TAXATION LAW 11: Comprehensive Analysis of CGT and Deductions

VerifiedAdded on 2022/08/24

|13

|2709

|25

Homework Assignment

AI Summary

This taxation law assignment analyzes several scenarios related to capital gains tax (CGT) and deductions. The first part addresses CGT implications from the sale of land, shares, and collectables, along with personal use assets. It examines acquisition costs, incidental costs, property ownership costs, capital improvements, and title costs, referencing relevant sections of the ITAA 1997. The second part of the assignment focuses on the deductibility of various expenses, including travel, relocation, uniforms, childcare, phone calls, food, fines, and travel to/from work, referencing key legal precedents such as Maddalena v FCT, Fullerton v FCT, and FCT v Mansfield. The assignment provides a detailed analysis of each scenario, applying relevant tax laws and court decisions to determine the tax implications.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer A: Sale of block of land:

The cost of the asset normally includes five elements. The first element of cost base

under “sec 110-25 (2)” includes the overall money paid or property given to obtain an asset.

While the second element of cost base represents the incidental costs under “sec 110-35”.

These cost includes stamp duty, legal fees etc. paid to acquire an asset. “Sec 110-36”

involves the cost of ownership as the third element of cost base (Nightingale 2014). The

ownership costs involves the interest, ownership cost of maintenance, insurance and land

taxes. The fourth element of the cost base involves the capital improvement and preservation

cost under “sec 110-38 ITAA 1997”. The examples of this type of cost includes

improvement, moving and installation expenditure.

The fifth element of the cost base includes capital expenditure that is occurred in

maintaining the title rights to assets. The examples of this cost under the “section 110-45

ITAA 1997” involves cost occurred in opposing the compulsory acquisition of land by

government.

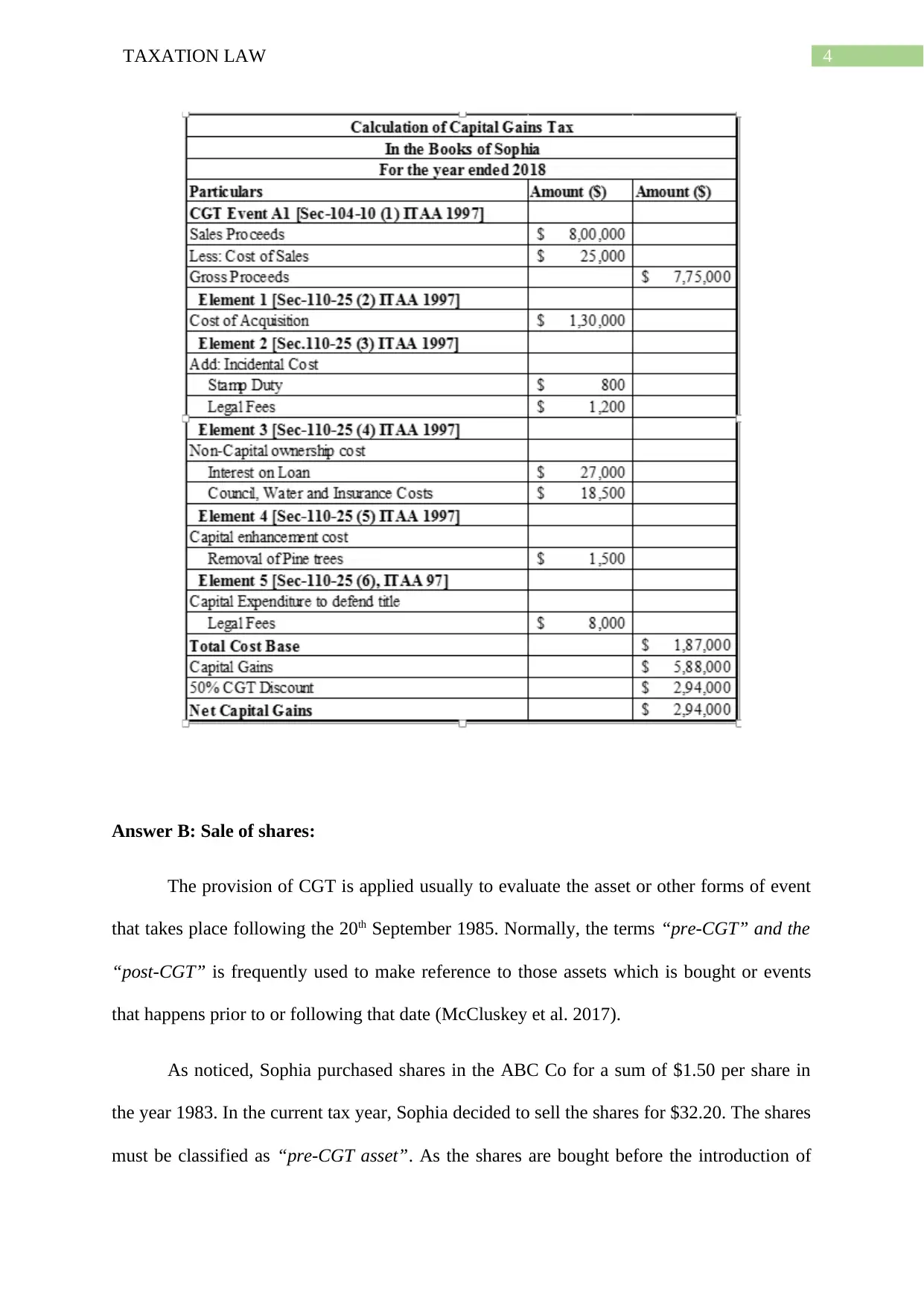

Sophia in the current case has reported the sale of block of land for $800,000. The

land was actually purchased by Sophia for $130,000 in 1991. In order to ascertain the CGT of

the land it is important to understand the acquisition cost of asset (Mankiw, Weinzierl and

Yagan 2019). Under the “sec 110-25 (2)” the acquisition cost of asset would include the

purchase price paid by Sophia to acquire the asset. Sophia further reports the payment of

stamp duty of $800 and legal fees of $1200. With regard to “section 110-35” these costs will

be classified as incidental costs and hence Sophia is required to include the same in the cost

base of her asset.

Answer to question 1:

Answer A: Sale of block of land:

The cost of the asset normally includes five elements. The first element of cost base

under “sec 110-25 (2)” includes the overall money paid or property given to obtain an asset.

While the second element of cost base represents the incidental costs under “sec 110-35”.

These cost includes stamp duty, legal fees etc. paid to acquire an asset. “Sec 110-36”

involves the cost of ownership as the third element of cost base (Nightingale 2014). The

ownership costs involves the interest, ownership cost of maintenance, insurance and land

taxes. The fourth element of the cost base involves the capital improvement and preservation

cost under “sec 110-38 ITAA 1997”. The examples of this type of cost includes

improvement, moving and installation expenditure.

The fifth element of the cost base includes capital expenditure that is occurred in

maintaining the title rights to assets. The examples of this cost under the “section 110-45

ITAA 1997” involves cost occurred in opposing the compulsory acquisition of land by

government.

Sophia in the current case has reported the sale of block of land for $800,000. The

land was actually purchased by Sophia for $130,000 in 1991. In order to ascertain the CGT of

the land it is important to understand the acquisition cost of asset (Mankiw, Weinzierl and

Yagan 2019). Under the “sec 110-25 (2)” the acquisition cost of asset would include the

purchase price paid by Sophia to acquire the asset. Sophia further reports the payment of

stamp duty of $800 and legal fees of $1200. With regard to “section 110-35” these costs will

be classified as incidental costs and hence Sophia is required to include the same in the cost

base of her asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

In order to purchase the investment property Sophia had secured a bank loan and paid

an interest amount of $27,000 against the loan. When the property was under the ownership

of Sophia she paid a council rates, water rates and insurance which totalled $18,500.

Referring to “section 110-36” these expenses must be classified as property ownership cost

and Sophia is required to add into the cost base in order to determine the net capital gains

(Burman et al. 2016). Later in the year a dispute happened with neighbour regarding the use

of property and Sophia incurred a legal fees which amounted to $8,000. Under “sec 110-25

(6)”, these costs will be regarded under the fifth element cost base for establishing the title

cost of property. Finally, before the property was put on sale, Sophia reported the expense on

removing the pine trees that hazardously present on the property (Higgins 2014). Under the

“sec 110-25 (5)” it is a capital expenditure which the taxpayer has occurred in increasing the

asset value and as a result, Sophia should include it in her cost base.

In order to purchase the investment property Sophia had secured a bank loan and paid

an interest amount of $27,000 against the loan. When the property was under the ownership

of Sophia she paid a council rates, water rates and insurance which totalled $18,500.

Referring to “section 110-36” these expenses must be classified as property ownership cost

and Sophia is required to add into the cost base in order to determine the net capital gains

(Burman et al. 2016). Later in the year a dispute happened with neighbour regarding the use

of property and Sophia incurred a legal fees which amounted to $8,000. Under “sec 110-25

(6)”, these costs will be regarded under the fifth element cost base for establishing the title

cost of property. Finally, before the property was put on sale, Sophia reported the expense on

removing the pine trees that hazardously present on the property (Higgins 2014). Under the

“sec 110-25 (5)” it is a capital expenditure which the taxpayer has occurred in increasing the

asset value and as a result, Sophia should include it in her cost base.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer B: Sale of shares:

The provision of CGT is applied usually to evaluate the asset or other forms of event

that takes place following the 20th September 1985. Normally, the terms “pre-CGT” and the

“post-CGT” is frequently used to make reference to those assets which is bought or events

that happens prior to or following that date (McCluskey et al. 2017).

As noticed, Sophia purchased shares in the ABC Co for a sum of $1.50 per share in

the year 1983. In the current tax year, Sophia decided to sell the shares for $32.20. The shares

must be classified as “pre-CGT asset”. As the shares are bought before the introduction of

Answer B: Sale of shares:

The provision of CGT is applied usually to evaluate the asset or other forms of event

that takes place following the 20th September 1985. Normally, the terms “pre-CGT” and the

“post-CGT” is frequently used to make reference to those assets which is bought or events

that happens prior to or following that date (McCluskey et al. 2017).

As noticed, Sophia purchased shares in the ABC Co for a sum of $1.50 per share in

the year 1983. In the current tax year, Sophia decided to sell the shares for $32.20. The shares

must be classified as “pre-CGT asset”. As the shares are bought before the introduction of

5TAXATION LAW

CGT regime on 20th September 1985, the capital gains derived by Sophia will not be included

in her taxable earnings.

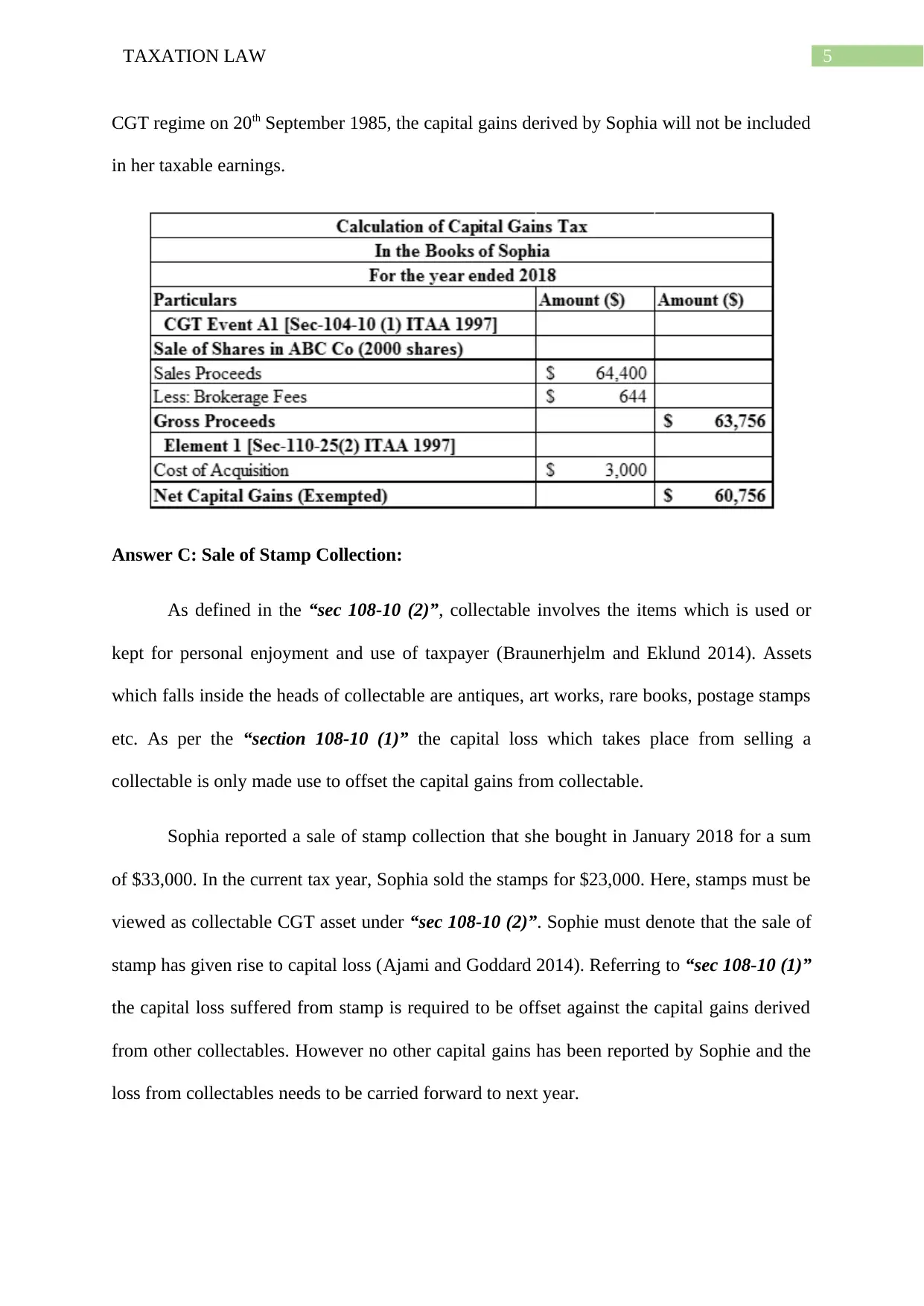

Answer C: Sale of Stamp Collection:

As defined in the “sec 108-10 (2)”, collectable involves the items which is used or

kept for personal enjoyment and use of taxpayer (Braunerhjelm and Eklund 2014). Assets

which falls inside the heads of collectable are antiques, art works, rare books, postage stamps

etc. As per the “section 108-10 (1)” the capital loss which takes place from selling a

collectable is only made use to offset the capital gains from collectable.

Sophia reported a sale of stamp collection that she bought in January 2018 for a sum

of $33,000. In the current tax year, Sophia sold the stamps for $23,000. Here, stamps must be

viewed as collectable CGT asset under “sec 108-10 (2)”. Sophie must denote that the sale of

stamp has given rise to capital loss (Ajami and Goddard 2014). Referring to “sec 108-10 (1)”

the capital loss suffered from stamp is required to be offset against the capital gains derived

from other collectables. However no other capital gains has been reported by Sophie and the

loss from collectables needs to be carried forward to next year.

CGT regime on 20th September 1985, the capital gains derived by Sophia will not be included

in her taxable earnings.

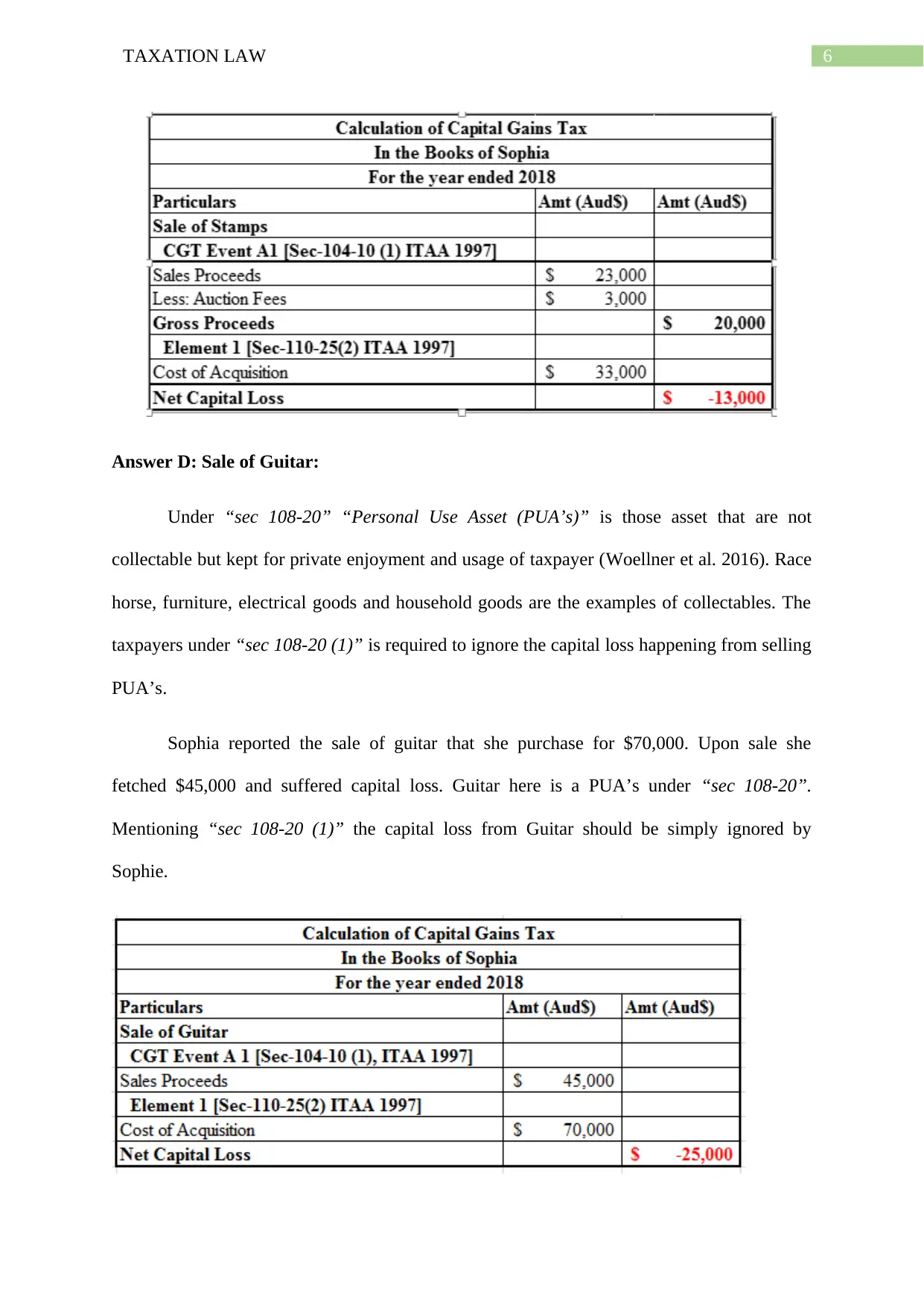

Answer C: Sale of Stamp Collection:

As defined in the “sec 108-10 (2)”, collectable involves the items which is used or

kept for personal enjoyment and use of taxpayer (Braunerhjelm and Eklund 2014). Assets

which falls inside the heads of collectable are antiques, art works, rare books, postage stamps

etc. As per the “section 108-10 (1)” the capital loss which takes place from selling a

collectable is only made use to offset the capital gains from collectable.

Sophia reported a sale of stamp collection that she bought in January 2018 for a sum

of $33,000. In the current tax year, Sophia sold the stamps for $23,000. Here, stamps must be

viewed as collectable CGT asset under “sec 108-10 (2)”. Sophie must denote that the sale of

stamp has given rise to capital loss (Ajami and Goddard 2014). Referring to “sec 108-10 (1)”

the capital loss suffered from stamp is required to be offset against the capital gains derived

from other collectables. However no other capital gains has been reported by Sophie and the

loss from collectables needs to be carried forward to next year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

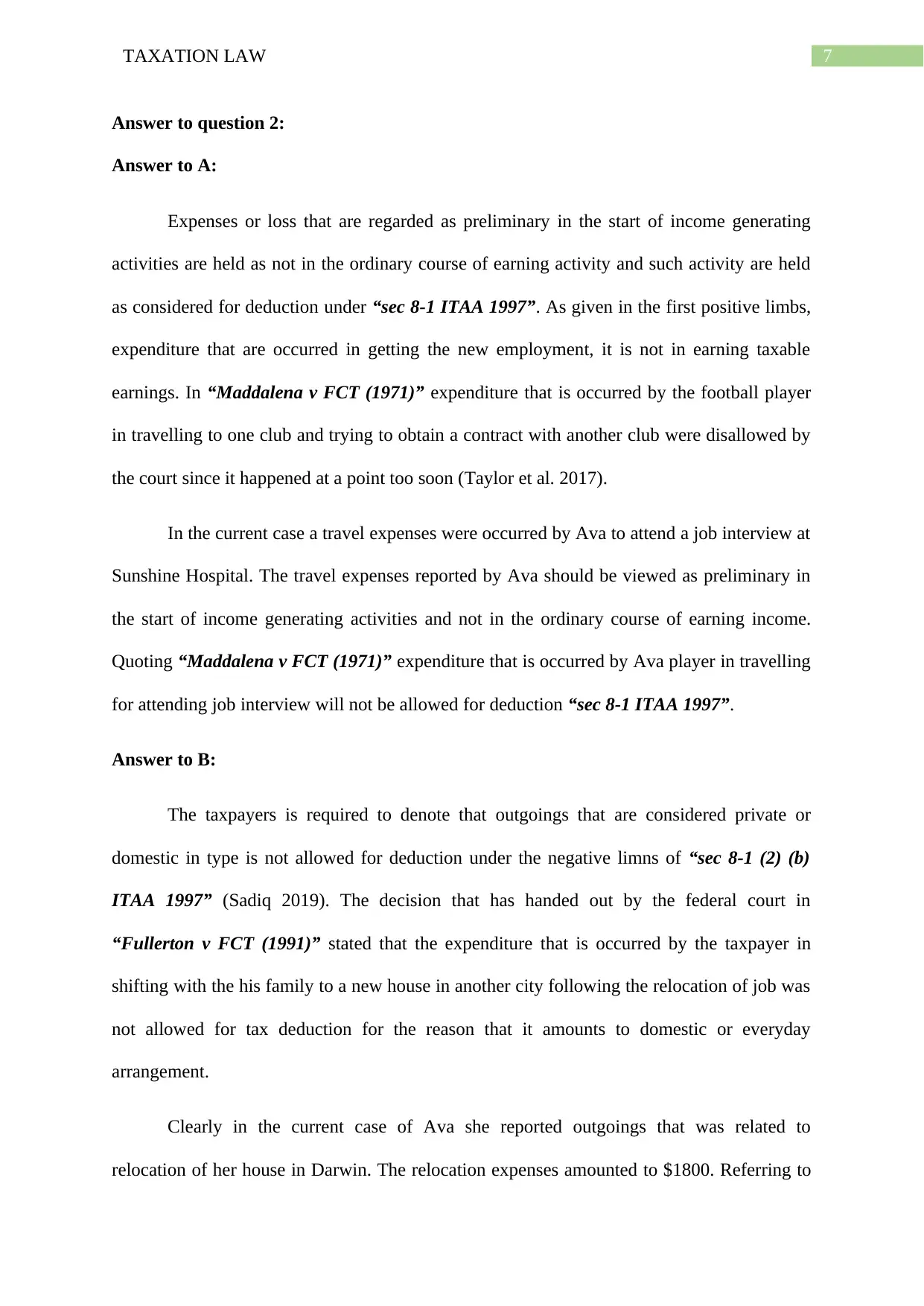

Answer D: Sale of Guitar:

Under “sec 108-20” “Personal Use Asset (PUA’s)” is those asset that are not

collectable but kept for private enjoyment and usage of taxpayer (Woellner et al. 2016). Race

horse, furniture, electrical goods and household goods are the examples of collectables. The

taxpayers under “sec 108-20 (1)” is required to ignore the capital loss happening from selling

PUA’s.

Sophia reported the sale of guitar that she purchase for $70,000. Upon sale she

fetched $45,000 and suffered capital loss. Guitar here is a PUA’s under “sec 108-20”.

Mentioning “sec 108-20 (1)” the capital loss from Guitar should be simply ignored by

Sophie.

Answer D: Sale of Guitar:

Under “sec 108-20” “Personal Use Asset (PUA’s)” is those asset that are not

collectable but kept for private enjoyment and usage of taxpayer (Woellner et al. 2016). Race

horse, furniture, electrical goods and household goods are the examples of collectables. The

taxpayers under “sec 108-20 (1)” is required to ignore the capital loss happening from selling

PUA’s.

Sophia reported the sale of guitar that she purchase for $70,000. Upon sale she

fetched $45,000 and suffered capital loss. Guitar here is a PUA’s under “sec 108-20”.

Mentioning “sec 108-20 (1)” the capital loss from Guitar should be simply ignored by

Sophie.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Answer to A:

Expenses or loss that are regarded as preliminary in the start of income generating

activities are held as not in the ordinary course of earning activity and such activity are held

as considered for deduction under “sec 8-1 ITAA 1997”. As given in the first positive limbs,

expenditure that are occurred in getting the new employment, it is not in earning taxable

earnings. In “Maddalena v FCT (1971)” expenditure that is occurred by the football player

in travelling to one club and trying to obtain a contract with another club were disallowed by

the court since it happened at a point too soon (Taylor et al. 2017).

In the current case a travel expenses were occurred by Ava to attend a job interview at

Sunshine Hospital. The travel expenses reported by Ava should be viewed as preliminary in

the start of income generating activities and not in the ordinary course of earning income.

Quoting “Maddalena v FCT (1971)” expenditure that is occurred by Ava player in travelling

for attending job interview will not be allowed for deduction “sec 8-1 ITAA 1997”.

Answer to B:

The taxpayers is required to denote that outgoings that are considered private or

domestic in type is not allowed for deduction under the negative limns of “sec 8-1 (2) (b)

ITAA 1997” (Sadiq 2019). The decision that has handed out by the federal court in

“Fullerton v FCT (1991)” stated that the expenditure that is occurred by the taxpayer in

shifting with the his family to a new house in another city following the relocation of job was

not allowed for tax deduction for the reason that it amounts to domestic or everyday

arrangement.

Clearly in the current case of Ava she reported outgoings that was related to

relocation of her house in Darwin. The relocation expenses amounted to $1800. Referring to

Answer to question 2:

Answer to A:

Expenses or loss that are regarded as preliminary in the start of income generating

activities are held as not in the ordinary course of earning activity and such activity are held

as considered for deduction under “sec 8-1 ITAA 1997”. As given in the first positive limbs,

expenditure that are occurred in getting the new employment, it is not in earning taxable

earnings. In “Maddalena v FCT (1971)” expenditure that is occurred by the football player

in travelling to one club and trying to obtain a contract with another club were disallowed by

the court since it happened at a point too soon (Taylor et al. 2017).

In the current case a travel expenses were occurred by Ava to attend a job interview at

Sunshine Hospital. The travel expenses reported by Ava should be viewed as preliminary in

the start of income generating activities and not in the ordinary course of earning income.

Quoting “Maddalena v FCT (1971)” expenditure that is occurred by Ava player in travelling

for attending job interview will not be allowed for deduction “sec 8-1 ITAA 1997”.

Answer to B:

The taxpayers is required to denote that outgoings that are considered private or

domestic in type is not allowed for deduction under the negative limns of “sec 8-1 (2) (b)

ITAA 1997” (Sadiq 2019). The decision that has handed out by the federal court in

“Fullerton v FCT (1991)” stated that the expenditure that is occurred by the taxpayer in

shifting with the his family to a new house in another city following the relocation of job was

not allowed for tax deduction for the reason that it amounts to domestic or everyday

arrangement.

Clearly in the current case of Ava she reported outgoings that was related to

relocation of her house in Darwin. The relocation expenses amounted to $1800. Referring to

8TAXATION LAW

“Fullerton v FCT (1991)” the relocation expenditure that is occurred by Ava is private

arrangement. The expenses fails to meet either of the positive limbs under “sec 8-1 (2) (b)

ITAA 1997” and it is not permitted for deduction.

Part C:

Expenses that are occurred by taxpayers towards ordinary objects of attire are not

allowed general tax deduction with in the general provision of “sect 8-1 ITAA 1997”. The

taxpayers are allowed exceptions for compulsory clothing, clothes that are specific to

occupation and protective uniform. The case of “FCT v Mansfield (1995)” denoted that a

taxpayer was permitted deduction relating to the cost of shoes and for expenses on stockings

because it was mandatorily needed to be worn by taxpayer while doing her job of flight

attendant (Endres, Uchtmann and Hoff 2019).

Accordingly Ava reported a payment of $200 for a compulsory doctor’s uniform. The

expenses occurred is towards doctor’s uniform amounts to an occupation specific clothing for

Ava. Denoting the factual situation given in “FCT v Mansfield (1995)” the clothing expenses

that is occurred by Ava for doctor’s uniform will be permitted for tax deduction under “sect

8-1 ITAA 1997”.

Answer to D:

Ava in the relevant tax year has occurred child care expenses towards maintaining her

two year old daughter. The outgoings occurred stood $18,200. As found in “Lodge v FCT

(1972)” the taxpayer claimed from his assessable earnings the expenses that were related to

his childcare (Arnold, Ault and Cooper 2019). The decision of the court stated that the

expenses were not at all relevant and was not incidental in the income generating activities of

the taxpayer. Therefore, the outgoings were not relevant in derivation of assessable income

and non-deductible under “sect 8-1 ITAA 1997”.

“Fullerton v FCT (1991)” the relocation expenditure that is occurred by Ava is private

arrangement. The expenses fails to meet either of the positive limbs under “sec 8-1 (2) (b)

ITAA 1997” and it is not permitted for deduction.

Part C:

Expenses that are occurred by taxpayers towards ordinary objects of attire are not

allowed general tax deduction with in the general provision of “sect 8-1 ITAA 1997”. The

taxpayers are allowed exceptions for compulsory clothing, clothes that are specific to

occupation and protective uniform. The case of “FCT v Mansfield (1995)” denoted that a

taxpayer was permitted deduction relating to the cost of shoes and for expenses on stockings

because it was mandatorily needed to be worn by taxpayer while doing her job of flight

attendant (Endres, Uchtmann and Hoff 2019).

Accordingly Ava reported a payment of $200 for a compulsory doctor’s uniform. The

expenses occurred is towards doctor’s uniform amounts to an occupation specific clothing for

Ava. Denoting the factual situation given in “FCT v Mansfield (1995)” the clothing expenses

that is occurred by Ava for doctor’s uniform will be permitted for tax deduction under “sect

8-1 ITAA 1997”.

Answer to D:

Ava in the relevant tax year has occurred child care expenses towards maintaining her

two year old daughter. The outgoings occurred stood $18,200. As found in “Lodge v FCT

(1972)” the taxpayer claimed from his assessable earnings the expenses that were related to

his childcare (Arnold, Ault and Cooper 2019). The decision of the court stated that the

expenses were not at all relevant and was not incidental in the income generating activities of

the taxpayer. Therefore, the outgoings were not relevant in derivation of assessable income

and non-deductible under “sect 8-1 ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to E:

Expenses that are associated to work related to phone calls and phone rental might be

permitted for deduction if the taxpayer has documented evidence of being on call or if they

call their employer or clients on regular basis while away from the workplace. The federal

court decision made in “Ronpibon Tin No Liability v FCT (1949)” held that expenses

relating to the phone calls for work purpose is allowed for tax deduction given the outgoing

meets any of the positive limbs given in “section 8-1 ITAA 1997” (Ajami and Goddard

2014).

In the relevant tax year Ava incurred expenses on phone calls when she was away

from hospital following her work hours so that she can check on the patients. The phone calls

cost Ava $200. Denoting the decision given in “Ronpibon Tin No Liability v FCT (1949)”

the phone call expenses will be allowed for deduction under the “section 8-1 ITAA 1997”

because it was mainly occurred for work purpose while she was away from her work.

Answer to F:

There are situations where a taxpayer may occur expenses that are associated to

human being or human society. Henceforth, outgoings occurred for food, housing, clothing of

common type is not allowable as deduction within the “section 8-1 ITAA 1997”

(Braunerhjelm and Eklund 2014). The judgement given in “FCT v Cooper (1991)” held that

the outgoings occurred by a rugby player on having extra food was non-deductible under the

positive limbs of “section 8-1 ITAA 1997”.

Ava reported outgoings on consuming food while working in the evening shift.

Referring to “FCT v Cooper (1991)” the food expenses is non-deductible within “sec 8-1

Answer to E:

Expenses that are associated to work related to phone calls and phone rental might be

permitted for deduction if the taxpayer has documented evidence of being on call or if they

call their employer or clients on regular basis while away from the workplace. The federal

court decision made in “Ronpibon Tin No Liability v FCT (1949)” held that expenses

relating to the phone calls for work purpose is allowed for tax deduction given the outgoing

meets any of the positive limbs given in “section 8-1 ITAA 1997” (Ajami and Goddard

2014).

In the relevant tax year Ava incurred expenses on phone calls when she was away

from hospital following her work hours so that she can check on the patients. The phone calls

cost Ava $200. Denoting the decision given in “Ronpibon Tin No Liability v FCT (1949)”

the phone call expenses will be allowed for deduction under the “section 8-1 ITAA 1997”

because it was mainly occurred for work purpose while she was away from her work.

Answer to F:

There are situations where a taxpayer may occur expenses that are associated to

human being or human society. Henceforth, outgoings occurred for food, housing, clothing of

common type is not allowable as deduction within the “section 8-1 ITAA 1997”

(Braunerhjelm and Eklund 2014). The judgement given in “FCT v Cooper (1991)” held that

the outgoings occurred by a rugby player on having extra food was non-deductible under the

positive limbs of “section 8-1 ITAA 1997”.

Ava reported outgoings on consuming food while working in the evening shift.

Referring to “FCT v Cooper (1991)” the food expenses is non-deductible within “sec 8-1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

ITAA 1997” since it fails to meet the criteria given in first limb. The outgoings is associated

to being a part of human society and hence non-deductible under “sec 8-1 ITAA 1997”.

Answer G:

As per the “section 26-5 ITAA 1997” fines that are imposed by Australian

government is non-deductible. During the year Ava reported a speeding fine of $207 when

she was getting late for her work. Citing the “section 26-5 ITAA 1997” fines that was

imposed is non-deductible to Ava.

Answer F:

Outgoings that are occurred for Travel between home and a taxpayer’s usual place of

work in usually not permitted for tax deduction under the “sec 8-1 ITAA 1997”. As “FCT v

Lunney (1958)” taxpayers clamed outgoing associated to work and travel (Mankiw,

Weinzierl and Yagan 2019). Deduction were not permitted to taxpayer because it was not

relevant in generating chargeable earnings. Rather the outgoings were private in type.

In the current situation, Ava occurred $330 as travel outgoings to and from work.

Citing “FCT v Lunney (1958)” the travel outgoings to and from work by Ava is non-

deductible because it is private in type and not associated to derivation of taxable earnings.

As a result no deduction is allowed to Ava under “sec 8-1 ITAA 1997”.

ITAA 1997” since it fails to meet the criteria given in first limb. The outgoings is associated

to being a part of human society and hence non-deductible under “sec 8-1 ITAA 1997”.

Answer G:

As per the “section 26-5 ITAA 1997” fines that are imposed by Australian

government is non-deductible. During the year Ava reported a speeding fine of $207 when

she was getting late for her work. Citing the “section 26-5 ITAA 1997” fines that was

imposed is non-deductible to Ava.

Answer F:

Outgoings that are occurred for Travel between home and a taxpayer’s usual place of

work in usually not permitted for tax deduction under the “sec 8-1 ITAA 1997”. As “FCT v

Lunney (1958)” taxpayers clamed outgoing associated to work and travel (Mankiw,

Weinzierl and Yagan 2019). Deduction were not permitted to taxpayer because it was not

relevant in generating chargeable earnings. Rather the outgoings were private in type.

In the current situation, Ava occurred $330 as travel outgoings to and from work.

Citing “FCT v Lunney (1958)” the travel outgoings to and from work by Ava is non-

deductible because it is private in type and not associated to derivation of taxable earnings.

As a result no deduction is allowed to Ava under “sec 8-1 ITAA 1997”.

11TAXATION LAW

References:

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice. Routledge.

Arnold, B.J., Ault, H.J. and Cooper, G. eds., 2019. Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Endres, A.B., Uchtmann, D. and Hoff, G., 2019. Law and Taxation: A Retrospective of 20

Years. farmdoc daily, 9(170).

Higgins, T., 2014. Income contingent loans: Theory, practice and prospects. Springer.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2019. Optimal taxation in theory and

practice. Journal of Economic Perspectives, 23(4), pp.147-74.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Nightingale, K., 2014. Taxation: Theory and practice. Pearson education.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Taylor, J., Walpole, M., Burton, M., Ciro, T. and Murray, I., 2017. Understanding Taxation

Law 2018. LexisNexis Butterworths.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References:

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice. Routledge.

Arnold, B.J., Ault, H.J. and Cooper, G. eds., 2019. Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Endres, A.B., Uchtmann, D. and Hoff, G., 2019. Law and Taxation: A Retrospective of 20

Years. farmdoc daily, 9(170).

Higgins, T., 2014. Income contingent loans: Theory, practice and prospects. Springer.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2019. Optimal taxation in theory and

practice. Journal of Economic Perspectives, 23(4), pp.147-74.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Nightingale, K., 2014. Taxation: Theory and practice. Pearson education.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Taylor, J., Walpole, M., Burton, M., Ciro, T. and Murray, I., 2017. Understanding Taxation

Law 2018. LexisNexis Butterworths.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.