Taxation Law Assignment: Payroll, Superannuation, and Business Income

VerifiedAdded on 2021/12/29

|7

|643

|277

Homework Assignment

AI Summary

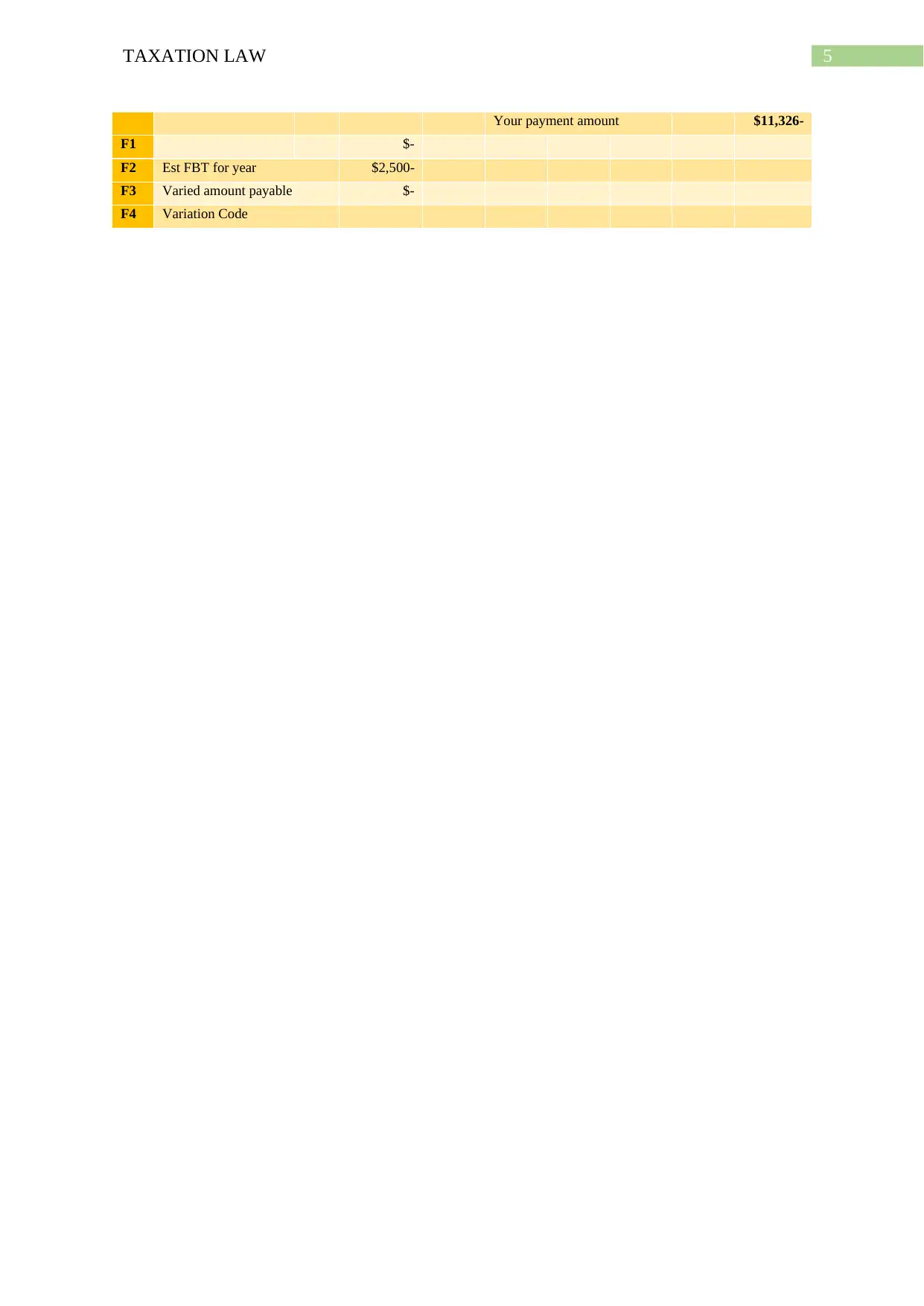

This Taxation Law assignment provides a comprehensive analysis of various tax-related concepts. It begins with the computation of a payroll schedule and the calculation of an employer's Superannuation Guarantee obligations. The assignment then delves into the definition of 'business' under the ITAA 1997, determining the taxability of different income sources, including training payments, prize winnings, and receipts from trade-in assets. Additionally, it examines permissible deductions, referencing relevant case law. The assignment also covers the conditions necessary to meet the requirements of GST, and presents an example of GST calculations and reporting options. Finally, it presents a summary of GST and PAYG calculations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.