Taxation Law Assignment: Income Tax, CGT and Deductions Analysis

VerifiedAdded on 2023/01/11

|20

|4763

|41

Homework Assignment

AI Summary

This taxation law assignment provides detailed answers to several questions covering various aspects of Australian taxation. The assignment begins with an overview of tax rulings, tax offsets, and the top tax rates for Australian residents. It then delves into capital gains tax (CGT), including exemptions and events, and the formula for income tax calculation. The assignment further explores specific scenarios related to tax deductions, including interest on loans, apportioned expenses, child care expenditure, losses from theft, and preliminary expenses. Several case studies are analyzed, referencing relevant legislation and court decisions to support the answers. Furthermore, the assignment examines CGT events F2 and B1, and partial exemptions for property used for both income generation and personal purposes. The assignment concludes with a summary of the key concepts discussed and relevant references.

Running head: Taxation Law

Taxation Law

Name of the Student

Name of the University

Author Note

Taxation Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Taxation Law

Table of Contents

Question No 1............................................................................................................................4

Answer 1A:............................................................................................................................4

Answer 1B:.............................................................................................................................4

Answer 1C:.............................................................................................................................4

Answer 1D:............................................................................................................................4

Answer 1E:.............................................................................................................................5

Answer 1F:.............................................................................................................................5

Answer to 1G:........................................................................................................................5

Answer to 1H:........................................................................................................................6

Answer to 1I:..........................................................................................................................6

Question No 2............................................................................................................................7

Answer to 2A:........................................................................................................................7

Answer to 2B:........................................................................................................................7

Answer to 2C:........................................................................................................................8

Answer to 2D:........................................................................................................................9

Answer to 2E:.........................................................................................................................9

Question No 3..........................................................................................................................10

Answer to 3A:......................................................................................................................10

Answer to 3B:......................................................................................................................10

Answer to 3C:......................................................................................................................11

Taxation Law

Table of Contents

Question No 1............................................................................................................................4

Answer 1A:............................................................................................................................4

Answer 1B:.............................................................................................................................4

Answer 1C:.............................................................................................................................4

Answer 1D:............................................................................................................................4

Answer 1E:.............................................................................................................................5

Answer 1F:.............................................................................................................................5

Answer to 1G:........................................................................................................................5

Answer to 1H:........................................................................................................................6

Answer to 1I:..........................................................................................................................6

Question No 2............................................................................................................................7

Answer to 2A:........................................................................................................................7

Answer to 2B:........................................................................................................................7

Answer to 2C:........................................................................................................................8

Answer to 2D:........................................................................................................................9

Answer to 2E:.........................................................................................................................9

Question No 3..........................................................................................................................10

Answer to 3A:......................................................................................................................10

Answer to 3B:......................................................................................................................10

Answer to 3C:......................................................................................................................11

2

Taxation Law

Answer to 3D:......................................................................................................................11

Question No 4..........................................................................................................................12

Answer to 4A.......................................................................................................................12

Answer to 4B:......................................................................................................................13

Answer to 4C:......................................................................................................................13

Answer to 4D:......................................................................................................................13

Answer to 4E........................................................................................................................14

Question No 5..........................................................................................................................14

Issues:...................................................................................................................................14

Laws:....................................................................................................................................14

Applications:........................................................................................................................16

Conclusion:..........................................................................................................................16

Reference..................................................................................................................................17

Taxation Law

Answer to 3D:......................................................................................................................11

Question No 4..........................................................................................................................12

Answer to 4A.......................................................................................................................12

Answer to 4B:......................................................................................................................13

Answer to 4C:......................................................................................................................13

Answer to 4D:......................................................................................................................13

Answer to 4E........................................................................................................................14

Question No 5..........................................................................................................................14

Issues:...................................................................................................................................14

Laws:....................................................................................................................................14

Applications:........................................................................................................................16

Conclusion:..........................................................................................................................16

Reference..................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Taxation Law

Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Taxation Law

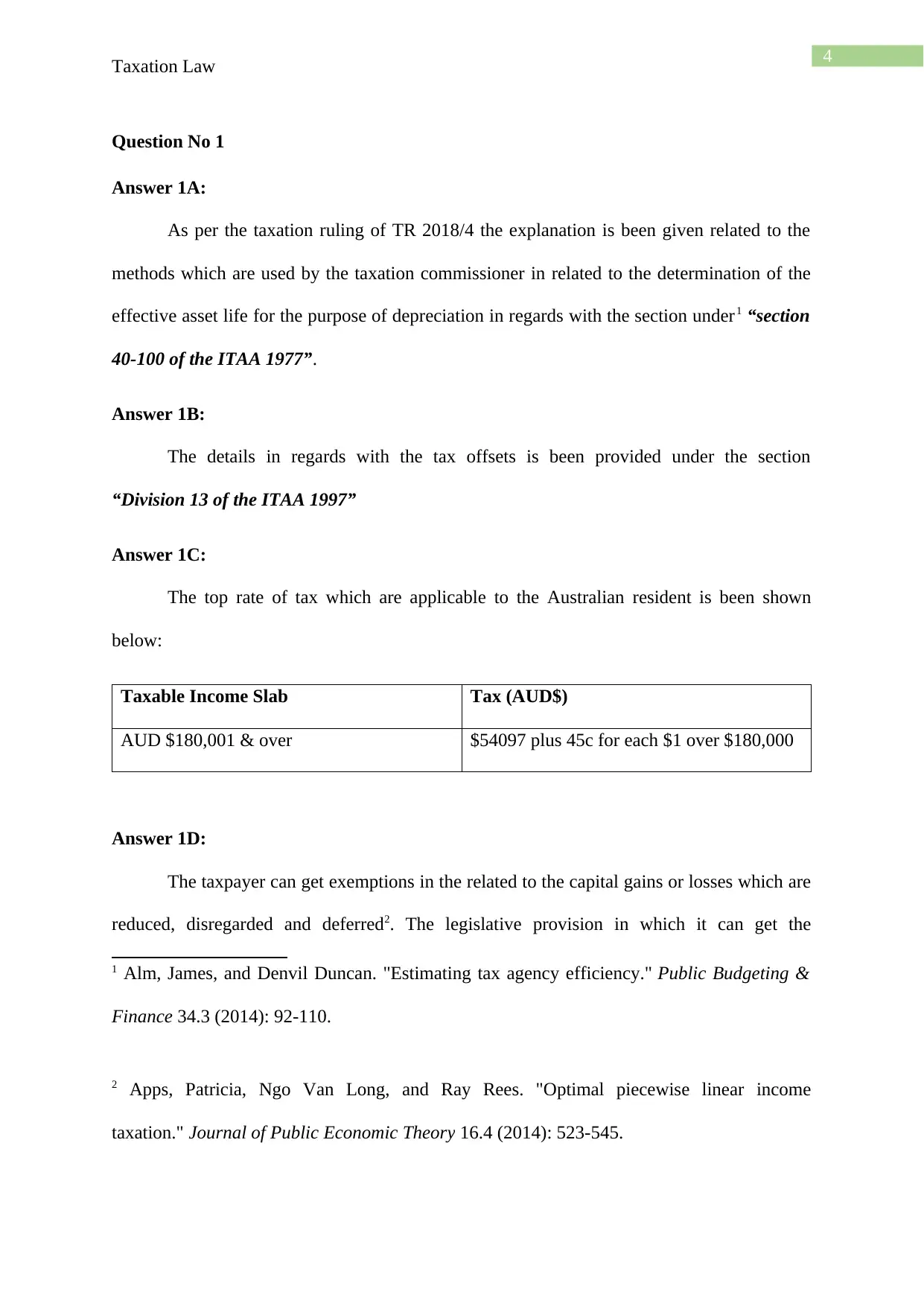

Question No 1

Answer 1A:

As per the taxation ruling of TR 2018/4 the explanation is been given related to the

methods which are used by the taxation commissioner in related to the determination of the

effective asset life for the purpose of depreciation in regards with the section under1 “section

40-100 of the ITAA 1977”.

Answer 1B:

The details in regards with the tax offsets is been provided under the section

“Division 13 of the ITAA 1997”

Answer 1C:

The top rate of tax which are applicable to the Australian resident is been shown

below:

Taxable Income Slab Tax (AUD$)

AUD $180,001 & over $54097 plus 45c for each $1 over $180,000

Answer 1D:

The taxpayer can get exemptions in the related to the capital gains or losses which are

reduced, disregarded and deferred2. The legislative provision in which it can get the

1 Alm, James, and Denvil Duncan. "Estimating tax agency efficiency." Public Budgeting &

Finance 34.3 (2014): 92-110.

2 Apps, Patricia, Ngo Van Long, and Ray Rees. "Optimal piecewise linear income

taxation." Journal of Public Economic Theory 16.4 (2014): 523-545.

Taxation Law

Question No 1

Answer 1A:

As per the taxation ruling of TR 2018/4 the explanation is been given related to the

methods which are used by the taxation commissioner in related to the determination of the

effective asset life for the purpose of depreciation in regards with the section under1 “section

40-100 of the ITAA 1977”.

Answer 1B:

The details in regards with the tax offsets is been provided under the section

“Division 13 of the ITAA 1997”

Answer 1C:

The top rate of tax which are applicable to the Australian resident is been shown

below:

Taxable Income Slab Tax (AUD$)

AUD $180,001 & over $54097 plus 45c for each $1 over $180,000

Answer 1D:

The taxpayer can get exemptions in the related to the capital gains or losses which are

reduced, disregarded and deferred2. The legislative provision in which it can get the

1 Alm, James, and Denvil Duncan. "Estimating tax agency efficiency." Public Budgeting &

Finance 34.3 (2014): 92-110.

2 Apps, Patricia, Ngo Van Long, and Ray Rees. "Optimal piecewise linear income

taxation." Journal of Public Economic Theory 16.4 (2014): 523-545.

5

Taxation Law

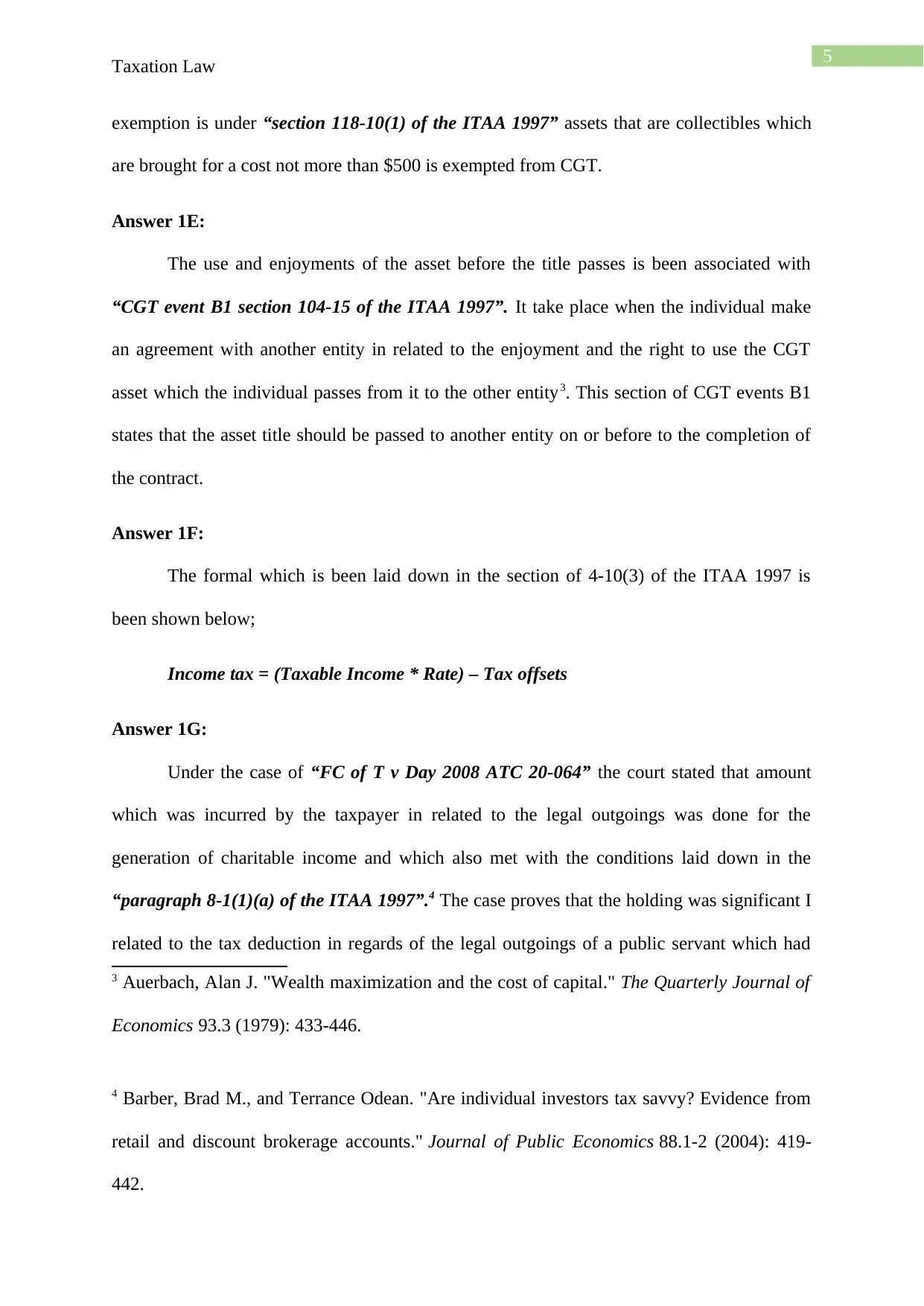

exemption is under “section 118-10(1) of the ITAA 1997” assets that are collectibles which

are brought for a cost not more than $500 is exempted from CGT.

Answer 1E:

The use and enjoyments of the asset before the title passes is been associated with

“CGT event B1 section 104-15 of the ITAA 1997”. It take place when the individual make

an agreement with another entity in related to the enjoyment and the right to use the CGT

asset which the individual passes from it to the other entity3. This section of CGT events B1

states that the asset title should be passed to another entity on or before to the completion of

the contract.

Answer 1F:

The formal which is been laid down in the section of 4-10(3) of the ITAA 1997 is

been shown below;

Income tax = (Taxable Income * Rate) – Tax offsets

Answer 1G:

Under the case of “FC of T v Day 2008 ATC 20-064” the court stated that amount

which was incurred by the taxpayer in related to the legal outgoings was done for the

generation of charitable income and which also met with the conditions laid down in the

“paragraph 8-1(1)(a) of the ITAA 1997”.4 The case proves that the holding was significant I

related to the tax deduction in regards of the legal outgoings of a public servant which had

3 Auerbach, Alan J. "Wealth maximization and the cost of capital." The Quarterly Journal of

Economics 93.3 (1979): 433-446.

4 Barber, Brad M., and Terrance Odean. "Are individual investors tax savvy? Evidence from

retail and discount brokerage accounts." Journal of Public Economics 88.1-2 (2004): 419-

442.

Taxation Law

exemption is under “section 118-10(1) of the ITAA 1997” assets that are collectibles which

are brought for a cost not more than $500 is exempted from CGT.

Answer 1E:

The use and enjoyments of the asset before the title passes is been associated with

“CGT event B1 section 104-15 of the ITAA 1997”. It take place when the individual make

an agreement with another entity in related to the enjoyment and the right to use the CGT

asset which the individual passes from it to the other entity3. This section of CGT events B1

states that the asset title should be passed to another entity on or before to the completion of

the contract.

Answer 1F:

The formal which is been laid down in the section of 4-10(3) of the ITAA 1997 is

been shown below;

Income tax = (Taxable Income * Rate) – Tax offsets

Answer 1G:

Under the case of “FC of T v Day 2008 ATC 20-064” the court stated that amount

which was incurred by the taxpayer in related to the legal outgoings was done for the

generation of charitable income and which also met with the conditions laid down in the

“paragraph 8-1(1)(a) of the ITAA 1997”.4 The case proves that the holding was significant I

related to the tax deduction in regards of the legal outgoings of a public servant which had

3 Auerbach, Alan J. "Wealth maximization and the cost of capital." The Quarterly Journal of

Economics 93.3 (1979): 433-446.

4 Barber, Brad M., and Terrance Odean. "Are individual investors tax savvy? Evidence from

retail and discount brokerage accounts." Journal of Public Economics 88.1-2 (2004): 419-

442.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Taxation Law

incurred the charges for defend the conduct which take places in daily activities5. The

deduction which was allowed in related to the legal expenditure was allowed to the taxpayer

under the legislative provision of “section 8-1, ITAA 1997” which was occurred him in the

income year 2002 for putting the defending the disciplinary actions that will be imposed

against the taxpayer by the employer

Answer 1H:

The assess of the burden of the taxation is done by the average rate of tax whereas the

marginal rate of tax which assesses the effect of the tax upon the incentive save, earn, invest

or spend6. The overall sum of tax is been divided by the total income which is been represent

by the average rate of tax and the incremental tax which is been paid upon the increased

income is been represent by the marginal rate of tax.

Answer 1I:

The tax which is been imposed upon the purchase of goods and services are regarded

as the expenditure tax which is also consider as the consumption tax. It can be further

referred to the system of taxation where the tax is been levied upon the people in the

proportion of how they consume the product instead of how much amount they add to the

economy.

5 Blunden, Hazel. "Discourses around negative gearing of investment properties in

Australia." Housing Studies 31.3 (2016): 340-357.

6 Ato.gov.au. "Elasticsearch." Ato.gov.au. N.p., 2019. Web. 1 May 2019.

Taxation Law

incurred the charges for defend the conduct which take places in daily activities5. The

deduction which was allowed in related to the legal expenditure was allowed to the taxpayer

under the legislative provision of “section 8-1, ITAA 1997” which was occurred him in the

income year 2002 for putting the defending the disciplinary actions that will be imposed

against the taxpayer by the employer

Answer 1H:

The assess of the burden of the taxation is done by the average rate of tax whereas the

marginal rate of tax which assesses the effect of the tax upon the incentive save, earn, invest

or spend6. The overall sum of tax is been divided by the total income which is been represent

by the average rate of tax and the incremental tax which is been paid upon the increased

income is been represent by the marginal rate of tax.

Answer 1I:

The tax which is been imposed upon the purchase of goods and services are regarded

as the expenditure tax which is also consider as the consumption tax. It can be further

referred to the system of taxation where the tax is been levied upon the people in the

proportion of how they consume the product instead of how much amount they add to the

economy.

5 Blunden, Hazel. "Discourses around negative gearing of investment properties in

Australia." Housing Studies 31.3 (2016): 340-357.

6 Ato.gov.au. "Elasticsearch." Ato.gov.au. N.p., 2019. Web. 1 May 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Taxation Law

Question No 2

Answer to 2A:

As per the Australian Taxation Office the individual can able to claim the deduction

for expenses which is been occurred for the interest on loan which getting the assessable

income7. Under the “section 8-1, ITAA 1997” it state that the individual can claim the

exemption in regards of the interest on loan which is been taken for the purpose of business

which is consider as deduction allowable.

The interest of the loan which is occurred by the Brent was for the payment of the

wages to the employees. As per the “Amalgamated Zinc Ltd v FC of T (1935)” it founded

that the interest on loan which was occurred by the Brent was for generating the taxable

earnings. Under the “section 8-1, ITAA 1997” allowable deduction will allowed to Brent in

regards with the interest on loan.

Answer to 2B:

There are some situations in which the losses or the outgoings is been required to be

apportioned or the partially deductible8. As per the court “Ronpibon Tin NL v FC of T

(1949)”

Said to the commissioner that it should determine the portion of the expenses which are

incurred in gaining the assessable income9. When the individual had some expenses in both

the private and work purpose than the taxpayer is been allowed for the work purpose only.

7 Carling, Robert G. Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies, 2015.

8 Collins, Julie H., and Deen Kemsley. "Capital gains and dividend taxes in firm valuation:

evidence of triple taxation." The Accounting Review 75.4 (2000): 405-427.

Taxation Law

Question No 2

Answer to 2A:

As per the Australian Taxation Office the individual can able to claim the deduction

for expenses which is been occurred for the interest on loan which getting the assessable

income7. Under the “section 8-1, ITAA 1997” it state that the individual can claim the

exemption in regards of the interest on loan which is been taken for the purpose of business

which is consider as deduction allowable.

The interest of the loan which is occurred by the Brent was for the payment of the

wages to the employees. As per the “Amalgamated Zinc Ltd v FC of T (1935)” it founded

that the interest on loan which was occurred by the Brent was for generating the taxable

earnings. Under the “section 8-1, ITAA 1997” allowable deduction will allowed to Brent in

regards with the interest on loan.

Answer to 2B:

There are some situations in which the losses or the outgoings is been required to be

apportioned or the partially deductible8. As per the court “Ronpibon Tin NL v FC of T

(1949)”

Said to the commissioner that it should determine the portion of the expenses which are

incurred in gaining the assessable income9. When the individual had some expenses in both

the private and work purpose than the taxpayer is been allowed for the work purpose only.

7 Carling, Robert G. Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies, 2015.

8 Collins, Julie H., and Deen Kemsley. "Capital gains and dividend taxes in firm valuation:

evidence of triple taxation." The Accounting Review 75.4 (2000): 405-427.

8

Taxation Law

Julie had got the mobile phone expenses as $500 in which 60% of the calls were made

for the work purpose. As per the “Ronpibon Tin NL v FC of T (1949)” Julie can get the

exemption as per 60% as it used the call for the office purpose and the rest 40% which was

consume for the personal purpose is will not be allowed as deduction under the section

“section 8-1(2)”

Answer to 2C:

As per the “section 8-1, ITAA 1997” there is no deduction in respect of the child care

expenditure10. As per the case “Lodge v Fc of T (1972)” it was founded that the individual is

not permitted for any deduction regarding the child care expenses while attending for work as

because it was not incidental or relevant in the way of producing with the taxable income.

As per the “section 8-1 (2) (b) of the ITAA 1997” it does not satisfy their criteria as

the baby sitter expenses which was occurred by the Sally for seeing her child as it is non-

deductible expenses because of it is a domestic or private in nature. As it does not meet the

requirement so it will not be allowed as deduction.

Answer to 2D:

The “Section 8-1, ITAA 1997” is for both the losses and outgoings which are been

incurred by the individual taxpayers11. As per the court in the case of “Charles Moore & Co

9 Carnegie, Garry. Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge, 2014.

10 Findlay, Christopher, and Ross Garnaut. The political economy of manufacturing

protection: Experiences of ASEAN and Australia. Routledge, 2017.

11 Plaxico, James S., and Darrel D. Kletke. "The value of unrealized farm land capital

gains." American Journal of Agricultural Economics 61.2 (1979): 327-330.

Taxation Law

Julie had got the mobile phone expenses as $500 in which 60% of the calls were made

for the work purpose. As per the “Ronpibon Tin NL v FC of T (1949)” Julie can get the

exemption as per 60% as it used the call for the office purpose and the rest 40% which was

consume for the personal purpose is will not be allowed as deduction under the section

“section 8-1(2)”

Answer to 2C:

As per the “section 8-1, ITAA 1997” there is no deduction in respect of the child care

expenditure10. As per the case “Lodge v Fc of T (1972)” it was founded that the individual is

not permitted for any deduction regarding the child care expenses while attending for work as

because it was not incidental or relevant in the way of producing with the taxable income.

As per the “section 8-1 (2) (b) of the ITAA 1997” it does not satisfy their criteria as

the baby sitter expenses which was occurred by the Sally for seeing her child as it is non-

deductible expenses because of it is a domestic or private in nature. As it does not meet the

requirement so it will not be allowed as deduction.

Answer to 2D:

The “Section 8-1, ITAA 1997” is for both the losses and outgoings which are been

incurred by the individual taxpayers11. As per the court in the case of “Charles Moore & Co

9 Carnegie, Garry. Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge, 2014.

10 Findlay, Christopher, and Ross Garnaut. The political economy of manufacturing

protection: Experiences of ASEAN and Australia. Routledge, 2017.

11 Plaxico, James S., and Darrel D. Kletke. "The value of unrealized farm land capital

gains." American Journal of Agricultural Economics 61.2 (1979): 327-330.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Taxation Law

(WA) Pty Ltd v FC of T (1956)” it allowed the individual the deduction in related to the loss

which was arise from the theft of day’s earning which was there at the time of transit towards

the bank.

Under the legislative section “section 8-1, ITAA 1997” The individual Jerry can able

to claim deduction for the goods which are long term employee stole. The loss which was

associated and it was incurred which is done by carrying the business and help in generating

the chargeable earnings.

Answer to 2E:

As per the section “section 8-1, ITAA 1997” the outgoings or the losses which are

preliminary in the beginning of revenue generating acts which did not occurred in the course

of the activity are not treated as items for deductions12. As per the case “Maddalena v FCT

(1971)” as the outgoing is occurred in the getting of new job which was not doing in the

course of the producing the taxable income since it occur at a point which was very soon and

that is the reason it is not termed as deduction under “section 8-1”

As per the “section 8-1, ITAA 1997” as the outgoings have been occurred as per the

contest in the local government election which was the preliminary to the beginning of the

revenue of producing so it does not occurred in the gaining or producing the income and so it

is not allowed as deduction13.

12 Moretto, Nicole, et al. "Yes, the government should tax soft drinks: findings from a

citizens’ jury in Australia." International journal of environmental research and public

health 11.3 (2014): 2456-2471.

13 Pomerleau, Kyle, and Alan Cole. "International tax competitiveness index 2015." Tax

Foundation (2015).

Taxation Law

(WA) Pty Ltd v FC of T (1956)” it allowed the individual the deduction in related to the loss

which was arise from the theft of day’s earning which was there at the time of transit towards

the bank.

Under the legislative section “section 8-1, ITAA 1997” The individual Jerry can able

to claim deduction for the goods which are long term employee stole. The loss which was

associated and it was incurred which is done by carrying the business and help in generating

the chargeable earnings.

Answer to 2E:

As per the section “section 8-1, ITAA 1997” the outgoings or the losses which are

preliminary in the beginning of revenue generating acts which did not occurred in the course

of the activity are not treated as items for deductions12. As per the case “Maddalena v FCT

(1971)” as the outgoing is occurred in the getting of new job which was not doing in the

course of the producing the taxable income since it occur at a point which was very soon and

that is the reason it is not termed as deduction under “section 8-1”

As per the “section 8-1, ITAA 1997” as the outgoings have been occurred as per the

contest in the local government election which was the preliminary to the beginning of the

revenue of producing so it does not occurred in the gaining or producing the income and so it

is not allowed as deduction13.

12 Moretto, Nicole, et al. "Yes, the government should tax soft drinks: findings from a

citizens’ jury in Australia." International journal of environmental research and public

health 11.3 (2014): 2456-2471.

13 Pomerleau, Kyle, and Alan Cole. "International tax competitiveness index 2015." Tax

Foundation (2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Taxation Law

Question No 3

Answer to 3A:

The section of “CGT event F2” is applicable for the individual taxpayers in regards

of the extents, renews and grants of the long term lease. This section is applied to all the

owner of the underlying land and also to the individual who had granted with the sublease.

As per the case it can be seen that the Andy is the owner of the land grants of a lease of five

year term to Brian at a premium of $5000. This effected in the “CGT event” so as a result of

it Andy could not able to get the 50%CGT discount since the terms are not applicable to CGT

event F2.

Answer to 3B:

As per the Australian Tax Office a “CGT event B1” state that the use of the land is

been mainly acquired by the new owners. As per the point of view, it state that when the new

owner acquired the land than only it can use the right of the use and enjoyment of the land

and when it permitted to the profit and rents14. So as per the case given the CGT event B1

attract so the John can able to claim the 50% discount as it exchange the $40000 Farm Ltd in

order to purchase the 100-acre farm for the sum of $80,0000 so it can able to claim the

deductions.

Answer to 3C:

As per the ATO, if the taxpayers is not using the property as a whole for the full

period of ownership but used this as generating the income than in such a case it should able

14 Pomerleau, Kyle, and Andrew Lundeen. "International tax competitiveness

index." Washington: Tax Foundation (2014).

Taxation Law

Question No 3

Answer to 3A:

The section of “CGT event F2” is applicable for the individual taxpayers in regards

of the extents, renews and grants of the long term lease. This section is applied to all the

owner of the underlying land and also to the individual who had granted with the sublease.

As per the case it can be seen that the Andy is the owner of the land grants of a lease of five

year term to Brian at a premium of $5000. This effected in the “CGT event” so as a result of

it Andy could not able to get the 50%CGT discount since the terms are not applicable to CGT

event F2.

Answer to 3B:

As per the Australian Tax Office a “CGT event B1” state that the use of the land is

been mainly acquired by the new owners. As per the point of view, it state that when the new

owner acquired the land than only it can use the right of the use and enjoyment of the land

and when it permitted to the profit and rents14. So as per the case given the CGT event B1

attract so the John can able to claim the 50% discount as it exchange the $40000 Farm Ltd in

order to purchase the 100-acre farm for the sum of $80,0000 so it can able to claim the

deductions.

Answer to 3C:

As per the ATO, if the taxpayers is not using the property as a whole for the full

period of ownership but used this as generating the income than in such a case it should able

14 Pomerleau, Kyle, and Andrew Lundeen. "International tax competitiveness

index." Washington: Tax Foundation (2014).

11

Taxation Law

to get a partial exemption is been allowed to the taxpayer15. As the property was bought by

both Jamie and Olivia and it was rented for a period of two years. After they acquire the

property they let out for generating the income and also used the same in for the main

residence before selling in 2018. As they used it for generating income so Jamie and Olivia

can able to claim 50% CGT discount form the net amount of capital gain tax.

Answer to 3D:

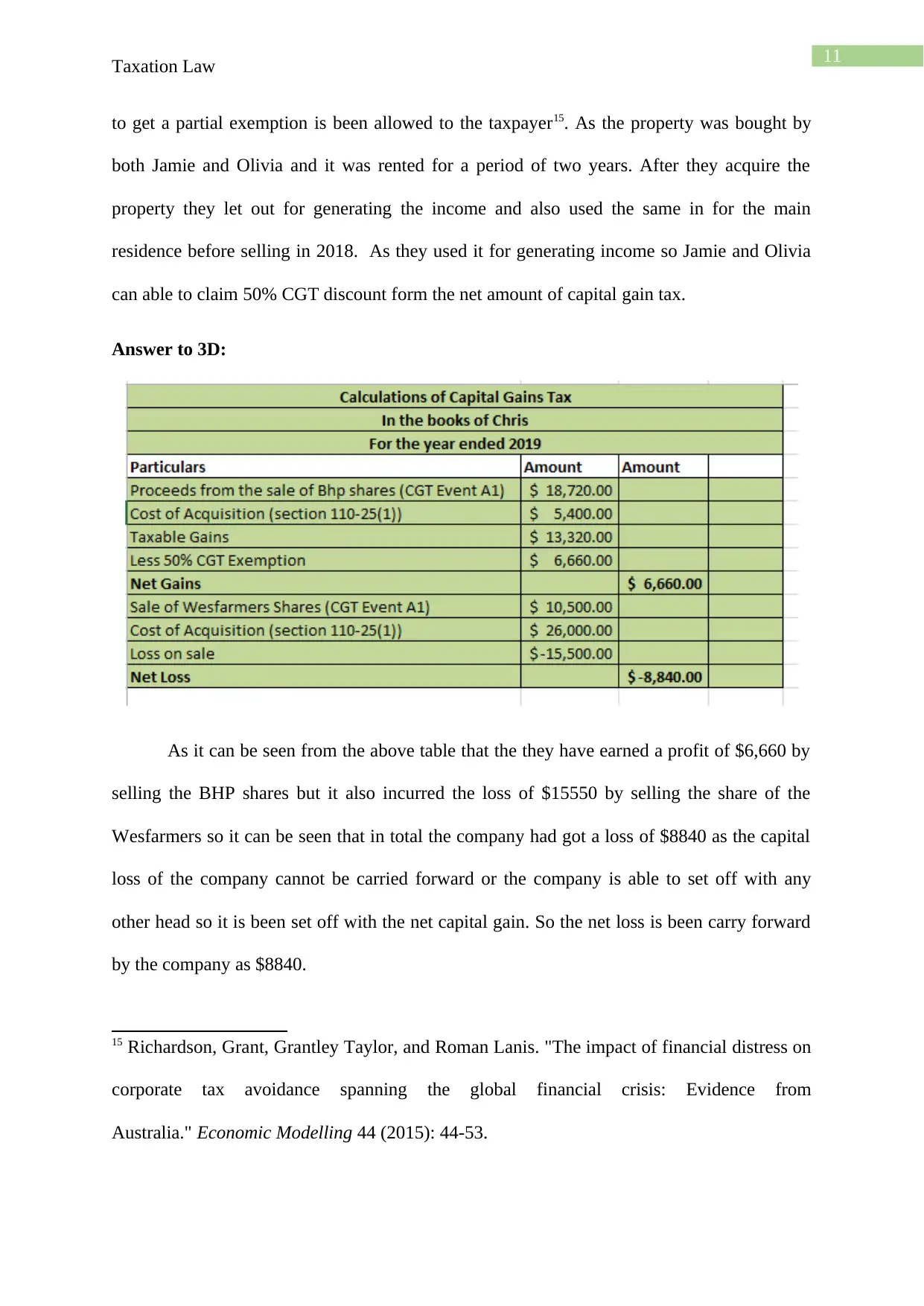

As it can be seen from the above table that the they have earned a profit of $6,660 by

selling the BHP shares but it also incurred the loss of $15550 by selling the share of the

Wesfarmers so it can be seen that in total the company had got a loss of $8840 as the capital

loss of the company cannot be carried forward or the company is able to set off with any

other head so it is been set off with the net capital gain. So the net loss is been carry forward

by the company as $8840.

15 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

Taxation Law

to get a partial exemption is been allowed to the taxpayer15. As the property was bought by

both Jamie and Olivia and it was rented for a period of two years. After they acquire the

property they let out for generating the income and also used the same in for the main

residence before selling in 2018. As they used it for generating income so Jamie and Olivia

can able to claim 50% CGT discount form the net amount of capital gain tax.

Answer to 3D:

As it can be seen from the above table that the they have earned a profit of $6,660 by

selling the BHP shares but it also incurred the loss of $15550 by selling the share of the

Wesfarmers so it can be seen that in total the company had got a loss of $8840 as the capital

loss of the company cannot be carried forward or the company is able to set off with any

other head so it is been set off with the net capital gain. So the net loss is been carry forward

by the company as $8840.

15 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

![Taxation Law Assignment - LAWS20060, Semester 1, [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzu%2F803f7afcdaf14edca4b16cd62f859dfd.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.