Taxation Law Assignment - University Taxation Law Analysis

VerifiedAdded on 2022/10/04

|21

|4234

|20

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Australian Taxation Law assignment. It meticulously addresses multiple questions, offering detailed answers supported by relevant legislation, including the Income Tax Assessment Act 1997 (ITAA97) and the Income Tax Assessment Act 1936 (ITAA36), as well as referencing Tax Rulings and case law. The assignment covers a range of topics, such as the definition of a small business entity, deductibility of gifts, the top tax rate, capital gains tax, CGT events, tax-free thresholds, ordinary vs. statutory income, Medicare Levy and Medicare Levy Surcharge, and the concept of "usual place of abode". The answers include analysis of self-education expenses like HECS-HELP, travel costs, and book expenses. It also explores the concept of permanent place of abode and its impact on taxation. The assignment is a valuable resource for students studying taxation law, providing insights into various aspects of Australian tax regulations and their practical application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................8

Answer to question 4:...............................................................................................................12

Answer to A:........................................................................................................................12

Answer to B:........................................................................................................................13

Answer to C:........................................................................................................................13

Answer to D:........................................................................................................................14

Answer to question 5:...............................................................................................................15

Answer A:............................................................................................................................15

Answer B:.............................................................................................................................15

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................8

Answer to question 4:...............................................................................................................12

Answer to A:........................................................................................................................12

Answer to B:........................................................................................................................13

Answer to C:........................................................................................................................13

Answer to D:........................................................................................................................14

Answer to question 5:...............................................................................................................15

Answer A:............................................................................................................................15

Answer B:.............................................................................................................................15

2TAXATION LAW

Answer C:.............................................................................................................................16

Answer D:............................................................................................................................16

Answer E:.............................................................................................................................17

References:...............................................................................................................................18

Answer C:.............................................................................................................................16

Answer D:............................................................................................................................16

Answer E:.............................................................................................................................17

References:...............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

The “taxation ruling of TR 2019/1” sets down the views of the commissioner

regarding when an organization commences carrying on the business inside the definition of

small business entity given under the “sec-23, ITRA 1986” as valid from 2015-16 and 2016-

17 income years and “sec-328-110, ITAA 1997”1.

Answer B:

“Division 30 of the ITAA 1997” sets down the rules for the taxpayers to work out the

deduction for certain contributions or gifts made during the year2.

Answer C:

The uppermost marginal tax rate that is levied on the resident for the current income year is

45%.

Answer D:

Car or motorcycle cannot be considered exempted from capital gains tax because they

are treated as the personal use asset under “sec-108-20, ITAA 1997” that is principally kept

or used by taxpayers for their own private use purpose3.

Answer E:

The “CGT event C1” given under the “subsection 104-20 (1), ITAA 1997” happens

when the CGT asset owned by an individual is destroyed or lost4. The time of “CGT event

1 Taxation Ruling TR 2019/01

2 The Income Tax Assessment Act 1997 (Cth), Div 30

3 The Income Tax Assessment Act 1997 (Cth), s.108.20

4 The Income Tax Assessment Act 1997 (Cth), s. 104.20

Answer to question 1:

Answer A:

The “taxation ruling of TR 2019/1” sets down the views of the commissioner

regarding when an organization commences carrying on the business inside the definition of

small business entity given under the “sec-23, ITRA 1986” as valid from 2015-16 and 2016-

17 income years and “sec-328-110, ITAA 1997”1.

Answer B:

“Division 30 of the ITAA 1997” sets down the rules for the taxpayers to work out the

deduction for certain contributions or gifts made during the year2.

Answer C:

The uppermost marginal tax rate that is levied on the resident for the current income year is

45%.

Answer D:

Car or motorcycle cannot be considered exempted from capital gains tax because they

are treated as the personal use asset under “sec-108-20, ITAA 1997” that is principally kept

or used by taxpayers for their own private use purpose3.

Answer E:

The “CGT event C1” given under the “subsection 104-20 (1), ITAA 1997” happens

when the CGT asset owned by an individual is destroyed or lost4. The time of “CGT event

1 Taxation Ruling TR 2019/01

2 The Income Tax Assessment Act 1997 (Cth), Div 30

3 The Income Tax Assessment Act 1997 (Cth), s.108.20

4 The Income Tax Assessment Act 1997 (Cth), s. 104.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

C1” commences when an individual first accepts the compensation for the loss or damage or

if they are not recompensed when the destruction happened or the loss is discovered.

Answer F:

The present tax-free threshold limit for the Australian resident individual stands $18,200.

Answer G:

The judgement made in “Hayes v FCT (1956) 11 ATD 68” explains that an account

had received a substantial amount of gift as shares in the public corporation from his former

employer who had established the company5. An unpaid service was rendered by the

accountant to his previous employer on the casual basis and also rendered some small unpaid

services. A genuine friendship existed between the families of the two parties. The federal

court concluded that the gift cannot be treated as earnings because it was not allied to any

revenue generating activities and the private relation among them was simply the occasion of

gift.

The case is considered significant because even though the donor might intend to

make a gift their motive is hardly decisive6. Even though the donor may have the intention of

making a gift but their motive is hardly considered decisive. Most importantly, gifts that are

unsolicited cannot be viewed as income in the hands or recipient just because it is prompted

by the gratitude for the services while it requires considerations of the other factors as well.

Therefore, this results in less likely consequences of the taxability of voluntary receipts.

Answer H:

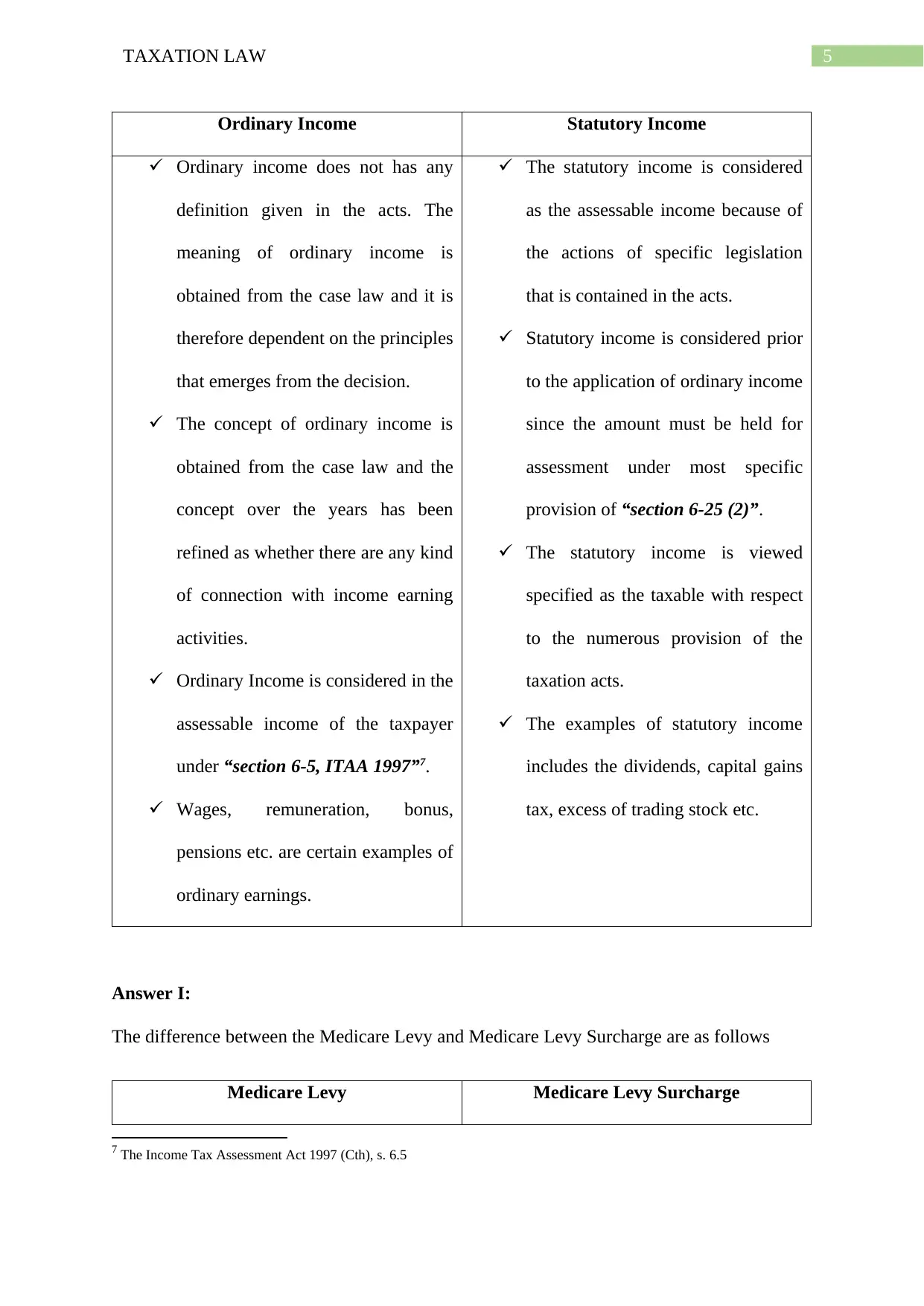

The difference between ordinary and statutory income is given below;

5 Hayes v F.C. of T (1956) 96 CLR 47

6 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

C1” commences when an individual first accepts the compensation for the loss or damage or

if they are not recompensed when the destruction happened or the loss is discovered.

Answer F:

The present tax-free threshold limit for the Australian resident individual stands $18,200.

Answer G:

The judgement made in “Hayes v FCT (1956) 11 ATD 68” explains that an account

had received a substantial amount of gift as shares in the public corporation from his former

employer who had established the company5. An unpaid service was rendered by the

accountant to his previous employer on the casual basis and also rendered some small unpaid

services. A genuine friendship existed between the families of the two parties. The federal

court concluded that the gift cannot be treated as earnings because it was not allied to any

revenue generating activities and the private relation among them was simply the occasion of

gift.

The case is considered significant because even though the donor might intend to

make a gift their motive is hardly decisive6. Even though the donor may have the intention of

making a gift but their motive is hardly considered decisive. Most importantly, gifts that are

unsolicited cannot be viewed as income in the hands or recipient just because it is prompted

by the gratitude for the services while it requires considerations of the other factors as well.

Therefore, this results in less likely consequences of the taxability of voluntary receipts.

Answer H:

The difference between ordinary and statutory income is given below;

5 Hayes v F.C. of T (1956) 96 CLR 47

6 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

5TAXATION LAW

Ordinary Income Statutory Income

Ordinary income does not has any

definition given in the acts. The

meaning of ordinary income is

obtained from the case law and it is

therefore dependent on the principles

that emerges from the decision.

The concept of ordinary income is

obtained from the case law and the

concept over the years has been

refined as whether there are any kind

of connection with income earning

activities.

Ordinary Income is considered in the

assessable income of the taxpayer

under “section 6-5, ITAA 1997”7.

Wages, remuneration, bonus,

pensions etc. are certain examples of

ordinary earnings.

The statutory income is considered

as the assessable income because of

the actions of specific legislation

that is contained in the acts.

Statutory income is considered prior

to the application of ordinary income

since the amount must be held for

assessment under most specific

provision of “section 6-25 (2)”.

The statutory income is viewed

specified as the taxable with respect

to the numerous provision of the

taxation acts.

The examples of statutory income

includes the dividends, capital gains

tax, excess of trading stock etc.

Answer I:

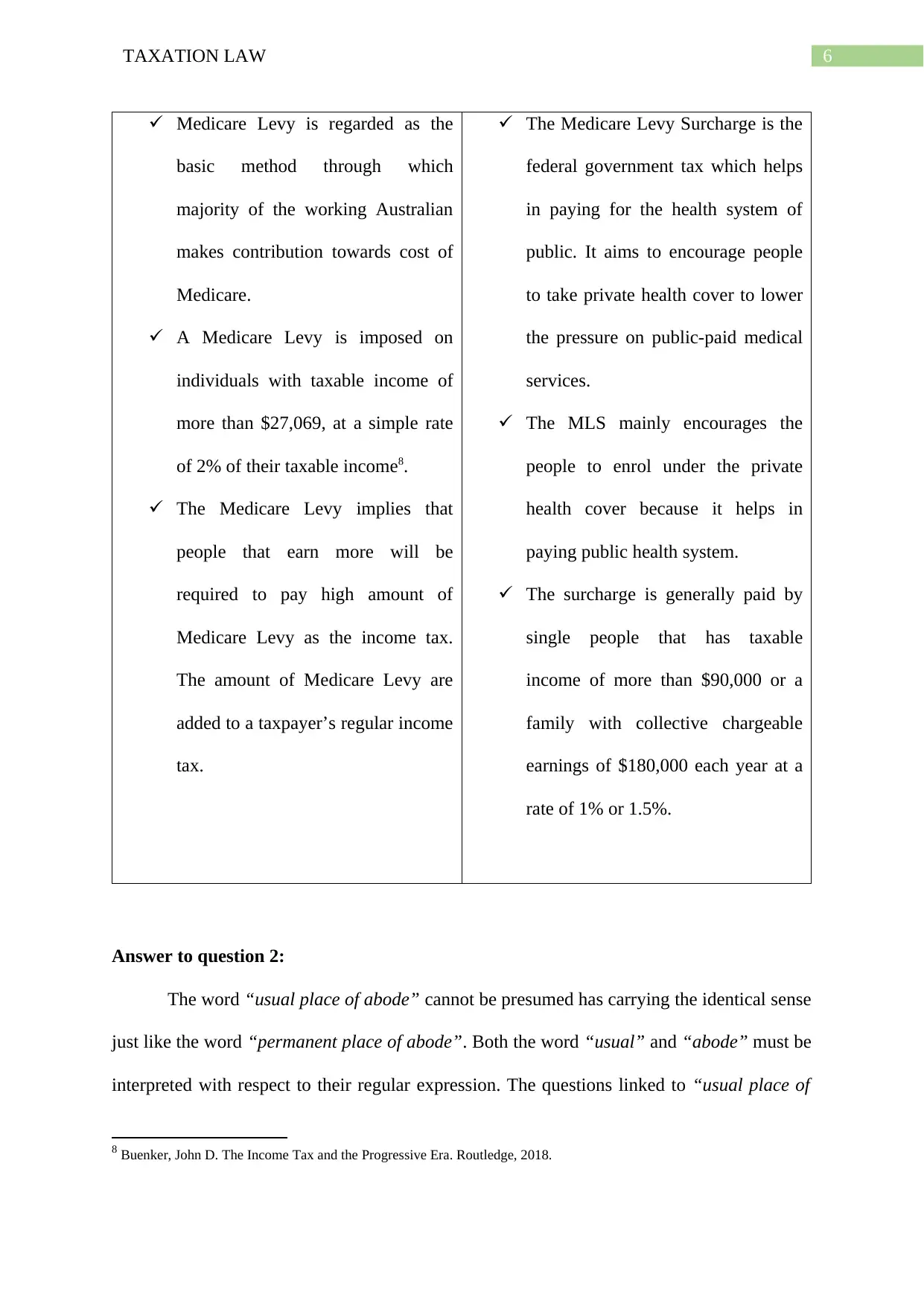

The difference between the Medicare Levy and Medicare Levy Surcharge are as follows

Medicare Levy Medicare Levy Surcharge

7 The Income Tax Assessment Act 1997 (Cth), s. 6.5

Ordinary Income Statutory Income

Ordinary income does not has any

definition given in the acts. The

meaning of ordinary income is

obtained from the case law and it is

therefore dependent on the principles

that emerges from the decision.

The concept of ordinary income is

obtained from the case law and the

concept over the years has been

refined as whether there are any kind

of connection with income earning

activities.

Ordinary Income is considered in the

assessable income of the taxpayer

under “section 6-5, ITAA 1997”7.

Wages, remuneration, bonus,

pensions etc. are certain examples of

ordinary earnings.

The statutory income is considered

as the assessable income because of

the actions of specific legislation

that is contained in the acts.

Statutory income is considered prior

to the application of ordinary income

since the amount must be held for

assessment under most specific

provision of “section 6-25 (2)”.

The statutory income is viewed

specified as the taxable with respect

to the numerous provision of the

taxation acts.

The examples of statutory income

includes the dividends, capital gains

tax, excess of trading stock etc.

Answer I:

The difference between the Medicare Levy and Medicare Levy Surcharge are as follows

Medicare Levy Medicare Levy Surcharge

7 The Income Tax Assessment Act 1997 (Cth), s. 6.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Medicare Levy is regarded as the

basic method through which

majority of the working Australian

makes contribution towards cost of

Medicare.

A Medicare Levy is imposed on

individuals with taxable income of

more than $27,069, at a simple rate

of 2% of their taxable income8.

The Medicare Levy implies that

people that earn more will be

required to pay high amount of

Medicare Levy as the income tax.

The amount of Medicare Levy are

added to a taxpayer’s regular income

tax.

The Medicare Levy Surcharge is the

federal government tax which helps

in paying for the health system of

public. It aims to encourage people

to take private health cover to lower

the pressure on public-paid medical

services.

The MLS mainly encourages the

people to enrol under the private

health cover because it helps in

paying public health system.

The surcharge is generally paid by

single people that has taxable

income of more than $90,000 or a

family with collective chargeable

earnings of $180,000 each year at a

rate of 1% or 1.5%.

Answer to question 2:

The word “usual place of abode” cannot be presumed has carrying the identical sense

just like the word “permanent place of abode”. Both the word “usual” and “abode” must be

interpreted with respect to their regular expression. The questions linked to “usual place of

8 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

Medicare Levy is regarded as the

basic method through which

majority of the working Australian

makes contribution towards cost of

Medicare.

A Medicare Levy is imposed on

individuals with taxable income of

more than $27,069, at a simple rate

of 2% of their taxable income8.

The Medicare Levy implies that

people that earn more will be

required to pay high amount of

Medicare Levy as the income tax.

The amount of Medicare Levy are

added to a taxpayer’s regular income

tax.

The Medicare Levy Surcharge is the

federal government tax which helps

in paying for the health system of

public. It aims to encourage people

to take private health cover to lower

the pressure on public-paid medical

services.

The MLS mainly encourages the

people to enrol under the private

health cover because it helps in

paying public health system.

The surcharge is generally paid by

single people that has taxable

income of more than $90,000 or a

family with collective chargeable

earnings of $180,000 each year at a

rate of 1% or 1.5%.

Answer to question 2:

The word “usual place of abode” cannot be presumed has carrying the identical sense

just like the word “permanent place of abode”. Both the word “usual” and “abode” must be

interpreted with respect to their regular expression. The questions linked to “usual place of

8 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

abode” is dependent on fact. Largely, the aforementioned expression is held as normal

residence or it is usually used when a person is physically existence in the country9. An

individual should have the fixed place of residence but they should also show the

characteristics of residence to live in instead of an overnight stay, weekly or periodic

accommodation of a traveller. It implies fixed association with the fixed place of dwelling

instead of those where a taxpayer has been an occupant or those having their “usual place of

abode” in Australia.

On noticing a person has the “usual place of abode” in Australia and exhibits that

they do not have any other fixed or “usual place of abode” out of the country however shifts

from one state to an additional state or constantly moves from state to another within the

country or possess any sort of relation with the specific place in foreign nation then that place

would be considered as transitory or temporary in nature10. An individual may be viewed as

having adopted another place of residence on their own choice or having the “permanent

place of abode” out of Australia.

In the meantime, the term “permanent place of abode” implies a taxpayer has a

residence in Australia. Meaning the definition of “resident” given in “subparagraph (a)(i)”

states that the taxation officer would only be satisfied when the “permanent place of abode”

of a taxpayer is not out of Australia. The meaning of the word “place of abode” implies that

the taxpayer has a house where they live and sleep with their family. The law court in

“Levene v IRC (1928)” explained that the word “place of abode” represents a person’s

dwelling or the physical surrounding where they live11.

9 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

10 Kenny, Paul, et al. Australian Tax 2016. 2016.

11 Levne v IRC (1928) AC 217

abode” is dependent on fact. Largely, the aforementioned expression is held as normal

residence or it is usually used when a person is physically existence in the country9. An

individual should have the fixed place of residence but they should also show the

characteristics of residence to live in instead of an overnight stay, weekly or periodic

accommodation of a traveller. It implies fixed association with the fixed place of dwelling

instead of those where a taxpayer has been an occupant or those having their “usual place of

abode” in Australia.

On noticing a person has the “usual place of abode” in Australia and exhibits that

they do not have any other fixed or “usual place of abode” out of the country however shifts

from one state to an additional state or constantly moves from state to another within the

country or possess any sort of relation with the specific place in foreign nation then that place

would be considered as transitory or temporary in nature10. An individual may be viewed as

having adopted another place of residence on their own choice or having the “permanent

place of abode” out of Australia.

In the meantime, the term “permanent place of abode” implies a taxpayer has a

residence in Australia. Meaning the definition of “resident” given in “subparagraph (a)(i)”

states that the taxation officer would only be satisfied when the “permanent place of abode”

of a taxpayer is not out of Australia. The meaning of the word “place of abode” implies that

the taxpayer has a house where they live and sleep with their family. The law court in

“Levene v IRC (1928)” explained that the word “place of abode” represents a person’s

dwelling or the physical surrounding where they live11.

9 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

10 Kenny, Paul, et al. Australian Tax 2016. 2016.

11 Levne v IRC (1928) AC 217

8TAXATION LAW

The law court in “FCT v Applegate (1979)” clarified that taxpayer had an Australian

residence, however he went to New Hebrides in Villa for setting up the office of his

company12. The judgement of full federal court noticed that the taxpayer had the “permanent

place of abode” outside Australia. For the relevant income year the taxpayer was considered

as non-resident.

Referring to another leading case of “FCT v Jenkins (1982)” where the taxpayer was

employed as bank officer and moved for three years to New Hebrides13. The taxpayer

eventually returned following 18 months stay and cited poor health conditions. In the

decision of Supreme Court the taxpayer had the “permanent place of abode” out of Australia

throughout the time span of his stay outside Australia even though the taxpayer did not

formed any material intention of staying in overseas for indefinite period14.

As per the “section 6 (1), ITAA 1936”, to define the citizenship position of an

individual reference to commonwealth superannuation fund test is also made. Accordingly,

an associate of the commonwealth superannuation fund who is regarded as the eligible

employee of commonwealth public servants along with the family members are treated as the

Australian tax resident. The commonwealth superannuation test is completely an objective

test.

Another reference to the case of “FCT v Harding (2019)” can be mentioned to

understand the “permanent place of abode” test. The finding of this contributes that any kind

of temporary place of lodging hardly precludes an individual of having a fixed home of

dwelling in foreign. The court emphasized that more wider interpretation of the term

12 F.C. of T. v Applegate (79 ATC 4307; (1979).

13 F.C. of T. v Jenkins 82 ATC 4098

14 LexisNexis issuing body. LexisNexis Practical Guidance : AU Tax. 2018.

The law court in “FCT v Applegate (1979)” clarified that taxpayer had an Australian

residence, however he went to New Hebrides in Villa for setting up the office of his

company12. The judgement of full federal court noticed that the taxpayer had the “permanent

place of abode” outside Australia. For the relevant income year the taxpayer was considered

as non-resident.

Referring to another leading case of “FCT v Jenkins (1982)” where the taxpayer was

employed as bank officer and moved for three years to New Hebrides13. The taxpayer

eventually returned following 18 months stay and cited poor health conditions. In the

decision of Supreme Court the taxpayer had the “permanent place of abode” out of Australia

throughout the time span of his stay outside Australia even though the taxpayer did not

formed any material intention of staying in overseas for indefinite period14.

As per the “section 6 (1), ITAA 1936”, to define the citizenship position of an

individual reference to commonwealth superannuation fund test is also made. Accordingly,

an associate of the commonwealth superannuation fund who is regarded as the eligible

employee of commonwealth public servants along with the family members are treated as the

Australian tax resident. The commonwealth superannuation test is completely an objective

test.

Another reference to the case of “FCT v Harding (2019)” can be mentioned to

understand the “permanent place of abode” test. The finding of this contributes that any kind

of temporary place of lodging hardly precludes an individual of having a fixed home of

dwelling in foreign. The court emphasized that more wider interpretation of the term

12 F.C. of T. v Applegate (79 ATC 4307; (1979).

13 F.C. of T. v Jenkins 82 ATC 4098

14 LexisNexis issuing body. LexisNexis Practical Guidance : AU Tax. 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

“permanent place of abode” should be taken into account to ascertain whether someone is

residing in a particular country on permanent basis.

As evident from the above stated case laws and legislation that an individual must not

be content given their “usual place of abode” is out of Australia. In the meantime, the first

statutory test requires a person to be satisfied given their “permanent place of abode” it

outside Australia.

Answer to question 3:

HECS-HELP: $850:

The question is regarding the self-education expenditure that are associated to an

individual work as the employee and it is incurred by the taxpayer when they do not obtain a

formal qualification from the school, college, university or any other education place15. To

obtain a self-education expense deduction, one must satisfy that the course is aimed at

improving the skill or specific knowledge needed for the present work activities. The ATO

additionally clarifies that an individual taxpayer is not allowed to claim income tax deduction

for the contributions made to the Australian Government under the HECS-HELP.

In the current situation the trainee accountant has incurred expenses of $850 for the

contribution made to HECS-HELP. Therefore, the trainee accountant is not entitled to

deduction for the contributions made to the Australian Government under the HECS-HELP.

Travel – work to university $110:

The ATO clarifies that for the purpose of self-education, a taxpayer is entitled to

income tax deduction for cost occurred in travel in either direction between the taxpayer’s

home and their place of education or from work place to the place of education. Quoting

15 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

“permanent place of abode” should be taken into account to ascertain whether someone is

residing in a particular country on permanent basis.

As evident from the above stated case laws and legislation that an individual must not

be content given their “usual place of abode” is out of Australia. In the meantime, the first

statutory test requires a person to be satisfied given their “permanent place of abode” it

outside Australia.

Answer to question 3:

HECS-HELP: $850:

The question is regarding the self-education expenditure that are associated to an

individual work as the employee and it is incurred by the taxpayer when they do not obtain a

formal qualification from the school, college, university or any other education place15. To

obtain a self-education expense deduction, one must satisfy that the course is aimed at

improving the skill or specific knowledge needed for the present work activities. The ATO

additionally clarifies that an individual taxpayer is not allowed to claim income tax deduction

for the contributions made to the Australian Government under the HECS-HELP.

In the current situation the trainee accountant has incurred expenses of $850 for the

contribution made to HECS-HELP. Therefore, the trainee accountant is not entitled to

deduction for the contributions made to the Australian Government under the HECS-HELP.

Travel – work to university $110:

The ATO clarifies that for the purpose of self-education, a taxpayer is entitled to

income tax deduction for cost occurred in travel in either direction between the taxpayer’s

home and their place of education or from work place to the place of education. Quoting

15 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

“section 8-1, ITAA 1997” a general deduction relating to travel to university from workplace

can be claimed by trainee accountant in this case as the self-education expenses is incurred in

the course of his present work activities16.

Books $200:

Self-education expenditure which is associated to the work as the employee and that

is occurred in the course of maintaining or enhancing a particular skill or knowledge needed

in the present work activities are allowable for tax deduction under the “section 8-1, ITAA

1997”. The court in “FCT v Highfield (1982)” ATC 4463 the taxpayer with the deduction

for expense incurred course fees, travel and lodging for undertaking MSC in periodontics17.

This is because the expenses were incurred in undertaking a degree which would improve the

knowledge and advance the taxpayer’s practice.

The expenses on books of $200 will be permissible for tax deduction under “section

8-1, ITAA 1997” the outgoings were experienced in undertaking a degree which would

improve the knowledge and advance the trainee accountant practice in his employment.

Childcare during her evening classes $80:

A loss or the expenses of domestic or private type is not entitled for deduction for the

reason that it does not meet any of the positive limbs and it is non-deductible under “second

negative limb” of “S8-1 (2)(b), ITAA 1997”. In “Lodge v FCT (1972)” deductions were

disallowed to clerk for childcare expenses for having her child mind while she attends her

work18. The outgoings not important in the making of taxpayer’s chargeable earnings.

16 The Income Tax Assessment Act 1997 (Cth), s. 8.1

17 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–9.

18 F.C. of T. v Lodge (1972) 128 CLR 171

“section 8-1, ITAA 1997” a general deduction relating to travel to university from workplace

can be claimed by trainee accountant in this case as the self-education expenses is incurred in

the course of his present work activities16.

Books $200:

Self-education expenditure which is associated to the work as the employee and that

is occurred in the course of maintaining or enhancing a particular skill or knowledge needed

in the present work activities are allowable for tax deduction under the “section 8-1, ITAA

1997”. The court in “FCT v Highfield (1982)” ATC 4463 the taxpayer with the deduction

for expense incurred course fees, travel and lodging for undertaking MSC in periodontics17.

This is because the expenses were incurred in undertaking a degree which would improve the

knowledge and advance the taxpayer’s practice.

The expenses on books of $200 will be permissible for tax deduction under “section

8-1, ITAA 1997” the outgoings were experienced in undertaking a degree which would

improve the knowledge and advance the trainee accountant practice in his employment.

Childcare during her evening classes $80:

A loss or the expenses of domestic or private type is not entitled for deduction for the

reason that it does not meet any of the positive limbs and it is non-deductible under “second

negative limb” of “S8-1 (2)(b), ITAA 1997”. In “Lodge v FCT (1972)” deductions were

disallowed to clerk for childcare expenses for having her child mind while she attends her

work18. The outgoings not important in the making of taxpayer’s chargeable earnings.

16 The Income Tax Assessment Act 1997 (Cth), s. 8.1

17 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–9.

18 F.C. of T. v Lodge (1972) 128 CLR 171

11TAXATION LAW

The childcare expenses of $80 incurred to attend the evening class is a domestic or

private type expenses. Citing “Lodge v FCT (1972)” the sum of $80 is not entitled for

deduction since it does not meet any of the positive limbs and it is non-deductible under

“second negative limb” of “S8-1 (2) (b), ITAA 1997”.

Repair to fridge at home $250:

As per “sec25-10, ITAA 1997” an individual taxpayer is permissible to deduction for

incidentals occurred on repairs to depreciating asset that is held or used completely for

making calculable earnings. As understood the taxpayer here occurs expenses of $250 to

repair the fridge at home. The sum of $250 will not be acceptable for deduction under

“sec25-10, ITAA 1997” because the fridge is solely used for private purpose.

Black trousers and shirt required to be worn at office $145:

As explained in “section 8-1, ITAA 1997” outlays that are occurred in the ordinary

dress for example suit etc. are not usually considered for deduction. In “Mansfield v FCT

(1996)” expenses on ordinary article of apparel was not permitted for tax deduction,

irrespective whether such outgoings is necessary to make sure that a fitting look in a specific

work or profession19.

The expenses of $145 for black trousers and shirt that is needed to be work at office is

an ordinary article of apparel. Referring “Mansfield v FCT (1996)” the sum of $145 is not

acceptable for deduction under “section 8-1, ITAA 1997”.

Legal expenses for writing up a new employment with a new employer $300:

As noted in “section 8-1, ITAA 1997” expenses or losses that are preliminary to start

of business activities is held as not in the sequence of earning chargeable earnings and not

19 Siebert, Horst. Reforming capital income taxation. Routledge, 2019.

The childcare expenses of $80 incurred to attend the evening class is a domestic or

private type expenses. Citing “Lodge v FCT (1972)” the sum of $80 is not entitled for

deduction since it does not meet any of the positive limbs and it is non-deductible under

“second negative limb” of “S8-1 (2) (b), ITAA 1997”.

Repair to fridge at home $250:

As per “sec25-10, ITAA 1997” an individual taxpayer is permissible to deduction for

incidentals occurred on repairs to depreciating asset that is held or used completely for

making calculable earnings. As understood the taxpayer here occurs expenses of $250 to

repair the fridge at home. The sum of $250 will not be acceptable for deduction under

“sec25-10, ITAA 1997” because the fridge is solely used for private purpose.

Black trousers and shirt required to be worn at office $145:

As explained in “section 8-1, ITAA 1997” outlays that are occurred in the ordinary

dress for example suit etc. are not usually considered for deduction. In “Mansfield v FCT

(1996)” expenses on ordinary article of apparel was not permitted for tax deduction,

irrespective whether such outgoings is necessary to make sure that a fitting look in a specific

work or profession19.

The expenses of $145 for black trousers and shirt that is needed to be work at office is

an ordinary article of apparel. Referring “Mansfield v FCT (1996)” the sum of $145 is not

acceptable for deduction under “section 8-1, ITAA 1997”.

Legal expenses for writing up a new employment with a new employer $300:

As noted in “section 8-1, ITAA 1997” expenses or losses that are preliminary to start

of business activities is held as not in the sequence of earning chargeable earnings and not

19 Siebert, Horst. Reforming capital income taxation. Routledge, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.