Melbourne Polytechnic BAC318 Taxation Law Assignment - Semester 2

VerifiedAdded on 2023/06/03

|5

|2150

|445

Homework Assignment

AI Summary

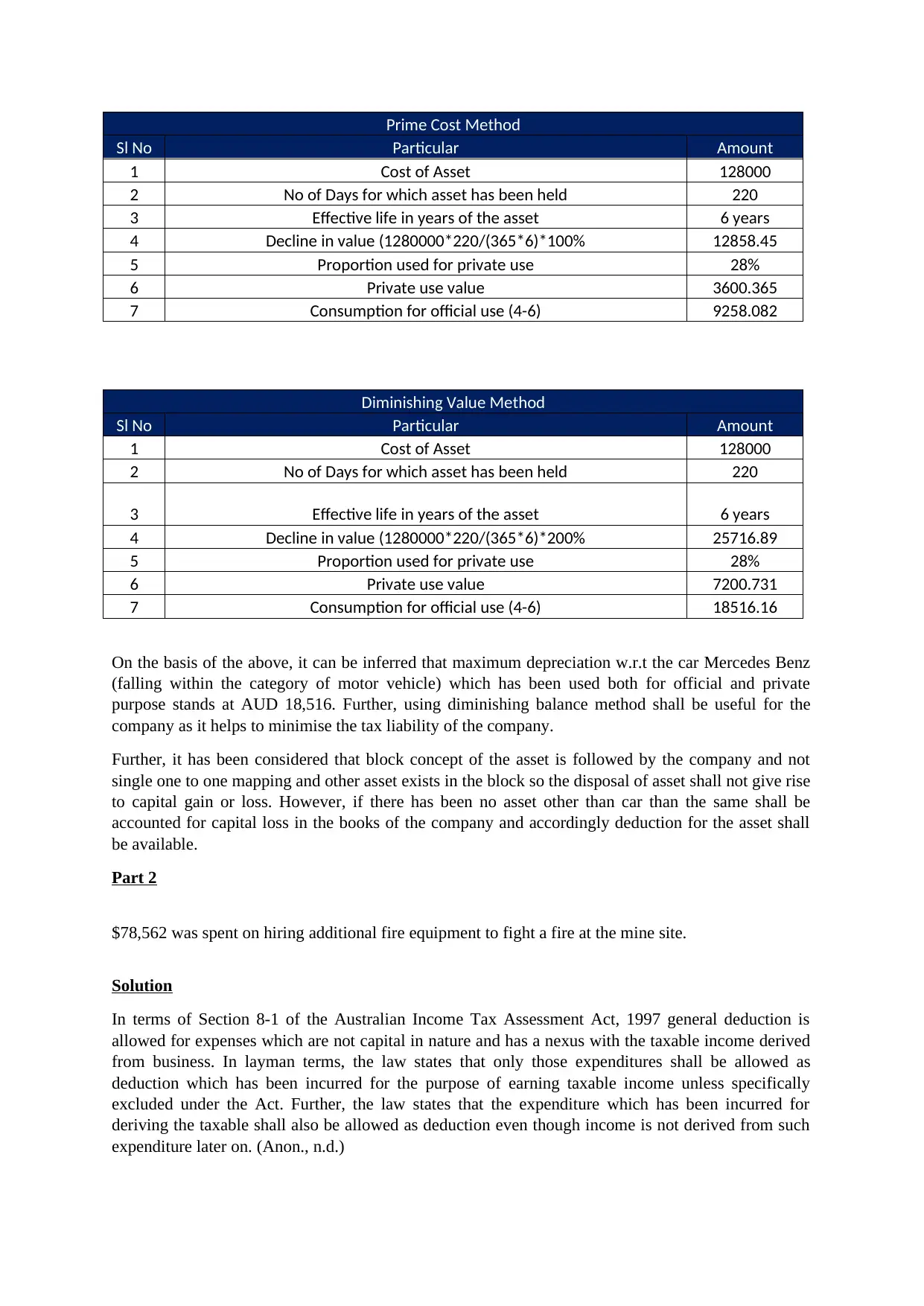

This assignment addresses several taxation law scenarios under the Australian Income Tax Assessment Act 1997. Part 1 analyzes depreciation methods (prime cost and diminishing value) for a Mercedes Benz, considering both work and private use, and calculates the depreciation amount and its implications. Part 2 assesses the deductibility of expenses for hiring fire equipment at a mine site, while Part 3 examines the deductibility of legal fees and advertising costs related to a government inquiry. Part 4 evaluates the deductibility of a provision for future liabilities from potential claims. Finally, Part 5 determines the tax implications of a donation to local community SES Fire services, all with reference to relevant sections of the Act and case law. The assignment provides detailed calculations, legal analysis, and justifications for each scenario, offering insights into tax planning and compliance.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.