Taxation Law Assignment - Income, Fringe Benefits, and Capital Gains

VerifiedAdded on 2021/05/27

|8

|1802

|193

Homework Assignment

AI Summary

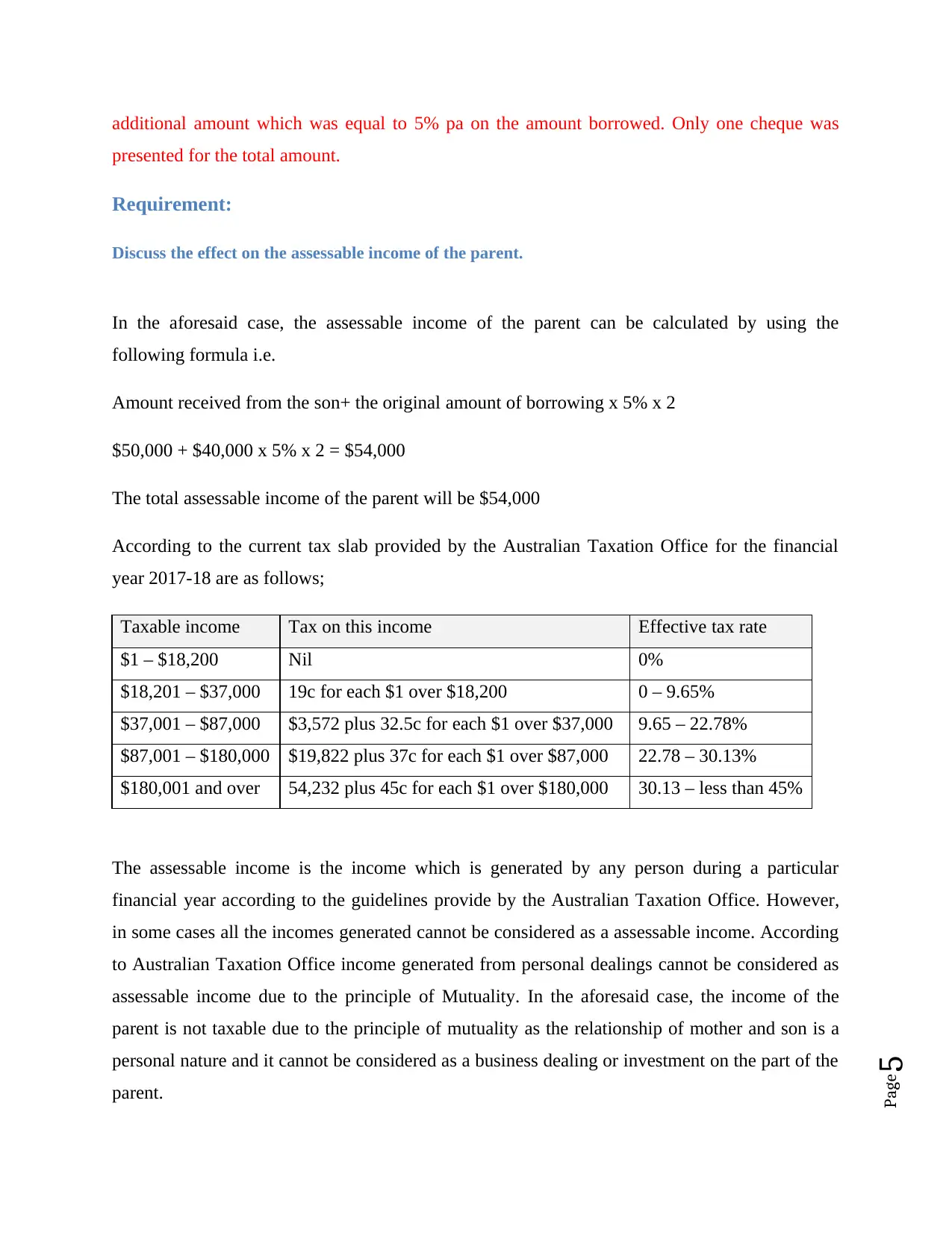

This taxation law assignment solution addresses several key areas of Australian taxation. It begins with an analysis of income from personal exertion, determining whether payments received by a mountain climber for her life story, manuscript, and photographs are assessable income. The solution then calculates the taxable value of a car fringe benefit using the statutory formula. Next, it explores the effect of a parent lending money to their son, considering whether the additional repayment is assessable income, and addresses the principle of mutuality. Finally, the assignment delves into capital gains tax (CGT), calculating Scott's net capital gain or loss from the sale of a property, and analyzing how the outcome would differ if the property was sold to his daughter or owned by a company. The document concludes with a list of relevant references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.