Taxation Law Assignment: Income Tax, Capital Gains, and Trusts

VerifiedAdded on 2020/03/04

|10

|2500

|112

Homework Assignment

AI Summary

This Taxation Law assignment analyzes the tax implications of a livestock trading account, capital gains arising from the disposal of partnership interests, and the creation of a trust. The solution includes a livestock trading account, detailing income reconciliation, expenses, and assessable income. It then examines the application of Part IIIA of the Income Tax Assessment Act 1936 to the disposal of partnership assets, considering capital gains tax (CGT) and small business concessions. The assignment also explores the CGT consequences of establishing a trust for beneficiaries, including the role of the trustee and the taxation of net capital gains. Finally, it discusses income averaging and capital allowances for primary producers, providing insights into tax planning strategies and relevant rulings. The assignment covers various aspects of Australian taxation law, including income tax, CGT, and trust law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................6

Reference List:...........................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................6

Reference List:...........................................................................................................................8

2TAXATION LAW

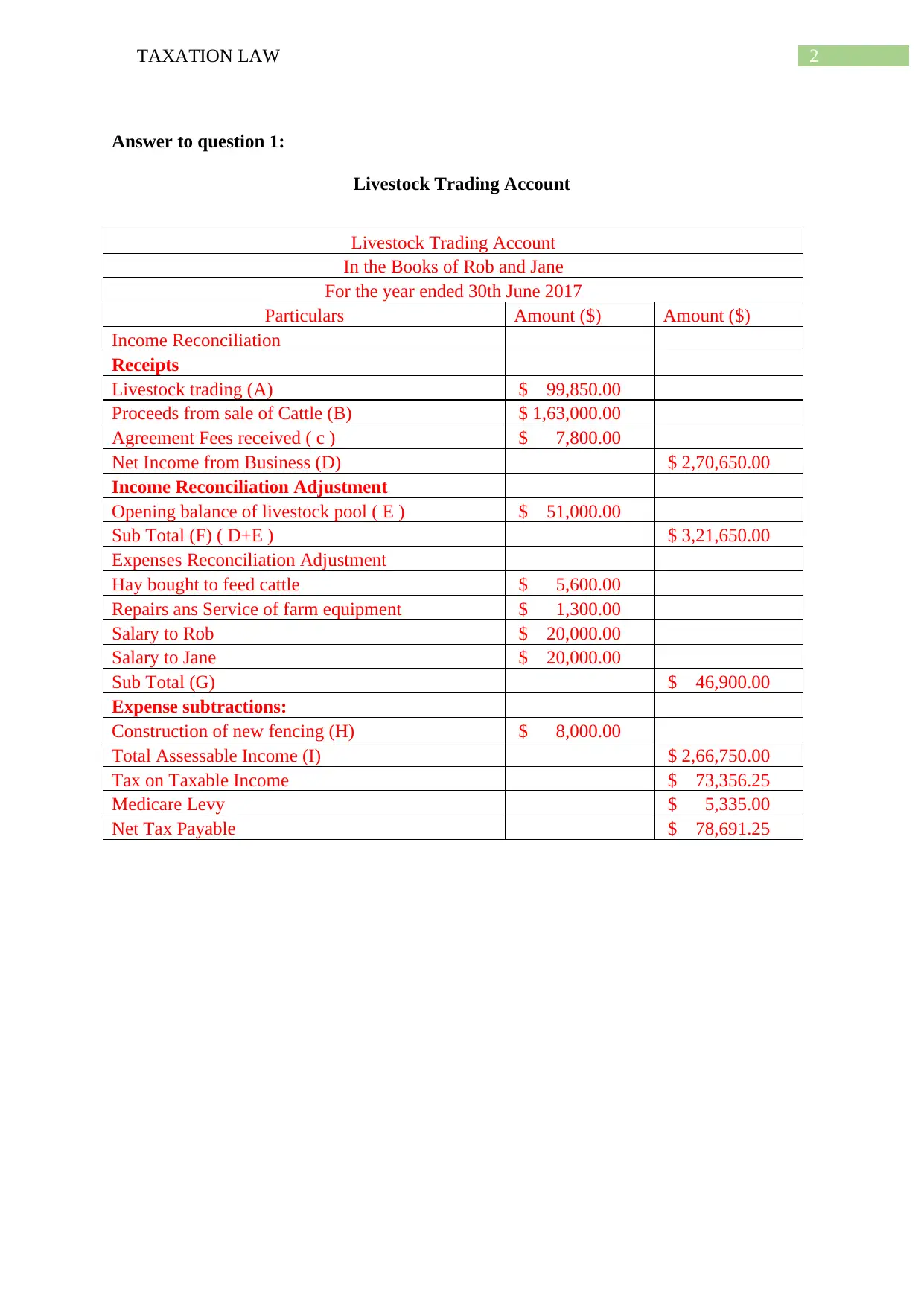

Answer to question 1:

Livestock Trading Account

Livestock Trading Account

In the Books of Rob and Jane

For the year ended 30th June 2017

Particulars Amount ($) Amount ($)

Income Reconciliation

Receipts

Livestock trading (A) $ 99,850.00

Proceeds from sale of Cattle (B) $ 1,63,000.00

Agreement Fees received ( c ) $ 7,800.00

Net Income from Business (D) $ 2,70,650.00

Income Reconciliation Adjustment

Opening balance of livestock pool ( E ) $ 51,000.00

Sub Total (F) ( D+E ) $ 3,21,650.00

Expenses Reconciliation Adjustment

Hay bought to feed cattle $ 5,600.00

Repairs ans Service of farm equipment $ 1,300.00

Salary to Rob $ 20,000.00

Salary to Jane $ 20,000.00

Sub Total (G) $ 46,900.00

Expense subtractions:

Construction of new fencing (H) $ 8,000.00

Total Assessable Income (I) $ 2,66,750.00

Tax on Taxable Income $ 73,356.25

Medicare Levy $ 5,335.00

Net Tax Payable $ 78,691.25

Answer to question 1:

Livestock Trading Account

Livestock Trading Account

In the Books of Rob and Jane

For the year ended 30th June 2017

Particulars Amount ($) Amount ($)

Income Reconciliation

Receipts

Livestock trading (A) $ 99,850.00

Proceeds from sale of Cattle (B) $ 1,63,000.00

Agreement Fees received ( c ) $ 7,800.00

Net Income from Business (D) $ 2,70,650.00

Income Reconciliation Adjustment

Opening balance of livestock pool ( E ) $ 51,000.00

Sub Total (F) ( D+E ) $ 3,21,650.00

Expenses Reconciliation Adjustment

Hay bought to feed cattle $ 5,600.00

Repairs ans Service of farm equipment $ 1,300.00

Salary to Rob $ 20,000.00

Salary to Jane $ 20,000.00

Sub Total (G) $ 46,900.00

Expense subtractions:

Construction of new fencing (H) $ 8,000.00

Total Assessable Income (I) $ 2,66,750.00

Tax on Taxable Income $ 73,356.25

Medicare Levy $ 5,335.00

Net Tax Payable $ 78,691.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 2:

Part IIIA of the Income Tax Assessment Act 1936 lays down the provision of capital

gains and losses arising from the partnerships (Pinto, 2011). In particular the taxation rulings

of TR IT 2540 lays down the provision relating to the disposal of the partnerships assets and

dealings by the partners concerning the interest that is held by them in the partnership

(Barkoczy, 2016). As evident from the following case of Rob and Jane who wants to dispose

the interest in partnership business in the upcoming year 2018. According to the viewpoint of

their business broker the partners Rob and Jane has better chances of disposing their interest

in partnership business together with their assets and trading stock for approximately $5

million.

As per the view stated in the FCT v. Everett (1980) 143 CLR 440, a partnership cannot be

considered as the separate lawful entity, which is distinct from the individual partners that

comprises of the partnership (Snape& De Souza, 2016). In spite of the partner has no kind of

specific title owned to the property by the partnershiphowever, he or she has the interest in

the partnership assets. The lawful title to the assets of the partnership remains to vest with the

partners and the agreement amid the partners might vary the terms by which lawful

ownership of the assets of the partnership is allocated between the partners.

An argument has been put forward under Part IIIA of the Income Tax Assessment

Act 1936 which is applicable to the partnership in spite of the partnership cannot own the

assets (Braithwaite, 2017). This is because the partnership is treated given that it was treated

as distinct entity for the purpose of Income Tax. Part IIIA is applicable on the Rob and Jane

since they own the equipment of business and trading stock, which they intend to sale. In

accordance with the Part IIIA any kind of capital gains or losses on the disposal of assets

accrues is incurred by the individual partners who owned the asset.

Answer to question 2:

Part IIIA of the Income Tax Assessment Act 1936 lays down the provision of capital

gains and losses arising from the partnerships (Pinto, 2011). In particular the taxation rulings

of TR IT 2540 lays down the provision relating to the disposal of the partnerships assets and

dealings by the partners concerning the interest that is held by them in the partnership

(Barkoczy, 2016). As evident from the following case of Rob and Jane who wants to dispose

the interest in partnership business in the upcoming year 2018. According to the viewpoint of

their business broker the partners Rob and Jane has better chances of disposing their interest

in partnership business together with their assets and trading stock for approximately $5

million.

As per the view stated in the FCT v. Everett (1980) 143 CLR 440, a partnership cannot be

considered as the separate lawful entity, which is distinct from the individual partners that

comprises of the partnership (Snape& De Souza, 2016). In spite of the partner has no kind of

specific title owned to the property by the partnershiphowever, he or she has the interest in

the partnership assets. The lawful title to the assets of the partnership remains to vest with the

partners and the agreement amid the partners might vary the terms by which lawful

ownership of the assets of the partnership is allocated between the partners.

An argument has been put forward under Part IIIA of the Income Tax Assessment

Act 1936 which is applicable to the partnership in spite of the partnership cannot own the

assets (Braithwaite, 2017). This is because the partnership is treated given that it was treated

as distinct entity for the purpose of Income Tax. Part IIIA is applicable on the Rob and Jane

since they own the equipment of business and trading stock, which they intend to sale. In

accordance with the Part IIIA any kind of capital gains or losses on the disposal of assets

accrues is incurred by the individual partners who owned the asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Section 160zo of the Income Tax Assessment Act 1936 requires the net capital gains

must he taken in to the considerations under the assessable income of the taxpayer (Cao et al.,

2015). In consistent with the views of Investments Pty Ltd v. FCT (1972) 128 CLR 158

disposal of business by the partner in the partnership business represents the disposal of

interest. The disposal of partnership assets generally represents the disposal of the interest of

the individual partnership assets. In order to determine any capital gain or capital loss to the

partners in relation to the Rob and Jane interest in each of the assets namely equipment and

trading stock it is obligatory to ascertain the part of the disposal proceeds that is attributable

to each of the partners interest (Saad, 2014).

The considerations that is paid or received by on the disposal of business Rob and

Jane will represent the disposal proceeds of the interest in the partnership assets. Such

disposal by Rob and Jane will be accepted under the disposal of Part IIIA of the Income Tax

Assessment Act 1936. Since the intended dealings is anticipated to take place in ordinary

commercial context therefore the capital gains arising from the disposal of assets and

business will be liable for Capital gains tax and must be included in the assessable income of

the partners.

On the other hand, it is further found that both Rob and Jane intends to downsize and

purchase two assets. They intend to use one as their investment property and the other as their

place of primary residence. According to the Taxation Determination ruling of TD 1999/67

an individual can implement the main residence exemption under the subdivision of 118-B of

the Income Tax Assessment Act 1997 whichever area of land on intends to choose where

their house is located(Ross et al., 2017). The capital gains or capital or losses, which one

makes from the land, is only disregarded under the main residence exemption if it is used for

the purpose of private or domestic association.

Section 160zo of the Income Tax Assessment Act 1936 requires the net capital gains

must he taken in to the considerations under the assessable income of the taxpayer (Cao et al.,

2015). In consistent with the views of Investments Pty Ltd v. FCT (1972) 128 CLR 158

disposal of business by the partner in the partnership business represents the disposal of

interest. The disposal of partnership assets generally represents the disposal of the interest of

the individual partnership assets. In order to determine any capital gain or capital loss to the

partners in relation to the Rob and Jane interest in each of the assets namely equipment and

trading stock it is obligatory to ascertain the part of the disposal proceeds that is attributable

to each of the partners interest (Saad, 2014).

The considerations that is paid or received by on the disposal of business Rob and

Jane will represent the disposal proceeds of the interest in the partnership assets. Such

disposal by Rob and Jane will be accepted under the disposal of Part IIIA of the Income Tax

Assessment Act 1936. Since the intended dealings is anticipated to take place in ordinary

commercial context therefore the capital gains arising from the disposal of assets and

business will be liable for Capital gains tax and must be included in the assessable income of

the partners.

On the other hand, it is further found that both Rob and Jane intends to downsize and

purchase two assets. They intend to use one as their investment property and the other as their

place of primary residence. According to the Taxation Determination ruling of TD 1999/67

an individual can implement the main residence exemption under the subdivision of 118-B of

the Income Tax Assessment Act 1997 whichever area of land on intends to choose where

their house is located(Ross et al., 2017). The capital gains or capital or losses, which one

makes from the land, is only disregarded under the main residence exemption if it is used for

the purpose of private or domestic association.

5TAXATION LAW

As evident from the following case study of Rob and Jane, they can obtain the main

residence exemption for the house, which they intend to purchase. The capital gains or losses

made by them will be disregarded under subdivision of 118-B of the Income Tax

Assessment Act 1997 (Davis et al., 2015). In addition to this, Rob and Jane can also claim a

small business capital gains tax concession for the rollover relief over the sale of active

assets. This will help Rob and Jane to defer all or a portion of their capital gain from the sale

of equipment and trading stock for two years. Since the turnover of the business is less than

$2 million the concessional rate of rollover, relief will be available at the time of disposing

the active assets.

Answer to question 3:

The taxation ruling of TR 2006/14 is concerned with the capital gains tax

consequences related to the creation of life and remained of the trust interest in the property.

The ruling is concerned with the consequences leading to the granting of the lifetime right to

reside in the property (Bevacqua, 2015). As evident from the following scenario of Rob and

Jane with the remainder of money from disposal of partnership business, they intend to set up

the trust for their two sons with Rob playing the part of the trustee.

The capital gains tax consequences are generally different from the equitable life and

those of legal life in the real property. It is noteworthy to denote that the lawful owner of the

asset held on trust for the benefit of the life interest together with the lawful person being the

representative of the deceased estate where the estate of the deceased are required to the held

on trust with the objective of providing life benefit and remainder owners (Lang, 2014). If the

trust is createdover, the original asset through the medium of declaration and settlement CGT

event under section 104-55 takes place at the time of creating the trust.

As evident from the following case study of Rob and Jane, they can obtain the main

residence exemption for the house, which they intend to purchase. The capital gains or losses

made by them will be disregarded under subdivision of 118-B of the Income Tax

Assessment Act 1997 (Davis et al., 2015). In addition to this, Rob and Jane can also claim a

small business capital gains tax concession for the rollover relief over the sale of active

assets. This will help Rob and Jane to defer all or a portion of their capital gain from the sale

of equipment and trading stock for two years. Since the turnover of the business is less than

$2 million the concessional rate of rollover, relief will be available at the time of disposing

the active assets.

Answer to question 3:

The taxation ruling of TR 2006/14 is concerned with the capital gains tax

consequences related to the creation of life and remained of the trust interest in the property.

The ruling is concerned with the consequences leading to the granting of the lifetime right to

reside in the property (Bevacqua, 2015). As evident from the following scenario of Rob and

Jane with the remainder of money from disposal of partnership business, they intend to set up

the trust for their two sons with Rob playing the part of the trustee.

The capital gains tax consequences are generally different from the equitable life and

those of legal life in the real property. It is noteworthy to denote that the lawful owner of the

asset held on trust for the benefit of the life interest together with the lawful person being the

representative of the deceased estate where the estate of the deceased are required to the held

on trust with the objective of providing life benefit and remainder owners (Lang, 2014). If the

trust is createdover, the original asset through the medium of declaration and settlement CGT

event under section 104-55 takes place at the time of creating the trust.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

A trust represents the obligations that is imposed on person for the benefit of the

beneficiaries. In the present context of Rob and Jane,the creation of trust represents a CGT

event under section 104-55 and the trustee will be held responsible for the management of the

trust’s tax affairs along with the lodging of the trust tax returns and the payment of tax

liabilities (Miller & Oats, 2016). The trustee in the present context is Rob who can make

capital gains or losses arising from the CGT event occurring to the original asset following

the commencement of being held under the trust for life interest and the their two sons. Any

form of capital gains or losses that is made by the trustee is taken into the considerations at

the time of working out the net capital gains or loss of the trustee.

The net capital gains are subjected to be included in the net income of the trust in

agreement with the subsection 95 (1) of the Income Tax Assessment Act 1936 and it is held

for tax in compliance with the subdivision of 115-C (Davison et al., 2015). As in respect of

the present scenario of Rob who is the trustee of the trust set up by him for his two sons the

net capital gains are subjected to be taken into the considerations in the net income of the

trustee. In compliance with the subsection 95 (1) of the Income Tax Assessment Act 1936the

net income will be held for taxation under subdivision of 115-C.

Answer to question 4:

Primary producers can choose to make use of the income averaging when

administering their tax affairs. Tax averaging provides the primary producers to even out

their income and tax payable over the period of maximum of five years as this allows them

for both good and poor year (Kaldor, 2014). This helps in making sure that the taxpayer does

not have pay more tax over time than the taxpayers of comparable however steady income.

Primary producers are also provided with deductions excluding the non-commercial loss with

the provision that are excluded from the computation of the basic assessable income

(Weisbach, 2016). The sum of averaging tax offset or the extra amount of income tax is

A trust represents the obligations that is imposed on person for the benefit of the

beneficiaries. In the present context of Rob and Jane,the creation of trust represents a CGT

event under section 104-55 and the trustee will be held responsible for the management of the

trust’s tax affairs along with the lodging of the trust tax returns and the payment of tax

liabilities (Miller & Oats, 2016). The trustee in the present context is Rob who can make

capital gains or losses arising from the CGT event occurring to the original asset following

the commencement of being held under the trust for life interest and the their two sons. Any

form of capital gains or losses that is made by the trustee is taken into the considerations at

the time of working out the net capital gains or loss of the trustee.

The net capital gains are subjected to be included in the net income of the trust in

agreement with the subsection 95 (1) of the Income Tax Assessment Act 1936 and it is held

for tax in compliance with the subdivision of 115-C (Davison et al., 2015). As in respect of

the present scenario of Rob who is the trustee of the trust set up by him for his two sons the

net capital gains are subjected to be taken into the considerations in the net income of the

trustee. In compliance with the subsection 95 (1) of the Income Tax Assessment Act 1936the

net income will be held for taxation under subdivision of 115-C.

Answer to question 4:

Primary producers can choose to make use of the income averaging when

administering their tax affairs. Tax averaging provides the primary producers to even out

their income and tax payable over the period of maximum of five years as this allows them

for both good and poor year (Kaldor, 2014). This helps in making sure that the taxpayer does

not have pay more tax over time than the taxpayers of comparable however steady income.

Primary producers are also provided with deductions excluding the non-commercial loss with

the provision that are excluded from the computation of the basic assessable income

(Weisbach, 2016). The sum of averaging tax offset or the extra amount of income tax is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

computed automatically and the taxpayers notice of assessment will represent the details of

the averaging.

The averaging rules takes into the considerations the rate of tax that the primary

producers would have to pay during the current year based on the basic rate of tax on their

average earnings. It is noteworthy to denote that the Medicare levy is not taken into the

considerations at the time of implementing the basic tax rate (Feld et al., 2016). The

averaging component on the other hand considers the part of the primary producers basic

income which is subjected to the average adjustment. This is usually made up of the both the

taxable primary production income and taxable non primary production income.

The primary producer has the assessable primary production income when the taxable

primary production income of the producer goes past the deductions. It is worth mentioning

that the assessable primary production income of primary producer is that part of the taxable

income, which is generated from carrying on of a primary production business. The primary

producers are also provided with the capital allowance for fodder storage assets, which is

primarily held, or the expenditure, which the primary producer incurs on the fodder storage

assets. Primary producers are provided with the opportunities of tax averaging that enables

them to even out their income and tax payables over the maximum period of five years

(Hegemann et al., 2017). This enables the taxpayers from paying more than the required

amount. When the income of primary producers is less than the deductions, the assessable

income of the primary producers is regarded as nil. Therefore, assessable income of the

primary production always forms the part of averaging elements.

computed automatically and the taxpayers notice of assessment will represent the details of

the averaging.

The averaging rules takes into the considerations the rate of tax that the primary

producers would have to pay during the current year based on the basic rate of tax on their

average earnings. It is noteworthy to denote that the Medicare levy is not taken into the

considerations at the time of implementing the basic tax rate (Feld et al., 2016). The

averaging component on the other hand considers the part of the primary producers basic

income which is subjected to the average adjustment. This is usually made up of the both the

taxable primary production income and taxable non primary production income.

The primary producer has the assessable primary production income when the taxable

primary production income of the producer goes past the deductions. It is worth mentioning

that the assessable primary production income of primary producer is that part of the taxable

income, which is generated from carrying on of a primary production business. The primary

producers are also provided with the capital allowance for fodder storage assets, which is

primarily held, or the expenditure, which the primary producer incurs on the fodder storage

assets. Primary producers are provided with the opportunities of tax averaging that enables

them to even out their income and tax payables over the maximum period of five years

(Hegemann et al., 2017). This enables the taxpayers from paying more than the required

amount. When the income of primary producers is less than the deductions, the assessable

income of the primary producers is regarded as nil. Therefore, assessable income of the

primary production always forms the part of averaging elements.

8TAXATION LAW

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bevacqua, J. (2015). ATO accountability and taxpayer fairness: An assessment of the

proposal to split the Australian taxation office. UNSWLJ, 38, 995.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ...&Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Davison, M., Monotti, A., & Wiseman, L. (2015). Australian intellectual property law.

Cambridge University Press.

Feld, L. P., Ruf, M., Schreiber, U., Todtenhaupt, M., &Voget, J. (2016). Taxing away M&A:

The effect of corporate capital gains taxes on acquisition activity.

Hegemann, A., Kunoth, A., Rupp, K., &Sureth-Sloane, C. (2017). Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), 571-

603.

Kaldor, N. (2014). Expenditure tax. Routledge.

Lang, M. (2014). Introduction to the law of double taxation conventions. LindeVerlag

GmbH.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bevacqua, J. (2015). ATO accountability and taxpayer fairness: An assessment of the

proposal to split the Australian taxation office. UNSWLJ, 38, 995.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ...&Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Davison, M., Monotti, A., & Wiseman, L. (2015). Australian intellectual property law.

Cambridge University Press.

Feld, L. P., Ruf, M., Schreiber, U., Todtenhaupt, M., &Voget, J. (2016). Taxing away M&A:

The effect of corporate capital gains taxes on acquisition activity.

Hegemann, A., Kunoth, A., Rupp, K., &Sureth-Sloane, C. (2017). Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), 571-

603.

Kaldor, N. (2014). Expenditure tax. Routledge.

Lang, M. (2014). Introduction to the law of double taxation conventions. LindeVerlag

GmbH.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Pinto, D. (2011). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Ross, M., Walker, J., & Walker, J. (2017). Multinationals targeted down under. Taxation in

Australia, 52(1), 22.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Snape, J., & De Souza, J. (2016). Environmental taxation law: policy, contexts and practice.

Routledge.

Weisbach, D. A. (2016). Capital Gains Taxation and Corporate Investment. Browser

Download This Paper.

Pinto, D. (2011). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Ross, M., Walker, J., & Walker, J. (2017). Multinationals targeted down under. Taxation in

Australia, 52(1), 22.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Snape, J., & De Souza, J. (2016). Environmental taxation law: policy, contexts and practice.

Routledge.

Weisbach, D. A. (2016). Capital Gains Taxation and Corporate Investment. Browser

Download This Paper.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.