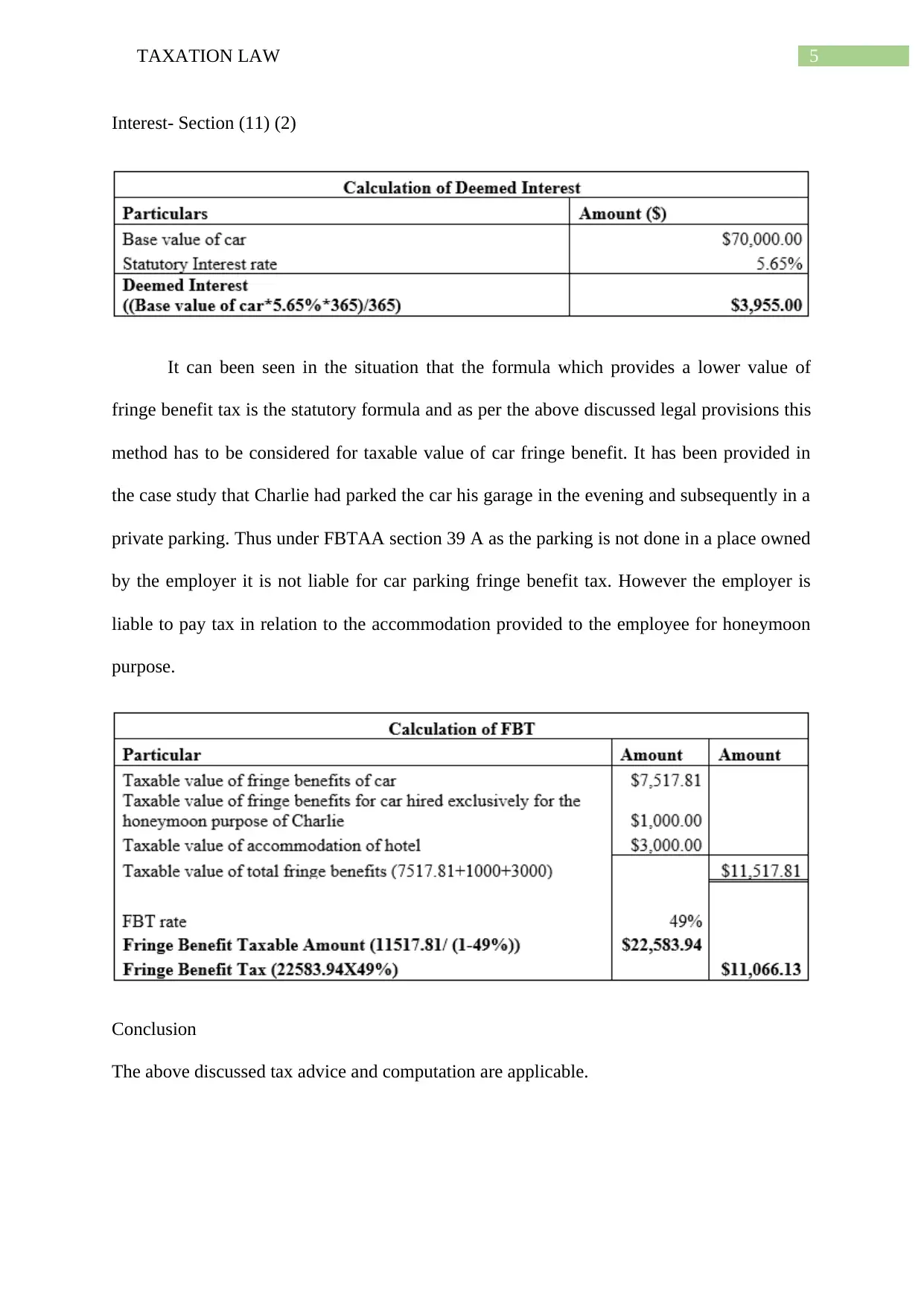

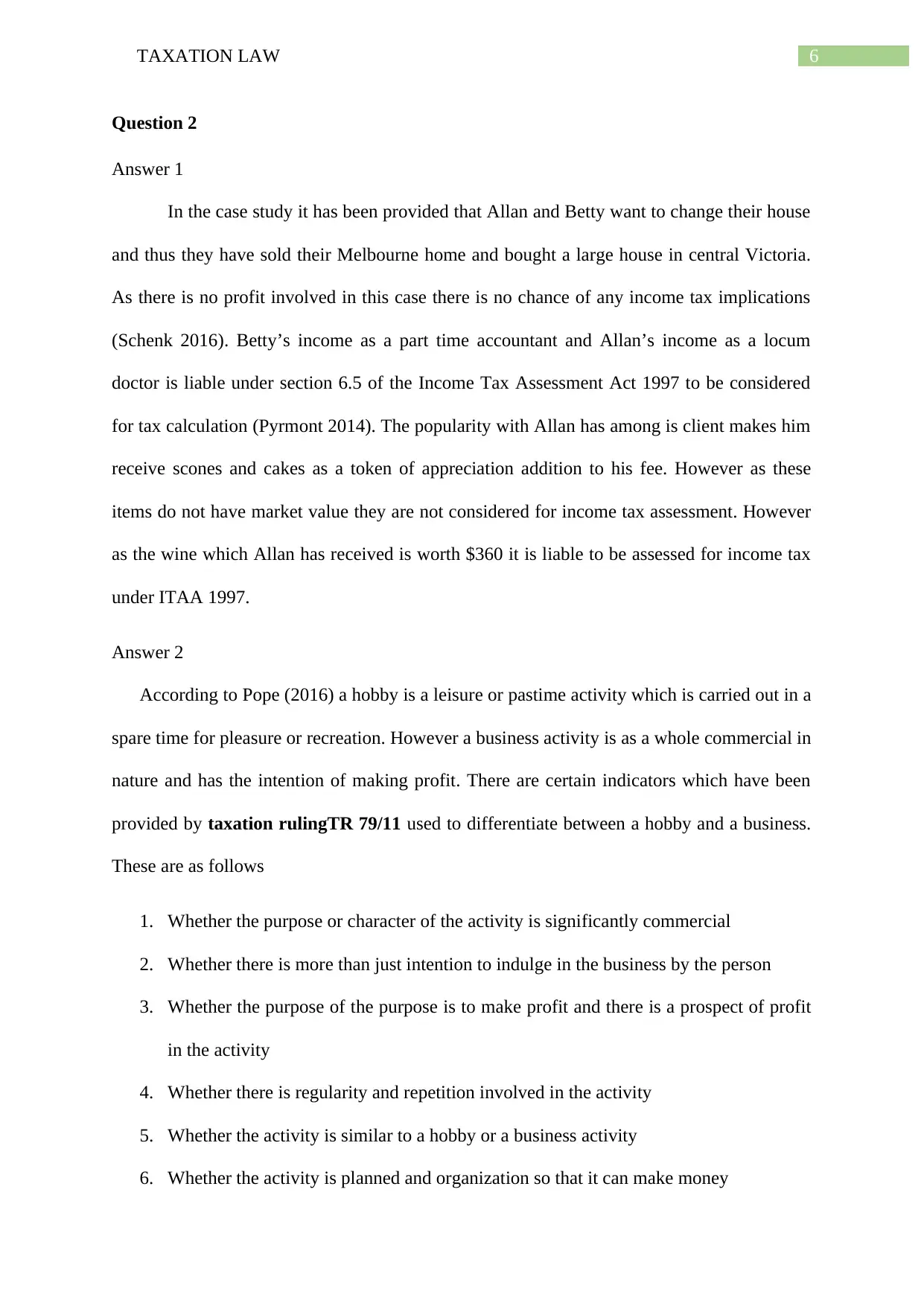

This taxation law assignment provides a comprehensive analysis of fringe benefits, income tax, and barter systems within the context of Australian taxation law. It addresses the tax implications of fringe benefits, including car fringe benefits, detailing the statutory formula and operating cost methods for calculation. The assignment further explores income tax considerations, such as the taxability of income from part-time work and gifts, as well as the distinction between a hobby and a business for tax purposes. It also examines the tax implications of a barter system, aligning with the guidelines set by the Australian Taxation Office. The assignment references relevant legislation, including the Fringe Benefits Tax Assessment Act 1986 and the Income Tax Assessment Act 1997, and includes case law to support its analysis, offering practical insights into various taxation scenarios.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.