HI6028 Taxation Theory, Practice & Law Assignment: Taxation Issues

VerifiedAdded on 2022/10/06

|11

|2438

|57

Homework Assignment

AI Summary

This taxation law assignment addresses key concepts of the Australian tax system, specifically focusing on Goods and Services Tax (GST) and Capital Gains Tax (CGT). The assignment analyzes a case study involving a company's purchase of land, legal services, and the application of the reverse charge mechanism for GST. It also examines the tax implications of selling land, shares, stamps, and a grand piano, considering the relevant CGT events, cost base elements, and the treatment of pre-CGT assets and personal use assets. The solution interprets relevant tax legislations and case law, applying taxation principles to real-life scenarios to demonstrate an understanding of the Australian income tax system.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

The study that is considered here is for the claim of input tax credit for the taxable

supplies and taxable imports.

Laws:

The provision of the Goods and Service Tax introduced during the 1st July 2000 to

replace the wholesale tax and the indirect tax. GST is observed as the final consumption

inside the Australia and imports inside the Australia. Noting the description provided inside

the “sec 7-1 GST of the Act”, GST is commonly paid by tax payers on the chargeable

supplies (Ramli et al. 2015). The taxpayer can lower the GST by claiming the input tax

credits on the creditable acquisition and creditable imports. Where the input tax credit is

found to be in excess of the GST payable on the assessable supplies then the taxpayer is

allowed for a refund.

The definition regarding the taxable supply is noted down with in the sec 9-5, that says;

a. There is ought to be a supply

b. The supply is only for the consideration

c. The supply is only for and in the business course of the company or for persistence of

the company activity

d. There should be a connection with Australia; and

e. The supplier is required to be listed or listed under GST.

Noting the explanation given in “sec 9-10 (1)” the description of supply is notably

given in “sec 9-10 (1) of the GST Act” to take into account any type of supply whatever. It is

necessary that the supply of goods and services should be made by the suppliers (Hass and

Answer to question 1:

Issues:

The study that is considered here is for the claim of input tax credit for the taxable

supplies and taxable imports.

Laws:

The provision of the Goods and Service Tax introduced during the 1st July 2000 to

replace the wholesale tax and the indirect tax. GST is observed as the final consumption

inside the Australia and imports inside the Australia. Noting the description provided inside

the “sec 7-1 GST of the Act”, GST is commonly paid by tax payers on the chargeable

supplies (Ramli et al. 2015). The taxpayer can lower the GST by claiming the input tax

credits on the creditable acquisition and creditable imports. Where the input tax credit is

found to be in excess of the GST payable on the assessable supplies then the taxpayer is

allowed for a refund.

The definition regarding the taxable supply is noted down with in the sec 9-5, that says;

a. There is ought to be a supply

b. The supply is only for the consideration

c. The supply is only for and in the business course of the company or for persistence of

the company activity

d. There should be a connection with Australia; and

e. The supplier is required to be listed or listed under GST.

Noting the explanation given in “sec 9-10 (1)” the description of supply is notably

given in “sec 9-10 (1) of the GST Act” to take into account any type of supply whatever. It is

necessary that the supply of goods and services should be made by the suppliers (Hass and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Kopanyi 2017). On the other hand, for a supply to be considered as the taxable there must be

a consideration for that supply. This would involve the matter of price that must be inclusive

of GST. Whereas in “sec 9-15” consideration is defined as the voluntary and involuntary

payments, acts or forbearances that is related with the supplies or inducements for the supply

of anything (McCluskey and Franzsen 2017). The explanation provided inside the “para 9-

5(a) of the GST Act” explains that when the supplier makes the taxable supply then the

taxpayer must make the supply for consideration. As described in the “sec 195-1”,

consideration generally involves the payment in relation with the supply. The decision which

the taxation commissioner has given in “AP Group Ltd v CT (2013)” provides that it is

necessary to have a connection with the consideration for supply. In addition to this, the

supply should always happen in the business course of the entity.

There are also some situations when it becomes necessary for the purchaser to pay the

GST while the onus of paying the GST does not fall on the supplier (Cvrlje 2015). This is

known as reverse charge. The mechanism of reverse charge says that the service receiver is

required to pay the GST rather the service provider. The reverse charge mechanism is applied

apart from the tangible goods purchase and mainly it is implemented on the supply of

services. The rules of reverse charge mechanism say that there should some conditions that

must be met before its applicability (Elkins 2019). The conditions are that the supply must be

made to the entity in the course of its enterprise activity and should have the connection with

Australia. The supply must be made to the entity in exchange of payment and the supply is

either in parts or completely for the business purpose.

Application:

The applicability of the above given laws can be made in the evidences that is gained

from the case of City Sky Co. The company is listed under the GST and during the year it has

Kopanyi 2017). On the other hand, for a supply to be considered as the taxable there must be

a consideration for that supply. This would involve the matter of price that must be inclusive

of GST. Whereas in “sec 9-15” consideration is defined as the voluntary and involuntary

payments, acts or forbearances that is related with the supplies or inducements for the supply

of anything (McCluskey and Franzsen 2017). The explanation provided inside the “para 9-

5(a) of the GST Act” explains that when the supplier makes the taxable supply then the

taxpayer must make the supply for consideration. As described in the “sec 195-1”,

consideration generally involves the payment in relation with the supply. The decision which

the taxation commissioner has given in “AP Group Ltd v CT (2013)” provides that it is

necessary to have a connection with the consideration for supply. In addition to this, the

supply should always happen in the business course of the entity.

There are also some situations when it becomes necessary for the purchaser to pay the

GST while the onus of paying the GST does not fall on the supplier (Cvrlje 2015). This is

known as reverse charge. The mechanism of reverse charge says that the service receiver is

required to pay the GST rather the service provider. The reverse charge mechanism is applied

apart from the tangible goods purchase and mainly it is implemented on the supply of

services. The rules of reverse charge mechanism say that there should some conditions that

must be met before its applicability (Elkins 2019). The conditions are that the supply must be

made to the entity in the course of its enterprise activity and should have the connection with

Australia. The supply must be made to the entity in exchange of payment and the supply is

either in parts or completely for the business purpose.

Application:

The applicability of the above given laws can be made in the evidences that is gained

from the case of City Sky Co. The company is listed under the GST and during the year it has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

purchased vacant land in South of Brisbane. The initial objective of purchasing the land is for

building apartments on it so that the company can resale it. Now in respect to the GST and

input tax entitlements it can be stated that the vacant land is observed as capital gains tax

asset. Therefore, it can be stated that no GST is payable on the purchase of vacant land and

there cannot be entitlement relating to the input tax credit for City Sky Co.

Despite the fact given above, it is also noted that City Sky Co also made a payment

$33,000 to Maurice Blackburn. The payment made were mainly for the legal services that

City Sky Co has taken from it for development of property on the land. The payment that is

made to Maurice Blackburn by City Sky Co is a reverse charge mechanism since the GST is

paid by City Sky Co as the company here is the receiver of service (Burman et al. 2016).

Additionally, the services are taken by City Sky Co while carrying on the business activities

in Australia. Furthermore, quoting the instance of “AP Group Ltd v CT (2013)” the supply to

City Sky Co is a consideration under “sec 9-15”. The services are in exchange of payment.

So under the reverse charge mechanism the company will be permitted to get the input tax

credit because the legal services are continuance of City Sky Co business activities

(Auerbach and Hassett 2015).

Conclusion:

Under the reverse charge mechanism, the entitlement relating to the input tax credit is

available to City Sky Co for the legal services taken while no GST credit is available for the

purchase of vacant land since it is a capital asset.

Answer to question 2:

Sale of block of land:

The sale of the CGT asset leads to “CGT event A1” within “s.104-10”. Most notably

sale happens only when the change in ownership happens. “Sec.110-25” deals with the five

purchased vacant land in South of Brisbane. The initial objective of purchasing the land is for

building apartments on it so that the company can resale it. Now in respect to the GST and

input tax entitlements it can be stated that the vacant land is observed as capital gains tax

asset. Therefore, it can be stated that no GST is payable on the purchase of vacant land and

there cannot be entitlement relating to the input tax credit for City Sky Co.

Despite the fact given above, it is also noted that City Sky Co also made a payment

$33,000 to Maurice Blackburn. The payment made were mainly for the legal services that

City Sky Co has taken from it for development of property on the land. The payment that is

made to Maurice Blackburn by City Sky Co is a reverse charge mechanism since the GST is

paid by City Sky Co as the company here is the receiver of service (Burman et al. 2016).

Additionally, the services are taken by City Sky Co while carrying on the business activities

in Australia. Furthermore, quoting the instance of “AP Group Ltd v CT (2013)” the supply to

City Sky Co is a consideration under “sec 9-15”. The services are in exchange of payment.

So under the reverse charge mechanism the company will be permitted to get the input tax

credit because the legal services are continuance of City Sky Co business activities

(Auerbach and Hassett 2015).

Conclusion:

Under the reverse charge mechanism, the entitlement relating to the input tax credit is

available to City Sky Co for the legal services taken while no GST credit is available for the

purchase of vacant land since it is a capital asset.

Answer to question 2:

Sale of block of land:

The sale of the CGT asset leads to “CGT event A1” within “s.104-10”. Most notably

sale happens only when the change in ownership happens. “Sec.110-25” deals with the five

5TAXATION LAW

elements of CGT. This involves the acquisition cost as the first element in “sec.110-25 (2)”

which represents the total money taxpayer paid to purchase the asset. The second elements is

associated with the incidental cost such as the stamp duty, legal fees, brokerage etc. under

“sec.110-25 (3)”. The third element is the charges of owning the asset under “sec.110-25

(4)”. This element involve interest paid on borrowed fund, rates, taxes etc. occurred while

owning the asset. Generally these cost is not permitted for tax deduction when the asset is not

used for making income (Wanless 2018). The fourth elements is known as the enhancement

cost under “sec.110-25 (5)” that takes into account the capital outgoings. This element

denotes the capital outgoing occurred for preserving or improving the asset value held by

taxpayer. The fifth element under “sec.110-25 (6)” is the title cost (Arnason and Gissurarson

2017). The title cost usually represents the cost of establishing, holding and defending the

title or right to the asset.

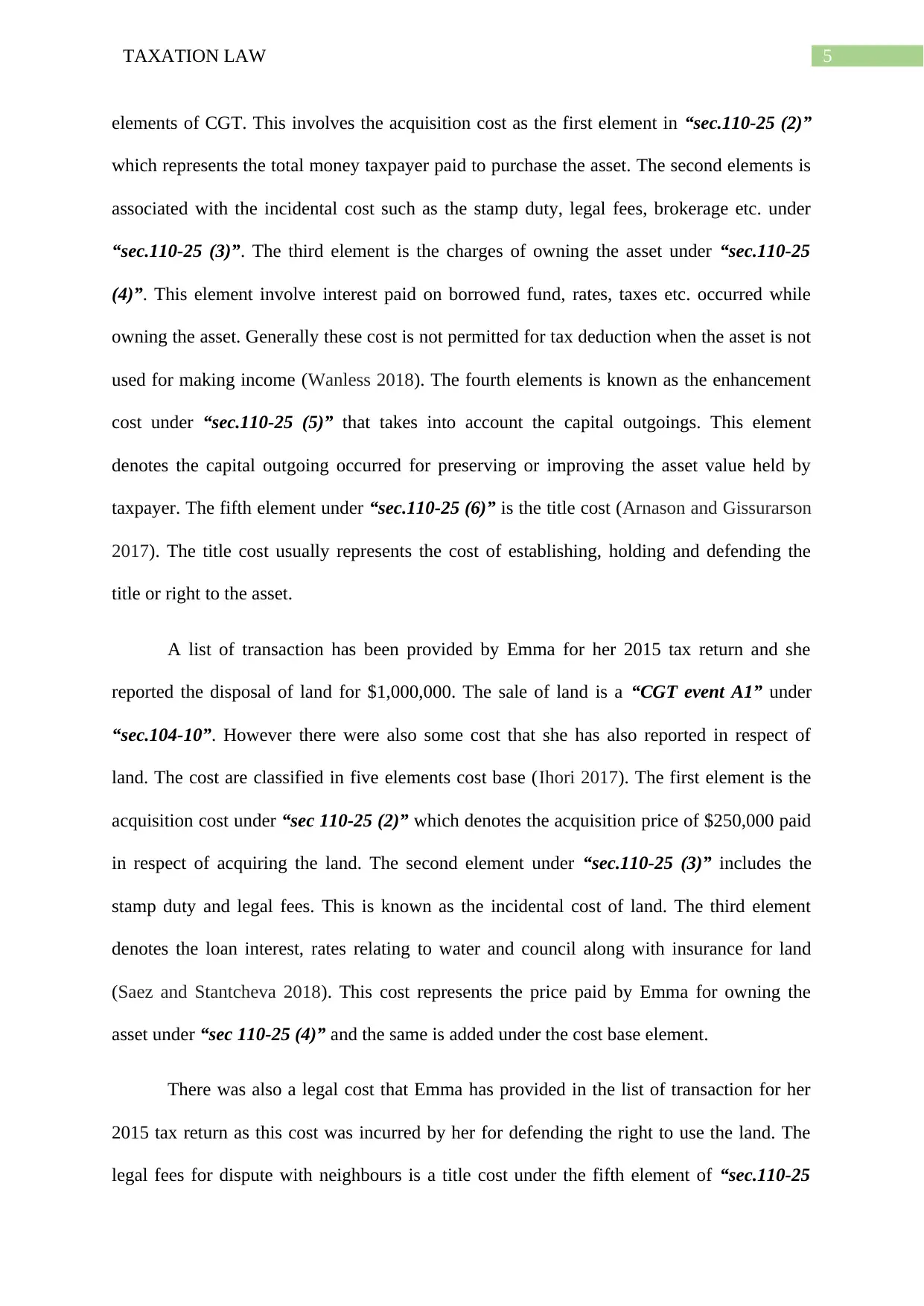

A list of transaction has been provided by Emma for her 2015 tax return and she

reported the disposal of land for $1,000,000. The sale of land is a “CGT event A1” under

“sec.104-10”. However there were also some cost that she has also reported in respect of

land. The cost are classified in five elements cost base (Ihori 2017). The first element is the

acquisition cost under “sec 110-25 (2)” which denotes the acquisition price of $250,000 paid

in respect of acquiring the land. The second element under “sec.110-25 (3)” includes the

stamp duty and legal fees. This is known as the incidental cost of land. The third element

denotes the loan interest, rates relating to water and council along with insurance for land

(Saez and Stantcheva 2018). This cost represents the price paid by Emma for owning the

asset under “sec 110-25 (4)” and the same is added under the cost base element.

There was also a legal cost that Emma has provided in the list of transaction for her

2015 tax return as this cost was incurred by her for defending the right to use the land. The

legal fees for dispute with neighbours is a title cost under the fifth element of “sec.110-25

elements of CGT. This involves the acquisition cost as the first element in “sec.110-25 (2)”

which represents the total money taxpayer paid to purchase the asset. The second elements is

associated with the incidental cost such as the stamp duty, legal fees, brokerage etc. under

“sec.110-25 (3)”. The third element is the charges of owning the asset under “sec.110-25

(4)”. This element involve interest paid on borrowed fund, rates, taxes etc. occurred while

owning the asset. Generally these cost is not permitted for tax deduction when the asset is not

used for making income (Wanless 2018). The fourth elements is known as the enhancement

cost under “sec.110-25 (5)” that takes into account the capital outgoings. This element

denotes the capital outgoing occurred for preserving or improving the asset value held by

taxpayer. The fifth element under “sec.110-25 (6)” is the title cost (Arnason and Gissurarson

2017). The title cost usually represents the cost of establishing, holding and defending the

title or right to the asset.

A list of transaction has been provided by Emma for her 2015 tax return and she

reported the disposal of land for $1,000,000. The sale of land is a “CGT event A1” under

“sec.104-10”. However there were also some cost that she has also reported in respect of

land. The cost are classified in five elements cost base (Ihori 2017). The first element is the

acquisition cost under “sec 110-25 (2)” which denotes the acquisition price of $250,000 paid

in respect of acquiring the land. The second element under “sec.110-25 (3)” includes the

stamp duty and legal fees. This is known as the incidental cost of land. The third element

denotes the loan interest, rates relating to water and council along with insurance for land

(Saez and Stantcheva 2018). This cost represents the price paid by Emma for owning the

asset under “sec 110-25 (4)” and the same is added under the cost base element.

There was also a legal cost that Emma has provided in the list of transaction for her

2015 tax return as this cost was incurred by her for defending the right to use the land. The

legal fees for dispute with neighbours is a title cost under the fifth element of “sec.110-25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

(6)” which is added under the five elements of cost base (Fleurbaey and Maniquet 2018).

There was instance where before selling the land some dangerous pine trees were cleared at a

cost of $27,500. This cost represents enhancement cost and should be termed as capital

outgoing for preserving the asset. So it will be included inside the fourth element cost base

under “sec.110-25 (5)”.

Sale of shares:

The key design feature of the CGT is that it considers those assets bought after 20 sept

1985. This generally means that CGT does not applies to the asset before the date of 20 sept

(6)” which is added under the five elements of cost base (Fleurbaey and Maniquet 2018).

There was instance where before selling the land some dangerous pine trees were cleared at a

cost of $27,500. This cost represents enhancement cost and should be termed as capital

outgoing for preserving the asset. So it will be included inside the fourth element cost base

under “sec.110-25 (5)”.

Sale of shares:

The key design feature of the CGT is that it considers those assets bought after 20 sept

1985. This generally means that CGT does not applies to the asset before the date of 20 sept

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

1985 (Ramsey 2015). An asset when it is acquired before the aforementioned date is known

as the pre-CGT asset and upon making the disposal there is no tax payable.

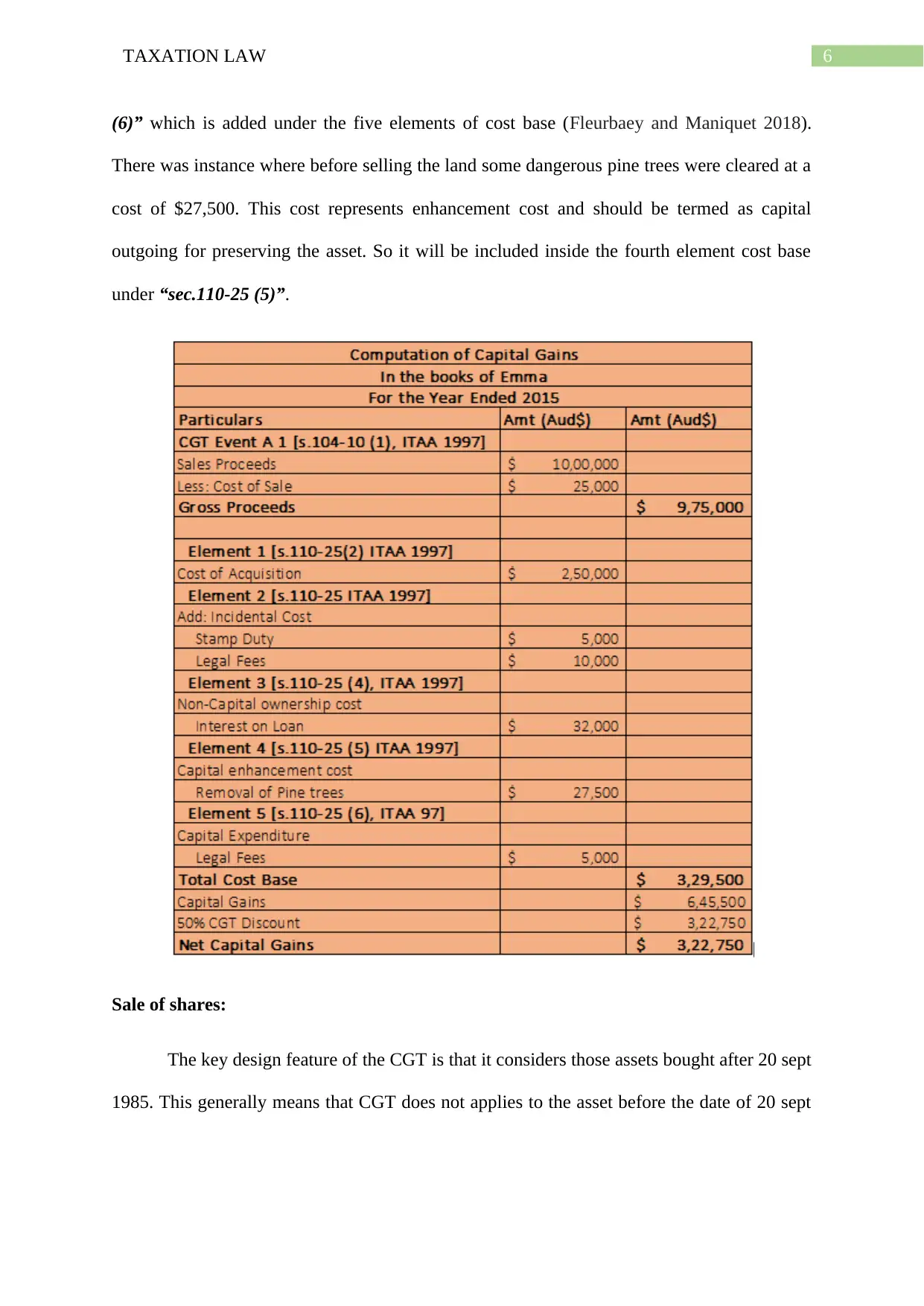

While filing for 2015 Emma Tax return it is noticed that she has also sold the shares

that she held in Rio Tinto. The shares she has held in Rio Tinto was bought in 1982. When

Emma sold the asset in 2015 she derived capital gains. Emma purchased the shares before 20

sept 1985. So the shares are pre-CGT asset and upon making its disposal in 2015 she does not

has to pay tax as it is exempted.

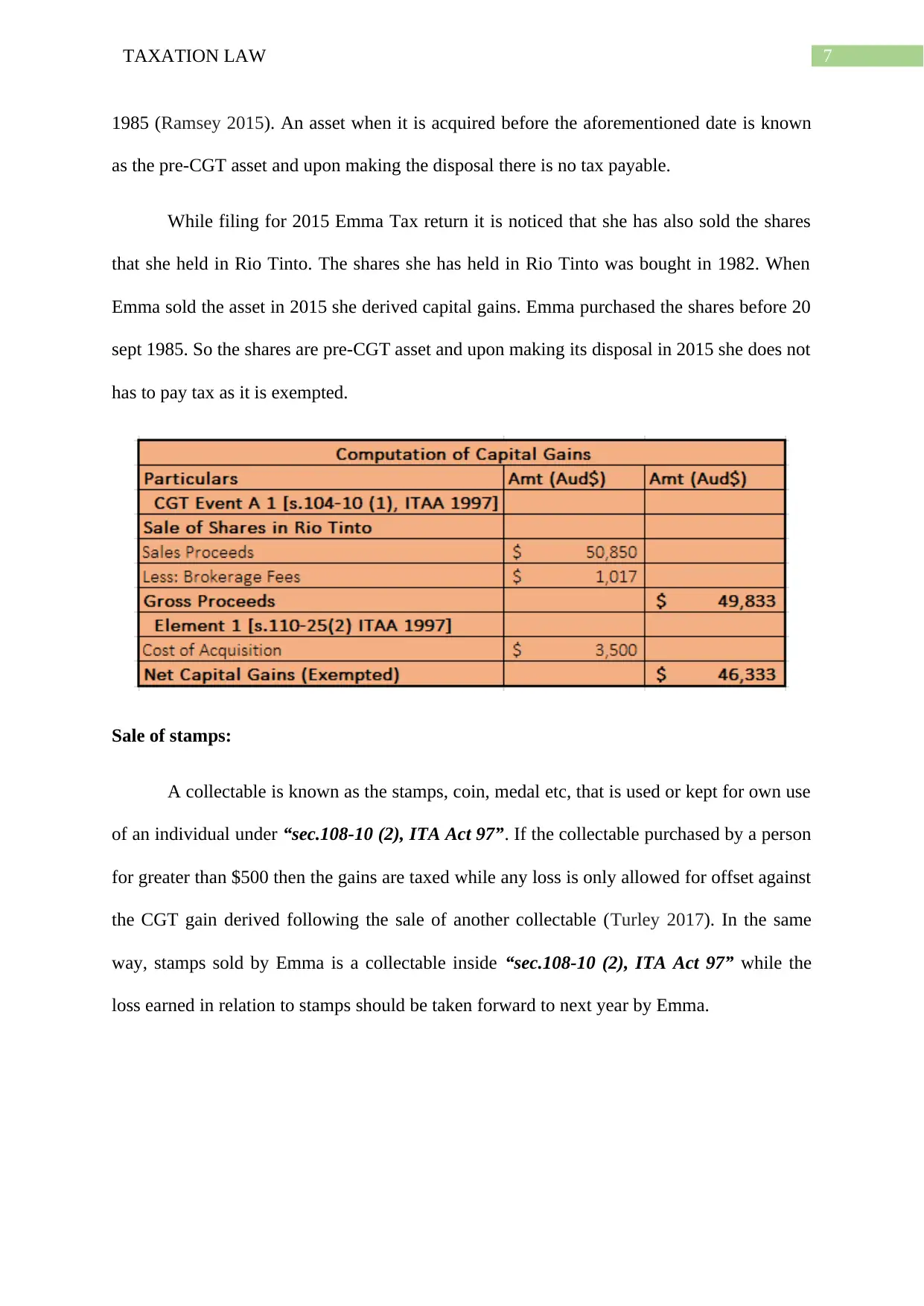

Sale of stamps:

A collectable is known as the stamps, coin, medal etc, that is used or kept for own use

of an individual under “sec.108-10 (2), ITA Act 97”. If the collectable purchased by a person

for greater than $500 then the gains are taxed while any loss is only allowed for offset against

the CGT gain derived following the sale of another collectable (Turley 2017). In the same

way, stamps sold by Emma is a collectable inside “sec.108-10 (2), ITA Act 97” while the

loss earned in relation to stamps should be taken forward to next year by Emma.

1985 (Ramsey 2015). An asset when it is acquired before the aforementioned date is known

as the pre-CGT asset and upon making the disposal there is no tax payable.

While filing for 2015 Emma Tax return it is noticed that she has also sold the shares

that she held in Rio Tinto. The shares she has held in Rio Tinto was bought in 1982. When

Emma sold the asset in 2015 she derived capital gains. Emma purchased the shares before 20

sept 1985. So the shares are pre-CGT asset and upon making its disposal in 2015 she does not

has to pay tax as it is exempted.

Sale of stamps:

A collectable is known as the stamps, coin, medal etc, that is used or kept for own use

of an individual under “sec.108-10 (2), ITA Act 97”. If the collectable purchased by a person

for greater than $500 then the gains are taxed while any loss is only allowed for offset against

the CGT gain derived following the sale of another collectable (Turley 2017). In the same

way, stamps sold by Emma is a collectable inside “sec.108-10 (2), ITA Act 97” while the

loss earned in relation to stamps should be taken forward to next year by Emma.

8TAXATION LAW

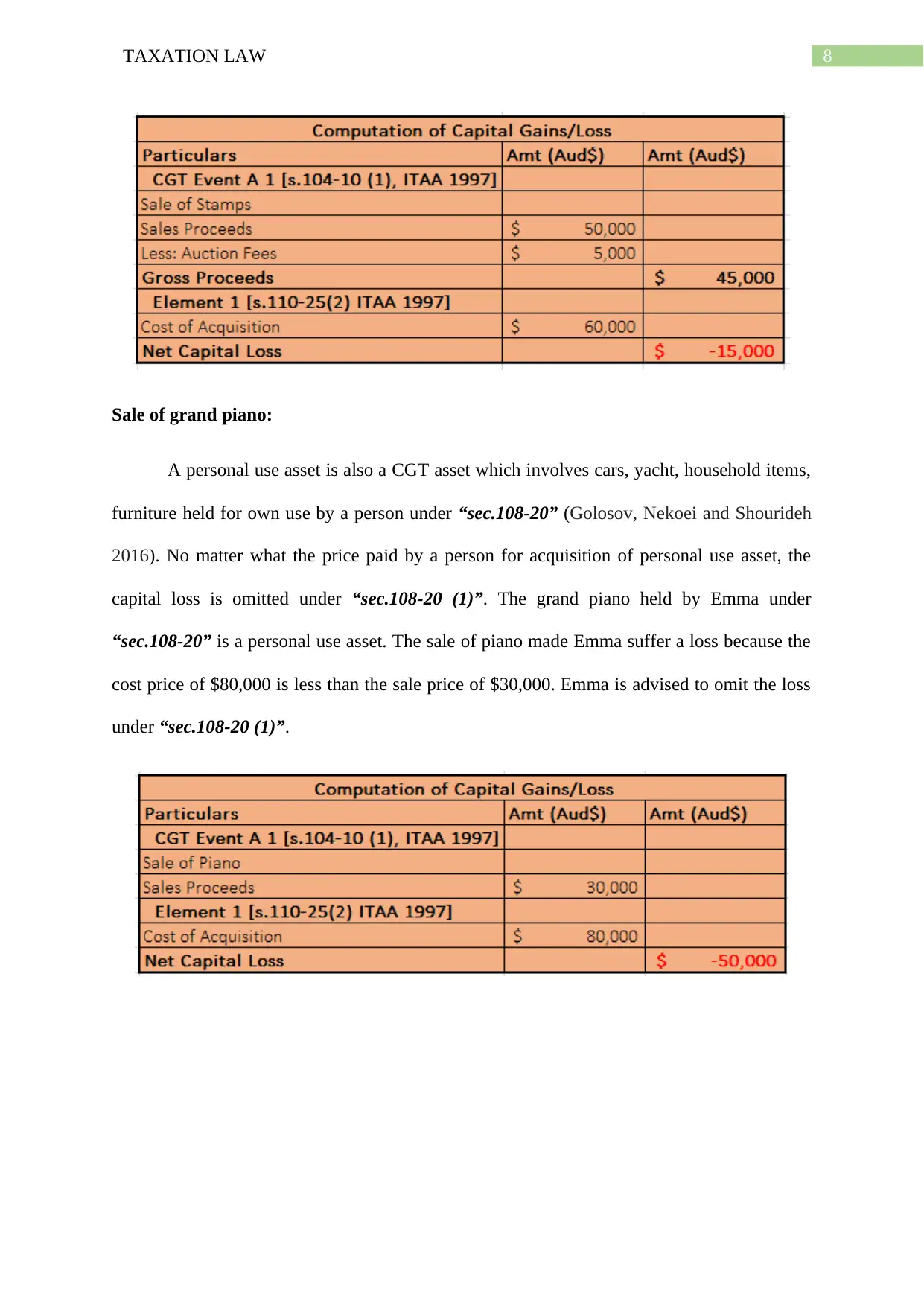

Sale of grand piano:

A personal use asset is also a CGT asset which involves cars, yacht, household items,

furniture held for own use by a person under “sec.108-20” (Golosov, Nekoei and Shourideh

2016). No matter what the price paid by a person for acquisition of personal use asset, the

capital loss is omitted under “sec.108-20 (1)”. The grand piano held by Emma under

“sec.108-20” is a personal use asset. The sale of piano made Emma suffer a loss because the

cost price of $80,000 is less than the sale price of $30,000. Emma is advised to omit the loss

under “sec.108-20 (1)”.

Sale of grand piano:

A personal use asset is also a CGT asset which involves cars, yacht, household items,

furniture held for own use by a person under “sec.108-20” (Golosov, Nekoei and Shourideh

2016). No matter what the price paid by a person for acquisition of personal use asset, the

capital loss is omitted under “sec.108-20 (1)”. The grand piano held by Emma under

“sec.108-20” is a personal use asset. The sale of piano made Emma suffer a loss because the

cost price of $80,000 is less than the sale price of $30,000. Emma is advised to omit the loss

under “sec.108-20 (1)”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Arnason, R. and Gissurarson, H.H., 2017. Individual transferable quotas in theory and

practice (Vol. 4). Almenna bókafélagið.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Cvrlje, D., 2015. Tax literacy as an instrument of combating and overcoming tax system

complexity, low tax morale and tax non-compliance. The Macrotheme Review, 4(3), pp.156-

167.

Elkins, D., 2019. Consumption Taxation in Rawls' Theory of Justice.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Golosov, M., Nekoei, A. and Shourideh, A., 2016. Taxation, Sorting and Redistribution:

Theory and Evidence.

Hass, A. and Kopanyi, M., 2017. Taxation of Vacant Urban Land: From Theory to

Practice. International Growth Center, London School of Economic and Political Science:

London, UK.

Ihori, T., 2017. The Theory of Taxation. In Principles of Public Finance (pp. 205-227).

Springer, Singapore.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

References:

Arnason, R. and Gissurarson, H.H., 2017. Individual transferable quotas in theory and

practice (Vol. 4). Almenna bókafélagið.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Cvrlje, D., 2015. Tax literacy as an instrument of combating and overcoming tax system

complexity, low tax morale and tax non-compliance. The Macrotheme Review, 4(3), pp.156-

167.

Elkins, D., 2019. Consumption Taxation in Rawls' Theory of Justice.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Golosov, M., Nekoei, A. and Shourideh, A., 2016. Taxation, Sorting and Redistribution:

Theory and Evidence.

Hass, A. and Kopanyi, M., 2017. Taxation of Vacant Urban Land: From Theory to

Practice. International Growth Center, London School of Economic and Political Science:

London, UK.

Ihori, T., 2017. The Theory of Taxation. In Principles of Public Finance (pp. 205-227).

Springer, Singapore.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Ramli, R., Palil, M.R., Hassan, N.S.A. and Mustapha, A.F., 2015. Compliance costs of Goods

and Services Tax (GST) among small and medium enterprises. Jurnal Pengurusan (UKM

Journal of Management), 45.

Ramsey, F.P., 2015. A Contribution to the Theory of Taxation. Economic Journal, 125(583),

pp.254-268.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Turley, G., 2017. Transition, taxation and the State. Routledge.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

Ramli, R., Palil, M.R., Hassan, N.S.A. and Mustapha, A.F., 2015. Compliance costs of Goods

and Services Tax (GST) among small and medium enterprises. Jurnal Pengurusan (UKM

Journal of Management), 45.

Ramsey, F.P., 2015. A Contribution to the Theory of Taxation. Economic Journal, 125(583),

pp.254-268.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Turley, G., 2017. Transition, taxation and the State. Routledge.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.