Taxation Law: Analyzing Taxable Income, Deductions, and Tax Payable

VerifiedAdded on 2021/12/28

|8

|887

|28

Homework Assignment

AI Summary

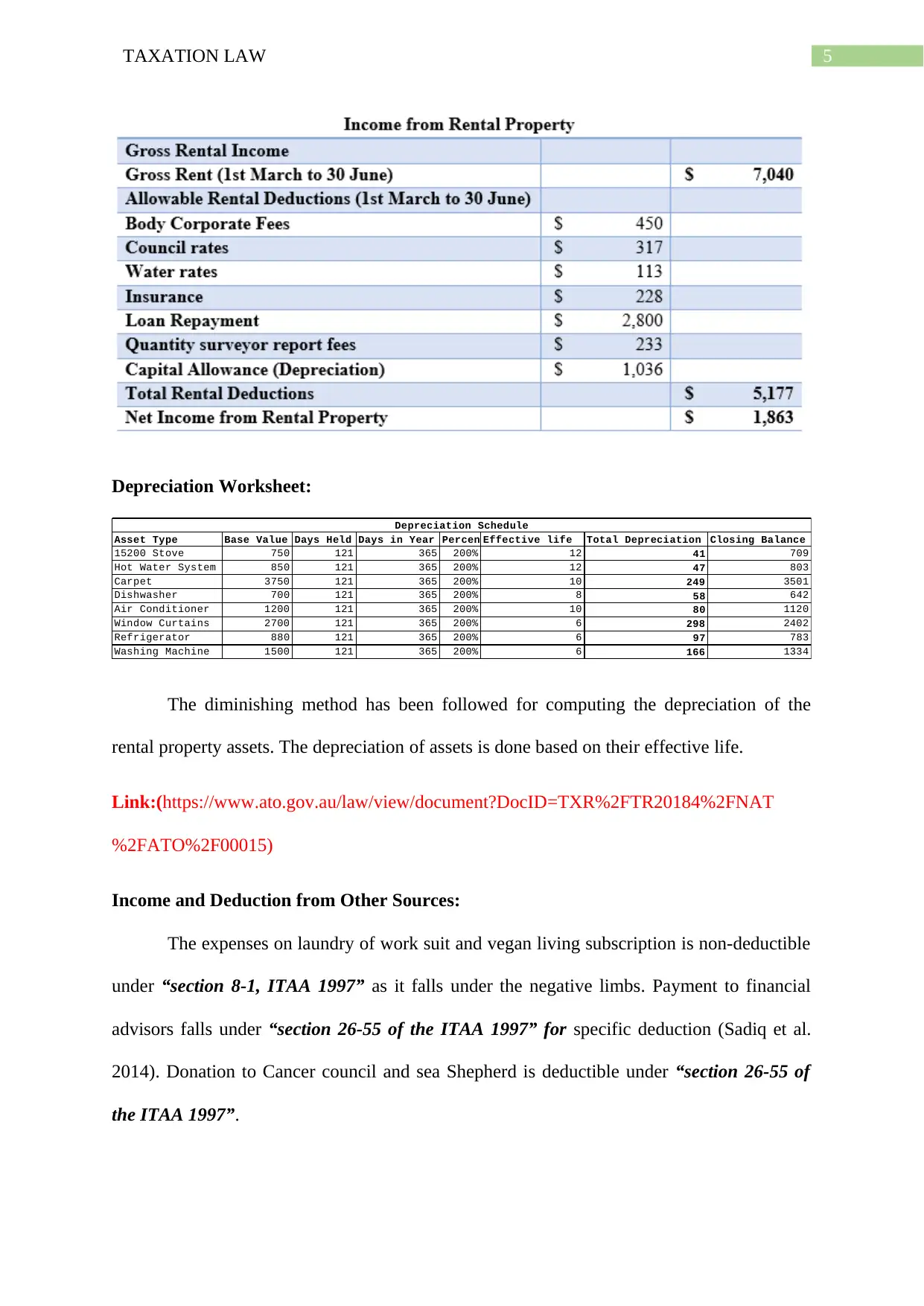

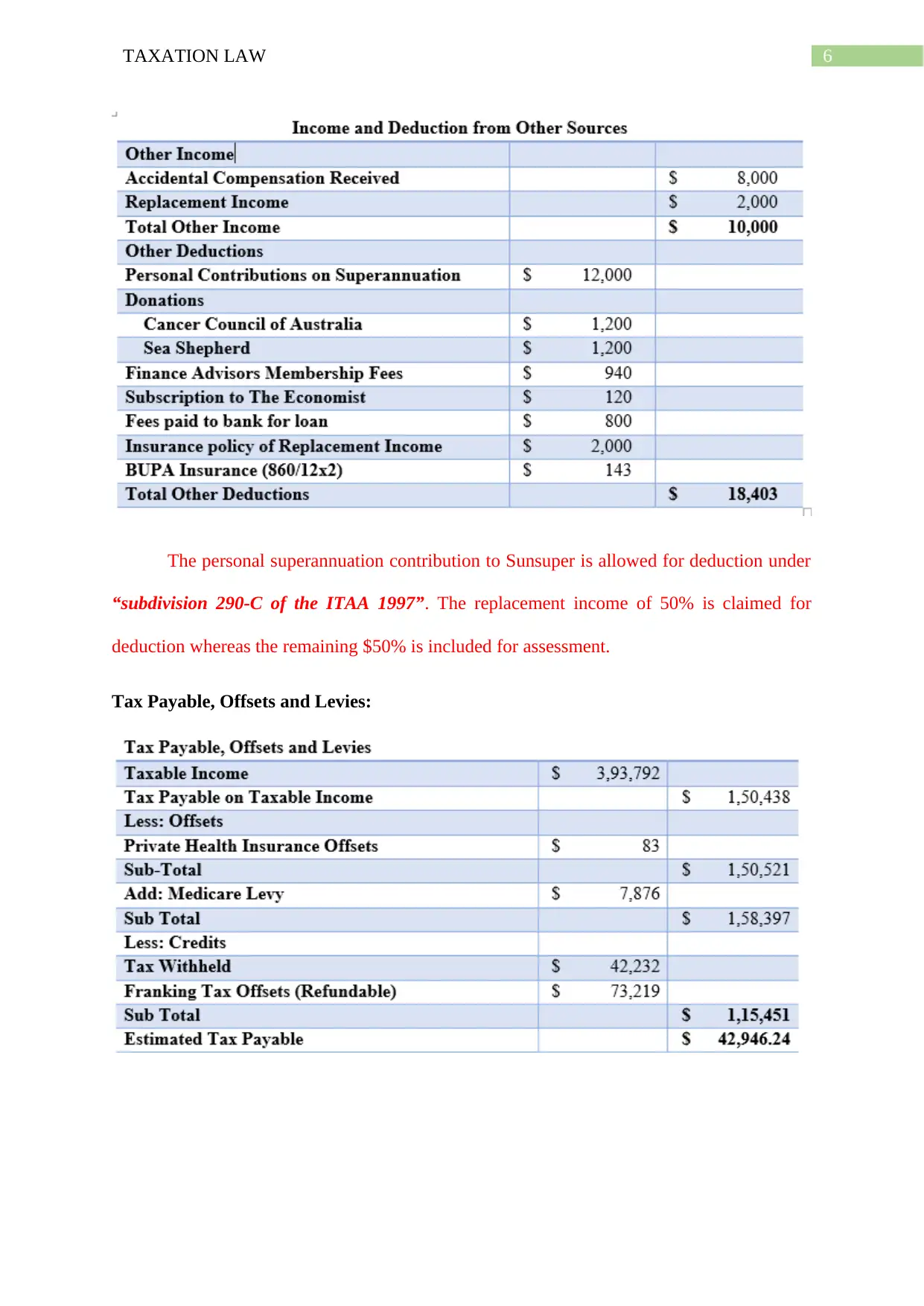

This taxation law assignment presents a detailed analysis of a taxpayer's financial situation, offering insights into taxable income, allowable deductions, and tax liabilities. The assignment includes a letter of advice addressing the taxpayer's gross salary, dividends, and capital gains from the sale of inherited shares. It covers work-related expenses, car expenses, and depreciation of a rental property. The analysis references relevant sections of the ITAA 1997 and ITAA 1936, providing calculations for tax payable, offsets, and levies. The solution also addresses non-deductible expenses and offers a comprehensive overview of the taxpayer's tax obligations. This assignment provides a practical application of taxation law principles, including income assessment, deduction eligibility, and tax calculation, offering a valuable resource for students seeking to understand and apply tax regulations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.