T2 2019 HAA3042 Taxation Law Assignment: Individual Tax Analysis

VerifiedAdded on 2022/11/09

|13

|2899

|164

Homework Assignment

AI Summary

This taxation law assignment addresses two key questions related to Australian tax law. The first question analyzes the capital gains tax (CGT) implications for Jasmine, covering the sale of her family home, car, business, furniture, and paintings, with detailed references to relevant sections of the ITAA 1997. The assignment examines pre-CGT assets, personal use assets, small business CGT concessions, and the treatment of collectables. The second question focuses on the depreciation of a CNC machine, exploring the determination of its cost base and the start time for calculating capital allowances, referencing relevant sections of the ITAA 1997 and case law. The assignment provides a comprehensive overview of these tax issues, offering practical application of tax law principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Laws and Application:...........................................................................................................7

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Laws and Application:...........................................................................................................7

Conclusion:..........................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Introduction:

“Part 3.1 of the ITAA 1997” explains that there are certain general rules that are

applied in determining the CGT liability. There is a limitation which is imposed by the “sec

100-25 (1), ITAA 1997” that restricts the assets on which part 3 is applicable to those which

is purchased on or following the 20th September 1985 (Miller and Oats 2016). The taxpayer

must understand that till 21st September 1999 those gains are levied tax that are falling within

the GST regime. The provision of CGT is only implemented on the realised or actual gains.

Under the “sec 6-10” capital gains are held for assessment as the statutory earnings while

under “sec 102-5 (1)” the capital gains is included as the assessable earnings of the taxpayer.

Answer A:

Sale of family home:

There is an explanation that is mentioned in “Div 118-B” that relates to the main

residence exemption (Anderson 2019). The common principles given in the “sec 118.110-

ITAA 1997” pronounces that capital gains or loss arising from house in which taxpayer’s

lives as their main dwelling is usually exempted from tax.

Jasmine as a resident of Australia has made the decision of moving to UK

permanently and decides to sell all of her assets. In the current year she sells her house that

valued $650,000. In 1981 the house was purchased for $40,000 by Jasmine. She used the

house for her main dwelling purpose and never used it for producing income. Therefore, the

house here should be treated as pre-CGT asset (Osborn 2018). This is because the house was

purchased before 20/9/1985. The capital gains that is made by Jasmine on selling the house is

exempted from tax under “sec 118.110-ITAA 1997”.

Answer to question 1:

Introduction:

“Part 3.1 of the ITAA 1997” explains that there are certain general rules that are

applied in determining the CGT liability. There is a limitation which is imposed by the “sec

100-25 (1), ITAA 1997” that restricts the assets on which part 3 is applicable to those which

is purchased on or following the 20th September 1985 (Miller and Oats 2016). The taxpayer

must understand that till 21st September 1999 those gains are levied tax that are falling within

the GST regime. The provision of CGT is only implemented on the realised or actual gains.

Under the “sec 6-10” capital gains are held for assessment as the statutory earnings while

under “sec 102-5 (1)” the capital gains is included as the assessable earnings of the taxpayer.

Answer A:

Sale of family home:

There is an explanation that is mentioned in “Div 118-B” that relates to the main

residence exemption (Anderson 2019). The common principles given in the “sec 118.110-

ITAA 1997” pronounces that capital gains or loss arising from house in which taxpayer’s

lives as their main dwelling is usually exempted from tax.

Jasmine as a resident of Australia has made the decision of moving to UK

permanently and decides to sell all of her assets. In the current year she sells her house that

valued $650,000. In 1981 the house was purchased for $40,000 by Jasmine. She used the

house for her main dwelling purpose and never used it for producing income. Therefore, the

house here should be treated as pre-CGT asset (Osborn 2018). This is because the house was

purchased before 20/9/1985. The capital gains that is made by Jasmine on selling the house is

exempted from tax under “sec 118.110-ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer B: Sale of Car:

Certainly, there are some of the CGT assets under “sec. 108-20, ITAA 1997” beside

the collectable that are used by taxpayer for private purpose or personal usage purpose. These

assets are known as personal use assets (PUA’S). Examples of personal use assets mainly

involve the racehorses, boats, furniture, household goods and electrical goods. In pursuit of

the “sec 118.110 (3), ITAA 1997” the taxpayer here are required to pay attention that

whenever there is a capital loss happening from sale of PUA’s they should be simply ignored

under “sec 108-20 (1)” (Herdegen 2016). Whenever a taxpayer sells the CGT asset there is a

CGT event A1 under “sec 104.10 ITAA 1997”. This event is applied on assets that is bought

by taxpayer afterwards 19/9/1985.

Jasmine in 2011 purchased a car. The car valued $31,000 when she purchased it. In

the present tax year the car worth approximately $10,000. The car is a personal use asset

under the definition of “sec 108.20 (1), ITAA 1997” (Frecknall-Hughes 2014). Jasmine

mainly kept the car for her personal use. The sale of car by Jasmine led to CGT event A1

under “sec 104-10, ITAA 1997”. As she made a capital loss from the car, the loss will be

ignored under “sec 108-20(1)”.

Answer C: Sale of business:

“Division 152-ITAA 1997” says that to help the small business there are certain

concessions from CGT is given. There are few rudimentary circumstances that must be met

(Qureshi and Kumar 2019). This includes;

a. The company should be classified as small business entity with the total turnover of

$2 million or the net value of it is assets is no more than $6 million.

b. The CGT asset should be categorized as the active asset.

Answer B: Sale of Car:

Certainly, there are some of the CGT assets under “sec. 108-20, ITAA 1997” beside

the collectable that are used by taxpayer for private purpose or personal usage purpose. These

assets are known as personal use assets (PUA’S). Examples of personal use assets mainly

involve the racehorses, boats, furniture, household goods and electrical goods. In pursuit of

the “sec 118.110 (3), ITAA 1997” the taxpayer here are required to pay attention that

whenever there is a capital loss happening from sale of PUA’s they should be simply ignored

under “sec 108-20 (1)” (Herdegen 2016). Whenever a taxpayer sells the CGT asset there is a

CGT event A1 under “sec 104.10 ITAA 1997”. This event is applied on assets that is bought

by taxpayer afterwards 19/9/1985.

Jasmine in 2011 purchased a car. The car valued $31,000 when she purchased it. In

the present tax year the car worth approximately $10,000. The car is a personal use asset

under the definition of “sec 108.20 (1), ITAA 1997” (Frecknall-Hughes 2014). Jasmine

mainly kept the car for her personal use. The sale of car by Jasmine led to CGT event A1

under “sec 104-10, ITAA 1997”. As she made a capital loss from the car, the loss will be

ignored under “sec 108-20(1)”.

Answer C: Sale of business:

“Division 152-ITAA 1997” says that to help the small business there are certain

concessions from CGT is given. There are few rudimentary circumstances that must be met

(Qureshi and Kumar 2019). This includes;

a. The company should be classified as small business entity with the total turnover of

$2 million or the net value of it is assets is no more than $6 million.

b. The CGT asset should be categorized as the active asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

On meeting the above conditions, small business can avail the below given four

concessions;

a. 15-year exemption from overall capital gains for assets that has been owned for

greater than 15 years and the taxpayer is minimum 55 years or older.

b. A reduction of 50% from CGT is given when the taxpayer qualifies under this

concession. The capital gains under this system is lowered by 50% following the

application of general discount

c. Retirement concession allows the taxpayer to ignore capital gains on sale of assets

related to business up to $500,000. The taxpayer must only use the gains for

retirement purpose (Butler 2019).

d. Roll-over relief is given upon deferring the capital gains when the taxpayer purchases

any replacement assets.

As jasmine is planning to leave Australia permanently, she sells her small cleaning

business for $125,000. The business equipment were sold by her for $65,000 while the

goodwill was sold for $60,000.

Jasmine in this situation can obtain a small business CGT concession in respect to

“Div 152-ITAA 1997”. This is because her cleaning business has the assets which has net

value of no more than $6million. The CGT asset that is held by Jasmine is also an active

asset. Jasmine can get the retirement concession from the sale of business equipment (Jones

and Rhoades-Catanach 2015). While for goodwill a “CGT event C1” happened when

Jasmine sold it for $60,000. It is assumed that the business was permanently ceased by

Jasmine when the goodwill was sold. Hence, the capital gains from goodwill can be ignored

under retirement concession.

On meeting the above conditions, small business can avail the below given four

concessions;

a. 15-year exemption from overall capital gains for assets that has been owned for

greater than 15 years and the taxpayer is minimum 55 years or older.

b. A reduction of 50% from CGT is given when the taxpayer qualifies under this

concession. The capital gains under this system is lowered by 50% following the

application of general discount

c. Retirement concession allows the taxpayer to ignore capital gains on sale of assets

related to business up to $500,000. The taxpayer must only use the gains for

retirement purpose (Butler 2019).

d. Roll-over relief is given upon deferring the capital gains when the taxpayer purchases

any replacement assets.

As jasmine is planning to leave Australia permanently, she sells her small cleaning

business for $125,000. The business equipment were sold by her for $65,000 while the

goodwill was sold for $60,000.

Jasmine in this situation can obtain a small business CGT concession in respect to

“Div 152-ITAA 1997”. This is because her cleaning business has the assets which has net

value of no more than $6million. The CGT asset that is held by Jasmine is also an active

asset. Jasmine can get the retirement concession from the sale of business equipment (Jones

and Rhoades-Catanach 2015). While for goodwill a “CGT event C1” happened when

Jasmine sold it for $60,000. It is assumed that the business was permanently ceased by

Jasmine when the goodwill was sold. Hence, the capital gains from goodwill can be ignored

under retirement concession.

5TAXATION LAW

Answer D: Sale of furniture:

Jasmine sold her furniture that valued $2,000 for a sale price of $5,000. The furniture

must be considered as personal use asset under sec 108-20 because she kept for her own

usage. There is a general rule under “sec 118.10(3)” which explains that the taxpayer should

ignore the capital gains from PUA’s when it is purchased for lower than $10,000 (Wattel,

Marres and Vermeulen 2018). The sale of furniture by Jasmine led to “CGT event A1” under

“sec 104-10, ITAA 1997”. The capital gains from furniture is ignored under “sec 118.10 (3)”

in the situation of Jasmine because the asset was acquired by her for $2,000 which is below

the first element cost base of $10,000.

Answer E: Sale of Paintings:

Accordingly “sec 108.10, ITAA 1997” denotes collectables as CGT assets which is

used by taxpayer for personal satisfaction and usage (Sikka 2017). The examples of this

assets are antiques, painting, coins, stamps etc. Under “sec 118.10 (1)” capital gains from

selling the collectables is disregarded when purchase price is lower than $500.

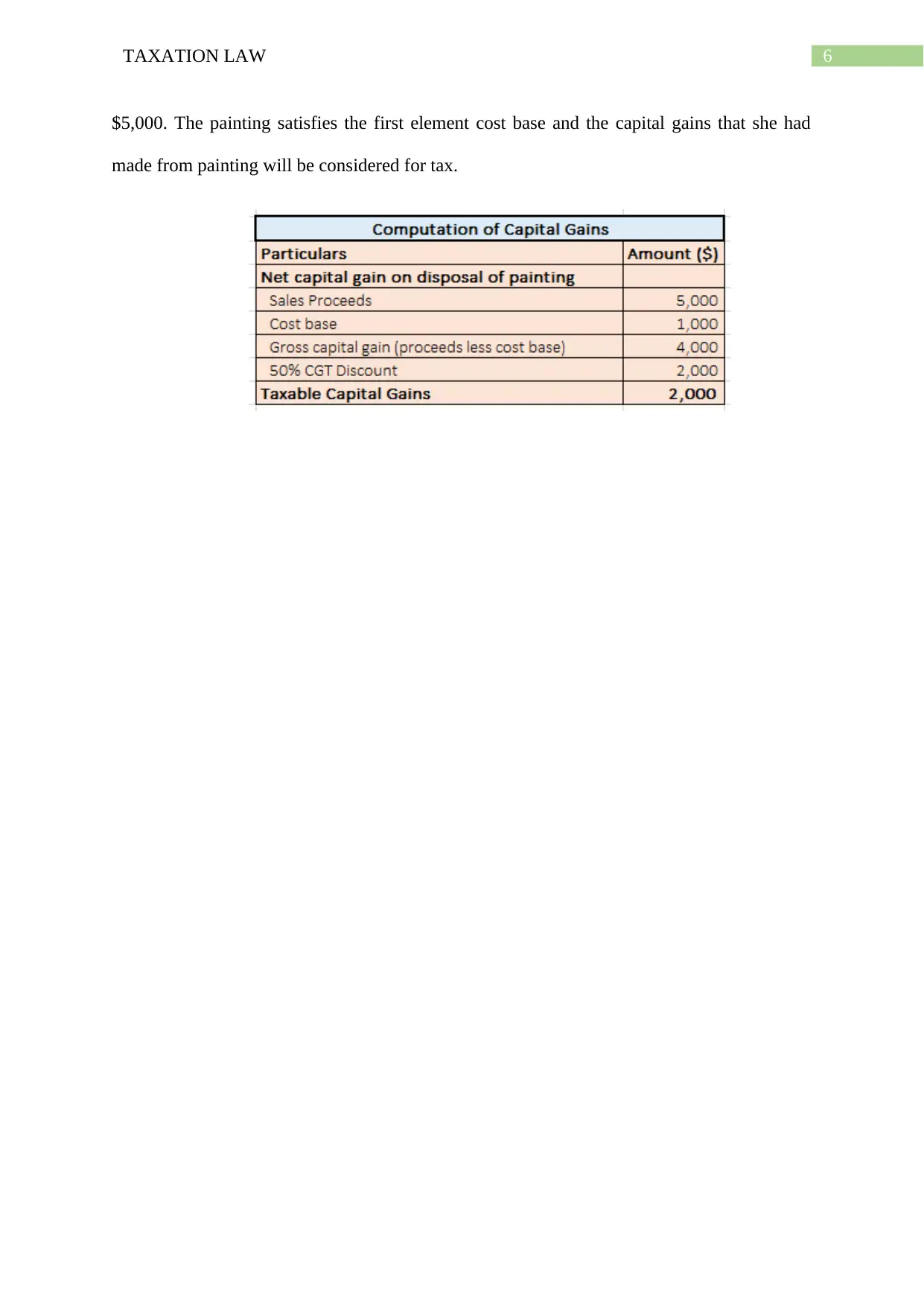

Numerous paintings was sold by Jasmine in the present tax year. All the paintings

were having the cost of $500 but she sold it for $35,000. A “CGT event A1” under “sec 104-

10, ITAA 1997” happened when Jasmine sold the paintings. The paintings are treated as

collectables under the definition given in “sec 108.10, ITAA 1997”. However, under “sec

118.10 (1), ITAA 1997” the capital gains from paintings made by Jasmine will be ignored

because the purchase price is only $500. There is also an exception where a painting was

purchased by Jasmine directly from the artist that had the value of $1,000 but was sold for

Answer D: Sale of furniture:

Jasmine sold her furniture that valued $2,000 for a sale price of $5,000. The furniture

must be considered as personal use asset under sec 108-20 because she kept for her own

usage. There is a general rule under “sec 118.10(3)” which explains that the taxpayer should

ignore the capital gains from PUA’s when it is purchased for lower than $10,000 (Wattel,

Marres and Vermeulen 2018). The sale of furniture by Jasmine led to “CGT event A1” under

“sec 104-10, ITAA 1997”. The capital gains from furniture is ignored under “sec 118.10 (3)”

in the situation of Jasmine because the asset was acquired by her for $2,000 which is below

the first element cost base of $10,000.

Answer E: Sale of Paintings:

Accordingly “sec 108.10, ITAA 1997” denotes collectables as CGT assets which is

used by taxpayer for personal satisfaction and usage (Sikka 2017). The examples of this

assets are antiques, painting, coins, stamps etc. Under “sec 118.10 (1)” capital gains from

selling the collectables is disregarded when purchase price is lower than $500.

Numerous paintings was sold by Jasmine in the present tax year. All the paintings

were having the cost of $500 but she sold it for $35,000. A “CGT event A1” under “sec 104-

10, ITAA 1997” happened when Jasmine sold the paintings. The paintings are treated as

collectables under the definition given in “sec 108.10, ITAA 1997”. However, under “sec

118.10 (1), ITAA 1997” the capital gains from paintings made by Jasmine will be ignored

because the purchase price is only $500. There is also an exception where a painting was

purchased by Jasmine directly from the artist that had the value of $1,000 but was sold for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

$5,000. The painting satisfies the first element cost base and the capital gains that she had

made from painting will be considered for tax.

$5,000. The painting satisfies the first element cost base and the capital gains that she had

made from painting will be considered for tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

This question is concerned with the issue of determining the start time of asset for

computing the decline in value of the asset.

Laws and Application:

Discussion of First Element of CNC Machine cost base:

The cost base of depreciating asset under the present legislation of “sec 40.175, ITAA

1997” is classified under two elements. “Sec 40.180” comprises of the specific rules relating

to first element. While “subsection 40.180 (1)” provides direction in computation of the first

element when the taxpayer starts holding the asset for taxable purpose (Gashenko, Zima and

Davidyan 2019). The first element under “sec 40.180” includes the price of purchase which

the taxpayer pays to purchase the asset.

There are two important regimes that is related to the capital allowance. The uniform

allowance is dealt under “Division 40, ITAA 1997” while the capital work allowance on

building depreciation is explained under “Division 43, ITAA 1997” (Keen and Mullins

2016). A company under “sec 40.25 (1), ITAA 1997” is permitted to claim the deduction for

the amount that is equal to the “fall in value” during the income year of the “depreciating

asset” which the taxpayer has “held” through the year. While “sec 40-25 (2)” says that

deduction is lowered when it is noticed that the assets fall in value is attributable to the other

use as well apart from the taxable purpose.

The factual situation of John shows that he has been operating the business of vehicle

parts and accessories manufacturing company. John generally produces certified BMW parts.

He bought a CNC machine that was imported from Germany where he incurred an

acquisition cost of $300,000. Under the “section 40-30, ITAA 1997” the CNC amounts to a

Answer to question 2:

Issues:

This question is concerned with the issue of determining the start time of asset for

computing the decline in value of the asset.

Laws and Application:

Discussion of First Element of CNC Machine cost base:

The cost base of depreciating asset under the present legislation of “sec 40.175, ITAA

1997” is classified under two elements. “Sec 40.180” comprises of the specific rules relating

to first element. While “subsection 40.180 (1)” provides direction in computation of the first

element when the taxpayer starts holding the asset for taxable purpose (Gashenko, Zima and

Davidyan 2019). The first element under “sec 40.180” includes the price of purchase which

the taxpayer pays to purchase the asset.

There are two important regimes that is related to the capital allowance. The uniform

allowance is dealt under “Division 40, ITAA 1997” while the capital work allowance on

building depreciation is explained under “Division 43, ITAA 1997” (Keen and Mullins

2016). A company under “sec 40.25 (1), ITAA 1997” is permitted to claim the deduction for

the amount that is equal to the “fall in value” during the income year of the “depreciating

asset” which the taxpayer has “held” through the year. While “sec 40-25 (2)” says that

deduction is lowered when it is noticed that the assets fall in value is attributable to the other

use as well apart from the taxable purpose.

The factual situation of John shows that he has been operating the business of vehicle

parts and accessories manufacturing company. John generally produces certified BMW parts.

He bought a CNC machine that was imported from Germany where he incurred an

acquisition cost of $300,000. Under the “section 40-30, ITAA 1997” the CNC amounts to a

8TAXATION LAW

depreciating asset. Mentioning the judgement of “Wangaratta Woollen Mills Ltd v FCT

(1969)” the CNC machine satisfies the definition plant because the machine has the limited

useful life. The machine is also anticipated to fall in value based on the usage over the years.

Referring “sec 40.25 (1), ITAA 1997” John is permitted to deduct the sum which is

equal to the sum of decline in value of machine during the income year of the depreciating

asset. This is because under “sec 40.25 (2), ITAA 1997” John has held the CNC machine all

through the year for taxable purpose (Sadiq 2019). With regard to sec “Subdivision 40-C” to

compute cost base of machine for claiming capital allowance of the depreciating asset with

the first element under “sec 40.180 (1)”, it would include the purchase price that is paid by

John to acquire the CNC machine (Shome 2018).

Discussion of Second Element of cost base of CNC Machine and its start time:

The taxpayer must denote that under “sec 40-60, ITAA 1997” the fall in value of the

depreciating asset begins from its “start time”. In other words, it usually denotes the time

when the company has first made the use of the asset or the taxpayer has installed the asset as

ready for utilization (Shome 2018). The depreciation is generally based on the cost of the

depreciating asset. Most notably, under “Subdiv-40”, the taxpayers are given guidelines to

determine the cost of the asset. Commonly, the cost of depreciating asset not only include the

price that paid at the time of purchase but also takes into the account the incidental cost

involved for delivery and installation. In addition to this, if any other minor outgoings that is

occurred while rearranging the plant then it is also included under the cost base.

Most importantly under the “sec 40-30, ITAA 1997” the depreciating asset is

regarded as the asset that only has limited useful life or usage. These assets are expected to

fall in value over their time of usage. Under “sec 45-40, ITAA 1997” plant usually includes

the machinery, tools or rolling stock (Brabazon 2019). The ordinary meaning of plant was

depreciating asset. Mentioning the judgement of “Wangaratta Woollen Mills Ltd v FCT

(1969)” the CNC machine satisfies the definition plant because the machine has the limited

useful life. The machine is also anticipated to fall in value based on the usage over the years.

Referring “sec 40.25 (1), ITAA 1997” John is permitted to deduct the sum which is

equal to the sum of decline in value of machine during the income year of the depreciating

asset. This is because under “sec 40.25 (2), ITAA 1997” John has held the CNC machine all

through the year for taxable purpose (Sadiq 2019). With regard to sec “Subdivision 40-C” to

compute cost base of machine for claiming capital allowance of the depreciating asset with

the first element under “sec 40.180 (1)”, it would include the purchase price that is paid by

John to acquire the CNC machine (Shome 2018).

Discussion of Second Element of cost base of CNC Machine and its start time:

The taxpayer must denote that under “sec 40-60, ITAA 1997” the fall in value of the

depreciating asset begins from its “start time”. In other words, it usually denotes the time

when the company has first made the use of the asset or the taxpayer has installed the asset as

ready for utilization (Shome 2018). The depreciation is generally based on the cost of the

depreciating asset. Most notably, under “Subdiv-40”, the taxpayers are given guidelines to

determine the cost of the asset. Commonly, the cost of depreciating asset not only include the

price that paid at the time of purchase but also takes into the account the incidental cost

involved for delivery and installation. In addition to this, if any other minor outgoings that is

occurred while rearranging the plant then it is also included under the cost base.

Most importantly under the “sec 40-30, ITAA 1997” the depreciating asset is

regarded as the asset that only has limited useful life or usage. These assets are expected to

fall in value over their time of usage. Under “sec 45-40, ITAA 1997” plant usually includes

the machinery, tools or rolling stock (Brabazon 2019). The ordinary meaning of plant was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

explained in the Australian case of “Wangaratta Woollen Mills Ltd v FCT (1969)”, where

the law court held a structure having a form of dye house was treated as a plant, in contrary to

the common circumstances with building structures. On the other hand “sec 40.190” is

associated with the second element. This widely takes into account the delivery charges paid,

expenses incurred for installation and capital improvements that is made to the asset.

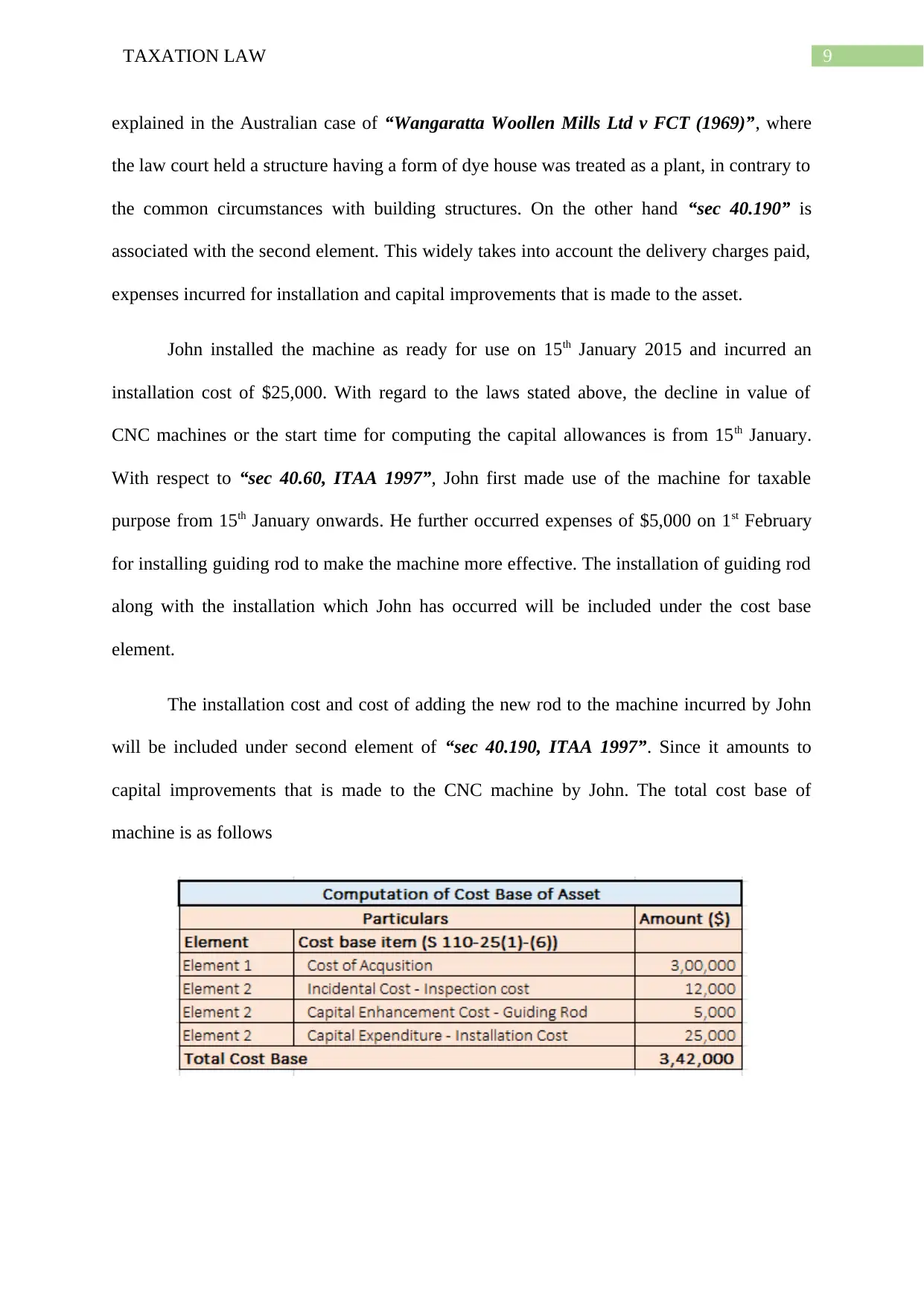

John installed the machine as ready for use on 15th January 2015 and incurred an

installation cost of $25,000. With regard to the laws stated above, the decline in value of

CNC machines or the start time for computing the capital allowances is from 15th January.

With respect to “sec 40.60, ITAA 1997”, John first made use of the machine for taxable

purpose from 15th January onwards. He further occurred expenses of $5,000 on 1st February

for installing guiding rod to make the machine more effective. The installation of guiding rod

along with the installation which John has occurred will be included under the cost base

element.

The installation cost and cost of adding the new rod to the machine incurred by John

will be included under second element of “sec 40.190, ITAA 1997”. Since it amounts to

capital improvements that is made to the CNC machine by John. The total cost base of

machine is as follows

explained in the Australian case of “Wangaratta Woollen Mills Ltd v FCT (1969)”, where

the law court held a structure having a form of dye house was treated as a plant, in contrary to

the common circumstances with building structures. On the other hand “sec 40.190” is

associated with the second element. This widely takes into account the delivery charges paid,

expenses incurred for installation and capital improvements that is made to the asset.

John installed the machine as ready for use on 15th January 2015 and incurred an

installation cost of $25,000. With regard to the laws stated above, the decline in value of

CNC machines or the start time for computing the capital allowances is from 15th January.

With respect to “sec 40.60, ITAA 1997”, John first made use of the machine for taxable

purpose from 15th January onwards. He further occurred expenses of $5,000 on 1st February

for installing guiding rod to make the machine more effective. The installation of guiding rod

along with the installation which John has occurred will be included under the cost base

element.

The installation cost and cost of adding the new rod to the machine incurred by John

will be included under second element of “sec 40.190, ITAA 1997”. Since it amounts to

capital improvements that is made to the CNC machine by John. The total cost base of

machine is as follows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Conclusion:

Decisively, John will be allowed to claim the deduction under “sec 40.25 (1), ITAA

1997” for the amount that is equal to the fall in value during the income year of CNC

machine which he had held for taxable purpose.

Conclusion:

Decisively, John will be allowed to claim the deduction under “sec 40.25 (1), ITAA

1997” for the amount that is equal to the fall in value during the income year of CNC

machine which he had held for taxable purpose.

11TAXATION LAW

References:

Anderson, E., 2019. Testamentary trusts: The need for integrity, effectiveness and

quality. Tax Specialist, 22(3), p.115.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design. Cambridge University Press.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Frecknall-Hughes, J., 2014. The theory, principles and management of taxation: An

introduction. Routledge.

Gashenko, I.V., Zima, Y.S. and Davidyan, A.V., 2019. Principles and Methods of Taxation.

In Optimization of the Taxation System: Preconditions, Tendencies and Perspectives (pp. 33-

39). Springer, Cham.

Herdegen, M., 2016. Principles of international economic law. Oxford University Press.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of taxation for business and investment

planning. McGraw-Hill Higher Education.

Keen, M. and Mullins, P., 2016. International corporate taxation and the extractive industries:

Principles, practice, problems. In International Taxation and the Extractive Industries (pp.

27-57). Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Osborn, A., 2018. Young lawyers: Tax and the young (non-tax) lawyer. Bulletin (Law

Society of South Australia), 40(5), p.20.

Qureshi, A.H. and Kumar, A., 2019. The public international law of taxation: text, cases and

materials. Kluwer Law International BV.

References:

Anderson, E., 2019. Testamentary trusts: The need for integrity, effectiveness and

quality. Tax Specialist, 22(3), p.115.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design. Cambridge University Press.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Frecknall-Hughes, J., 2014. The theory, principles and management of taxation: An

introduction. Routledge.

Gashenko, I.V., Zima, Y.S. and Davidyan, A.V., 2019. Principles and Methods of Taxation.

In Optimization of the Taxation System: Preconditions, Tendencies and Perspectives (pp. 33-

39). Springer, Cham.

Herdegen, M., 2016. Principles of international economic law. Oxford University Press.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of taxation for business and investment

planning. McGraw-Hill Higher Education.

Keen, M. and Mullins, P., 2016. International corporate taxation and the extractive industries:

Principles, practice, problems. In International Taxation and the Extractive Industries (pp.

27-57). Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Osborn, A., 2018. Young lawyers: Tax and the young (non-tax) lawyer. Bulletin (Law

Society of South Australia), 40(5), p.20.

Qureshi, A.H. and Kumar, A., 2019. The public international law of taxation: text, cases and

materials. Kluwer Law International BV.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.